Unfortunately, this is not Catherine Wood’s Hedge Fund. This one is a $300-400mn Hedge Fund managed by Seven Canyon Advisors (SCA). Per filings, SCA, which believes in ''True Small-Cap Investing" as marketed on its webpage also held HDFC Bank ADR.

6 Likes

Jyoti Resins and Adhesives Limited (JRAL) came up on my 10 year 100x multibagger screen on screener.in. It has done remarkably well on most metrics - profit growth, capital efficiency, margin expansion, low leverage. Q3-FY21 results were an absolute stunner and I got up early today, brewed some coffee and made first impression notes. This company is incredible, I wanted to share. Maybe an addendum later.

• Per the recent Investor Presentation (Slide 13 here), “The company imports raw materials from several countries”. However, Note 35 on page 92 of the Annual Report (FY20-21) discloses “Value of imports calculated on CIF basis” as Nil.

• Up until FY17, Statutory Auditors were Raman M. Jain & Co. Per Annual Report for FY17, Raman M. Jain & Co. “expressed their unwillingness to hold office from the conclusion of this Annual General Meeting till the conclusion of next Annual General Meeting”. (Emphasis mine). Suresh R Shah & Associates were appointed as the new Statutory Auditors from FY18.

• Till FY17, Auditors Raman M. Jain & Co. in their Independent Auditor’s Report stated the Auditor’s Responsibility to be:

“An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the Financial Statements. The procedures selected depend on the Auditor’s judgment, including the assessment of the risks of material misstatement of the Financial Statements, whether due to fraud or error. In making those risk assessments, the Auditor considers internal financial control relevant to the Company’s preparation of the Financial Statements, that give a true and fair view, in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on whether the Company has in place an adequate internal financial controls system over financial reporting and the operating effectiveness of such controls. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of the accounting estimates made by the Company’s Board of Directors, as well as evaluating the overall presentation of the Financial Statements.” (Emphasis, mine).

The emphasised portion (in bold) is a safety parachute and absolves the Auditors of providing any opinion on financial misreporting by management. This is typically done in cases where Auditors and Management have a differing view on representation of accounts. The fact that they eventually resigned suggests the differences were too large to be reconcilable.

The new Auditors (Suresh R Shah & Associates) merrily skipped the emphasised (bold) portion within the Auditor’s Responsibility within their Reports. Overlooking and not expressing an opinion on financial (mis)statements might have been a feature for their retention over the past 4 years.

• Earlier Auditors (Raman M. Jain & Co.) write in each of their Audit Reports:

“In our opinion and as per the information and explanations provided to us, the Company has not entered into any long term contracts including derivative contracts, requiring provisions, under the applicable law or accounting standards, for material foreseeable losses.” (Emphasis, mine).

… while the new Auditors (Suresh R Shah & Associates) write:

“The Company has made provision, as required under the applicable law or accounting standards, for material foreseeable losses, if any, on long-term contracts including derivative contracts.” (Emphasis, mine).

It is unclear what these ‘long-term contracts’ are. It is also quite a coincidence that the change in language happened with the new Auditors.

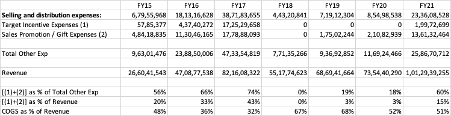

• Between F15 and FY17, incentives doled out to salespersons and distributors (Target Incentive Expenses and Sales Promotion/Gift Expense) ballooned from 20% of revenue (FY15) to 43% of revenue in FY17. To contextualise, raw material expenses as a % of revenue stood at 32% in FY17 (note that JRAL is a manufacturing company). Coinciding with the change of Auditor in FY18, FY17 P&L was restated to not include such incentives and it was netted out of revenues too. Similarly, FY18 had no disclosure of such incentives. Over FY19 and FY20, disclosure pertaining to Sales Promotion expense resumed but was very muted at 3% of revenues, but no Target Incentive Expenses. FY21 disclosed such incentives at 15% of revenue. It remains to be seen whether this is a case of underreporting or reduced incentives owing to higher brand awareness. [See Table below; FY17 numbers are before restatement]

• Provisions for (Unpaid) Expenses as reported under Current Liabilities have ballooned to INR 96.75 crore as of H1-FY22. It is not clear whether these are provisions for warranties/guarantees or for raw materials payable to suppliers. But such provisions accounted for an astonishing 71% of the total balance sheet size (excluding revaluations) for FY21. This was 6% in FY15, 24% in FY16 and grew to 55% in FY17 (the year the old Auditors resigned).

