New update on Monarch capital report.

16 Likes

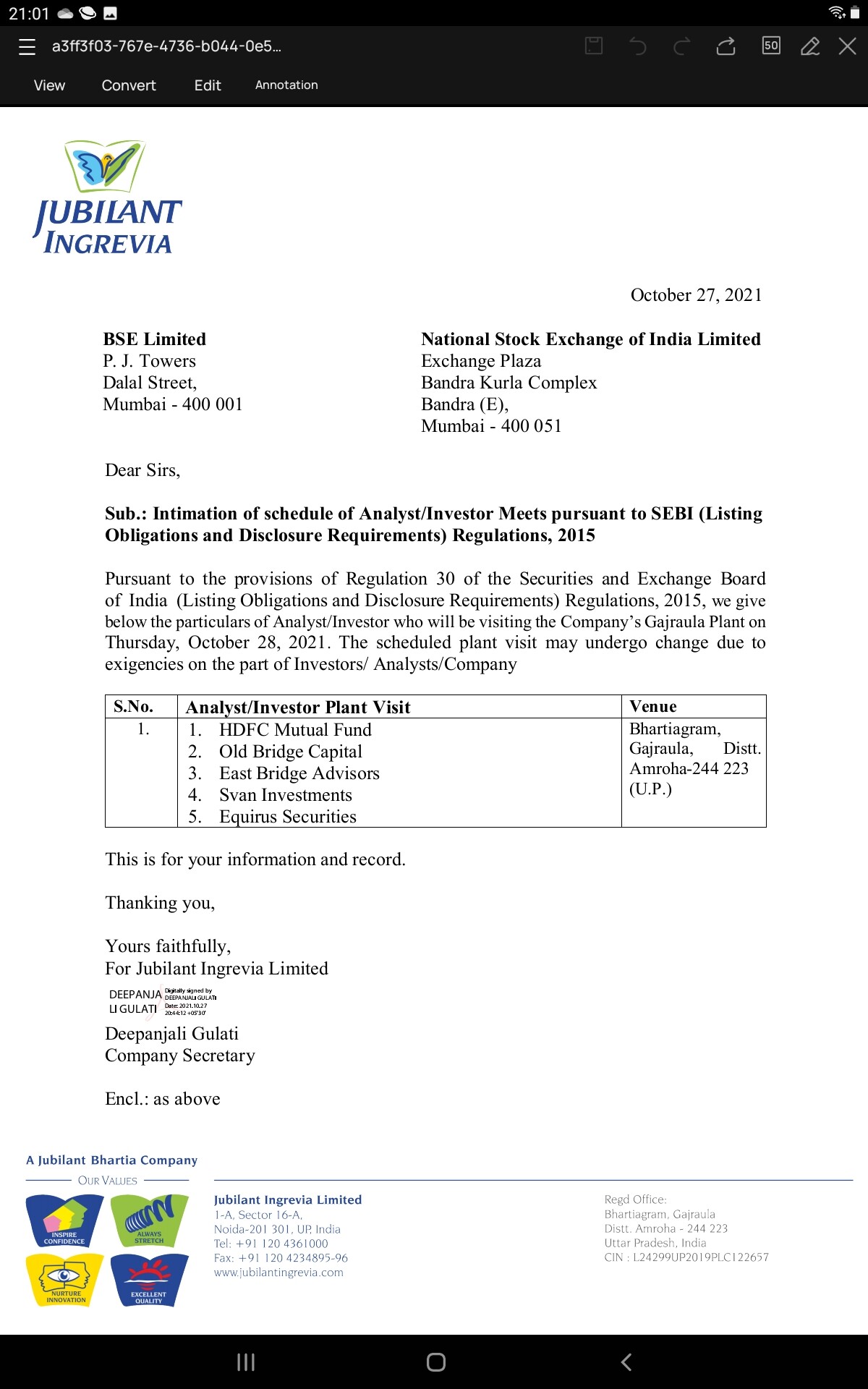

While inestors concalls are more common, plant visits by bunch of good institutional investors - from past investors - erstwhile investors East Bridge capital Master fund have trimmed down from good 8% in March end to 1.4% in Sept 21. Ripe for new folks to on board now that shakeout is done post Q2 results.

RJ is currently largest in public shareholder with close to 6% holding , public holding up from 23% in March to 36% in Sept- definitely under owned by institutions in current state.

11 Likes

They have mentioned as double the revenue from base of 2021. Don’t you think CAGR will be less than 15% going forward as 2022 revenues seems much higher than 2021 ?

