Ingrevia got demerged from Jubilant Life science and started trading from yesterday at a very moderate valuation to peers it seems. There is not enough information about the past years & Balance sheet but the information provided by the company in the investor meet this week gave most of the required info about the company. The fair value as per me with an estimated EPS (INR 18) for FY21 should be 360 or thereabouts so it seems to not have been correctly valued yet & the market has to correctly price it as per sector & EPS. I am of the opinion that this will be a long-term compounder & is available with enough Margin of safety for now.

Management

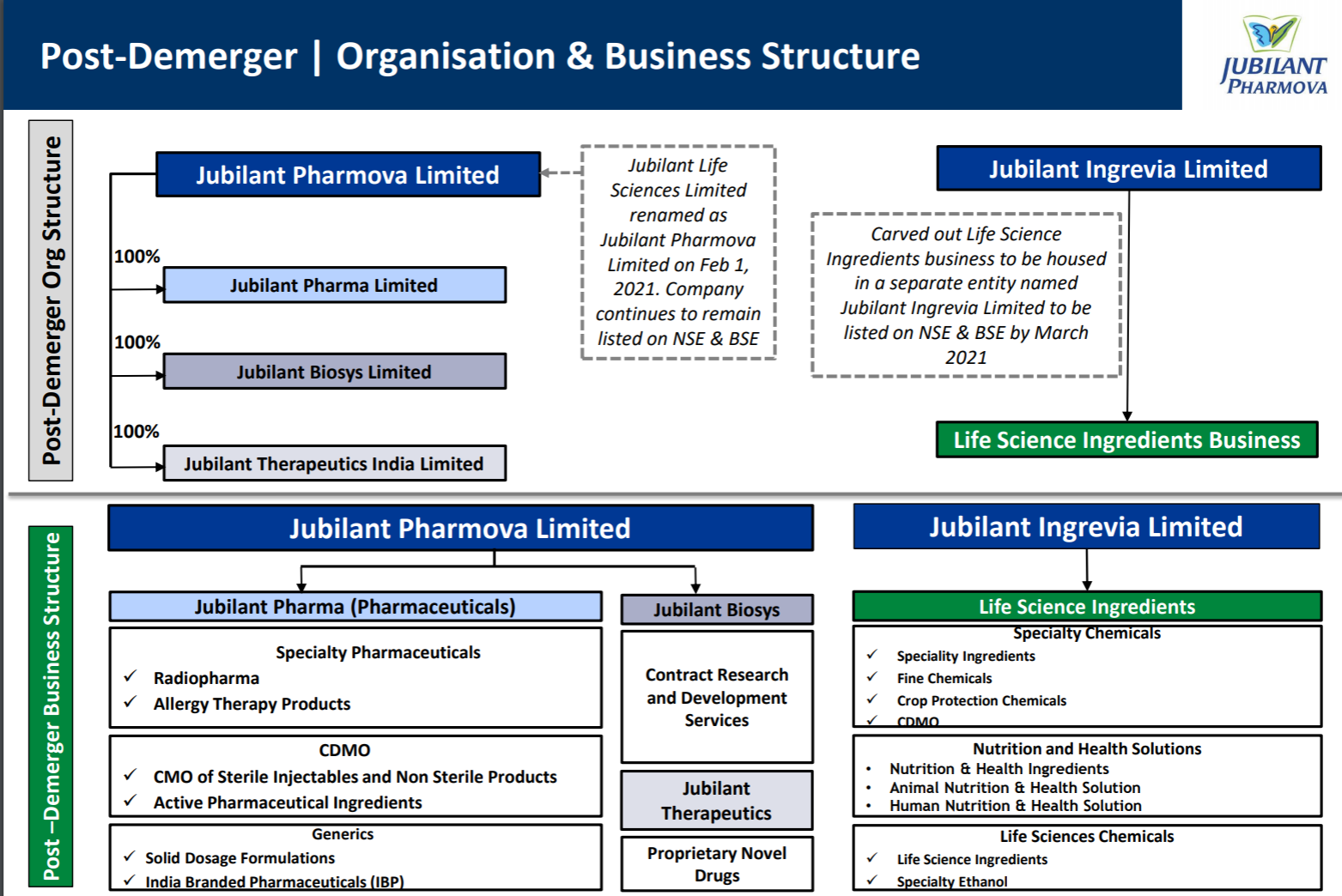

Bhartia Group is a well-established & reputable group and have been successful so far. They have interests in various sectors & this demerger of Speciality chemicals business was done to unlock shareholder value.

