Disappointing Numbers. Similar to what we saw with Laxmi Organics.

2 Likes

the energy cost literally killed the bottom line.

2 Likes

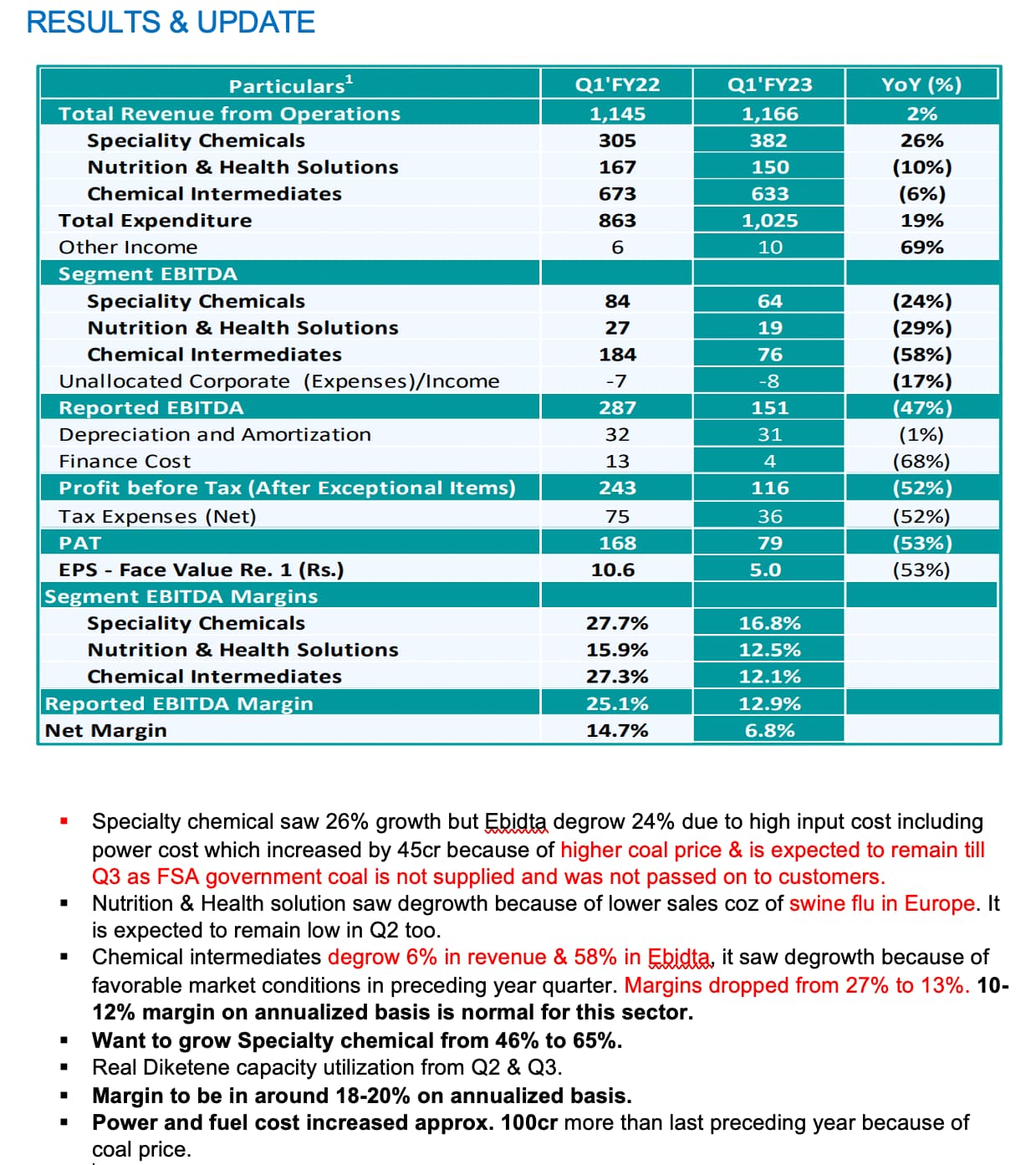

Q1 FY23:

• ENERGY COST INFLATION: Coal was not supplied by Government as per arrangement. Because of this, coal had to be imported at sky high prices. 45cr impact. From 1st of December Government supply should resume.

