On lighter note, I think they wanted it to rhyme with the leader in dish washer - VIM

Between good to see Marico leading the pack in innovation. A small homegrown FMCG showing the way. Also, a little disappointed with the business enviornment in India where herd mentality is going on. It shows the clear lack of business moat in any of the firms. Lack of superior innovation, which is hard to follow as well.

Herd mentality in Sanitizers, disinfectants and now in vegetable wash also. I think very few companies products are hygiene/nutrition related where they truly enjoy a moat and innovation hard to copy. Some example - Dabur for chyawanprash and ayurvedic innovations, Patanjali Ayurved, Reckitt - Dettol as leader, Amway - Nutrilite etc. Would be good to know any other company having a product/category hard to copy?

Other all depend on supply chain and availability only.

I don’t think any of moats you mentioned match up to the moat created by Marico in coconut oil. I don’t think anyone even knows any competitor to Parachute oil in the segment. Other coconut oil package also follow same packing as Parachute to make people aware that it is coconut oil bottle ane their moat is so strong that people directly consider any other coconut oil to be counterfeit of parachute.

Agreed, I was talking about moats for consumer companies, specially FMCG for post covid era…parachute is a strong brand even before for coconut oil as well as today. I was thinking, can any FMCG company brand become a game changer in next year or so to swarm ahead of the pack in growth…or even in consumer discretionary…

Eg of such transformational brand is say a surge in gym bikes and services offered in US like peloton, Netflix again in US, Amazon etc. Do we have any such consumer facing companies with superior moats that would grow manifold in postcovid era? Thanks

Yes. And it could also mean that the business does not need the money even if it has growth opportunities because either the growth requires no capital or that the growth can be funded with other people’s money - preferably customers or vendors and not lenders

A simple and predictable business with long history and still long way to go. Definitely it fits in the consistent compounder list.It definitely has got moat but the thing I like most here is the longetivity. It is the ‘n’ in the formula of compounding which creates magic. It is visible here. And again as they say the entry price decides the quantum of wealth you create. I think all criteria of wealth creation fits here. (These are my personal views and I have got all rights to be wrong and these are in no way recommendation for anybody.) I have compiled some data from 1992 to 2020. After seeing the data there was a smile on my face seeing the way the company has progressed be it any problem. Tried to find data from 1965 to 1992 but didnt get it if any body can find it, the file would be complete. Thing I noted here is the market capitalisation of 2003 is equal to current PAT of the company. Now imagine the effect of this on dividend . I think this file says everything nothing to add more. ITC history.xlsx (15.6 KB)

Let me give my simple personal opinion, Why should a business be run ? PROFIT , thats the final end result.

Look at the below chart and the comparison between the market cap and net profit, ITC makes the max profit of 12592 Cr against the market cap of 241788 Cr and a PE of 16. Also like it or not, there is a cash machine in background a sin business Cigarettes (habit forming business) which always brings the money. Plus the FMCG business is no more a new business they have brands which are already market leaders, also some brands are very well known to the public.

Now let’s take the other names such as the NESTLE : 167836.14 cr market cap 1969.55 cr net profit, at 82PE, HUL : 498222 cr market cap 6054 cr net profit, at 72PE.

For sure NESTLE and HUL are quality companies and market leaders, but my sense is that they are being traded at very expensive valuations and the market will soon realise this and auto correct.

ITC looks to be a good bet at this valuations.

The only other way i see to get into a good quality FMCG business is to go the Bombay Burmah way where you can a claim to 50% of shares in Britannia for 6954 cr market cap vs 888 cr net profit at PE of 6.33

I would suggest in case you interested into discussing more about Britannia or Bombay Burmah, please take discussion that thread. While I appreciate your viewpoint about taking indirect way to get benefit from Britannia by way of investing in Bombay Burmah, one need to consider two factors while exploring Bombay Burmah in my opinion:

Trust in Management of Wadia. The management has widely misallocated resources of the company. Even in Britannia, otherwise very good business, analyst continued to seek details about ICD between/among group companies and that being highlighed by analyst even on conference call. So, one need to check properly before investing. Ness Wadia: Ness Wadia sent to two years in jail in Japan over drugs possession: Report

The structure in which the shares of Britannia being held by Bombay Burmah. Find enclosed details in My understanding.