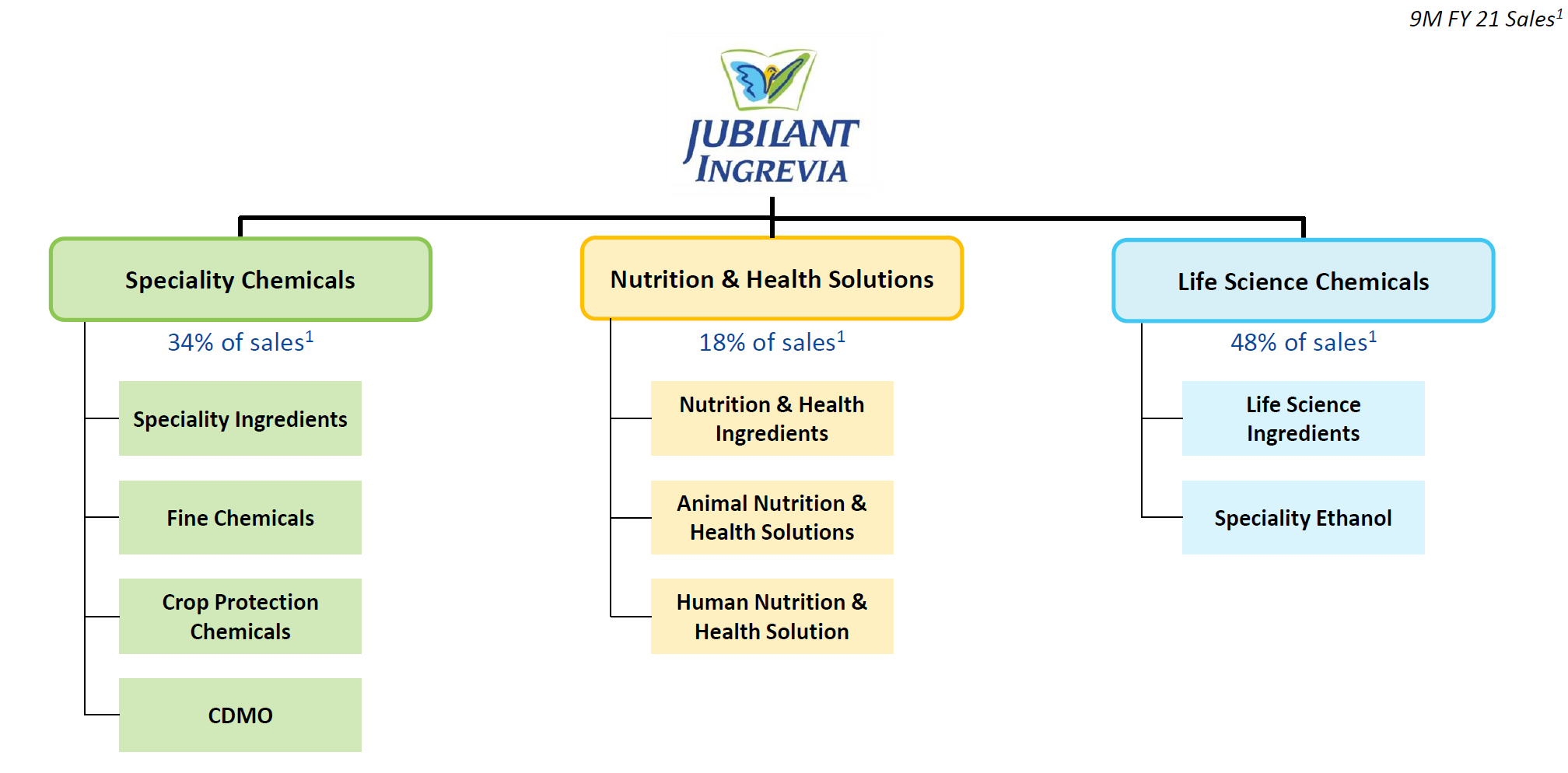

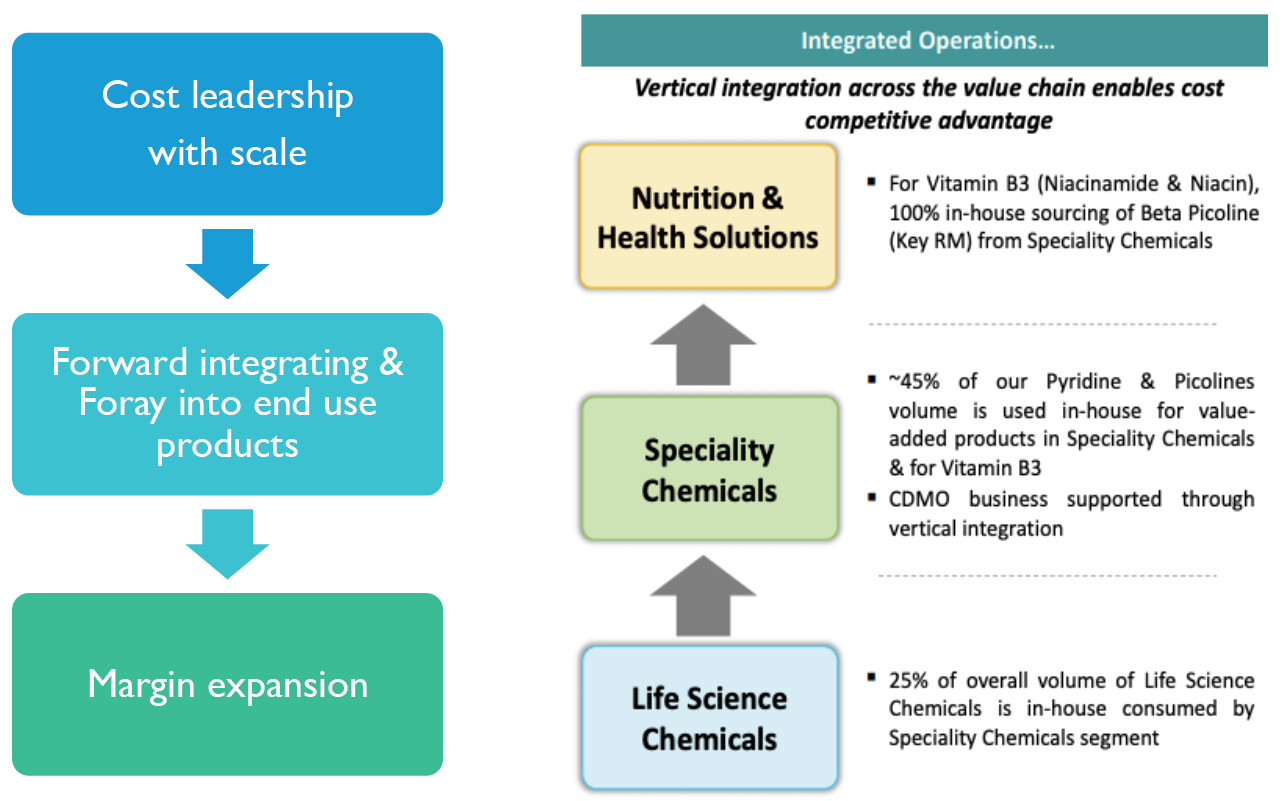

The products have use across Pharma, Nutrition, Agro chem, Industrials & consumer products. which are all growing at a decent pace.

They have worked on their internal operations to optimize and that has resulted in efficiencies and cost savings.