Raw material input cost increase passed on but unprecedented coal prices couldn’t be passed on. Expect to pass on some cost in q2.

• VOLUME GROWTH: Speciality Chemicals revenue grew by 26% YoY driven by volume growth across product segments

Chemical Intermediates volume have grown while revenue is impacted mainly due to lower prices of key RM i.e., Acetic Acid. Acetic Anhydride volumes grew by 22% on YOY basis

• QOQ DIP IN SPECIALITY CHEMICALS VOLUME:

China 2-3 months lockdown impacted some export volumes.

They had to change Catalyst in one plant (changed every 6-7 years), that impacted some production and subsequent sales of SC.

Both of the situations are now normalizing. Expect volume growth QOQ in Q2.

• Share of revenue to customers having Agro Chemical end use grew significantly.

Speciality chemicals: Serving 15 of top 20 Global Pharma & 7 of top 10 Global Agrochemical companies

• EUROPE: Big growth in sales and market share in Europe for Acetic anhydride due to new uses for anhydride

• ANIMAL NUTRITION: Sales impacted due to avian and swine flu in US and Europe. Situation said to be improving. To normalize by quarter/year end.

• Diketene plant fully stabilized. Sales to start contributing from Q2 onwards.

• All Capex plans going as per plan.

13 Likes

Annual report, felt positive after reading the MDA and other sections explaining the potential/opportunities.

Invested, biased.

6 Likes

This is a good pick only when operating leverage starts playing out Till then it is a question mark though lot of guys are bullish on this

Initiating coverage on Jubilant Ingrevia and its peer Laxmi Organics

7 Likes

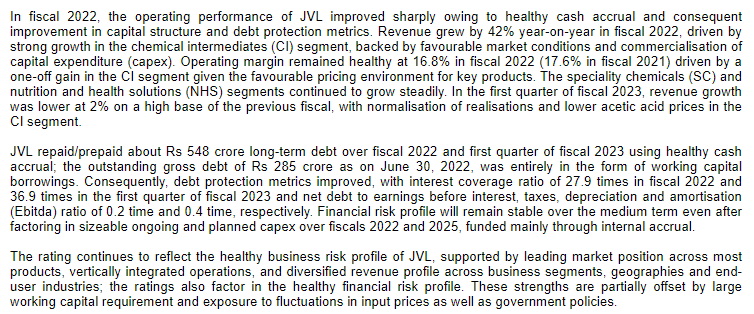

From crisil rating doc,

JVL repaid/prepaid about Rs 548 crore long-term debt over fiscal 2022 and first quarter of fiscal 2023 using healthy cash accrual; the outstanding gross debt of Rs 285 crore as on June 30, 2022, was entirely in the form of working capital borrowings

10 Likes

So Q3 results are out and they don’t look great. PAT, EBIDTA and Revenue all slumped considerably QoQ. Net profit is down 29% to Rs 92 crore on 10.16% decline in revenue from operations to Rs 1,152.63 crore in Q3 FY23 over Q3 FY22. Even YOY, overall revenue is 10% lower, mainly on account of lower sales performance of nutrition & health solution business.

The Good:

- Revenue from specialty chemicals grew by 34% YoY to Rs 468 crore and absolute EBIDTA grew by 15%, driven by higher price realization and volume growth across product segments. Share of revenue to customers having agro chemical end use has shown significant growth

- The company has further improved its market share and volumes of Acetic Anhydride in EU region on YoY.

- Committed to ongoing Growth Capex plan, which is now improved from earlier Rs 2,050 crore to now Rs 2,275 crore during FY22 to FY25 Period.

The Bad

- Revenue from nutrition business de-grew YoY by 39% to Rs 132 crore in Q3 FY23, on account of lower demand, due to prolonged impact of bird and swine flu in EU and US regions, leading to lower realization

- Revenue from chemical intermediates de-grew by 23% on YoY to Rs 559 crore in Q3 FY23, mainly driven by lower price of feed stock (ie Acetic Acid) leading to lower realization of finished products i.e. Acetic Anhydride & Ethyl Acetate

Commentary

- The demand related challenges of Vitamin B3 are short-term and we continue to remain focused towards improving our presence in food and cosmetics segment. In chemical intermediates business the revenue on YoY basis is impacted due to lower prices of feed stock (Acetic Acid), leading to lower sales prices of Acetic Anhydride and Ethyl Acetate.