1 Like

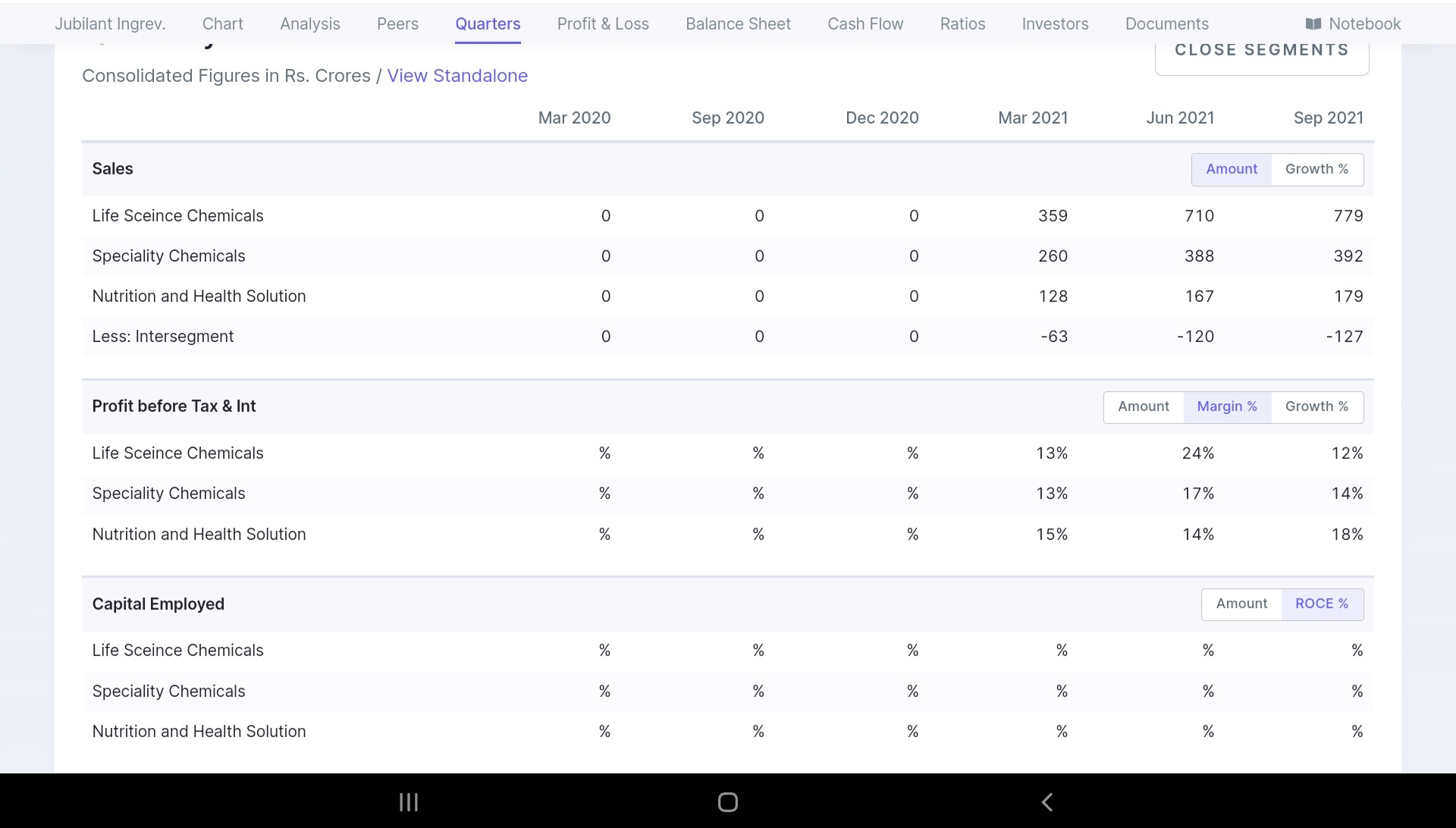

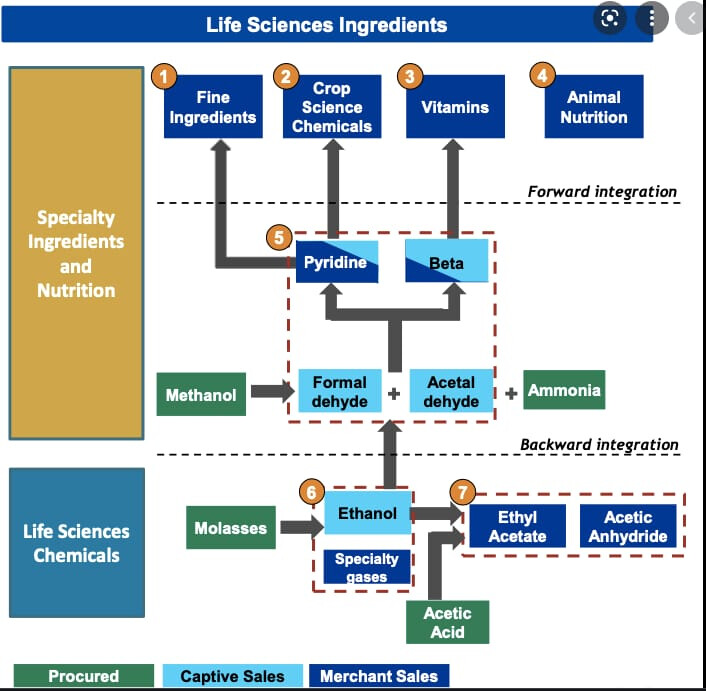

As of now they are 60% Life sciences, 25% speciality chemicals and 15% Nutrition and health.

In next 3 years they are doing 550cr capex in speciality, 250cr in life sciences and 100 in Nutrition.

So speciality chemical share should improve going forward which is high margin business but as we can see from results of previous 2 quarters, margins are very volatile so if anyone with more experience can guide me on what we should expect in margin going forward.

2 Likes

Assume this as doubling of EBITDA and not revenues because majority of raw material costs is a pass through.