• Per the Company’s own admission to the Ministry in a letter dated April 2019, JRAL had an existing Synthetic Resin Adhesive (PVAA) capacity of 600 tons per month (TPM). In the letter, JRAL had applied for environment clearance of an additional capacity of 900 TPM. Such EC was received in July 2020. It is surprising that the latest Investor Presentation talks about existing capacity being 1000TPM (rather than 600TPM).

• Per the letter, the expansion was to be carried out on the existing land with an estimated capital cost of INR 2.80 crore. The letter stated that “No additional land will be required for the proposed expansion.” However, FY21 reports an addition of INR 15.20 crore towards purchase of land. While this purchase could be construed as an opportunistic land purchase for the envisaged capacity expansion to 2000TPM, it would take several years before the incremental 150% capacity (from 600TPM to 1500TPM) would be fully utilised. A lot can change in 4-5 years! It would be interesting to find out from whom the land was purchased ![]() .

.

• Then there are the already highlighted issues of high remuneration, three fancy cars (ostensibly for the three executive directors), etc. The Auditors have been very supportive in the enterprise, but they will conclude their term in FY22 – I believe the management would have started scouting for a friendly new auditor already. Hedge fund Ark Global Emerging Companies, LP, holds 1.25% in JRAL (per Dec-21 SHP). I was excited; unfortunately, this Ark has nothing to do with Cathy Wood’s Ark Funds ![]()

• As a fun exercise, add up the line items within the Asset side of the Balance Sheet, barring fixed assets (they do have a factory so let’s assume this to be genuine) and Other Current Assets (statutory deposits etc). Now compare this with the Provisions they have disclosed. Deduce whatever you’d like ![]()

28 Likes

@rupaniamit I see you started the thread. Are you still tracking the company? I recently started looking at it and got interested by seeing that company has become second largest brand in white glue. I wanted to know company growth trigger if company is going in other areas as well.

I live beside a carpenter’s market in a tier-3 city. All I see is the brand EURO 7000 product (60-70% of all product range) on every shelf for more than 30 - 40 shops displayed in front space ahead of Fevicol… selling like butter, at least in the west of the country in smaller cities. They call themselves the second biggest brand in wood adhesive white glue, and I don’t see any reason to defy that.

The company has recently completed the capacity expansion from 1500MTPA to 2000MTPA, and it was completed in the month of August. Currently, they are commissioning a warehouse to energize the distribution reach. They have also started focusing on building brand visibility and cash flow generation on the internal operation side. It is, in my understanding, an effort to gain the interest of big investors.

Company Guidance at present is -

“We are targeting +25-30% CAGR for Revenues over the next 3-4 years (Base Year: FY2022). Continue to maintain +30% ROE and +40% ROCE. Stay debt free and generate positive operating cash flows and free cash flows.”

As per my understanding, the Growth Triggers are not related to new product launches but mainly on account of the execution into venturing and entering new states and expanding the distribution network with increasing the market share outside the west region, especially in the north and south. Coupled with the fact that the free float is extremely less and buying from the big funds lets the stock roaring high… and I think there is a considerable buying interest at a lower level. The company has completed the issue of bonus shares in the ratio of 3:1, which I think is an effort to satisfy the request of incoming investors.

Disclaimer:- People in the above chain have raised some concerns over the management, but I found that the promoters have kept on buying shares at every level, and my entry is at a much lower level. Biased as this constitutes 20%+ of my overall allocation. Do your own diligence.