- The company has firm plans to significantly reduce overall energy cost in phased manner through various initiatives by sourcing power from Grid and renewable sources, optimizing coal consumption through efficiency improvement in consumption as well as in generation

6 Likes

Seems like there have been no major quesions in concalls(still going through) related to pollution crimes committed by this business. Why isn’t this being given importance to. Is it because mgmt won’t allow those asking questions in next concall like Pharmova also does to Sajal Sir.

This is not a small risk and we have seen crackdowns done by China on chemical industry.

A sustainable view on a business is always important before entering. I won’t explain too much as Chins has done an amazing job above already.

Also, seems like one of the better threads on this forum. Has multiple viewpoints and forms a nice lifecycle thread to carefully monitor their transition.

Disc: Invested but doing small scale scuttlebutts on this front.

4 Likes

Jubilant Ingrevia Ltd acquires 37.98% stake in Mister Veg Foods Pvt Ltd | EquityBulls

Jubilant Ingrevia Limited has acquired 37.98% stake of Mister Veg Foods Private Limited, an associate company of the Company.

MVFPL is a private limited company incorporated and domiciled in India. It was incorporated on 11 September 2020 under the Companies Act 2013. The Company’s registered office is situated at Plot No 150, Sector 58, Faridabad. The Company is primarily involved in the business of food products.

3 Likes

In 2021 annual report they informed 165+ products and in 2022 the number of products reduced to 125. I was unable to find a reason or mention about it in the conference calls. It is perfectly fine to decommission some products but not giving an explanation or details will not build trust on the management. If anyone from our forum know the reason or have an opinion, please share.

My complete analysis on Jubilant Ingrevia

does not include the current quarter’s updates.

JUBILANT INGREVIA- Multiple Triggers In Place

Currently the company is not faring well, due to external factors but as and when the cycle turns it can benefit immensely in my opinion.

ABOUT

Jubilant Ingrevia, a global integrated Life Science products and Innovative Solutions provider serving, Pharmaceutical, Nutrition, Agrochemical, Consumer and Industrial customers with their customized products and solutions that are innovative, cost-effective and conforming to excellent quality standards.

Ingrevia was demerged from Jubilant Life sciences as on 01.02.2021 and company was listed on 19.03.2021.

Jubilant Ingrevia’s portfolio also extends to custom research and manufacturing for pharmaceutical and agrochemical customers on an exclusive basis.

Life science chemicals (56% of sales)

Specialty chemicals (28% of sales)

Nutrition (16% of sales)

Handles 5 Global scale Manufacturing sites with 50 plants and top 10 customers accounting for 20-25% of the overall revenue.

Expertise in 35 Technology platforms which include Acetyl, Pyridine/ Piperidine,

Ketene/ Diketene, Halogenation & others (At large commercial scale).

INDUSTRY

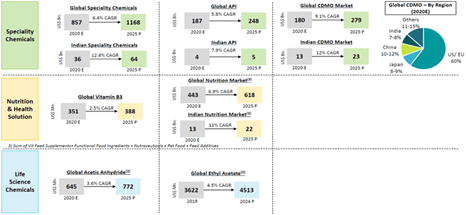

The products have use across Pharma, Nutrition, Agro chem, Industrials & consumer products which are all growing at a decent pace. Due to the diversified end user base Ingrevia is shielded from industry slowdown. They have a long runway for growth in all three areas they work in and have provided the below summary of market landscape.

The highest margin/value segment is Nutrition followed by speciality and then life science.

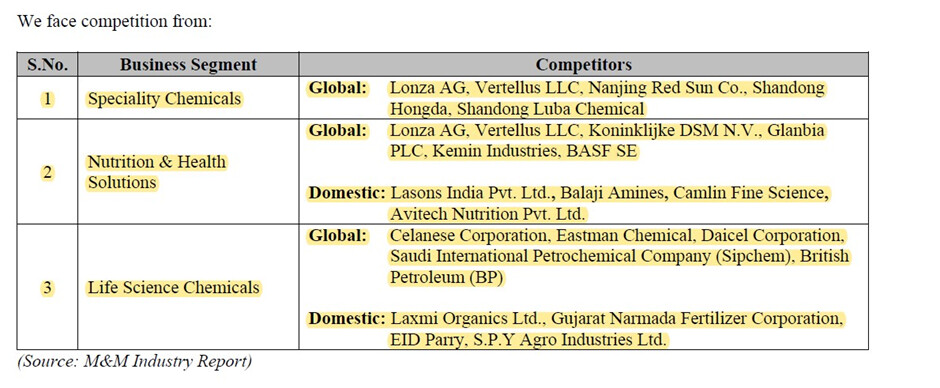

Major competitors are international MNC’s.

