They are cash flow negative and never generated cash. Any pointers on why?

Also their receivables are always high.

They are cash flow negative and never generated cash. Any pointers on why?

If you could click, on the (+) sign, then you would find, the real reasons. I think there is no such problems.

DISC-Invested

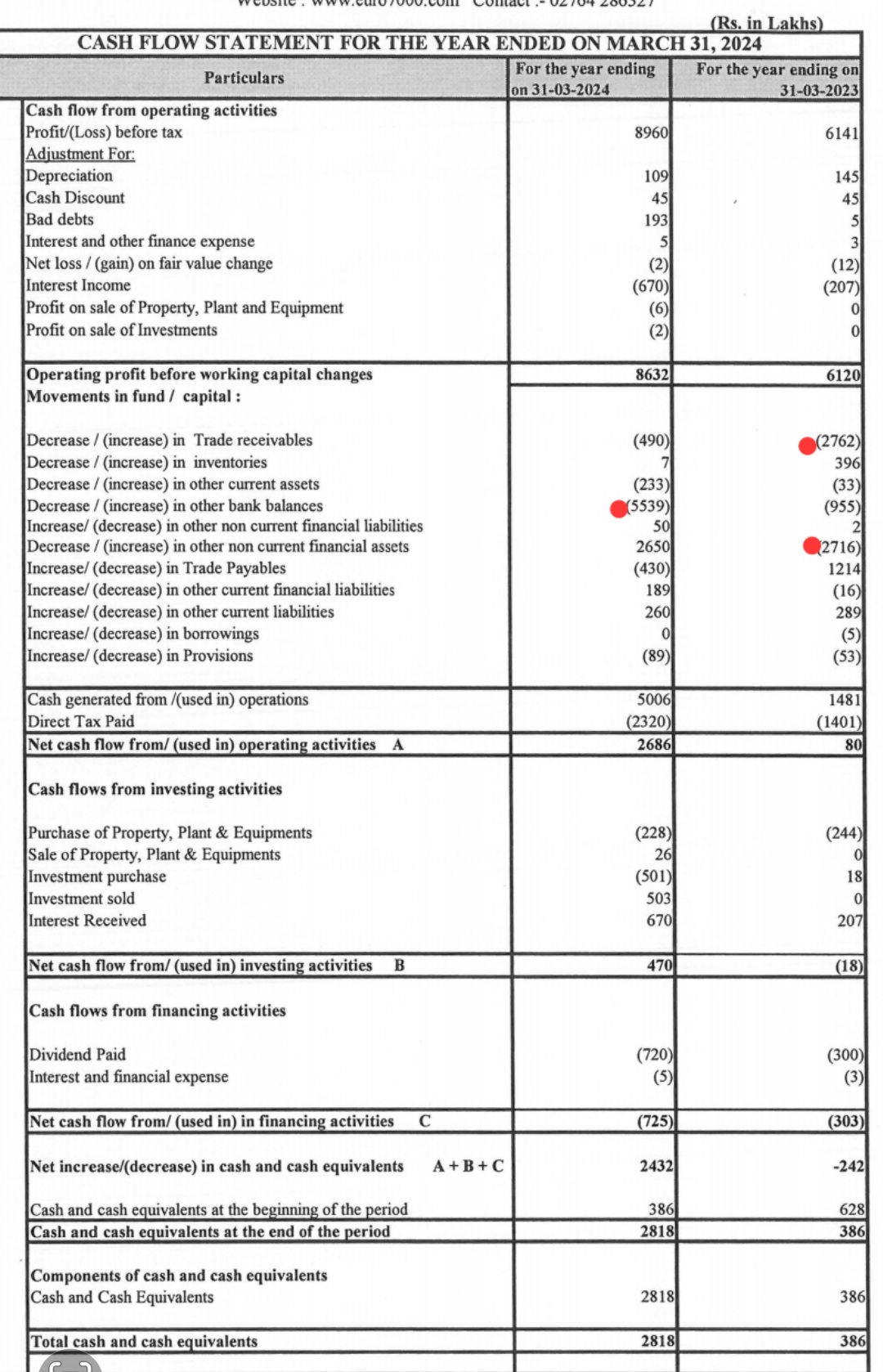

trade receivables is also increasing very rapidly. could be a red flag to monitor

Hi, this company is running a very interesting model - they own the distribution channel themselves to whom they present significantly longer working capital cycle than any building materials companies. Then secondly they give these channel partners a 10-15% of sales as discounts/benefits yet for some reason growth guidance is tepid. They somehow need cash to keep the channel happy but the channel is owned by them? Open to interpretation but capital allocation here is questionable.