3 Likes

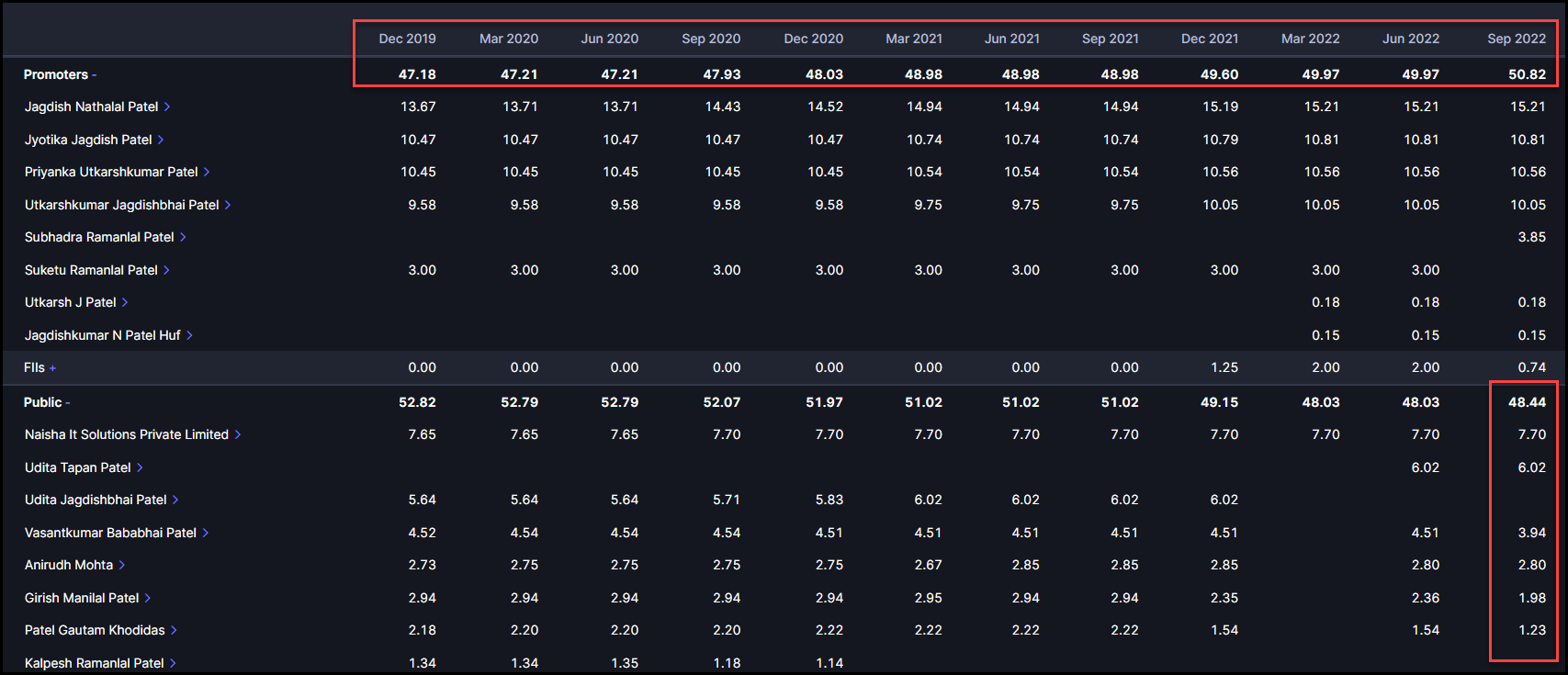

I cross-checked from BSE website Sep 2022 disclosure.

Public hold - 48.44

Promoters - 50.82

FII - 0.74

DII - Nil

therefore neither free float is low nor the stock has been bought by big funds.

It was my mistake to use the term ‘Free Float’ - This gives a completely different impression. What I wanted to highlight is that the supply of shares is very limited. To make my point, there are very few holders of the stocks to change hands with any big funds, and that is upping the game for this company. Not that I think the stock is extremely overpriced or something but the sheer supply and holders are very limited.