Since Ingrevia is the lowest cost producer in most of its products, they are the market leaders in those products and have the highest market share.

Amongst top 2 in pyridine-beta globally

#1 in 11 pyridine derivatives globally

Top 2 in vitamin B3(niacinamide) globally

#1 in vitamin B4 in domestic market

Top 2 in acetic anhydride globally .

MANAGEMENT

Bhartia Group is a well-established & reputable group and have been successful so far, are the promoters of Ingrevia. They have interests in various sectors & this demerger of Speciality chemicals business was done to unlock shareholder value.

Pre demerger, Jubilant lifesciences was not able to reduce its debt from 2010. Post demerger the management of Ingrevia has been successful in reducing the debt position significantly, this shows the renewed interest/focus or drive of the management to grow the business.

The promoters are very professional and let the hired management/team run the business. 5 out of the 7 committees are led by independent directors. The board of directors are also balanced in terms of promoters and independent directors. This shows the corporate governance standards of the company.

The company and management are very clear with the ESG standards and adhere to it.

ENTRY BARRIERS

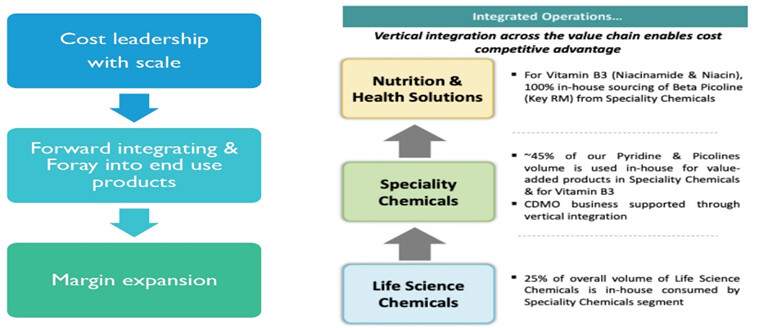

Backward integration **- They are the lowest cost producer because they are fully backward integrated to the key raw material beta picoline thus being able to source the raw materials in-house without facing any supply volatility, also lesser freight costs (for raw materials to be transported). It takes a lot of time and capex to get to the level of backward integration Ingrevia is at.

Price leadership **- Lowest cost producer of pyridine-beta and all value added products. Due to years of experience

Switching costs **- Long and tedious approval process by customers, takes 3-5 years for product approval and facility audit.

Complex chemistry **- Demonstrated expertise in handling multi-step chemistries (up to 13 steps). Due to strong R&D and experience.

Technological knowhow **- Uses the niche technology (air oxidation) for manufacturing niacinamide-leading to lowest cost. Developed this process from scratch thus difficult to duplicate.

Connections with farmers **- Attained deep reach within the farmer community for Animal nutrition and Health products. Takes a lot of time as most farmers are not educated and must really understand the benefit they can derive from the product.

Brand recognition **- ‘ANICHOL’ for vitamin B4 is a leading brand and the company has another 18 brands. Brands are positioned in the minds of the customers thus hard to replace.

Handling large volumes of ketene **- Ketene is a very volatile compound and very difficult to handle or store. Ingrevia can handle huge volumes of it due to its decadal experience in the chemistry.

Multiple plants **- Ingrevia has 61 plants spread out in such a way so as to be the preferred choice of their customers in terms of freight costs and delivery time

Forward integration **- Ingrevia uses the end products of its three business segments (nutraceuticals, speciality chemicals and life science) as feedstock for production among each other.

THESIS

Expansion - Ingrevia has planned a capex of Rs 2,050 crore over fiscals 2022 and 2025 towards expansion for diketene derivative products, expansion of facilities for crop protection chemicals, vitamin B3 products and acetic anhydride. The capex is progressing as per schedule and is expected to be funded through internal accrual, with minimal reliance on external borrowings. The expected asset turns will be >2x and >20% ebitda margins. Expected peak revenue is 9500cr, but speciality and nutrition segment will increase from current 46% to 65% thus higher margins. Commissioned the Diketene phase one and acetic acid plant.

