At PE of 15 it is the most reasonably priced FMCG stock available at Indian bourses. ITC has long runway for growth, non cigarette FMCG basket may surprise the market positively in next five years.

Only negatives with the company are a couple of businesses with low ROCE like hotels & paper etc. but company is trying to increase the ROCE of these businesses e.g. in hotels by increasing the managed hotels in future than investing in new ones.

Investors with investment horizon of more than five years, ITC with 3% dividend yield & PE of 15 times with brands like Ashirwad, Sunfeast, savlon, B natural,bingo, yippee etc is a good buy even at current price.

Disclosure: I have investment in ITC & my views may be biased. Not a recommendation & am not a SEBI registered advisor. Reader must do his own research before investing in this script.

ITC has intimated that it will give 80-85% dividend pay out in the coming years.14500 Cr X 0.8 = 11600 Cr payout with no DDT. Hence Div yield = 11600*100/227400 = 5.1%. its no longer 3% yield.

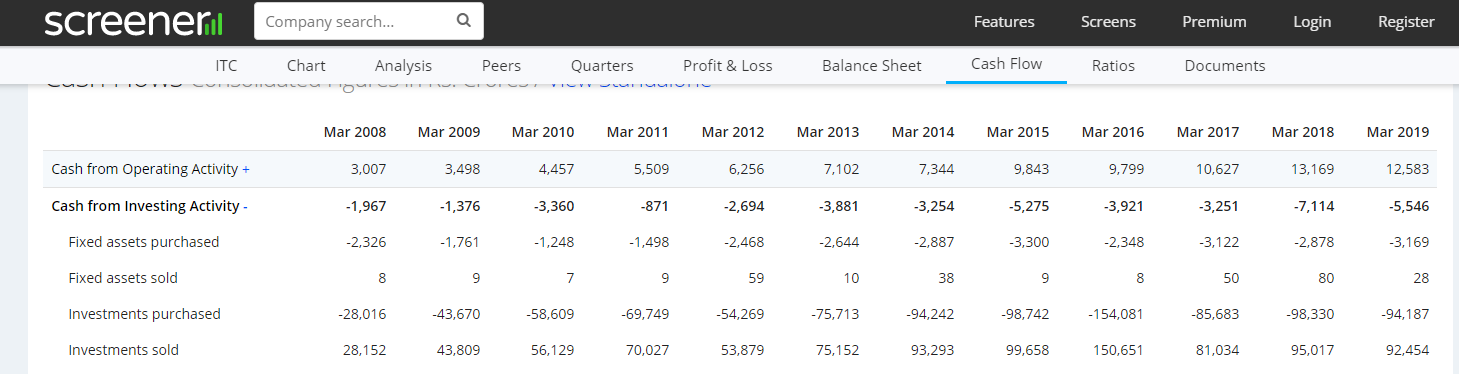

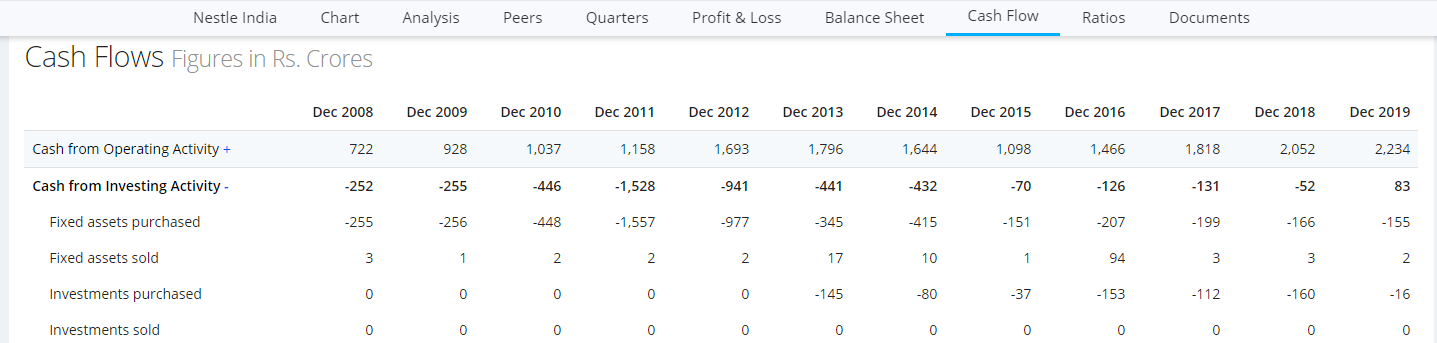

Hi All, Trying to understand ITC cashflow statement and wondering why does ITC have huge cash investments and sales each year… it does not seem standard industry practice, eg. Nestle has very few over the years

eg. Mar 19 ITC Investments purchased -94,187 while investments sold 92,454 while for Nestle the latest figures available for Dec 19 are -16 and 0

I also have the same query. How the investments purchased during the year and investments sold are the almost same during the year? From the basic accountancy that I understand, under cash flow from investing activities you show investments purchased where cash is an outflow and investments sold, where cash is an inflow. But when both are same do they have policy of keeping money in short term low risk investments where purchase and sales comes to same during the year.

Also I have come across from various reports on the FMCG others revenues and margins. But is there anywhere I can find the break up of FMCG -others profit/loss statement to find out how the margins are so low. There is no debt for any interest expense, don’t find them spending on advertising as others do. Then where are they losing out.