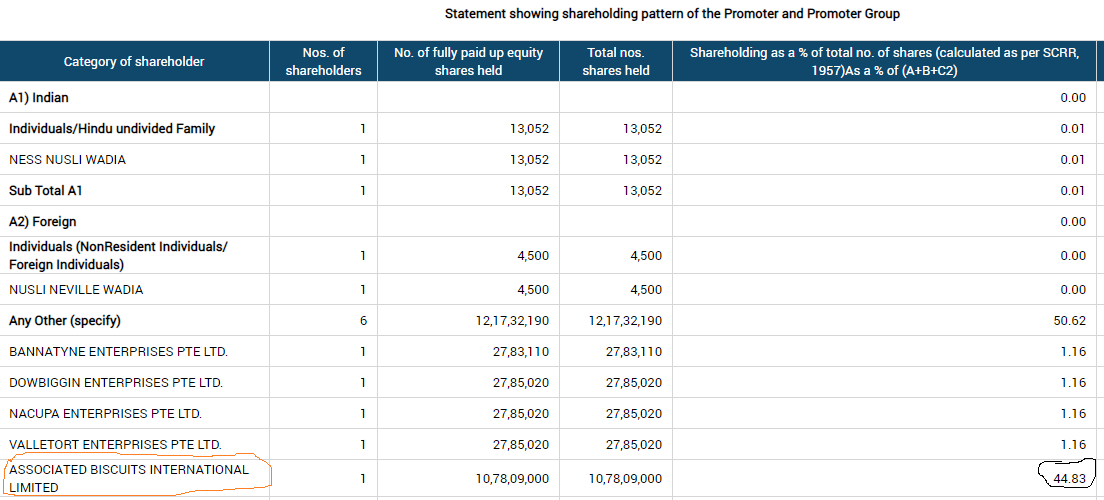

Brtiannnia Promoter holding as per BSE March 2020:

Nearly 45% holding of Britannia is held by Associated Biscuits International Limited.