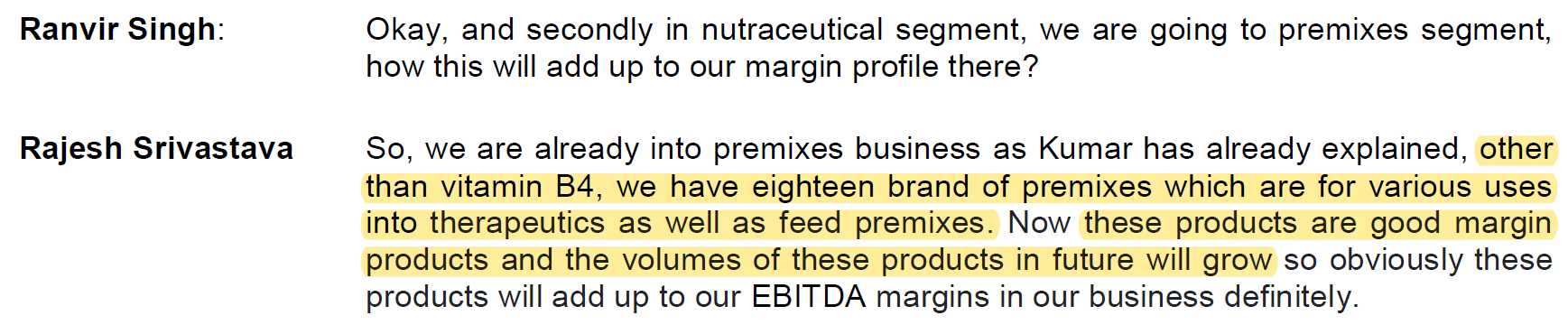

CDMO services are also taking off, They have 7 projects in pharma and 4 in agro sector. They are doubling their existing CDMO capacity & have order book of ~250 Cr. Going forward this should contribute larger revenue with higher margins.