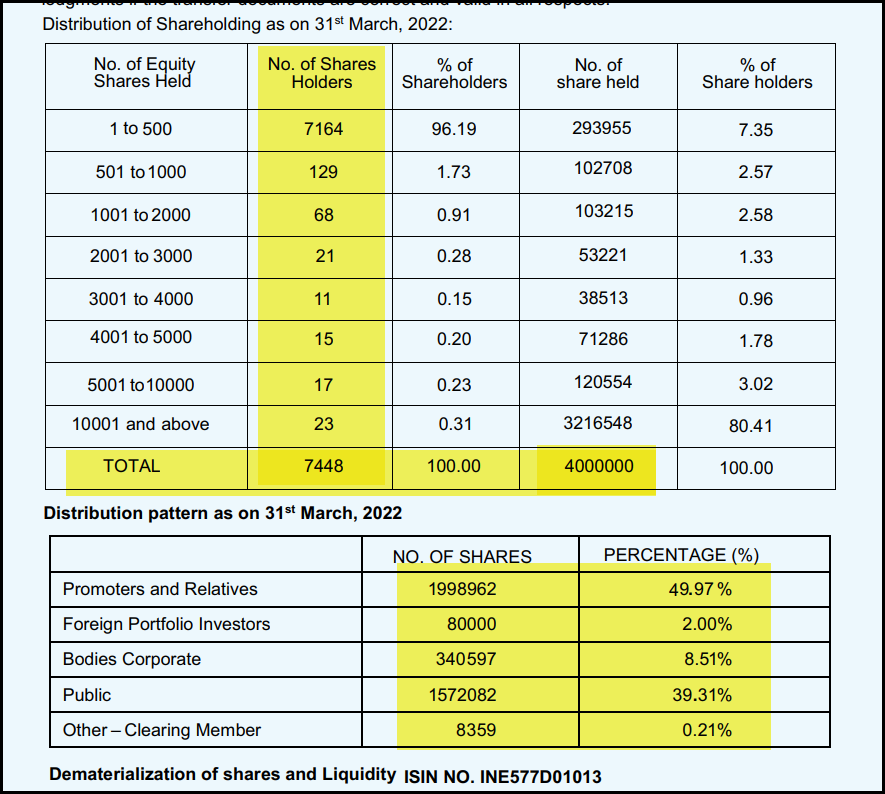

Here’s an image from 2022FY AR to highlight the same. (Note: This is before the 3:1 stock split when the total outstanding shares were only 40Lac but see the pattern of the holders, which as per my understanding, are extremely less at 7448)

It has been a bummer for institutions to enter the game, but when you check the BSE notifications, you would notice that every now and then, the company is meeting the institutional investor showing their interest, and I reckon the recent move to allot bonus shares were a move requested by these investors to encourage taking the initial position. Of course, it is a hunch, but keeping track of this company… I have a strong feeling about this… you can even refer to the trading volume to cross-validate my point. I won’t be surprised if a new share split or bonus is announced in the near future.

Disc: Invested - Core Holding.