New products **- Plans to launch 60+Products (in Pipeline) for next 4 years. These new products will majorly be higher value products (margin accretive).

Management expectations **- Wants to double the revenues by 2026 . This will be achieved through the mammoth 2000cr capex, entering new products and better reach to customers.

Firing the CDMO engine - New GMP and non-GMP facilities, which are expected to be ready during Q3 FY’23, will help them in capturing growing demand of CDMO projects. CDMO is again margin accretive. This will start adding meaningfully once the facilities reach optimum utilization. Entered a contract worth 270cr over 3 years.

Loan Prepayment - Ingrevia repaid/prepaid about Rs 548 crore long-term debt over fiscal 2022 and first quarter of fiscal 2023, reducing debt at a fast pace to lighten the balance sheet and increase profitability.

Foray into Diketene chemistry - Indian market size is $150mn (2019); 40% was imported; Laxmi Organics is sole Indian manufacturer with 55% market share; Plans to launch 6 derivates; One of the few global companies capable of handling large volume of ketene; Huge demand coming up for diketene and one of the leading producers has exited. This product is mainly to substitute imports. Already was into ketene production now entering the value added diketene segment.

Agro-active - Moving up value chain from ingredients to producing agro-actives (for pesticides).

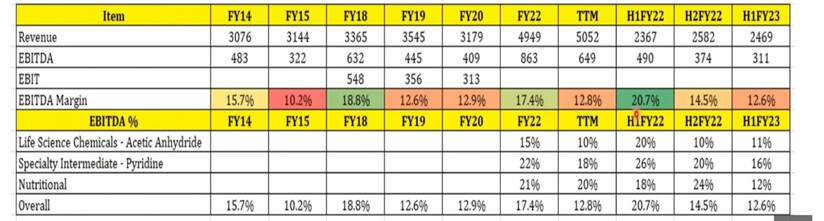

Margins bottomed - As we can see from the picture below the lowest margins for Ingrevia range from 10-13%. In FY15 the margins were 10.2% then there was a margin expansion, same happened in FY19 and 20. Currently ebitda margin is at 12.6%, the margins of all three segments are currently compressed due to supply chain, inventory and cyclic reasons.

Credits to @Worldlywiseinvestors sir’s and @suru27 sir’s youtube video for this particular thesis pointer and image.

Pre mixes - The nutrition segment consists of vitamins and premixes, there is a flu going around Europe. This is affecting the demand for the vitamins and thus causing a contraction in margins of manufacturers of vitamins all around the world. The management is trying to increase the share of the pre mix segment in the total revenue. Pre mix has higher margins which will help balance out the current margin contraction that can be caused by the vitamins.**

Foray into Fluorine chemistry - Ingrevia is trying to enter the fluorine chemistry, although the competition here is high** **(srf, navin fluorine, gfl) the demand or fluorine products/derivatives is also high. This segment is high margin. No clarity given on the type of products they will be manufacturing.

ANTITHESIS

Regulatory risks - Previously Paraquat (herbicide) which uses pyridines was banned by multiple countries thus Ingrevia had to stop its production. There is risk if the government brings in new regulations or product bans for any of Ingrevia’s existing products.

Lifescience segment - The lifescience segment of Ingrevia is commoditised, it has no supply/ pricing power for any of its products. The products here have very low margins therefore acting as an overhang for the overall margins. If the management isn’t able to walk the talk of reducing the share of this segment as has been told then this may impact margins as well as the reputation of the company.

Raw material volatility - Acetic acid is the major raw material and is largely imported. China has world’s 42% capacity of acetic acid. There can be volatility in prices due to freight costs or availability also as China is trying to control its pollution levels, the government is shutting down various plants and manufacturing sites this can lead to shortage is supply if acetic acid plants are shut down.

ESG compliance - Before 2015 there were various esg compliance issues with the company there were various cases by employees and villagers against the operations and functioning of the Gajraula plant, there was a chemical leak at the Nira plant and few other pollution related cases (although this was long back and no such issues now).

Power and fuel costs - Energy costs form a significant part of the operating costs, current spike in energy prices has hurt the margins and can also do so again in the future if these prices persist. Coal is being imported right now as government couldn’t fulfill their contract to supply it due to some shortages although it is expected that the supply from the government will resume from January 2023.