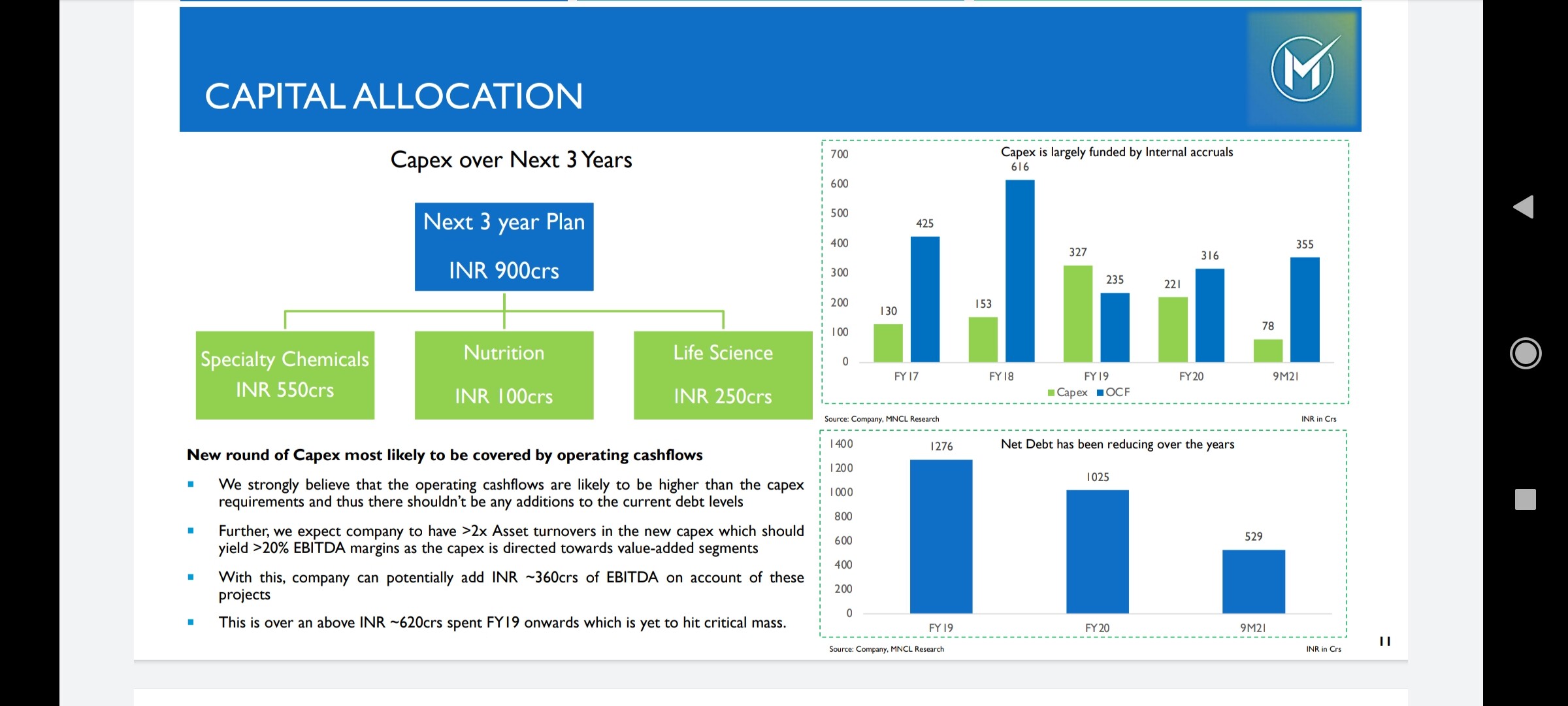

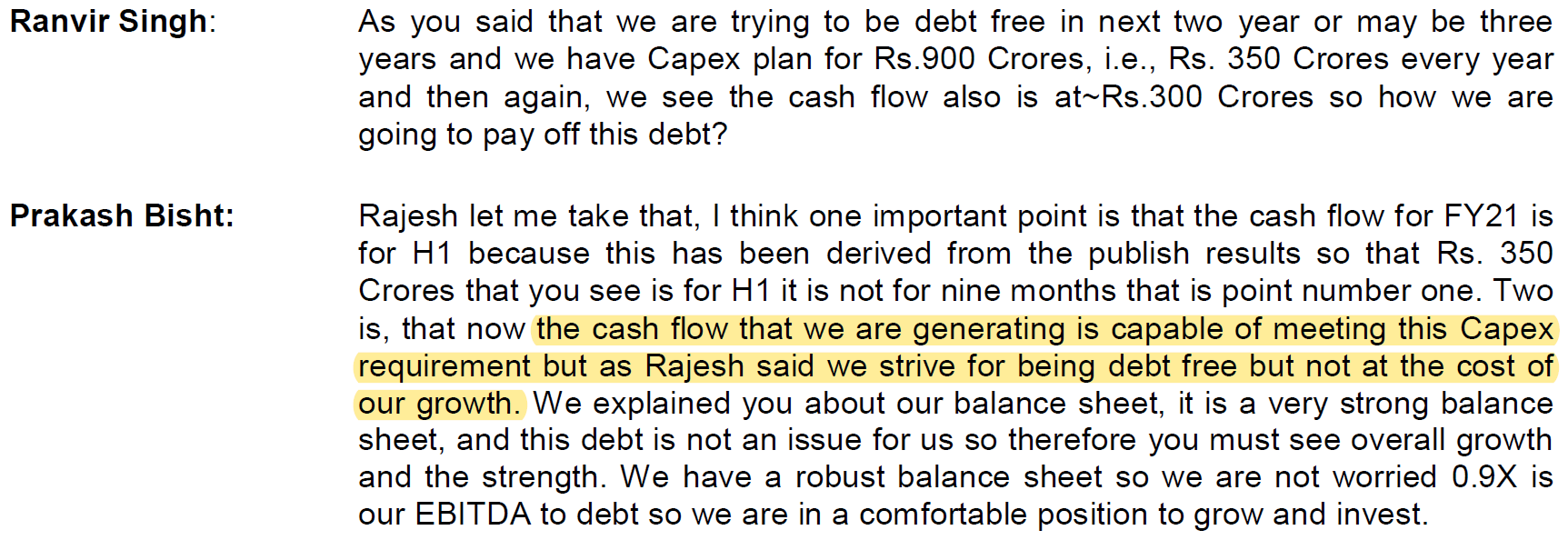

They are planning 900 Crs of capex for next 3 years (550 in specialty chemicals,100 in Nutrition & health chemicals, 250 Cr in Life sciences chemicals) which should further expand the capacities, Currently they are running at 70-80% utilization.

Financials

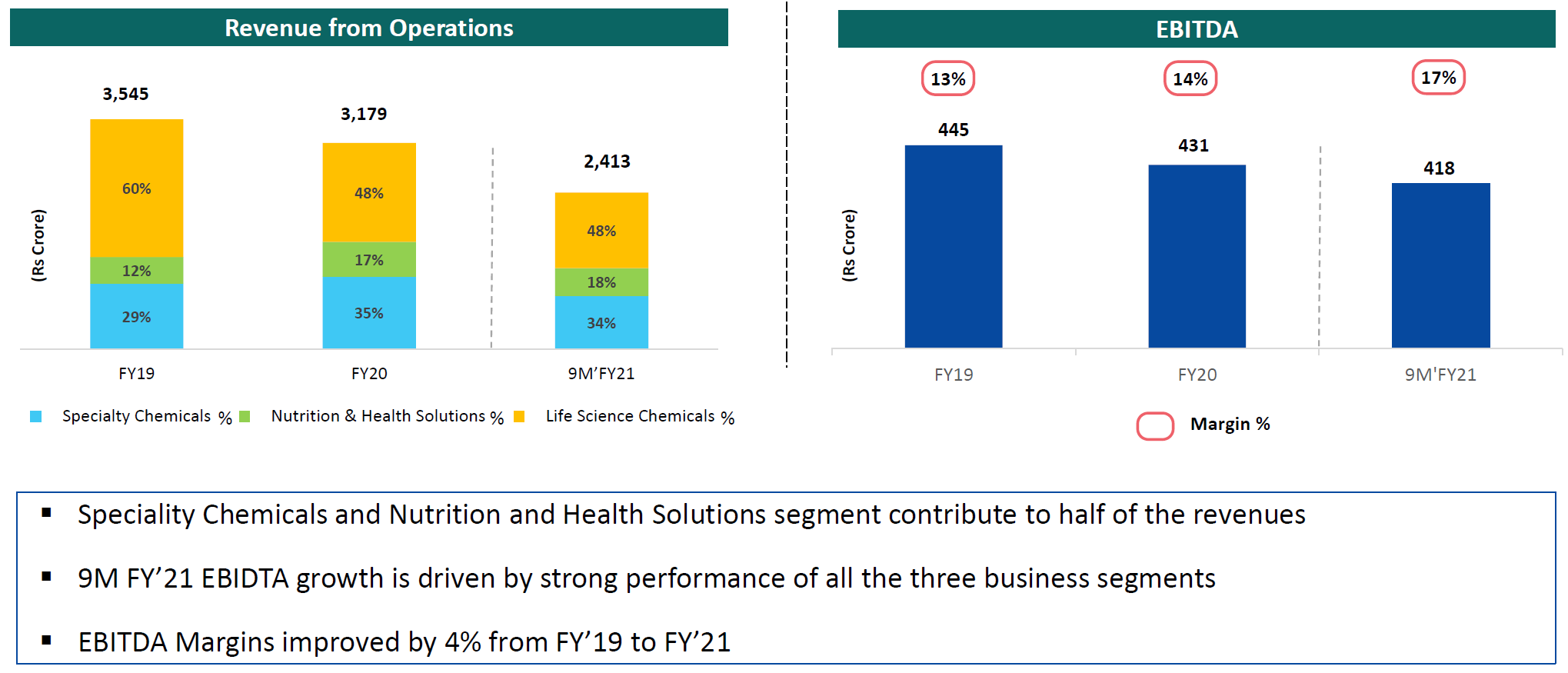

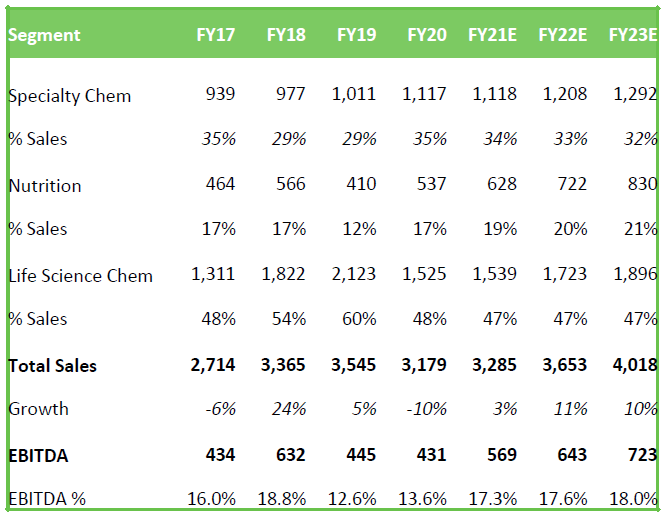

They have provided the below information on revenue comparison for Fy21 & FY20 from all verticals and the margin profile which I think will improve further going ahead.