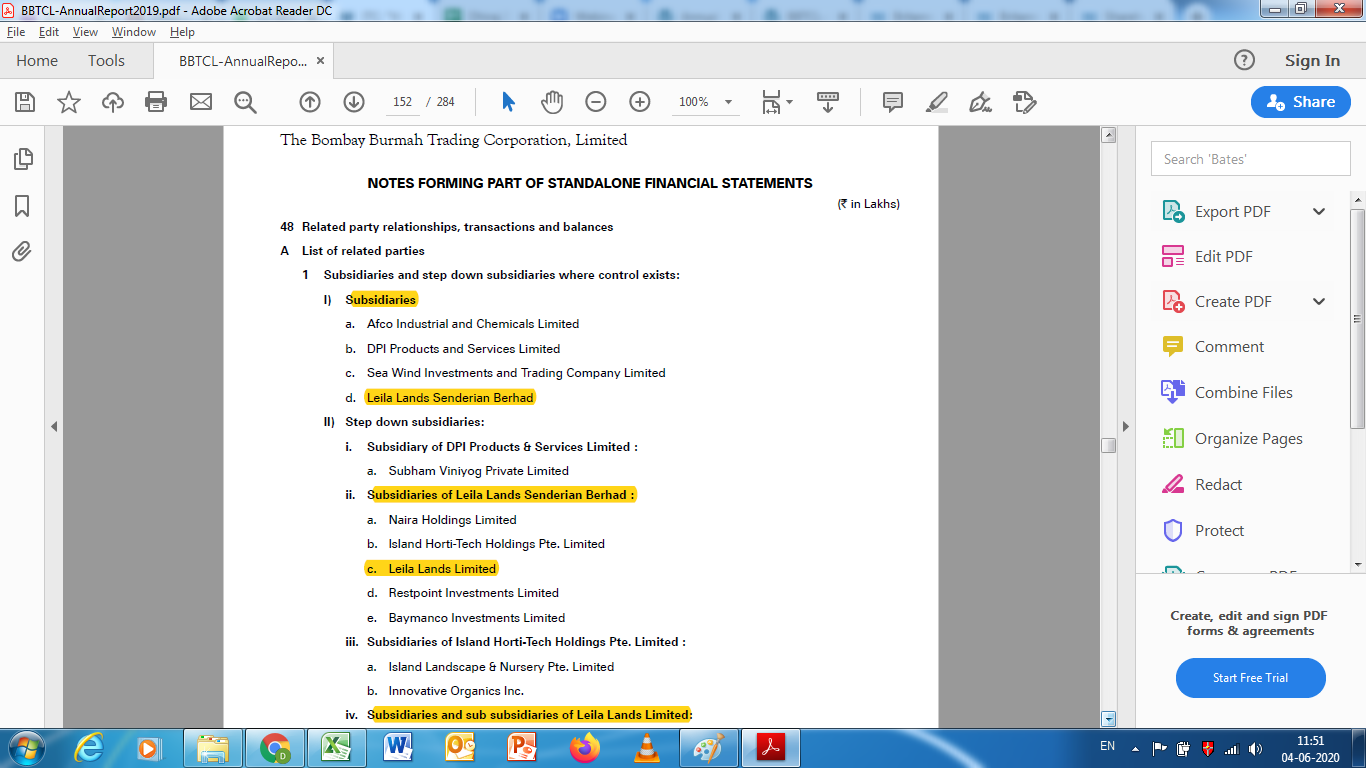

Now look at structure in which finally, Bombay Burmah (or Wadia Group ) hold thesse shares. I am enclosing same from Bombay Burmah annual report FY19 (Page 150).

One need to take into considerasation of various jurisdiction and tax impact of same when it finally come to Bombay Burmah (assuming all shares are liquidated by the promoters and funds are move upwards to Bombay Burmah).

Bombay Burmah has subsidiary Leila Lands Sanderian Berhad based out of Malaysia holds 100% shares in Leila Lands Limited in Mauritius which holds 100% shares in ABI Holding Limited in UK which holds 100% shares in Associated Biscuits International Limited in UK which in turn hold ~45% shares in Britannia Industries Limited.

Given the kind of long structure, I feel market would continue to face higher discounting for the holding in Britannia which I find approprate.

In case @JJoy or other members have any suggestion on Britannia or other company, or on this post, I would request them to post on resprective thread, so that we can keep this thread to ITC and related players/peer/competitors.

Discl: Have token position in Britannia, Not a SEBI Registered advisor, Not recommeding any investment. My view may be biased.

Hey, I’m surprised on your @dd1474 conclusion that i was diverting from ITC, throughout the post i was giving a comparison of ITC with other FMCG names to make a point.

