Crazy selling by one of the fii in ingrevia…can some senior members justify this selling…are we expecting very bad qtrly results?

Please share your inputs

6 Likes

In recent spot contracts, Acetic Acid prices have gone up ~15% / Ethyl Acetate prices by ~12%. EBITDA per tonne remains the same but with higher Acetic acid prices, margins will come down.

3 Likes

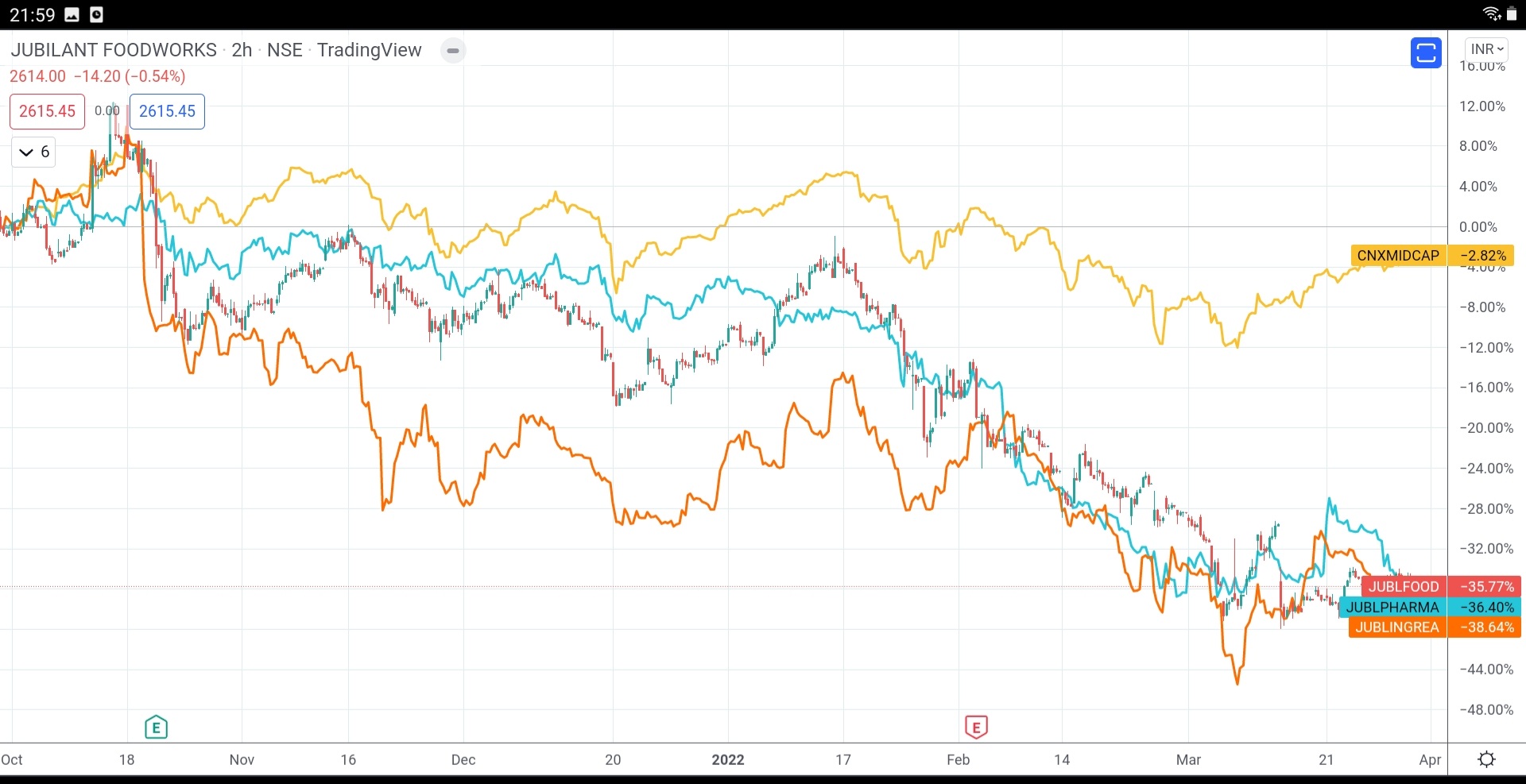

Somewhat connected aspect to Ingrevia, but more so to promoter group.