Thanks for creating the thread. I had a look at the investors presentation and went through their site. I was wondering for comparison sack can advance enzyme (Human and Animal nutrition, food processing) and Fermenta (Vit D3 for Human and Animal feed) be considered? or it is entirely in niche segment?

note: I got shares of Ingrevia as part of demerger.

The market has rightly given it a subdued valuation.

The Analyst Presentation mentions a future investment of roughly Rs. 900cr over the next 3 years. Either that will be in the form of debt, which will erode the present net profit significantly, if not entirely. Or it could be by way of equity dilution. Better to wait and watch.

Disc: Not invested.

What management said in the presentation is current ebidta of 350 Cr will take care of capex and with better margin expansion debt reduction will be bonus…also, debt to equity ratio of 0.9 they are quite comfortable…nowhere they mentioned capex with debt…they have already reached capacity utilisation of 85% and capex is must to capture growth.

Disc. Invested since long…views maybe biased.

I was working out the rough conservative comparison of valuation with Laxmi Organics which can be closest peer in terms of products offering of ~80% Below is my assessment.

For the first two segments I have assumed the valuation of Ingrevia at 268 per share & for Laxmi IPO at 130 (which is expected to be 250 as per grey market premium) so comparing these two for just the 83% of business Ingrevia is at almost half at valuation comparison with Laxmi which will start trading from 26th.

Adding the third section of business Nutrition & health segments I could not find any peers in Indian markets. Would request folks here tracking this to suggest any names to be compared with this section of the business. I am sure that will make this further cheaper.

Also, There is the CDMO business with decent pipeline which will start adding meaningfully to top line & high margins in ingrevia.

Also, Attaching the publicly available Monarch report as well which has a comparison with Laxmi & detailed analysis of both the businesses. – Monarch coverage Report - Ingrevia

Sorry if the question sounds very naïve. Which company has the CDMO part - Pharmova or Ingrevia ? I looked the website of both , but could not make out.

It is fascinating to watch how Laxmi Organic is going up after a good listing yesterday and Jubilant Ingrevia is in continuous lower circuits despite the stark valuation gap between the two. It is not just retailers going gaga over Laxmi Organic - two prominent fund houses bought Laxmi Organic in bulk yesterday and looks like few more are lined up today going by the traded volumes. This is after over-subscription of QIB portion by 175 times. May be we are missing something in terms of valuation of Jubilant Ingrevia?

Laxmi was smart in conveying its intention of foraying into fluro-based chemistry and using the IPO proceeds mainly towards this capex and to reduce debt.

The street probably believes there might be a heavy burden of debt to fund the massive capex by Ingrevia, and given the past history of Lifesciences Division, the concerns are not unfounded.

However, given the confidence shown by the management and the resolve shown to considerably improve its Lifesciences division performance during the recent Ingrevia analyst call, I think it might not be a bad bet to increase one’s holding in gradual stages as and when the management starts delivering.

Not so important, but worth noting that RJ usually always refrains from buying shares during an IPO listing, but seems to have made an exception this time by increasing his stake immediately post listing, even before the management has proved its mettle.

Thanks for starting this very useful thread. I am adding some of my notes which were not covered in the original post.