4 Likes

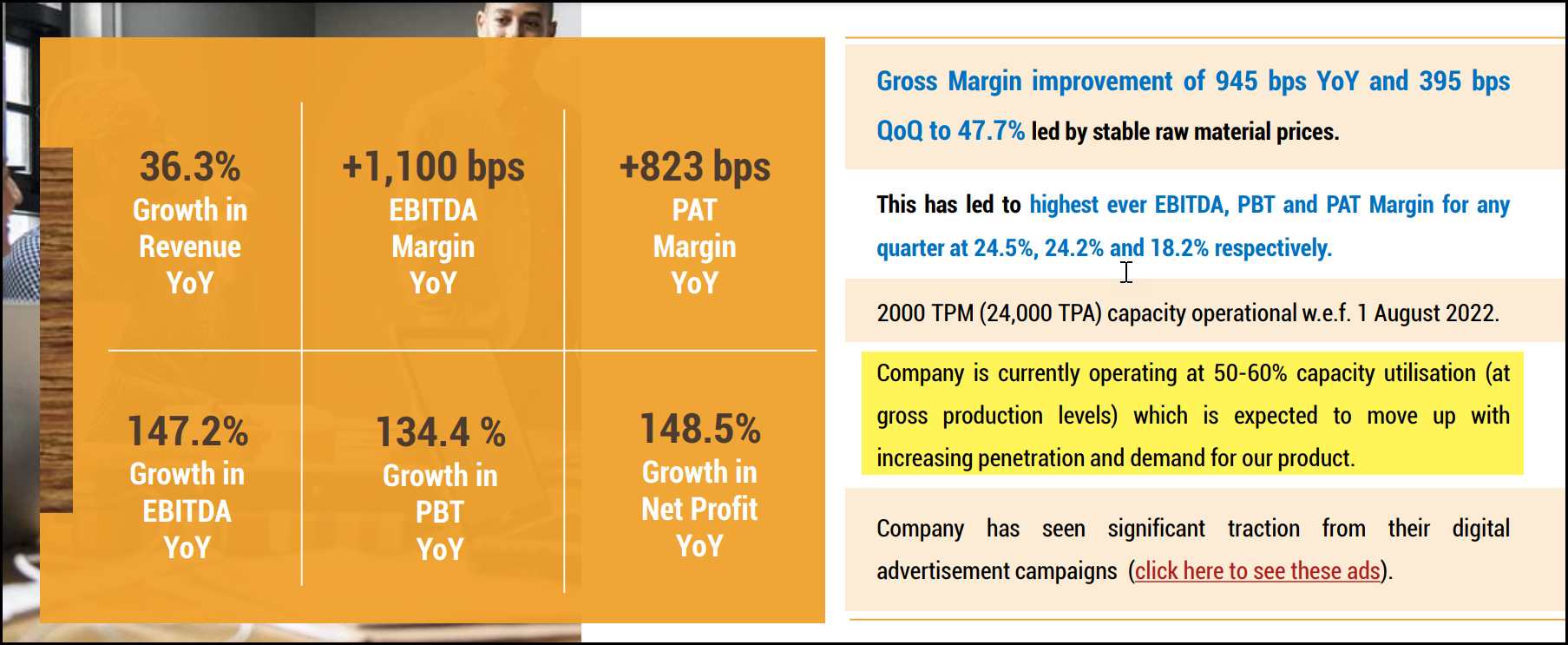

Great set of results. Although, it’s surprising to see sudden drop in Raw Material prices, it doesn’t make sense to me how within just a quarter the raw material prices have gone down sharply given historically company was sitting at already highest operating margins. Now I get that there are scopes of improvement every now and then but it’s a 1100 bps improvement. So, there must be some material change that has led to this improvement or something wrong was there earlier.

Does anyone know what their raw material is?

Is there any mention anyone has found about their expansion plans in rest of the country? Because it’s been quite a while the company is sitting in just 13 states which is less than half the country.

Disc. Invested and want to add more but not before I have the answers.

1 Like

@rupaniamit How do you see company from valuation perspective? Company has give guidance of 25-30% growth and available at MCap of 1800cr. Company seems to be getting into new states and not going into new products like what Pidilite have. It will be good to get your perspective from valuation perspective as rest looks good in the company.

In my understanding, there is a fair degree of expectations built into the price and I don’t currently trust the longevity of the margins reported in the Dec 2022 ended quarter. I strongly believe the Market will be judging the next results more on QoQ basis rather than YoY basis.

I’m assuming a sales run-rate of 280-360 Cr. for the next year with 18% EBIT margins and a safe PE of 35 (due to consumption and building product, small base - nature of business); I expect 1300 Cr. Market Cap or 1100 Rs price point to be a safe entry point for long-term investors. Coincidently, 1100-1150 is also the near-term technical support on charts. This holds true even if there are any misses on the next two-quarter results.

However, if the company is successful in maintaining 20%+ margins with decent topline growth, I expect the price to hold at the current levels or 10% + or -.

Only, with a good QoQ sales growth (12%+) and a Margin profile of above 22%, the company should be able to get past the previous highs of 1800+. That scenario may further re-rate the stock to new highs.

Disc:- Major holding from bottom levels. These are my expectations, opinions, and predictions for the price/movements for the upcoming March results.

Thanks for your comment on valuation and expected sales growth. Since you have invested from the bottom level, can you please tell how did you find company like Jyoti Resin. e.g. how did you filter this company and build your conviction to have a major holding in your portfolio.

I would start by saying that this was 6-7% of my initial capital allocation, but the sheer size of return in the last two years made it this significant in my portfolio today. I’m tempted to trim down, but I want to see how it performs in the next two quarters. You know, we give ourselves some leeway when we know that we have a sufficient margin of safety. And you start understanding compounding a bit when a stock gets this big, but yes, I still see the potential ahead.