Flu in Europe and US - The majority of the vitamins manufactured are supplied to US and Europe. There has been a continuous rise in flu cases thus the demand for vitamins has fallen, leading to inventory built up by both distributors and Ingrevia.

Demand risk - Ingrevia already has done a huge capex. If there is an economic slowdown or anything that may suppress demand for its products, the company won’t be able to convert this huge capital expenditure into cash flow. This may result in underutilisation of the new plants and thus an increase in debts to fund the working capital.

As @SajKap sir said, company ki niyat kharab nai hai but samay kharab chal raha hai.

Think about it.

22 Likes

Ingrevia Q4 concall notes

Lower realization in acetic anhydride and ethyl acetate, due to lower price of acetic acid.

Although the niacinamide business is still facing headwinds (due to the flu in the EU and US), the management has started witnessing improvement in demand for it.

Due to the current inventory levels of agrochemicals with customers, the demand for specialty chemicals has been subdued. Management expects normalization by the second half of FY24.

There was also a lot of energy cost increase in previous quarters, but now energy costs have been decreasing due to a reduction in coal prices, and efficiency in consumption. Further, there are plans to source power from the grid at Gajraula (this will start in Q2).

There was an improvement in demand as well as the price of Niacinamide in this quarter.

They have approved the capex to build the new cGMP-compliant facility which will produce about 3,000 tons per annum cosmetic grade of Niacinamide. Doing capex during a down cycle. confidence?

The management believes that it is the bottom that they are at in terms of margins and situation.

For their products like niacinamide and pyridine, there is competition from China. If China becomes aggressive, there will be an impact on the margins of these products.

The new diketene plant is at 65% utilization, this should grow.

Management is confident that EBITDA in FY24 will be better than in FY23.

On Chemical Intermediates, because of their new acetic anhydride plant starting, their overall sales will be better.

The niacinamide situation has gotten better in Q1 FY24 itself, in terms of demand and price. Expects normalization going forward (in a few quarters).

For specialty chemicals, the first half will stay depressed.

Overall the situation seems to be getting better, with niacinamide demand returning and better realizations, the specialty chemicals demand should get normalized by H2 when the inventory of customers drop down. The power costs should also go down as coal prices are reducing and as and when they will start taking the electricity from the grid, also the solar energy source should come online soon.

The biggest risk right now is China opening up and dumping their products, thereby impacting the realizations and margins of Ingrevia.

17 Likes

Q1FY24:

• Human Nutrition great comeback. Speciality chemicals profit margins improved qoq (12% in q4fy23 to 16%) despite lower sales and agrochem headwinds indicating pricing power and CDMO benefit.

• During the quarter ended 30 June 2023, the Holding Company has commissioned new ‘Acetic Anhydride’ plant at Bharuch, Gujarat.

• Change in CEO & Managing director: Superannuation (Retirement with pension benefits) of Mr. Rajesh Kumar Srivastava, CEO and Managing Director.

Appointment of Mr. Deepak Jain as CEO & Managing Director of the Company. Deepak has more than 18 years of rich & diverse global experience with Bain & Company where he has been working as Senior Partner responsible for APAC Advanced Manufacturing & Services practice covering Automotive, Chemical and Cement industries. Deepak is an accomplished leader who has been recipient of multiple accolades like “ET 40 under Forty” and Fortune India’s “40 Under 40”. Deepak is a Chemical Engineer from IIT Delhi where he earned the Silver Medallist award, and an MBA from IIM, Ahmedabad where he was an Industry Scholar.

• Specialty Chemicals Business: Demand from Agrochemical customers globally continue to face headwinds due to exceptionally higher pipeline inventories. However, demand from our Pharmaceutical and other customers has improved leading to improved price realization and margins from these products including CDMO.

Registered growth in volumes of Specialty products towards non-agrochemical end-use including CDMO, resulting into normalization and sequential margins improvement of overall segments.

Our GMP and non-GMP plants for CDMO products, commissioned in the last quarter are ramping up as per plan and are helping to meet increased demand from our CDMO customers.

• Nutrition & Health Solution Business: Niacinamide sales volumes improved significantly, resulting into revenue growth. We continue to witness improved price realisation due to higher demand in the segment. Business continue to maintain global leadership position in Niacinamide and focus on Niche segments like Food & Cosmetics.