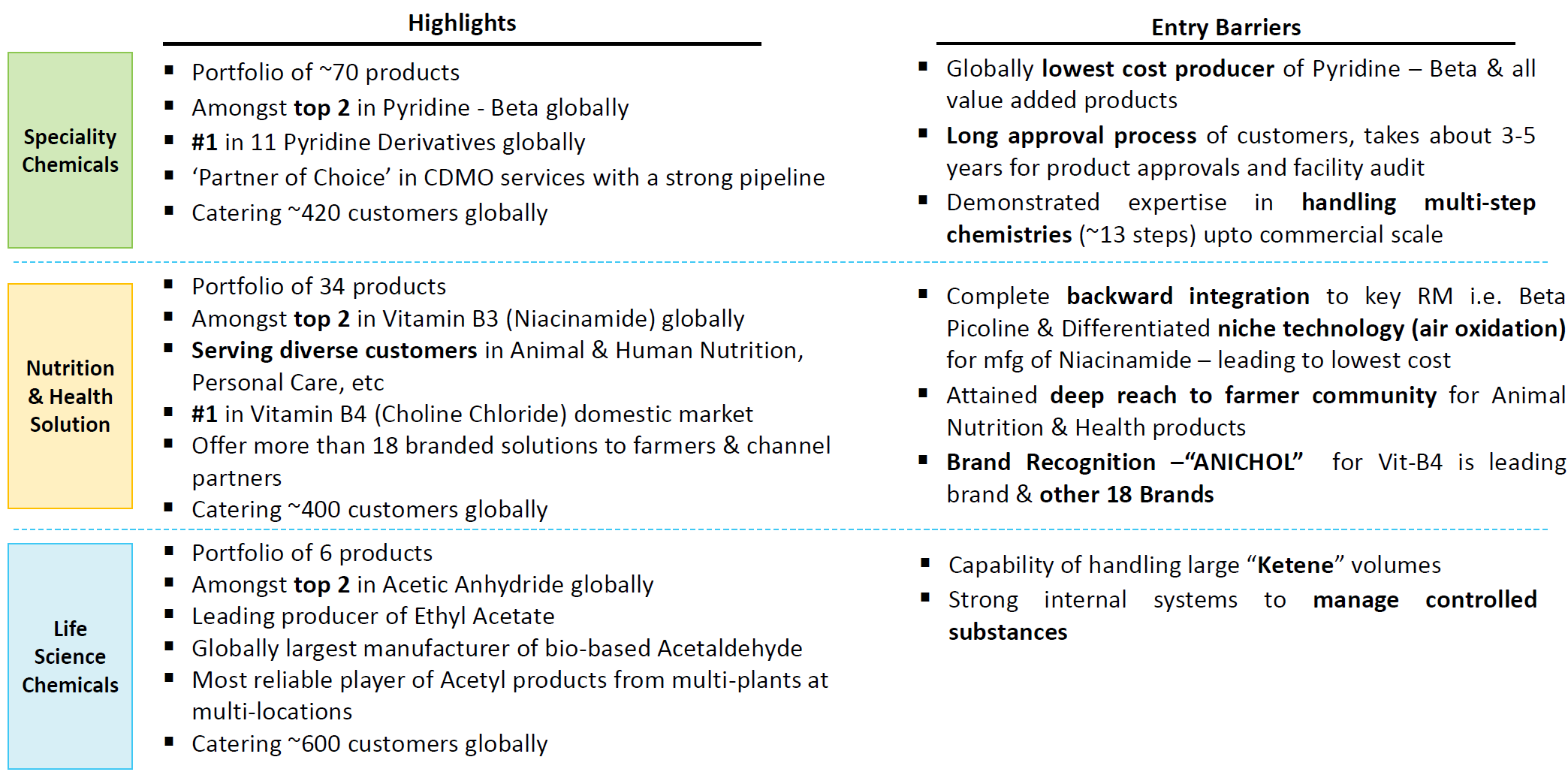

Manufacturing capacity: 61 plants across 5-sites in 3 states (UP, Maharashtra, Gujarat) with a very diversified customer base (top-10 accounting for 20% sales). Company gets better pricing from smaller customers.

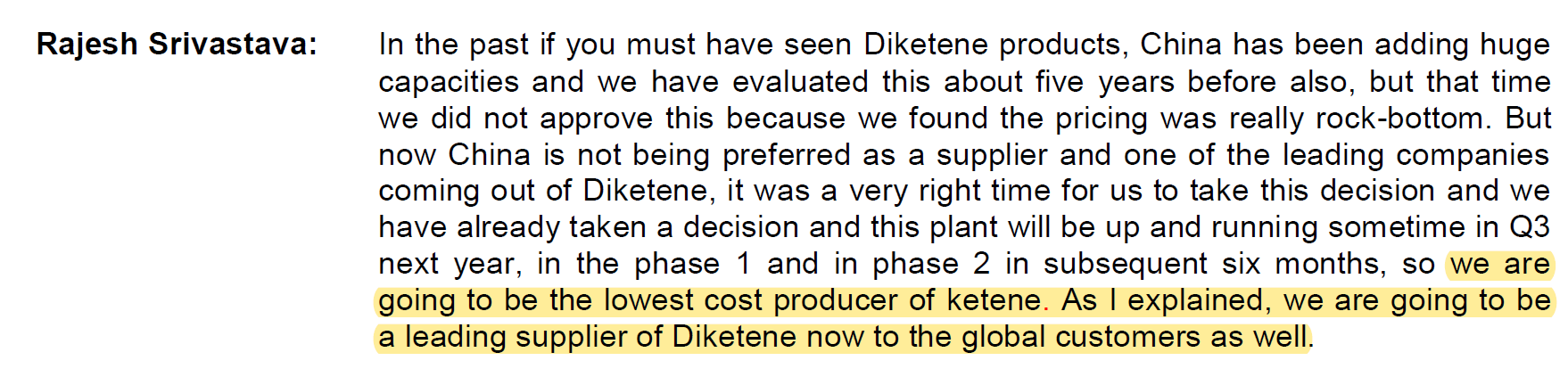

Opportunities Forey into Diketene chemistry: Indian market size is $150mn (2019); 40% was imported; Laxmi Organics is sole Indian manufacturer with 55% market share; Plans to launch 6 derivates; One of the few global companies capable of handling large volume of ketene; Huge demand coming up for diketene and one of the leading producers has exited CDMO: Invest in GMP and non-GMP multi-product facilities for pharma and crop protection (will they get higher margins by investing into GMP facilities?) Agro-active: Moving up value chain from ingredients to producing agro-actives (for pesticides)

Pyridine chemistry: Global leader in 11 pyridine derivates; Used to produce beta-picoline which is used to produce Vitamin B3; Uses 45% of volumes captively; More than 50% goes into producing agrochemicals; Lowest cost producer in pyridine beta and value added products; Takes 3-5 years in product approval and facility audit