5 Likes

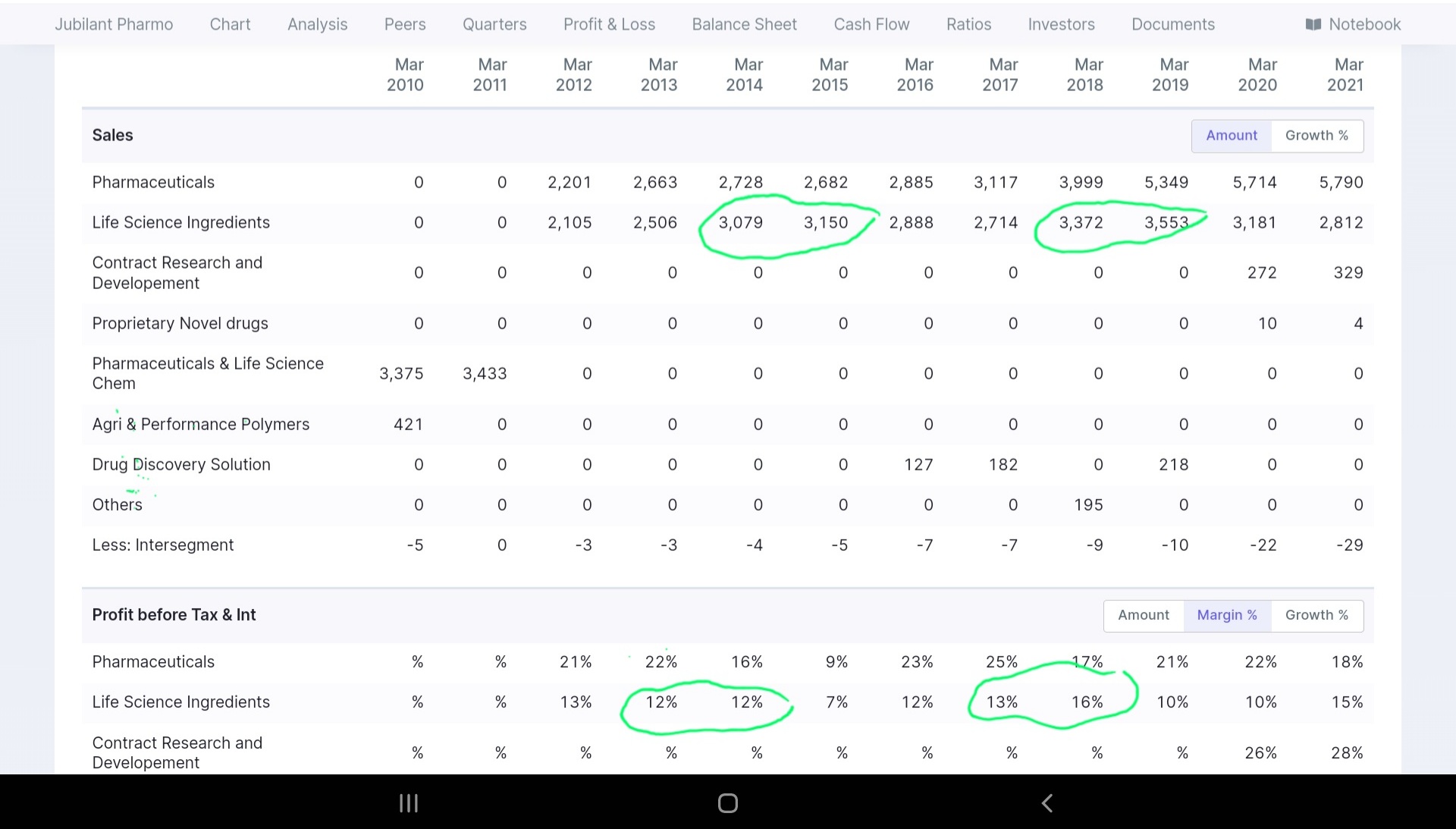

How cyclical is LSI biz - history may provide some clue - ( pulled from Jubiliant pharmova) - for simplicity treating majority as current LSI biz part( low margins as evident from margins)

-

Revenue seems to go up for 2 years and then come down for next 2-3 years and cycle repeats.