In the second half of 2020, this counter started appearing simultaneously in my Results Blockbuster screen (Funda) + All that is Hot (Price-action) screen. I like growing, high ROCE companies with limited share, supply, and, of course, cheap valuations are the cherry on the cake. The only caveat I encountered were issues with Cash Generations and high TR in the B/S. I visited this thread and came across some audit-related concerns. But all in all, I ended up taking a small position due to some things that stood out for me across the pessimism, and I kept building my position in the next six months. One big thing which intrigued me was the claim of being the 2nd biggest company in white glue adhesive. What you are comparing now is 300Cr. MC micro-cap to the 1,20,000+ Cr. Mark Cap Pidilite, and I understand Pidilite is not just adhesive now, but still, that sheer comparison took me off guard. So I did some searching, which I highlighted in my Dec 2022 post. Here are a few other things that I find interesting:

- Ferocious buying from the promoter group across the shareholding history.

- It started with very cheap valuations and significantly fewer no. of shares O/S (40Lac - Pre Split: This is a turbo engine when everything is going hunky-dory).

- The language in the filings and disclosures started mentioning ‘Cash Generations Focus’ and ‘Brand Visibility,’ and they started delivering on that front.

- Demand:- The company declared a 500MTM expansion from 1000 to 1500 MTM and, within 6-8 months, increased it to a further 2000MTM.

- Interestingly, their Product (Euro 7000) does have a degree of brand identification, and I would say it is pretty successful in tier 2-3 cities.

- Relatively small base and consumption-related nature of business. My portfolio in that period lacked such a consumption-related counter. Specifically, what I like about this theme is that if you prove the fundamentals of the business are strong, you can command a much higher price premium than any other kind of business.

Next, the results keep getting better and better, so I am still holding it now. But I would say I’m pretty anxious about what this company has to offer currently and if I should trim the size of it. One exciting thing I noticed in the latest EP is that the capacity utilization was still 50-60%, which I thought would be upwards of 70-80%.

Disc: Invested

5 Likes

Significantly stretched receivables.

Also, I noticed that Fixed assests in current FY are same as last FY but the depreciation is now more than double. Unable to make sense of it. Am I missing something?