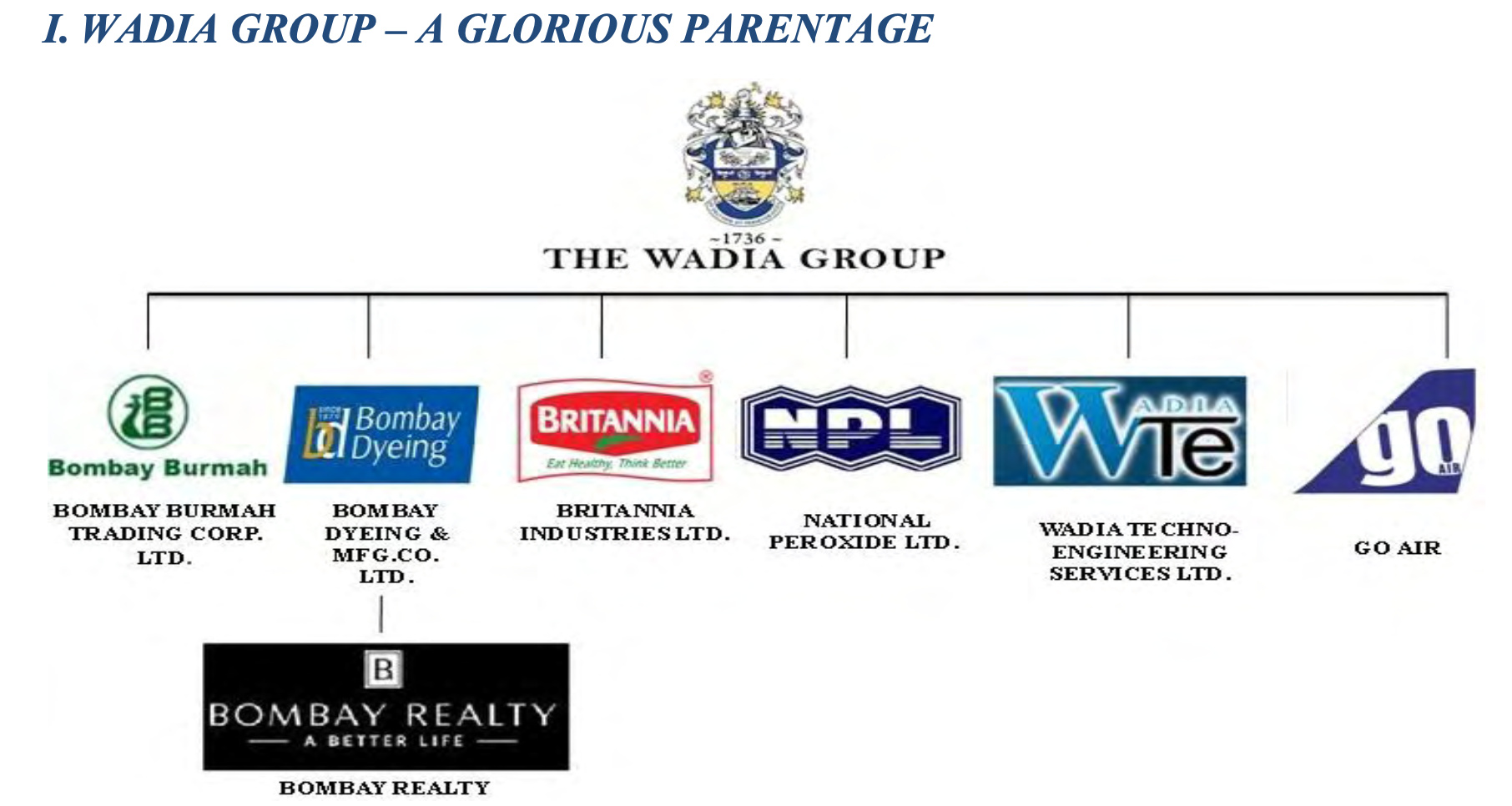

Now the owners Bombay Burmah, Wadia’s are not beginners , they are in business from 1736 i.e 280 years, They have created business such as Britannia, goAir and Bombay Dyeing to name a few from scratch. Off course there are cases registered against Ness Wadia, however he is the great-grandson of the founder of Pakistan - Muhammad Ali Jinnah. Finally he will emerge as a true businessman.

@JJoy

I appreciate you view point and also efforts to do peer comparison of ITC and other players. I am glad that you contributed that. However, invariably, once other name appear on message board, I find that related discussion on that company appear on main board. It is perfectly fine to discuss ITC with peer, but I suspect than soon we would have multiple post on Britannia and other peers on ITC board which is not useful to any one and also out of context. Hence, this was more of pro-active suggestion to keep thread relevant and not to discourage discussion. The second message about Wadia group history I would request you to post of Britannia thread where it would be important then on ITC thread.

By no mean I would like to undermine your contribution. My only endvour is to keep thread contextual. If you read this thread even in pat we have some message on sin product and other related points. It is critical for evaluation of ITC but it is also not the only critical factor and there various other points which shall be considered. I have raised my concern on that point as well.

My apology if my message being harsh but wanted to maintain sanity of thread. Increasingly finding that threads have same point repeated which was covered in past because reader did not have time to go through 200 messages. Just wanted to avoid that and hope you appreciate that.

I also request members which are for and against this point, please express their view by like to message which they support rather than writing another post (unless you bring out another perspective). The test of that is to assume you visit this thread after two years and you read around 700 messages on thread! If you like reading what you write-now then only please put message. Let us all of us word more frugally.

They might want to show that their prices are lower than Jonson and Johnson. However believe me, J&J has way more brand strength these guys and also there are many cheaper alternatives available.

From my personal experience I can tell you that I can only see Savlon’s availability (in Kolkata) and product range increase in the last few years. Savlon used to be quite visible in the late 90s but then almost disappeared from the selves of Kinara stores and supermarkets at least my locality.

That said I feel that there is still a lot to be done on Savlon. ITC doesn’t spend much A&P on Savlon that it spends on Vivel, Fiama, Bingo etc. So, I agree with you that promotion on Savlon was lacking but availability increased certainly. Hope that will change after COVID as Savlon is at the forefront of ITC’s hygiene portfolio.

Disc: invested in ITC and a loyal Savlon user from 90’s (never liked Dettol). I used to be disappointed seeing it disappear from my locality & switched to Suthol for few years & now came back again to Savlon. I had no idea about the brand owner of Savlon before I started reading about ITC.