-

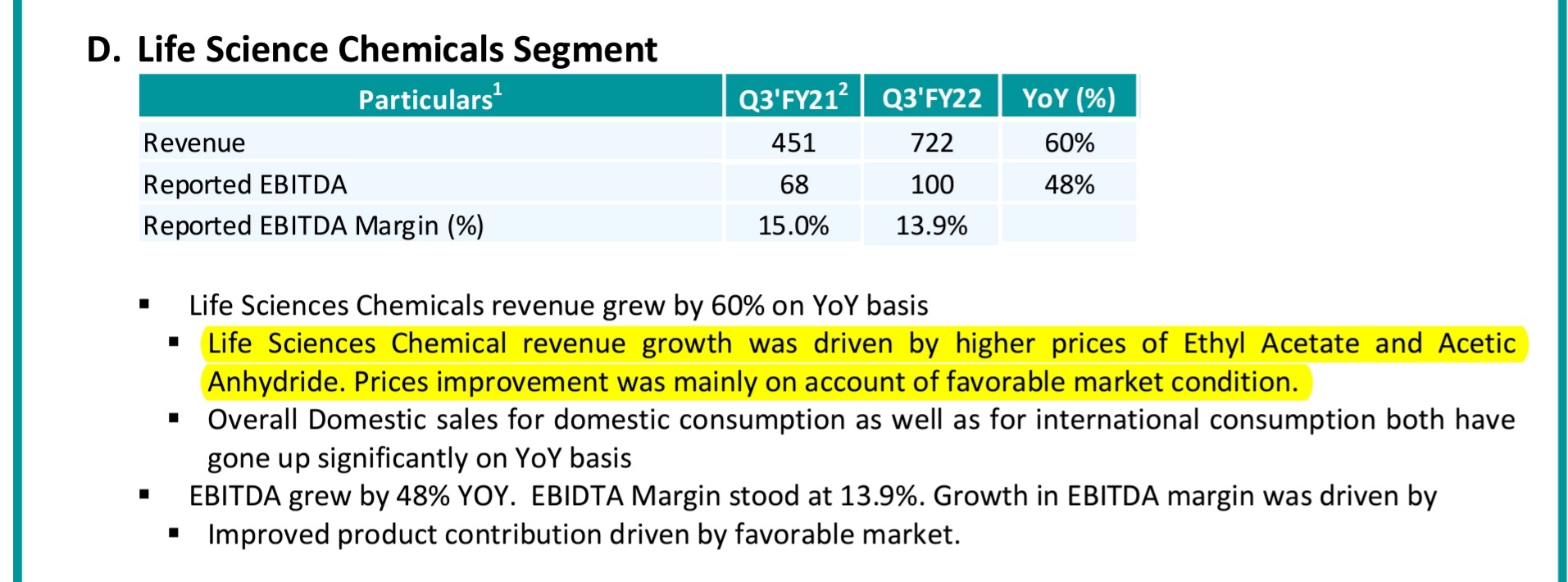

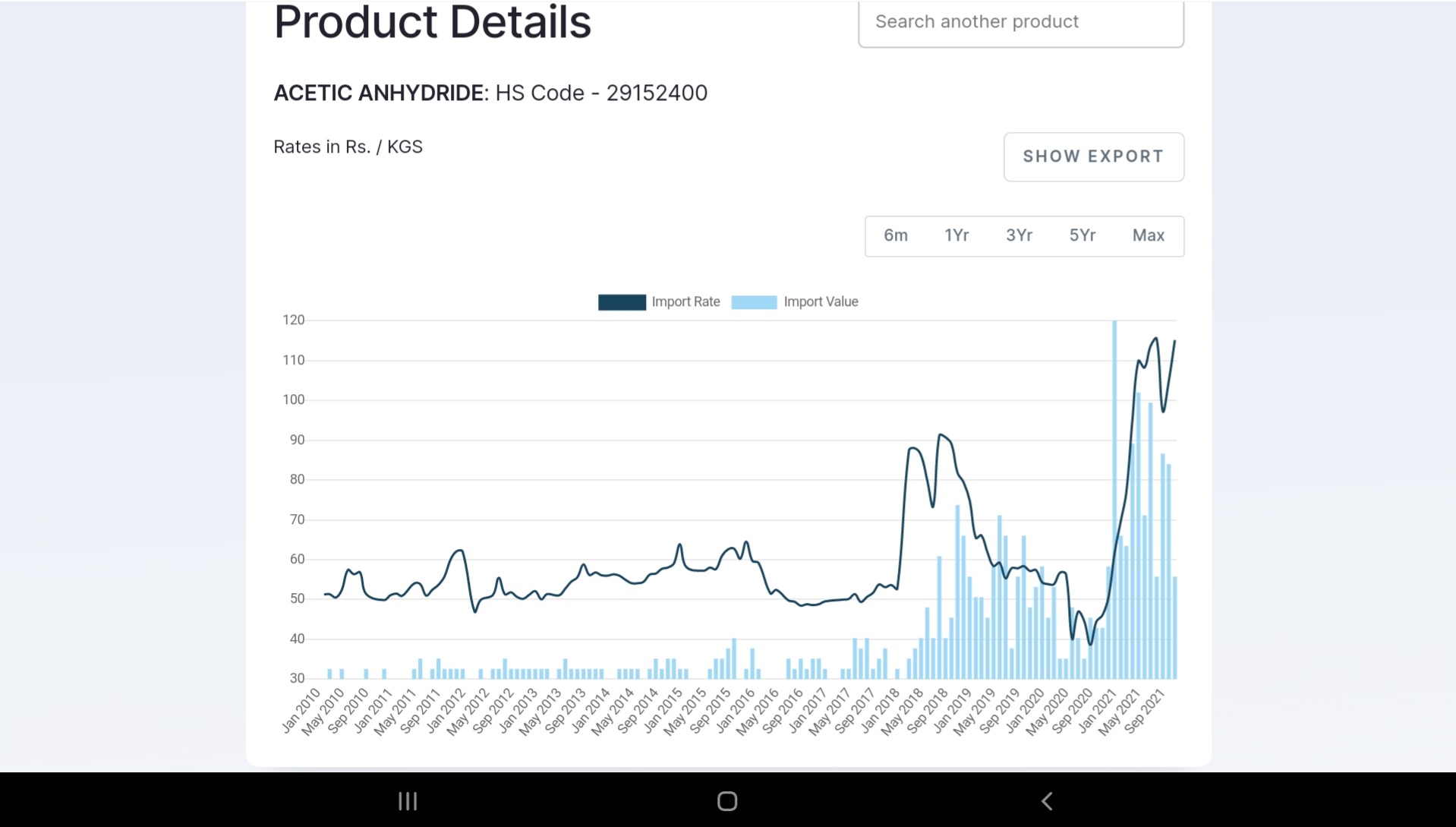

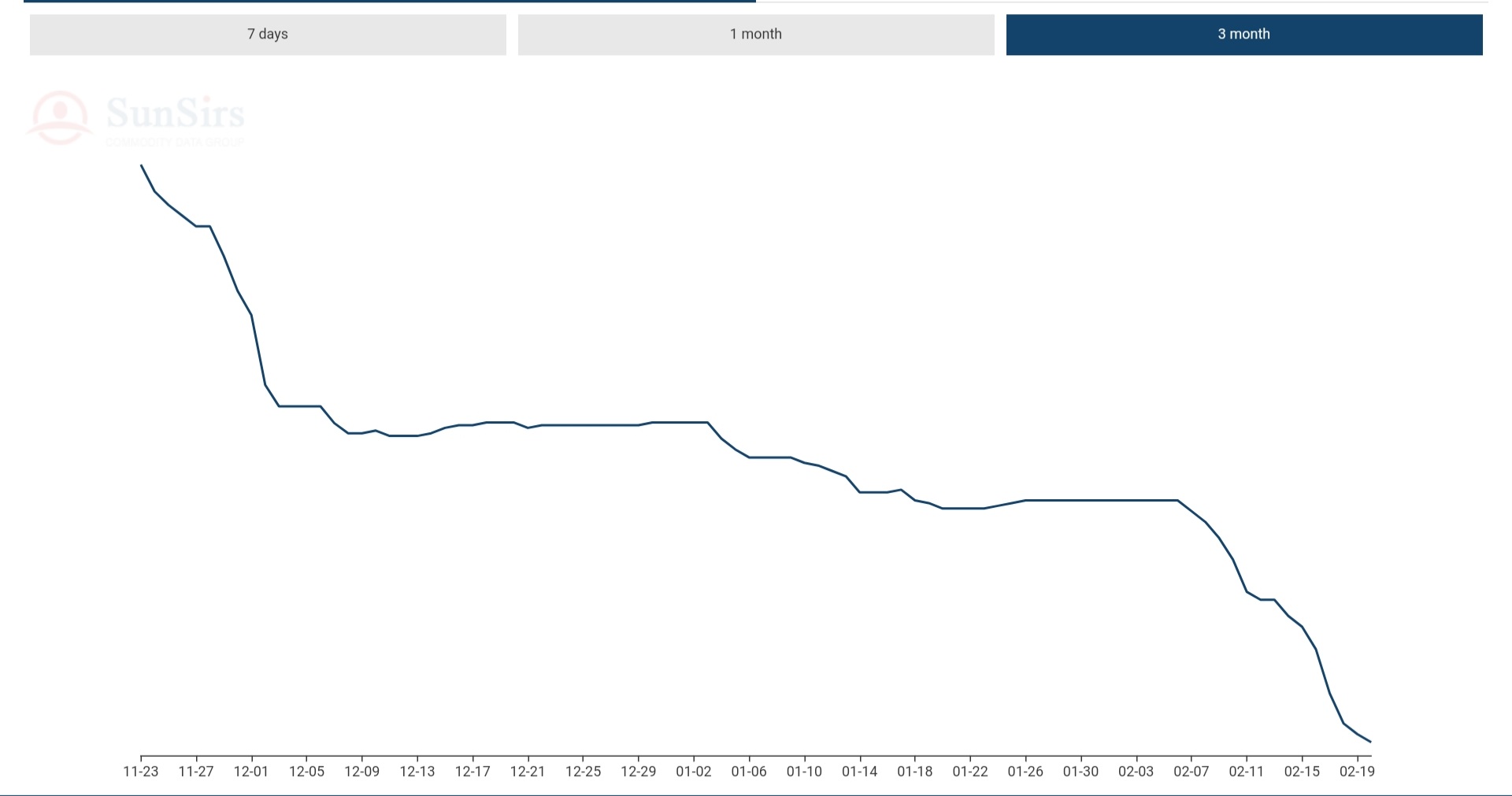

Ethyl acetate which is key RM has shown similar trend of price/kg having similar spaced out vallyes and troughs. We are currently at new peak and most likely to go downwards from here. However interesting point is on a longer horizon ( 10+ years), there is up trend. Also it’s HH and LH structure- meaning each valley after high is higher than last valley - thus base shifts slightly upwards.

How to validate above translated to Ingrevia reported numbers? Let’s look at ethyl acetate H1 21 prices ( avg 50/kg) vs H1 22 prices ( avg 100/ kg)- on average has been double per kg. - trend has been visible in H1 22 revenue numbers with LSC revenue near doubling.

For LSC - What market probably is factoring is the realization may drop to where it was pre corona ( or atleast closer to it), that means that LSI per qtr will be downwards range from recent 700 cr+ per qtr. Taking overall bottomline down as well.

Silver lining is that Sp chem and Nutrition are at 40% revenue for this quarter and have more predictable margins range and new Capex is tilted towards them – together they are 600 cr with 16-18% margins range at current run rate. Annualized 2400 cr and 450 cr+ EBDITA, excluding upcoming diketene in Q4 22. Next leg of 450 cr capex by FY23 and 350 cr already spent in this year - will add min 500 to 600 cr + diketene numbers in FY23 - that is 3000 cr+ revenue and 500 cr+ EBDITA for FY 23. Qualifies for 2.5X sales and 15X EBDITA conservatively thus mkt cap of 7500 cr for these two biz.

LSC biz will continue to be treated like a commodity biz - if at 1X sales ( don’t know honestly here) - 2000-3000 cr

Together 10-11K mkt cap on FY 23. Some decent upside from current 8K mkt cap. Some rerating possibilities if value Added products trajectory continues but believe it will be multi year process and patience. Need to remember that Optically H2 22 and H1 23 will look subdued YoY given higher base of commodity biz contributions

One key learning - keep any eye for Favorable market conditions and pricing in results update, its other way of saying we don’t have pricing power but enjoying temp gains.