Cause for concern -

They are entering into newer states and it’s obvious that to sustain they must give higher credit period and thus receivables are high.

In its Q4FY24, the company’s margin guidance was disappointing at 22-25% vs. current level of 30%+. They are venturing into newer geographies which has led to higher working capital already and looks like they may compromise on margins as they get into UP and other terrritories. Other things look promising though. The company looked confident for sales growth hereon.

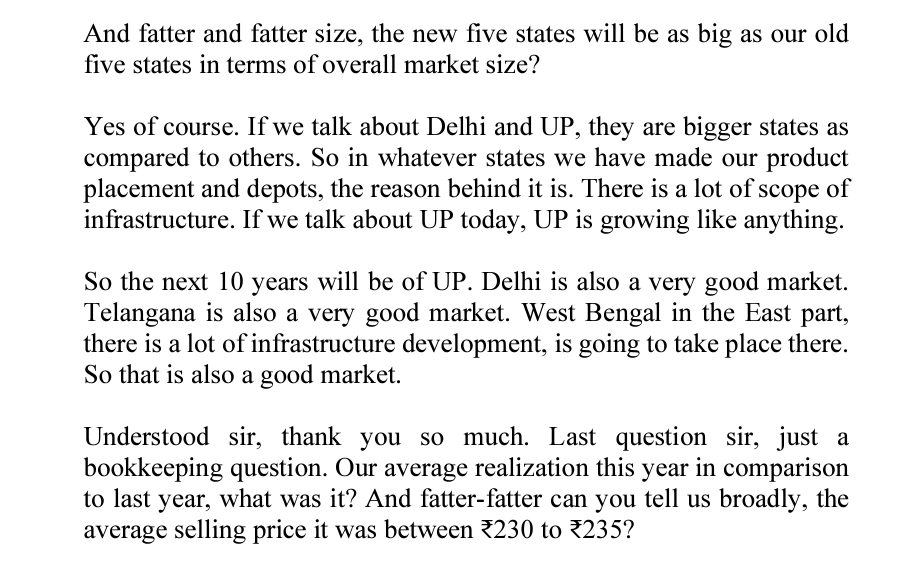

Great hilarity on the earnings transcripts.Kept wondering what is this fatter fatter they are talking about. Deduced it must be mota mota (approximate colloquially in Hindi). . Or am I missing something?

Probably, they were adressing market size in those states.

Shabdon se zyada bhavnaon ko samjhna hoga. Reading between the words rather than lines ![]()

This company has some weird policies regarding their stint with carpenters. Seems like Anway kind of thing.

Was invested but exited earlier this year.