Post Oct 21, market has had its downs and has recovered mostly at Index levels. Something interesting at Bhartiya group level - all three listed companies vs midcap index

While each business is very different from each other but barring Ingrevia, other two has clear visible issues, discussed in respective threads. Ingrevia doesn’t seem to have any known issues barring some margins volatility as of now( LSC part primarily, rest of biz doing well). Given each biz has sizable float and retail holding, volatility is higher, none of them have covered lost ground.

Could this drag on Inbrevia be a temp effect due to group level narrative, believe so as of now.

Pl draw your own conclusions, this is just an observation at group peers - Invested in Ingrevia.

4 Likes

Jubilant Ingrevia Corporate Video on FY22 journey.

5 Likes

Can any senior boarders help where to find current acetic acid, ethyl acetate and anhydride prices…i want last 1 year chart for price comparison

Thanks

2 Likes

it’s available in screener premium version

Thanks its really helpful…took the paid version but still data is available till jan2022…is there anyways we can see weekly or live current prices…i want to see the avg prices for jan feb and march

Thanks

Saumil

acetic acid is there. ethyl acetate is not there. see if the prices of it’s ingredients are there, then you can make a guess

1 Like

GNFC Q4 22 results Management commentary

The performance is driven by Chemical Segment. Chemicals like Acetic Acid, WNA, A N Melt and Ethyl Acetate did quite well.

This indicates that LSC division of Jub Inv may post good Q4 numbers.

Today GNFC is having their Q4 concall @ 3.30 pm.

4 Likes

Q4FY22 ConCall Highlights:

-

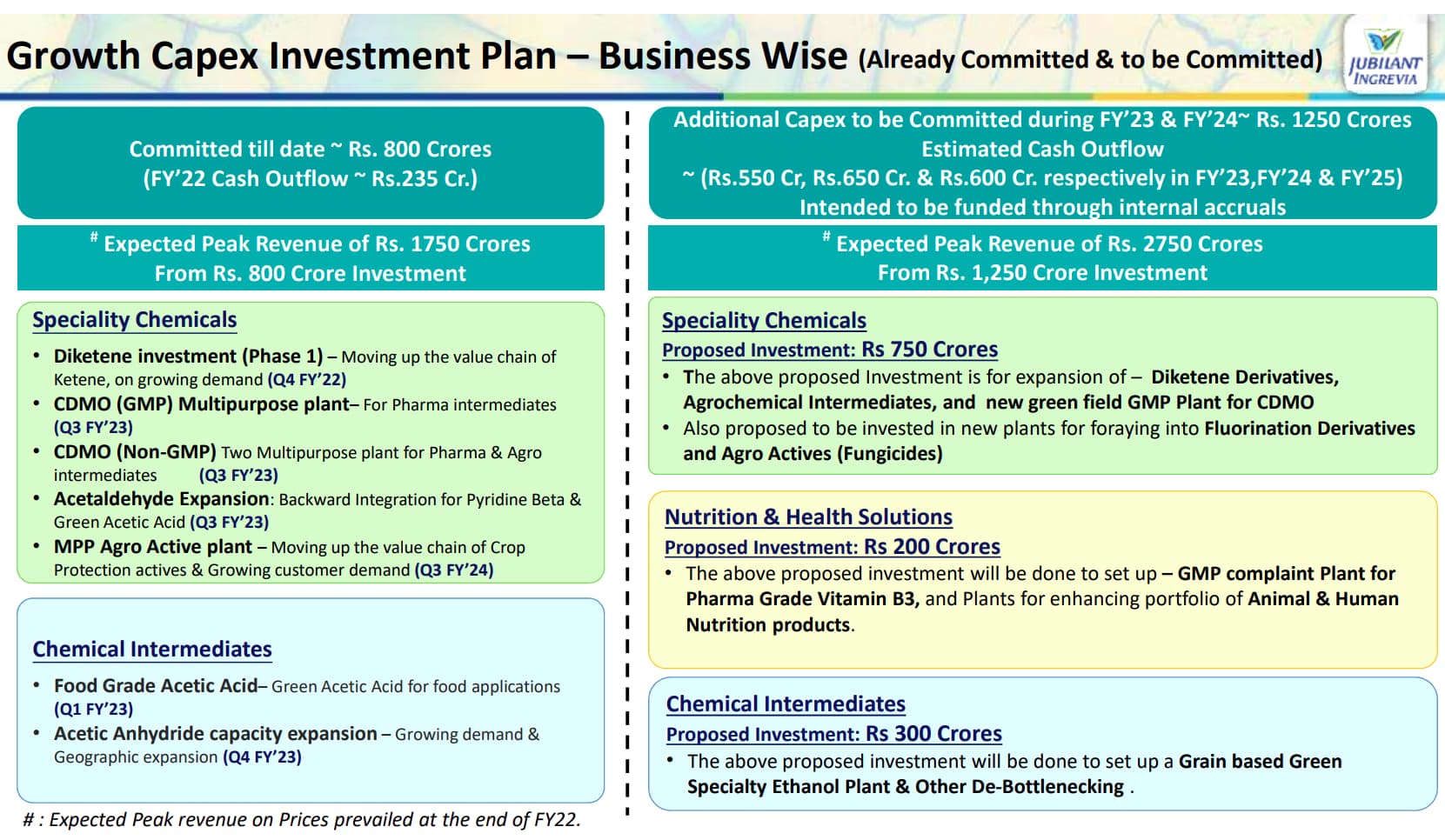

Successfully commissioned Phase 1 of Diketene and derivatives manufacturing facility at Gajraula on 15th February 2022. The capacity is about 7000 tonnes per annum (TPA)