Normally money is parked in short term and long term paper For investment by managment . So the amount of short term paper held on last account closure date would mature during the year. Depending on assessment of situation management would decide whether to reinvestment and what amount to reinvest in next year and hence nothing unusual In My opinion, to find kind of matching entry in cashflow.

On second point about low margin, most of brands which gets developed in FMCG has long gestation period. Initial 10-15 years are heavy expenditure on brand building and distribution. Once it break even, then profitability is very high.

In case of ITC, they virtually has nil presence and non cigarette-brands till 2005. Most of brand building efforts started after 2005. So please look at ROCE and PBIT margin of Non Cigarette FMCG business. For almost decade, that business was loss making and now since 3-4 years has turned around and started contributing positively with improving tread every year.

Also, another perspective could be ITC being focus to capture market share first place and get sufficient penetration before investing worrying about profitability. They also have good cashflow and profitability in cigarette business which place them relatively better to offer good value for money. While it may be true and I am not expert to confirm same, I generally like business which are run with equal weightage on profitability and market share as both are critical for success of FMCG. Whether ITC has capability of milking brand after developing third largest Distribution reach in India, only time will tell.

Each investor need to look at his her risk return profile, valuation and portfolio allocation before making any investment decision. Ideas are simple to borrow, conviction is difficult. True test of conviction is adverse situation at weakest point it assist you to held on investment.

Discl: Among top 3 holding and view may be biased. Not a SEBI registered advisor, not recommending any investment action.

Totally agree. The central theme behind investing in ITC is a.) Longevity of their business b.) Making successful transition from cigarette to FMCG. One has to remember that even if ITC becomes very profitable FMCG business still part of the business earns money from cigarette business. So they have deep pocket to invest and can sustain long period of pain during brand building process. It is unreasonable from our side to compare ITC to other established FMCG companies like Nestle, HUL , Marico or Godrej etc. They are all veteran in the space and have been around for more than few decades. No matter how much we talk about ITC, ultimately narrative points to the same place - ITC as FMCG. So one has to take conscious call while investing in ITC : do I have the mental ability to stay without seeing any return for long period.

I finally entered ITC in a huge way during the recent crash and I’ve continued to add in dips since. The change in dividend policy is huge. It finally means they’ll stop throwing cash at hotels! That’s the only thing I never liked about ITC… however, maybe in a few years the hotels will start contributing too. They’ve used profits from cigarettes over the past decade to create an entire Fmcg arm from scratch and even create an agri business to help decrease costs for their Fmcg. It’s been a rough decade for investors in ITC (though tbf they did benefit from bonus and hence increased dividends). However, now is the time to buy. Investors over the next decade in ITC will see far more returns than investors over the past decade.

Disc: it now has 33 percent of my blue chip fire and forget portfolio.

very nice discussions. But still would like to know though the question may sound naive. The margins are not been generated as a result of what? Generally a company gives up its margins when it wants to increase its market share. We can see that in the case of Ola, Uber where lot of vouchers, free rides, lower charges per kms were fixed to gain market share. In these cases, the fixed cost may remain the same.

In the case of ITC, is the margins under pressure on account of selling the products at lower price to gain market or from the cost/expenses front. When established players are enjoying 20% margins surprising to see ITC at 3%

As already discussed on business, it is very difficult to set up FMCG business. Maintaining and establishing Distribution along with proper marketing and logistic are key to success. Even in case of Hindustan Unilver, the present Return on equity which we see, are more of mature brands and distribution milking. In early 1970, even Hindustan Unilever has 9-11% Return of equity. The data has limitation as I do not past detail financials of Hindustan Lever (except book value and EPS, which make calculation of RONW possible).

The limited point is setting a profit making business is very difficult and time consuming process. However, once scale is achieved, the profit and return is phenomenol. I shall try working similarly on Nestle to get more insight.

Enclosing excel file of working. Please refer to HLL RONW worksheet for calculation and BSE price 1959 for actual data and sources.

Everyone has right to commit error and hence I would like do my work and consider risk return profile and finally invest. At least, I would blame or take credit for whatever outcome. While appreciate Mr Damodaran and also learnt a lot from his books on valuation (during my MBA days), still would advise against blindly following ANYONE.

In past, Mr Damodaran was optimistic on Eicher at around 30,000 in July 2017, which was near peak. Of course, the context was to explain not to invest only based on PE and hence one shall not read too much. However, just wanted to put as a caution that everyone has right to be wrong and stock market and we shall take investment only after understanding same.

COVID-19 has made itself an unwelcome and seemingly permanent guest. While it might seem like an incredible inconvenience, “We have got to run our businesses and lives and carry on with economic activity,” states Puri, with absolute certainty. Well, we are not giving up to coronavirus without a fight and if it means adapting to a seemingly new normal, then so be it!

No crisis comes without a challenge, unfortunately impacting everyone differently. But every challenge has a winner, especially those who find silver linings and opportunities in the darkest times. ITC Limited has struck solid gold with the FMCG sector, with demand for trusted brands at an all-time high.

If you see their launches it seems that they have their fingers in too many pies. Some of the products to me doesn’t seem to be having a mass appeal. This is one point where I don’t like this company. They shd focus on strengthening known brands than getting into everything

Other way to look at this is, they are a cash-rich company in tough times, maybe they are just trying to obtain the “first-mover” advantage in the niche FMCGs.

At times when almost all companies are trying to preserve cash, they are building up their product portfolio.

Nestle did the same thing with their Poha offering.

Can anyone help with what is the revenues and profits of FMCG other than cigarette of ITC for each of the last three quarters. Would be of great help. Thanks in advance