1 Like

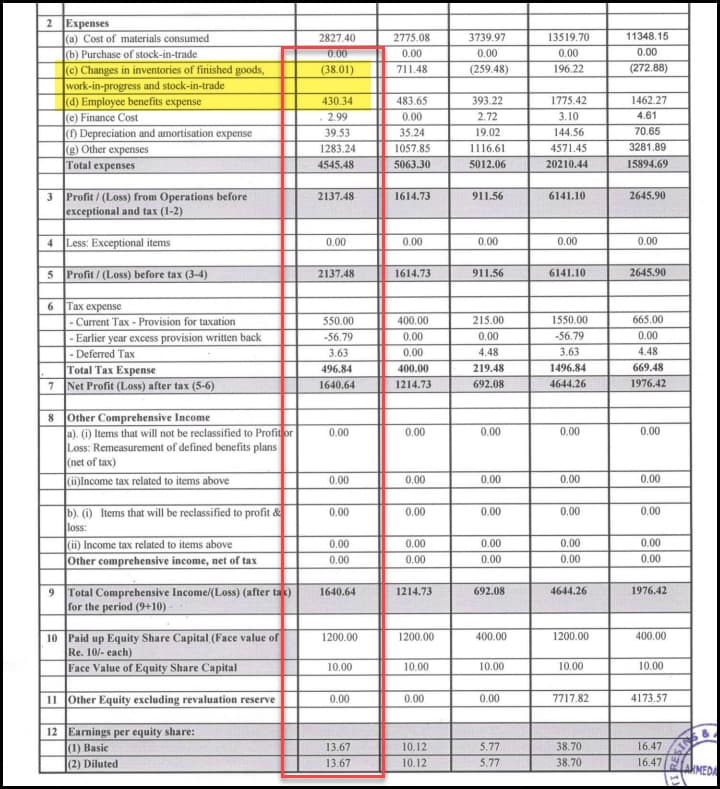

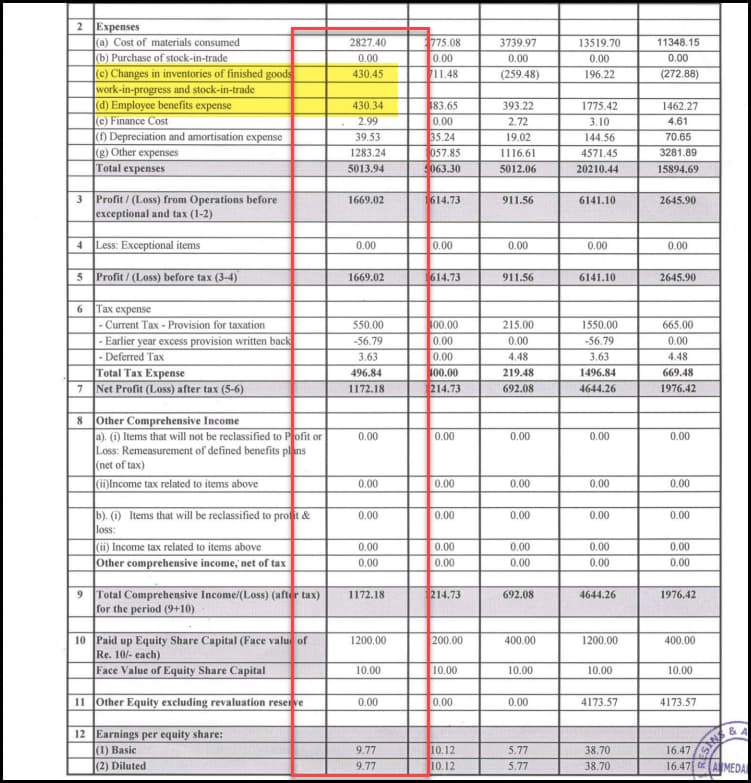

Interesting, but not sure if this a good news (increase in EPS) or bad (change in the line item value of audited results)… The company has shared revised results with some ‘changes in the finished stock of inventory’ line items…

New Results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/12815290-81d5-4f36-b0d5-3942a7adeb64.pdf

Old Results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/3df1e63e-f277-429a-a7a3-ec65d04a0808.pdf

The EPS of the latest quarter because of this change has risen from 9.77 to 13.67.

The line item is change in inventory, so I am not sure if we should read much into it as this is something constantly varying, but such changes 45 days post quarter completion, don’t know how to look at it.

The company has historically been operating on stretched receivables, in fact if you see as a percentage of total assets, it has been more or less same for the past 4-5 years, so nothing has changed there.

Depreciation as a percentage of expense is very small, so shouldn’t be a concern, but yes, wasn’t able to find the reason why it doubled.

The typo in the receivable is understandable to some degree because I believe they have mistook it with the value of ‘Employee Benefit Expense’ which is also at similar level of 4.3 Cr. something…while inputting the figure. Of course, such miscalculations is not ideal in any case.

About the depreciation, the value might be double because the capacity has increased from 1000MTPM to 2000MTPM as of August 2022.

Disc. Invested.

As per my understanding, there are too many ifs and buts now.

This was already a high risk bet for me because of the growth they’ve been showing, I had already ignorred answers to below question:

- What changes were made in the raw material that even after their topline has moved up significantly, their raw material consumption has gone down?

- Their increase in Fixed assets was predominantly based on reevaluation of land and not much purchases. So, the cash that was coming in was going somewhere else, probably in someone’s pockets

- Now, they’ve doubled the depreciation without any increase in fixed assets, doesn’t matter if they double or triple the capacity, it hasn’t come up in the books yet, so how can depreciation shoot up?

- On 24 crores of Profit, their OCF was some 2.5 crores in FY 22 and now they’ve reported 61 crores of profit and their cashflow is 1 crore only

- 27 crores have been moved to bank FD, why is it so? That’s almost a third of the profits.

And lastly, it was all on their topline growing, and in the current quarter, their’s no significant topline growth as well.

Disc. Exited

7 Likes

Jyoti Resins and Adhesives Ltd - Q4&FY23 Post Earnings Conference Call

1 Like

First Resignation comes in.

To bhai log, kharidna hai ya nahi? I never knew that Euro was a listed company. One would see the products in any hardware shop. Good brand recall… Did not know that promoters are crooks…Can we discount accounting shenanigans and bet on growth? Jivanjor is another such brand but I think they are not everywhere.

3 Likes