-

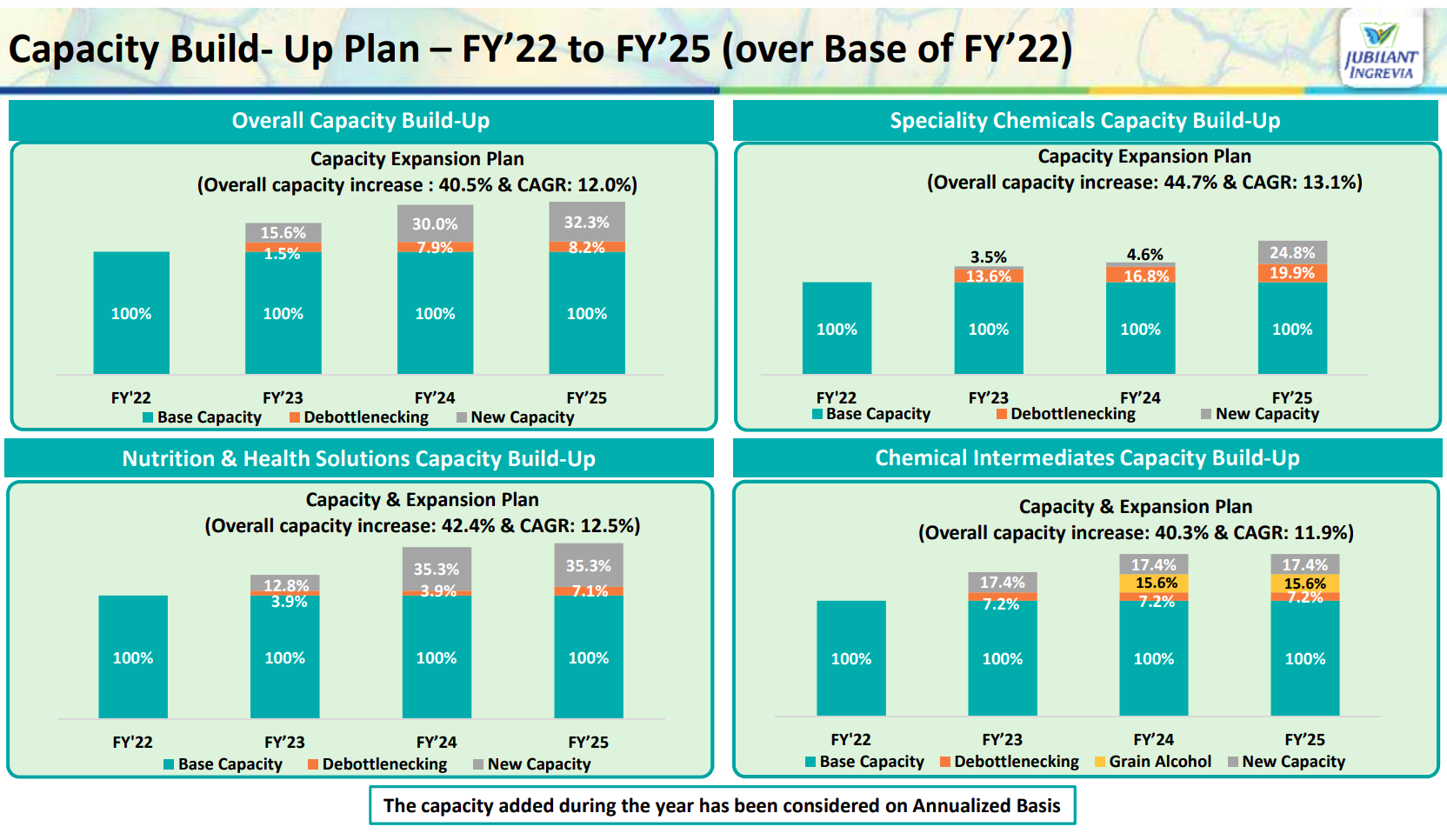

Total planned CapEx was INR 2,050 Crs - 800 Crs already spent and balance 1,250 Crs. to be committed between FY23 and FY24. Everything funded via internal accruals. All new facilities to be ready for operations by FY25

-

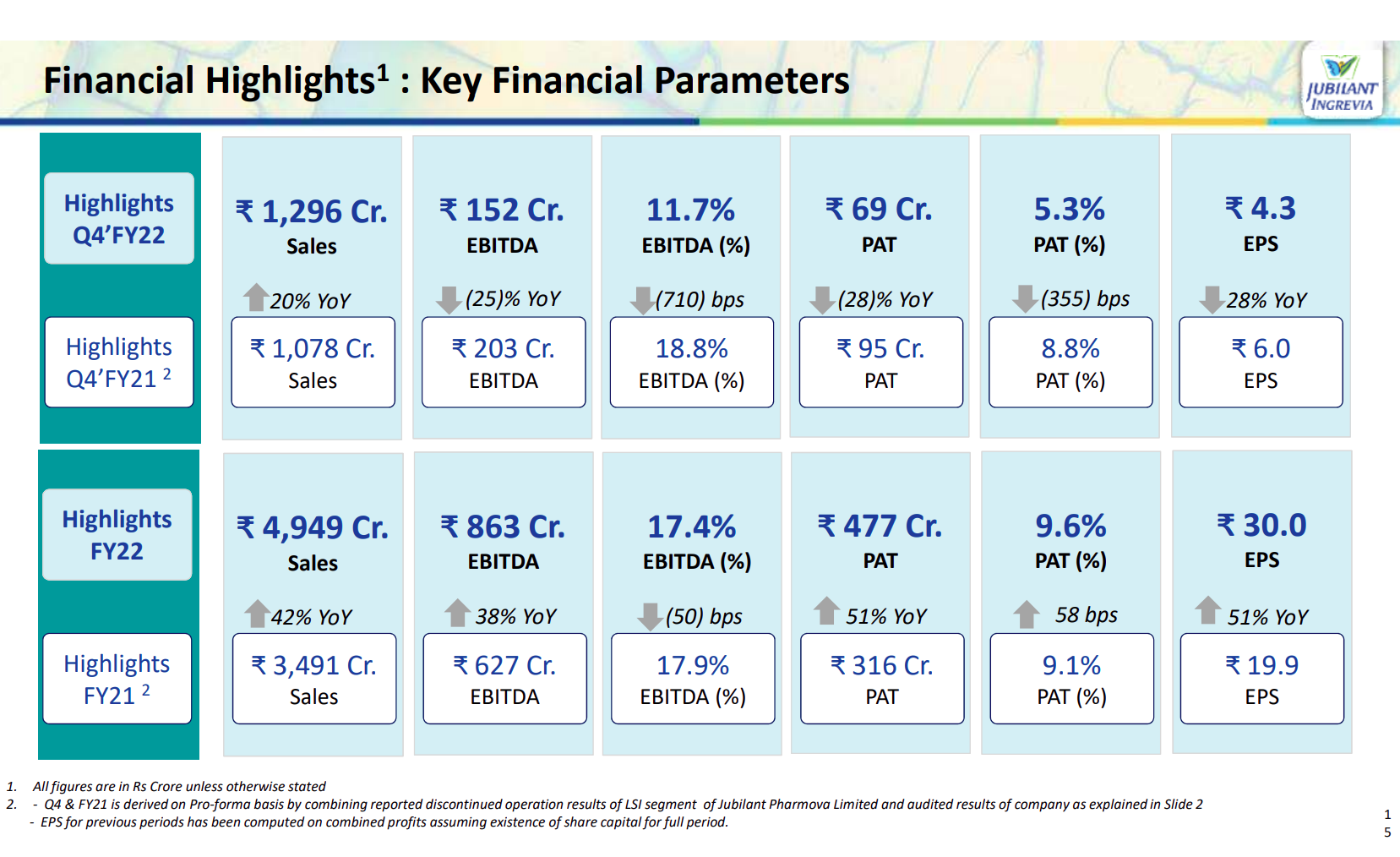

The expected peak revenue after all this expansion stands at around INR 9,500 Crs (FY22 revenues of INR 5000 Crs.) BUT along with this, the revenue share of high margin specialty and nutrition segment is expected to increase from current 46% to over 65% by FY25 end (margin are going to expand so we could expect FY25 EBITDA of around INR 1700 Crs. from INR 860 Crs. in FY22)