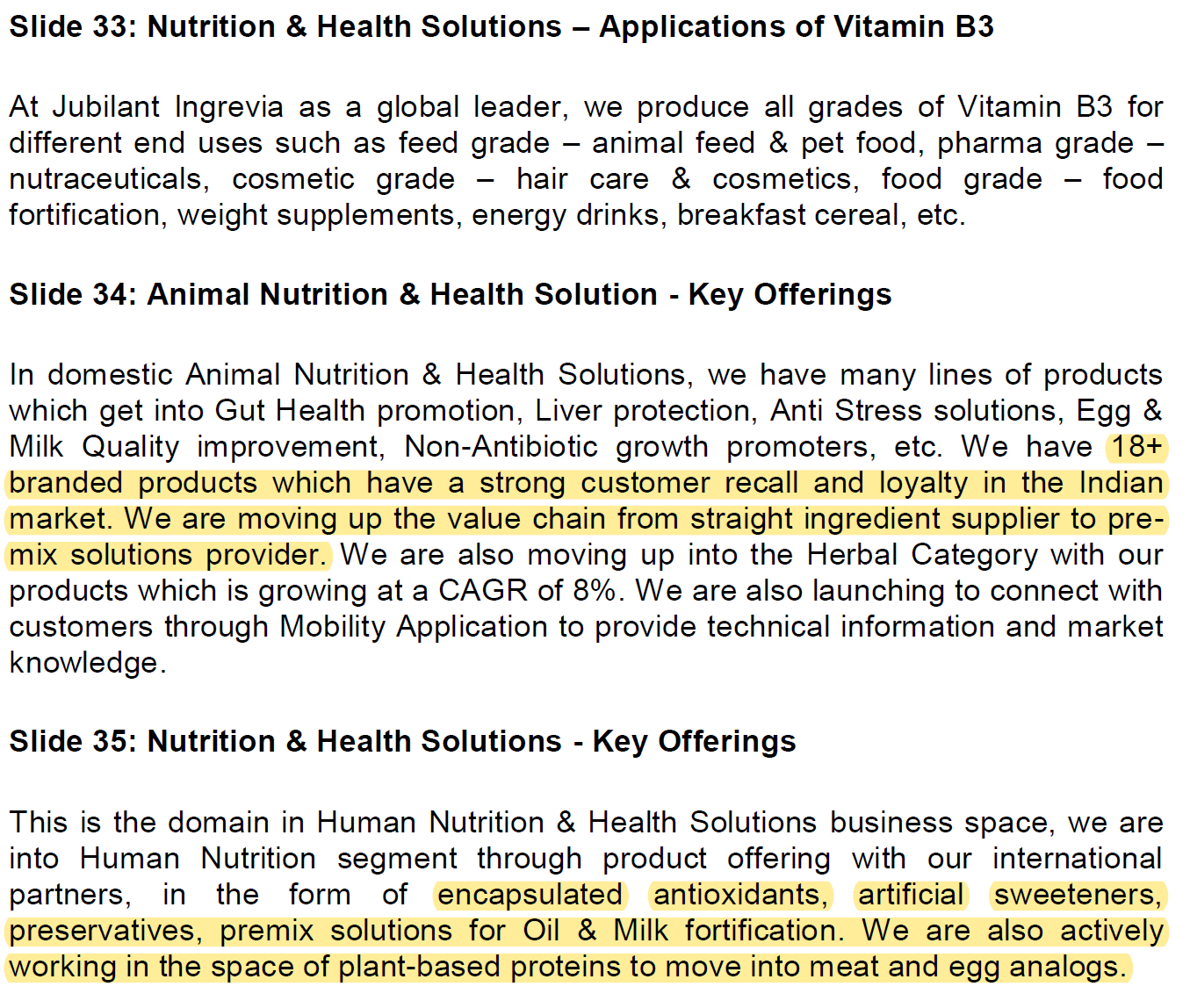

Vitamins (branded + commoditized): B3 (Niacin, niacinamide) global market share of 19%; B4 (Choline Chloride) domestic market share of 50%; Commoditized product facing competition from Chinese players who have excess capacity; Backward integrated into key raw material (beta picoline & differentiated technology; air oxidation for manufacture of niacinamide; main brand: ANICHOL); Looking to create brands for animal feeds; Most demand is from animal (80%) and human (16%) nutrition

Acetyls (low margin, high volume, very high ROCE):

o Acetic anhydride: 71% domestic, 15% international market share; among top-2 globally; current capacity: 145’000 TPA; increase capacity by 35% in 3-years; Used in paracetamol, vitamins, aspirin;

o Ethyl acetate: 33% domestic, 4% international market share; Used as extracting agent in pharma; as industrial solvent in paints, adhesive, and also in flexible packaging; It’s a green solvent

o Bio acetaldehyde: 35% domestic market share; world’s largest manufacturer

o Specialty ethanol: 8% domestic market share; backward integrated using molasses; Leading supplier to oil marketing companies

o Propionic anhydride: Among top-2 global manufacturers

o Key raw material is acetic acid and is largely imported (China has 42% of global capacity); Prices fluctuates a lot

Environmental practices

Most facilities are zero liquid discharge facilities

Zero Liquid Discharge Plants, Multi Effect Evaporators, Reverse Osmosis, Water Polishing Plants

Liquid & Gaseous Waste Incineration facility with online Vent Gas Monitoring

Interesting things to watch out for

Pyridine and beta picoline are produced together. Because of regulatory ban on paraquat, pyridine demand is going down taking prices down with it. As a result, supply of pyridine will also decrease, but demand for beta picoline is going up because there is no impact on vitamin B3 demand. As a result, company expects beta picoline prices to increase. For Jubilant, pyridine demand is mostly captive and not only for paraquat. This should overall be beneficial for jubilant.

Past group track record

Tried to charge royalty for using brand name “Jubilant”. It was later withdrawn.

Jubilant life was not able to reduce debt since 2010, ending into issues of too much foreign currency borrowings, hedging problems, etc.

Has tried leverage buyouts in the past some of which have not played out leading to write-offs (in the pharma business line)

They are not really into enzymes, they produce Vitamin B3 and B4 which is used mostly in animal feeds (and is also commoditized because of excess Chinese capacity).

It seems that their nutrition segment is a mix of brand (higher margins) and commodity, not sure if blended margins are higher than company level margins. Management has mentioned that their highest margin business is that of fine chemicals which comes under specialty chemical business line.

Its not very clear how much of this business comes from innovators (high margin) vs contract manufacturing operations for generics (much lower margin). Also, their pipeline is not very rich (7 in pharma, 4 in agro). For context, PI Industries has a pipeline of 40-45 products in agro CSM on a similar revenue base.

Thanks for adding the remaining details about the company. Adding a few personal thoughts which may add color to the current scenario.

The valuations are back to the listing day now and the gap with Laxmi has increased further after Laxmi listing at premium and with the current price of both & the expected EPS earnings.

I do not expect Laxmi to go down in valuations anytime soon, as it seems in line with other peers in specialty chem sector and if they walk the talk of Fluro chemistry capex & improve the bottom-line going forward.

Ingrevia has lower market cap than Laxmi with more than double the top line & more than triple EBIDTA compared with Laxmi, so it should revert to atleast mean valuation in future. In how much time, it remains to be seen.