Invested

34 Likes

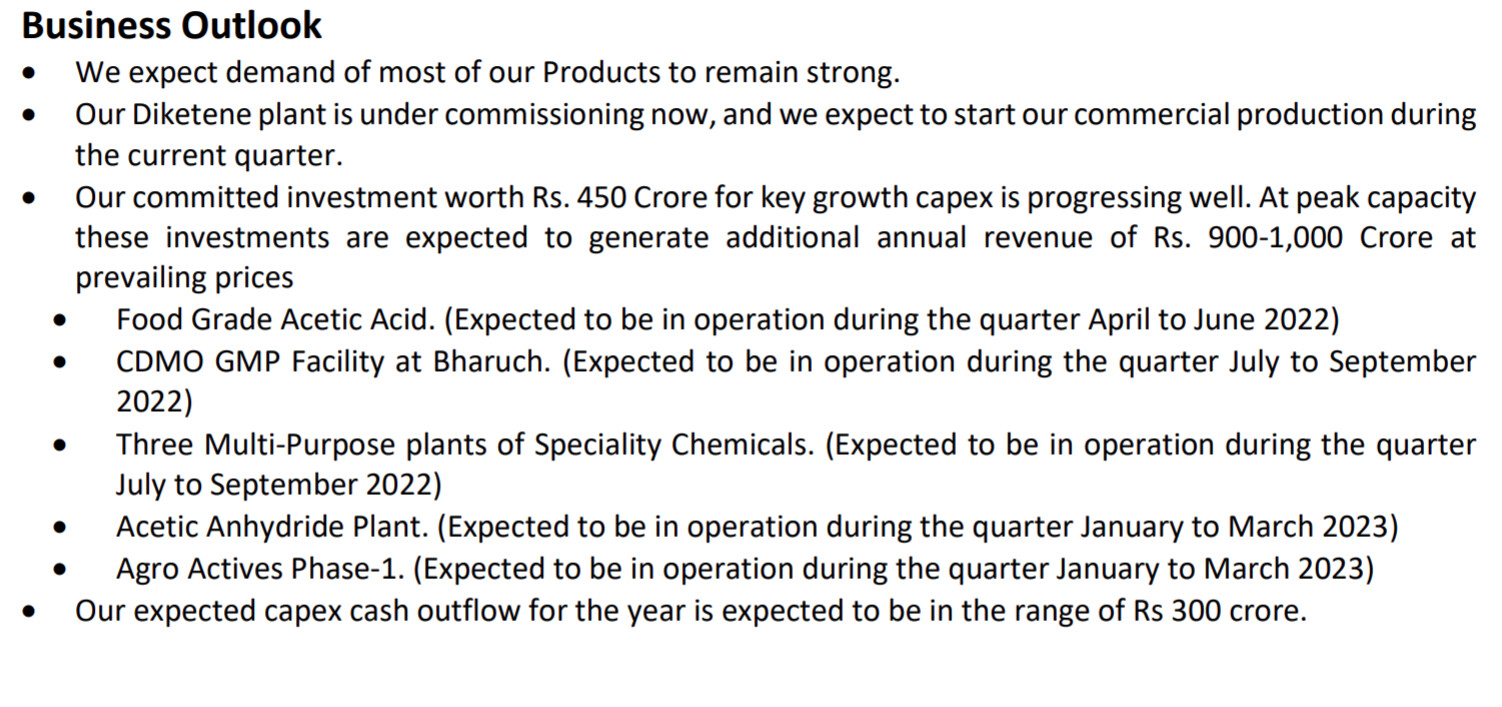

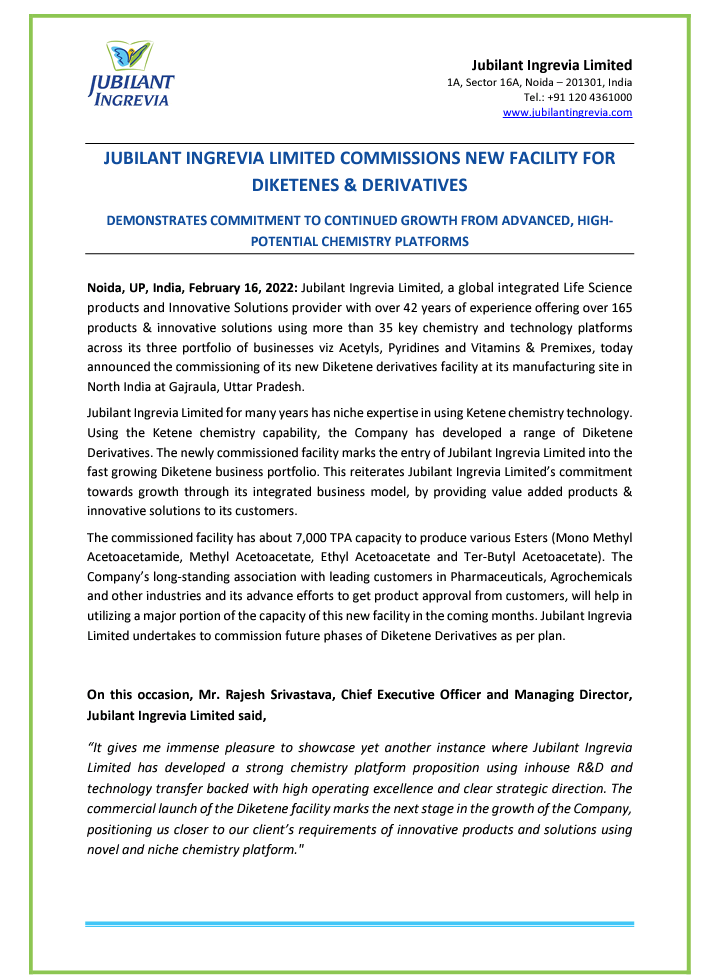

Any idea when the Diketene Plant is going to be commercialized and what can be the expected Revenue from the same ? Thanks.