-

Company getting into Flourine Chemistry : “We have been working on many R&D platforms for the past 3-4 years, the fruits of which will start getting implemented now”

-

Company gradually moving towards HIGH MARGIN specialty and nutrition business

-

Diketenes have 3 major uses : Dyes and Pigments, Agro Chemical and Pharmaceutical. Jubilant will be focusing more towards agro and pharma sectors.

-

Company has NO PLANS to expand on the Acetic Acid capacity. They DONT see economic sense in it.

-

Jubilant has been able to beat even the Chinese players in the global Pyridine market!

22 Likes

The expansion into Diketene chemistry could be really a big addition to the company’s product profile. Diketenes are a major component in Paints, Dyes and Agro Chemicals. Now there are two primary ways to produce Ketenes (Diketenes are manufactured by dimerising ketenes):

-

Using Acetic Acid

-

Using Acetone.

I am really curious to know as to which route will Jubilant be taking up. Gut feeling says that they will take the Acetic Acid considering the company’s specialisation into it (Acetic Acid is one of the primary RM for the current line of production) and also the fact that the process using AA produces just Water as a by product compared to harmful Methane gases produced in the second reaction. Now if the big Diketene expansion also gets exposed to Acetic Acid price volatility (as we saw in the last two quarters), it cannot be a sustainable story going ahead.

Edit: Even Laxmi Organics produces Diketenes using Acetic Acid as can be seen in their EC report form 2014 here

I am still not able to understand that if Jubilant is so much dependent upon Acetic Acid, why not start manufacturing the same along wwith so many other backward integrations they are coming up with? Which economic sense is hindering the company from insulating its major products from price volatilities of their Raw Material costs?

Senior boarders, please help.

Disclosure: Invested in this counter.

6 Likes

The question was raised but the reasoning given was not very precise…here is the snippet from the last call…

Dhruv Bhimrajka: Sir my question is, are there any plans for us to pick up a captive acetic acid capacity? I know you have answered the question with respect to forward

agreements. So, if you can clarify on this also, please?

Rajesh Srivastava: No, we do not have a plan to make the investment on producing acetic acid for capital use, because that is not making sense. This acetic acid plant is very

specialized food grade acetic acid. So therefore, this much volume, which is currently required by market, we have entered it, but we have no plans to make investment on acetic acid further or captive consumption.

3 Likes

Yup, went through that concall and the 2 before that. Many participants have raised this doubt on expanding their Acetic Acid manufacturing but it seems the management does not see economic feasibility for the same. I am curious to really understand the complete thought of the management in arriving at this decision.

I am not a technical expert but sharing the following from my limited knowledge of the business:

Acetic Acid can be made through two routes- using either methanol or ethanol as a feedstock. In India GNFC produces Acetic Acid (AA) through methanol route. Methanol being a crude oil derivative its prices are fairly volatile and most of the time cheaper than Ethanol. As such AA made through methanol route is almost always cheaper than that made through Ethanol route. Ethanol on the other hand is also used for making potable alcohol and now for petrol blending, which are far more lucrative for a distillery. As a result producing AA using ethanol as feedstock is not always economically viable. Most Ethyl Acetate manufacturers therefore don’t prefer to produce AA in-house but outsource it.

5 Likes

The argument makes sense but Jubilant uses even Methanol as feedstock to make formaldehyde and acetaldehyde. Why not also use it to make Acetic Acid?

1 Like

I can only take an educated guess- 1. Primarily it must be a Make vs Buy decision 2. Also capex for methanol based AA plant would be quite high. eg GNFC spent 250 crs in 2002 to expand its AA capacity from 45000 tpa to 90000 tpa. In 2022 it would be far higher.

3 Likes

Hi All - would like to understand more on Jubilant Ingrevia recent downwards price movement. To my understanding the only issue i see is the margin contraction and impact of acetic acid prices volatility. Anyone happen to notice any other reason?

JUBILIANT INGREVIA.docx (161.0 KB)

14 Likes