Ingrevia

Laxmi Org

9M Fy21 EBIDTA is 418 Cr & EPS is INR 13.81

6M Fy21 EBIDTA is 85.4 Cr & EPS is INR 2

Estimated FY21 EV/EBIDTA based on 9MFY21 EBIDTA

Estimated FY21 PE based on 9M FY21

Estimated FY21 EV/EBIDTA based on H1 EBIDTA

Estimated FY21 PE based on H1 FY21

7

14

29

47

Ingrevia demerger brought back memories of the Solara Demerger from Sequent & Strides in June 2018. After listing, Solara, in 43 trading days was at 9 continuous Lower circuits & after few days 16 Upper circuits.

It was nerve wrecking to muster courage and keep adding after those continuous LCs and just enough information about the demerged assets, management background and past financials. In hindsight it paid out worth every penny. Solara is one of my top multibagger holding today, not necessarily just because API sector played out in last year but I was gunning for decent Margin of safety in buying at those lower prices, confidence in the business and promotors with longer term time frame.

With this demerger, All erstwhile JLS investors would have got Ingrevia shares free of cost and many of them who do not want to hold it anymore are looking to exit which creates imbalance in supply & demand of shares. Also, some degree of information asymmetry in Ingrevia exists as the official past financials are not disclosed yet and they are still to declare any official results post demerger. Potential new investors would want these to be able to invest meaningfully. These factors may keep the valuations subdued, but not for long I believe/hope.

There was just one compilation of Past financials in the Monarch report which I am sharing for ready reference.

Not necessarily, Since they have a huge list of products, many of them would not require to be produced from GMP facilities and since the cost is lower in non GMP facilities, it makes strategic sense to have both and use as required.

Since, Controls, documentation and release criteria’s are different for GMP & non GMP, and having both types of facilities, which essentially utilize the same starting components, sterile consumables and equipment, A GMP technician can be used in both GMP and non-GMP processes leading to better resources utilization and synergies in operations as needed for different products.

Nutrition & health solution segment

Although the Nutrition & health solution segment is small now, I believe this would be able to grow decently as the products they are focusing on looks promising. The branded products will provide higher margins and Plant based proteins are becoming significantly big and fast. I hope they are able to get a pie.

I agree completely with this reply, given the current situation of low interest rates are here to stay for sometime and the business expansion will fetch much better returns than the cost of funds.

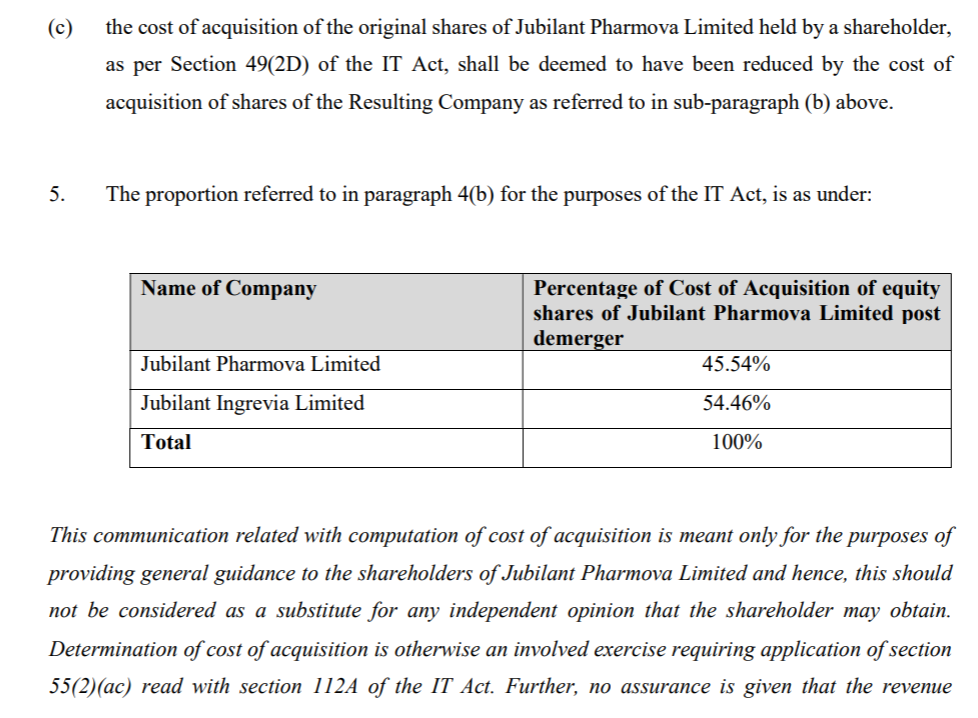

Technically it has to be assumed to be 54.46% of the original JLS acquisition price for taxation purposes. But if you look at the price of Pharmova on 5th Feb of 915 Rs & the subsequent reduction till the listing of Ingrevia and considering you choose to hold both. You are getting an excellent Midcap specialty chemicals business without losing much value on the original Pharmova (which is also undervalued) shares making it effectively with negligible cost.

Rajesh Srivastava: If you look at our last three years, we have not added major capacities except for

that one anhydride plant which we told you was added last year. We have been heavily focusing on balancing our balance sheet and that is why you see our cash generation has been good. We have actually come down in our debt to EBITDA

ratio at a comfortable level. Having said that, there have been a couple of market

situations in our major products like Pyridine which you might know that Pyridine is

used in one of the herbicides called Paraquat. Paraquat started getting banned in

various countries two years ago and that actually lead to the demand reduction.

During the time of pyridine demand reduction, we have gone into various value

added products and now we are producing Pyridine as well as Beta together and

they have a strong position in global market to take this business and Niacinamide

to the next level. While other people, who do not produce Beta to that extent

because of this demand reduction will find difficult times, so you will see the time

for Jubilant coming up and going forward both in specialty chemicals and

nutraceuticals.

This according to my understanding gives a clear message that many accounting tricks have been done to make the picture very rosy and the income side isn’t going to be recurrent type.

From the commentary you have quoted I do not see “a clear message of many accounting tricks”. Care to elaborate/support your allegation with real data/ numbers?