36:50 LOST IN TRANSLATION

was wondering if it was name of a product

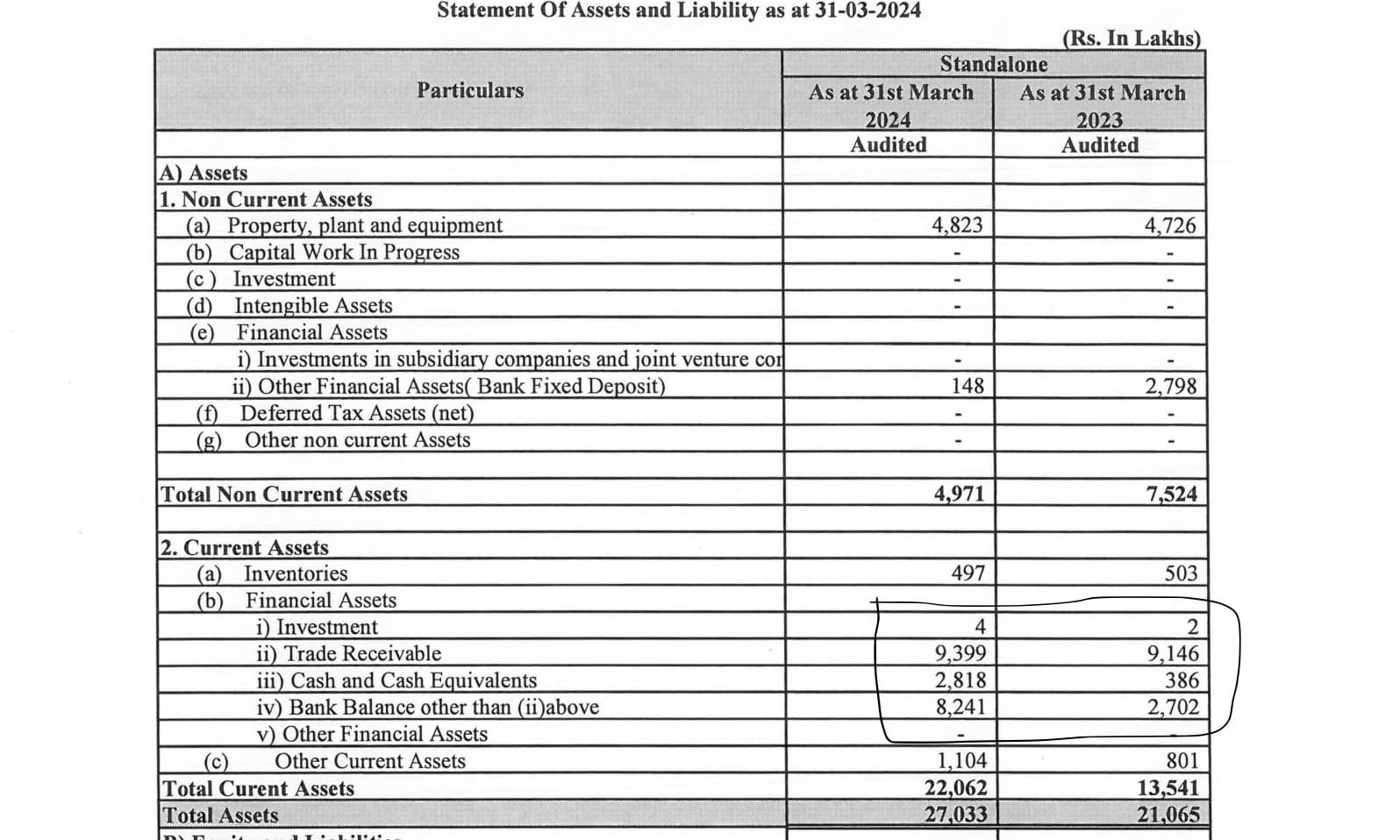

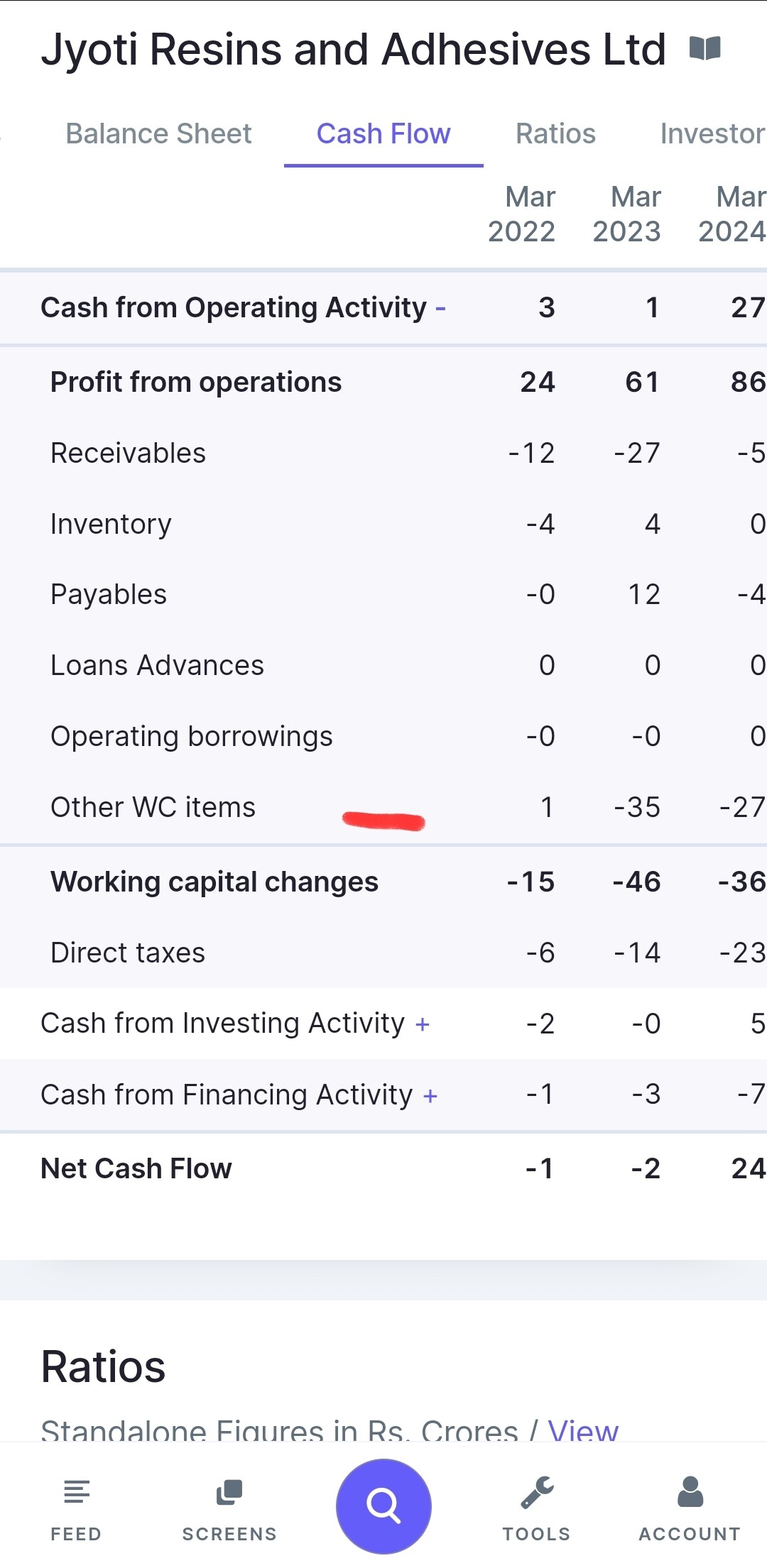

Why jyoti resins have very less CFO(cash flow from operation) as compared to PAT(net profit) ?

=Till 2021, Pat and Cfo are almost similar. However ,from 2022 onwards, cfo is very much less compared to Pat

====================

2022

Pat@20 cr

Cfo@ 3cr

=This disparity was due to high receivables(12cr)

2023

Pat@46 cr

Cfo@ 1cr

=This disparity was due to

A…High receivables(27cr) and

B…Increase/ Decrease in noncurrent financial asssets(-27cr)

2024

Pat@67 cr

Cfo@ 27 cr

=This disparity was due to Increase/decrease in other bank balance(55cr)

====================

Can anyone throw light on following two items and why these 2 are under working capital changes?

A…Increase/ Decrease in noncurrent financial asssets

B…Incerase/decrease in other bank balance

=In screener, above two items are kept under “other wc items”

Average results once again, flat QoQ,. PE will come down due to 20% YoY PAT increase. Q1 contribution has been least historically so next quarters can be expected to be better. But clearly company has been struggling at the moment to increase sales. Hopefully real-estate tailwind will help in next 2-3 years. Stock still can be considered undervalued.

disc: Invested and biased.

bhai ye kya ho raha hai is company mein guidance ko leke. guidance karte hai yoy 25 %, ata 3% hai??

Hey Bhupendra/community members , Any comments form last Con call for for next stage of top line growth. It seems they are struggling since last few quarters. The materiel cost is going down and the crude as well, which is good. However without sales growth, the price is difficult to move.