1 Like

Decent set of results. Declared dividend of 2.5 Rs. Commentary in the ppt is quite optimistic.

Seems like mngmnt is working to improve its image in ESG as well.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/60a68cae-d3f9-43cb-b801-92020fc68c18.pdf

On Debt, Seems a large chunk of Long term papers were converted to short term & will be cleared off soon. Similar thing happened in Q1 as well, In few qtrs. I hope the debt will be almost gone.

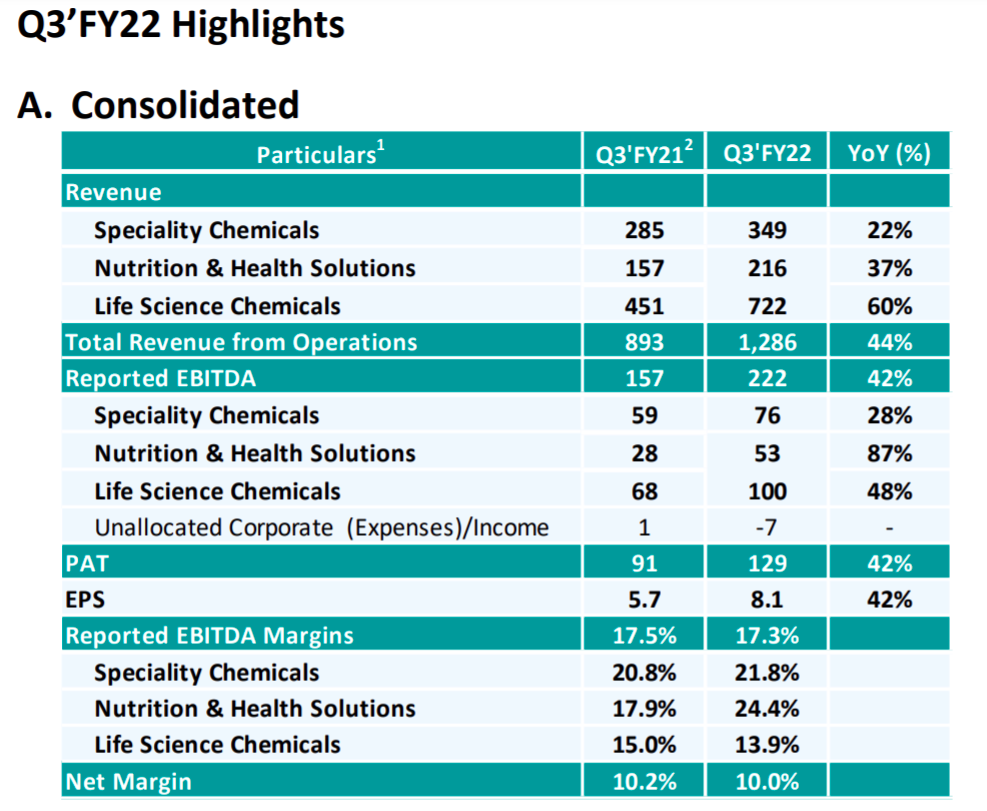

With 25 Rs EPS & 3.6 K Cr Topline, 712 Cr EBIDTA, for 9 months the runrate of this qrtr seems sustainable. However, The markets seem to be discounting a lot, don’t know what/why?

Disc : Invested & Biased

24 Likes

BCD on import of methanol and acetic acid reduced from 5% to 2.5% and 7.5% to 5% respectively. Marginal negative for GNFC, GSFC and Deepak Fertilizers. Positive for Laxmi Organics and Jubilant Ingrevia

6 Likes

Taking a stab at market discomfort around re-rating in line with peers( inferences based on concall of Ingrevia and peers)

Promoter/ leadership

-

Mgmt super conservative callout on doubling revenue from FY 21 base (3200 cr) to 6400 cr in FY 26 - FY 22 they are going to close around 4800 cr - suggests meagre growth ambitions of sub 10% CAGR - why even call out such statements - good thing is it was challenged in call, mgmt plans to revise it in near future updates.

-

Mgmt itself uses term of being nervous in giving Margin guidance, understandable given till now majority of revenue was commodity LSC( acetic anhydride and ethyl acetate etc) which had bumper favorable mkt price (2X of long term averages) in CY21, which mgmt and mkt knows are unsustainable

-

Capex beyond known/announced 450 cr - cashflow are much higher, debt is negligible, capacities are running at high (82% for Nutrition) and Dividend is being announced. Time for mgmt to unveil longer term capexes( almost all size chemical all are going aggressive with next 5+ years planned Capex- something similar is expected from Jubiliant ingrevia.

-

Promoters perception compared to say Deepak nitrite, Aarti and so on - Mkt seem more clear about narratives on peers- E.g. we all know Deepak Narrative of Right to win and import substitution theme, Aarti Benzene supremacy and pioneer in muti year mega contracts + 2-3 times rev/profit guidance driven by heavy capex. Most of mgmt are giving calibrated media presence, core focus is chemical/chemistries - can same thing be said for Bhartiya brothers? Softer aspects but does matter when one needs identity in China+1 theme to stand out and get recognized. This may change/improve over time but does reflect relatively lower institutional holdings( strong hands) in Ingrevia. Would not hurt to communicate little bit more, share longer term aspirations, be bit more pro active on growth ambitions.