Sales increased 35% yoy. Ebitda margins improved to 8% from 3% in q4fy23. Still down from 13% in q1fy23 indicating more recovery is left for the division. (Improving realizations should drive margin recovery)

In NHI business developmental work for Food grade Vitamin B4 is almost over and business is at advance stage of finalising capex for GMP compliant facility of Vitamin B4,approval shall take place in the ensuing quarter.

• Chemical Intermediates Business: We continue to improve our market share of key product Acetic Anhydride, despite the challenges of lower demand from Agrochemical end-use segment. We also witnessed lower price realisation in the segment due to pricing pressure from Agro end-use of Acetic Anhydride and lower realisation of Ethyl Acetate in Exports market.

Newly commissioned Acetic Anhydride plant at Bharuch is ramping up as expected.

Acetic Anhydride: Globally No. 2 in Merchant Mkt No.1 in India Estimated to be Global leader by FY’24

CONCALL:

• Gross Margins of 48% are very much sustainable

• On Agrochem slowdown: There are two reasons for this situation of agrochemical. One is the weather conditions in Brazil, U.S. and Europe in last 6 to 8 months have been very, very difficult, and that has actually reduced the demand. And the second is that the customers have piled up the inventory in anticipation of higher demand. So some of the customers have inventory up to even 10 months. You can imagine that this kind of inventory liquidation will take time. Though we estimate that this situation,as per customers, should be normalized sometime November, December. What we expect is that the last quarter of our financial year should be the normal quarter. That is what we can estimate based on what our customers are intimating to us.

• Nutrition segment to continue improving: Nutrition business, normally we take the orders for a quarter. So if the prices start improving, we don’t see the impact immediately. It takes about a quarter or 4 months to seek to reach to the actual normalized situation. So last quarter, the improvement started mid of the quarter, if you remember, and we could not enjoy the full quarter benefit. So now more or less, we are not still on the same level of last year, but we are now reaching to closer to the normal situation. I can definitely say that even the ongoing quarter as well as the future quarters should be definitely better.

• Capex: What is the number that we should work with for FY '24 and FY '25 in terms of the cash outflow? FY '24 should be between INR600 crores to INR700 crores. FY '25 will be close to INR500 crores, so far. If we find something interesting, it might go up a little bit more.

• Speciality chemicals margins: I have been always talking on our Specialty Chemical, product mix basis, our margin to be close to 16% to 18%. I’ve been saying that. So I think what you are saying 20% to 22% is still not there because we have to utilize our GMP facility completely, all the new products, which we have launched in CDMO have to come on commercial scale. So it will take a little time to reach to that 20% level, which is what I had said earlier also.

• Cost of production vs China: Also in terms of our cost of production, just a sense on Pyridine, what would be the differential between us and China? We would be evenly matched with China? - Cost of production, we always claim that we are best in the world. Otherwise, if China does not dump the material, we also get an opportunity to sell in China. It is only when China decides to sell. If you remember, about 1.5 years before, there was a situation when China was being very, very modest in their pricing. They did not do the dumping about 1.5 years before, and that is the time we took some market from China. So unless they decide to sell lower than the cost, we are definitely best cost situation in terms of Pyridine and Pyridine derivative.

13 Likes

In latest company communication to exchanges company informed that Jubilant Infrastructure Limited (“JIL”), wholly owned subsidiary of the

Company has purchased 6.67% equity Share in Forum I Aviation Private Limited (‘FAPL’) from

MAX ATEEV Limited.

Post-acquisition, JIL holds 9.12% equity shares in FAPL.

FAPL is engaged in business

of operating Aircrafts on Charter

basis under the Non-scheduled

Airlines.

Can anyone here please help me understand why they being a chemical company investing in a charter company?

Source:

8d91f154-811c-454a-a327-37c44e1180ed.pdf (360.4 KB)

1 Like

I also read this in their exchange filing but unable to understand what will they do with this acquisition. What benefit will the company get with this acquisition.

This is the case with every corporate house in India. DGCA will give NSOP only if the company which is applying is backed by a strong promoter. The new company will charter aircraft to the group companies to fly employees/directors. They can also render services to outsiders if aircraft is not needed for the group. This is as such not a new business venture

2 Likes

Any views on Q3FY24. Revenue and profits are down as expected.