There was no con-call this quarter. The coming quarter is expected to be better both from historical perspective and also expecting the real estate up-cycle should help now. Their product only comes in picture after real estate inventory is ready to move in. So hoping some positive results but almost no top line movement from 6 qtrs mean PE might get de-rated in spite of some earning growth. It is a fantastic cash cow buisness with huge margins so it is a safe stock but management needs to give clear picture on how they are planning to bring top line up. Has really tested patience.

Jyoti resins

(My views on financial shenanigans)

There are many negatives points and accountant shenanigans raised against jyoti resins in this forum

Even in one previous post, i have also raised doubt about its cash flow. However when we go deeper, picture looks something different.

I have done few scruttlebutts from my architec and carpenter. As per them product has difinately grown in last 5 yrs.One of my relative is employee at santej plant of jyoti resins.He also told good growth story.That means growth is not fake(most probably!)

I am giving my views as per management commentry and from my few scruttlebutts.

=========================

1…Cash Flow from operation

Concern raised here is that the company has generated very low cash flow in the past 10 years.

Ans:

A…Company has posted reconcillation slide in its june 2024 investor presentation

Post Reconcillation, we can see good operating cash flow in f.y 2023 and f.y 2024

=After reconcillation, OCF changed from 1 cr to 37 cr(in 2023) and

26cr to 82 cr(in 2024)

B…A closer review of the Cash Flow Statement reveals that the company has been investing its earnings heavily into working capital and that is main strtegy of company for its growth.