How does future looks like in number

*Current mix is 55:45 for commodity : Sp chem - they will be comfortable with 20% EBDITA with future capex coming online though and mix going to 70:30 type. Data points suggests that this commodity part of biz is still enjoying favorable conditions ( mkt driven prices), not something that can be taken as sustainable.

Good thing is that them spreads are always stable, per budget 22, inputs price ( acetic acid) will correct with custom duty cut, Chinese capacities are back online so we can believe that we are not in inflated market condition they enjoyed in CY 21, between next few qtrs a sustainable number should emerge .

LSC conservative realization- To be conservative one can assume 75-85 cr/qtr number for profits from LSC( closer to multi year and Q3 FY21 realization of 60-65/KG range than Q3 22 of 100-120/KG range) - I.e. **350-400 cr annual runrate EBDITA on current capacities for LSC **

Here are long term price ranges

- Q3 22, Spec chem and Nutrition annualized run rate this qtr is 76 cr and 53 cr EBDITA- per mgmt commentary there is no favorable price angle to it, it is with volume+ prices , healthy demand and increasing value add mix trend for future - together they can deliver about 500 cr EBDITA on annualized basis. capex are coming online almost each qtr from here on.

Valuation

FY22 snapshot

-

LSC - 350-400 cr commodity biz EBDITA at lower band of realization - (note actual numbers will be much higher but we are baking worst case numbers at long term realization per above)

-

500 cr spec chem and Nutrition biz EBDITA - majority focus for future capex is here.

-

Current ongoing capex to add 900 cr revenue in next 2 year per mgmt + Diketene revenue of 300 cr( phase 1 and phase 2 together) = 1200 cr by FY 24 - given majority is for Higher margin biz( spec chem and Nutrition) - approx 300 cr for LSC and 900 cr for higher margins spec chem+nutrition. In addition, Normal debottlenecking and capacity utilization to add normal 10% growth on Fy 22 base.

FY 24 will look more likely below post ongoing Capex

- Spec chem and Nutrition at 700-800cr+ EBDITA - Base case of 15X EBDITA at 11000 cr, optimist case of 20X EBDITA at 15000 cr

- LSC 450-500 cr EBDITA - Base case of 8X EBDITA at 4000 cr and optimist case of 10X EBDITA at 5000 cr( again keeping very low realization inline with pre corona)

FY 24 Base case mkt cap 15000cr and optimist 20000 cr.- current mkt cap is 9500cr

This is back of envelope and could be off and management is likely to announce more capex given much higher cashflow.

Numbers are relatively visible, Narrative hopefully should evolve as well.

Invested from lower levels and adding in dips.

45 Likes

Have you changed your allocation to the company due to their attitude towards pollution compliance? I have been following the company and this is the only thing preventing from buying this dip…Fellow boarders have also brought to light what might be their change in attitude. Would like to know what you think about this?

1 Like

Seems market was right in anticipation of LSC realization mean reverting - key input - acetic acid price on downhill( and so will Ingrevia LSC products), Long term avg price based realization was visible in Q3 21 LSC performance. ( 68 Cr EBDITA), short term Volatility likely.

4 Likes

Hi @Dev_S thank you for the charts - is this data public, I’ve also been trying to find source of this data, without success.

Is there a better/more efficient process to manufacture acetic acid (like GNFC claims here Indian Acetic Acid Market Analysis I Prices I Forecast I) vs Jub Ingrevia/Laxmi Org’s process.

Thank you

Sharing my views would be glad if any senior members can also throw some light on current prices of acetic acid and the impact of that on lsi business

Some of the Negatives for lsi business

This qtr acetic acid prices fallen by about 30%

One of the major company producing acetic acid in china has restarted production so this can be a big negative for ingrevia

Nutrition business can have minor impact since vitamin intakes will be back to pre covid levels

Only positive diketene plant has been commissioned which can have some positive impact on sales

Overall Expecting this qtrs eps in the range of 6.0-6.5 rs which is 20% lower then previous qtr…

Disc

Recently Invested and adding on every dips

3 Likes

Acetic Acid is their raw material , What they sell is Ethyl Acetate and Acetic Anhydride. If they can maintain same profit margins in absolute terms (not %tage terms ) with similar volumes of sale , there wont be any impact on profit numbers.

9 Likes

So to earn same profit margins in absolute terms they will have to increase there volumes or increase there profit margins…

as per my understanding depending upon acetic acid prices this qtrs ethyl acetate and anhydride prices will also be lesses hence profit on absolute number will be impacted…

we have seen in past when the prices were lower there sales and np also was lesser…

1 Like

Please help me understand as to why the profit will be lower? As per my understanding, there sales number may get impacted due to fall in prices of raw material (Acetic acid), impact on profit should depend on prices of there end products right??

I remember management saying that in q1- margins in life science business was higher (27%) because of sudden spike in Acetic acid prices while they had inventory at low cost leading to inventory gain. Margins of speciality chemicals were under pressure due to high input cost. And now the situation is the opposite. The company might incur inventory loss in life science business due to falling acetic acid prices while at the same time may report better margins in speciality chemical because of low input cost (if the end product prices remains high). Is my understanding correct?

3 Likes

I have the same confusion.

Last qtr if we see 100 crores ebitda came from life science business…so major portion is from this business and this will be impacted due to lower prices of ethyl acetate and anhydride…

Speciality chemical yes they might benefit due to lower input cost

Nutrition business i feel will be lower then previous qtr due to geo political problems in eu…there major chunk comes from eu

3 Likes