As company does not require to invest heavily in fix assets and it is zero debt company, it invest that money in working capital.

=========================

2… High Receivables

Querry:

Other problem is of higher receivables.

Ans:

As per Utkarsh Patel: I believe that is our strength.We are comfortable with that debtor days, but the reason if we want to penetrate the market, we have to give comfort to the retailers .

=As we have mature states as an example Gujarat, Rajasthan, MP. These states already have a good response to our product, and we have penetrated well and also become profitable. So here our terms and conditions are 75 to 80 days

=We have started penetrating UP and Delhi we launched this last year. So that is a newer market for us. So we cannot do any terms and conditions, because my product is not familiar. There is no strong consumption there. So our goal is that the existing dealers in UP and Delhi how to place the

material of the Euro.

How to promote our product there, so in that condition we cannot ask

for the payment terms and conditions. Our priority, is to focus more to

grab the market first. So how can we take the market share? So there our credit period increases.

When we compare receivables with sales , there is defintely improvement over last 10 yrs

(Although jyoti has higher receivables as compare to industry peers)

Receivables % of sales is better indicator

Receivable% sales

2013@70%

2015@57%

2017@90%

2019@78%

2021@51%

2022@52%

2023@35%

2024@36%

Receivable days

2013@245 days

2017@333 days

2019@288 days

2021@188 days

2022@129 days

2023@128 days

2024@133 days

=========================

3…Company has created unpaid expenses reserves on liabilities side in their balance sheet.

=Liabilities have grown from 1.45cr in FY14 to 46.7cr in FY18 . It is 95 cr by 2024

=It’s steep jump in unpaid expenses

Ans:

=These unpaid expenses on liability side represent incentives to carpenter.

Company has repetatedly told about incentives .This has always been in ₹80 crores to ₹90 crores range against that we have cash and cash equivalents of around ₹112 crores.

=The company has an efficient carpenter reward model system which is a loyalty program for

carpenters. On every bucket / drums purchased by carpenters, their receive certain amount of points,

which are then recorded by downloading and logging into the app designed by the company. Post a

certain threshold, the carpenters can then redeem these points in return for gifts in several forms.

=As and when the carpenter will redeem the points, right. This

liability goes down. And against whatever he redeems, he gets given

the gift against that the cash goes down proportionately. And whenever

there is any new point created, this liability goes up.

=========================

4…Gross block

=There was sharp rise in gross block from 1 Crs. in 2017 to 40 Crs (a 40x climb in less than 5 years)

=Their increase in Fixed assets was predominantly based on reevaluation of land and not much purchases.

Ans:

=Passing the revaluation reserve entry through cash flow was an error which has been corrected later.

=========================

5…Raw material cost

=One querry raised in valuepicker was about raw material cost and i found answer from valuepicker only

=Their raw material cost has just went down from 60%+ to less than 30%. This just doesn’t make sense.

Ans:

= It is an industry wide phenomena. Look at the quarterly material cost of Pidilite, HP Adhesives etc. and you will see a declining trend. Since Pidilite is well diversified, the trend is not as deep as it is in case of Jyoti Resins.

=Someone on value picker has checked the price history .

The price has dropped from a peak of Rs.194/Kg in July 2022 to current levels of Rs.68/Kg which is a 65% drop. Hence a 50% drop in material cost is in line with this data.

=========================

6…Stock manipulation

A= 1997-98, SEBI investigated the unnatural increase in the price of Jyoti Resins and concluded that it was indeed a case of price rigging:

=The SEBI concluded that the share price of the company was manipulated and the main promoter of the company in collusion did the manipulation with an operator

B=In 2003, there was once again a case: Sebi vs Jyoti Resins & Adhesives Ltd. on 10 April, 2003

=Investigations by SEBI prima facie revealed that Shri Devendra Kantilal Dalal in connivance with the promoters of JRAL heavily dealt in the scrip to manipulate the price of the scrip.

C…In 2015-16 once again, the price was supposedly rigged. Related MoneyLife article

=========================

7…Auditor resign

Up until FY17, Statutory Auditors were Raman M. Jain & Co. Per Annual Report for FY17, Raman M. Jain & Co. “expressed their unwillingness to hold office from the conclusion of this Annual General Meeting till the conclusion of next Annual General Meeting”.

=========================

Disc…Invested since last 4 months