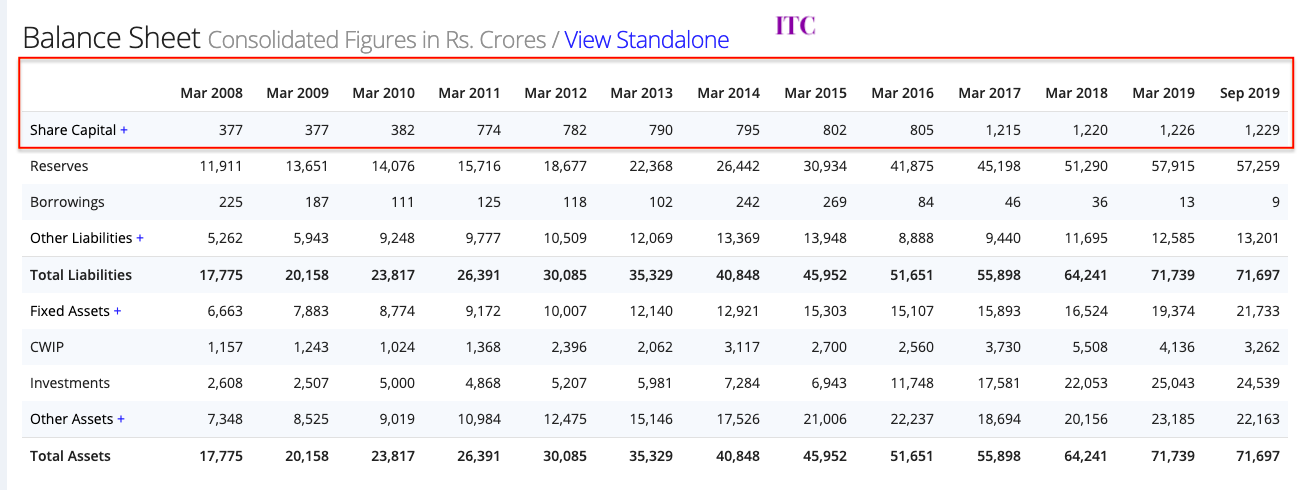

“ITC has free cash worth HUL’s, Nestle’s, Dabur’s and Marico’s free cash combined.”

It shows how fundametally strong the company is.And from this year onwards out of this 80-85% will be distributed as dividends(Assuming that it will be mostly same as profit).

The EBIDTA margins should improve for ITC FMCG division from nowonwards as their FMCG contribution from packaged food is more(Ashirwad,Bingo,Yippe,Candyman,newly aquired Sunrise spices).

I genuinely thought that disinfectant spray was not going work. Savlon disinfectant spray is getting good attraction. Also ITC has first mover advantage. Price is also cheap. 5K+ ratting in very short time.

Lifebuoy has also launched similar product but price is too high, 149 INR for 75 ml.

Ending a seven-year dispute between two FMCG majors over use of ‘Magic Masala’ and ‘Magical Masala’ as expressions to market their noodles brands, the Madras High Court said they are common English and Indian words and both the companies cannot claim monopoly over them as these words are laudatory and common to the trade.

I always believe that the odds of market being right about a stock is high at most of the time. Market is valuing it cheap for several reasons including the stake sale by Govt and LIC, resulting in excess supply. No buyback on account of BAT taking control. Also ESG norms are not letting funds buy it. So this low valuations may remain here for long long time, stock price may fall much further and test patience. The stock being available at very good value with enough margin of safety was heard when it was 220, 200, 180. But it reached till 145. We dont know it may again fall further. Already not given any return in last 10 years. Also the cigarette business wont do good as volumes are shrinking and millennials prefer a drink over a smoke (may be wrong here, sample is among ppl i know) and the regulatory hurdles. So any positive on cigarette business may do good needs to be discounted.

The only ray of hope is the FMCG others showing improvements in margins. If this does, then its a gold mine. Only market may know when that may/may not happen. The companies against which it is competing has been for ages, so it may not be as easy as one thinks. But atleast in India, a growing young market, one doesnt have to snatch share of others pie as the entire pie is likely to grow, letting every one have their share. If one thinks this as a 5 year Bank FD and remains invested, then may be a good bet.

In my view any meaningful unlocking of value for shareholder, can be achieved by demerging the business heads and listing them.5 new stocks…ITC Cigarettes,ITC Hotels,ITC FMCG,ITC Agro and ITC Paper &Packaging.And each stocks will be traded at their industry valuation.Even they can trade at premium as they belong to ITC group.

I think it’s high time board looks into it and each business is matured enough to sustain on it’s own.

ESG norms are not letting funds buy it. So this low valuations may remain here for long long time, stock price may fall much further and test patience.

The only ray of hope is the FMCG others showing improvements in margins. If this does, then its a gold mine.

What happens if FMCG starts picking up? Would it stop being a sin stock?

I am sure revenues from cigarette are here to stay for a long long time.

I am sorry, don’t know a lot about ESG screening criterias and companies qualify for it.

After all the years of pain waiting for this moment… ie the end of capex on hotels, the blossoming of the Fmcg brands and the increase in dividends payout why would anyone want it to split now? The whole point in investors staying on the ship for the past decade was to wait for this moment. It’s basically a machine that prints money from cigarettes and now will soon print money from fmcg. Just look at its free cash flows too. In a few years Fmcg revenue will overtake cigarette revenue and all the FIIs will come running back

Exactly. People keep talking about agro and packaging being a waste but it’s one of the smartest moves I’ve seen made by an Fmcg company. Imagine being almost full self sufficient with cash coming in from cigarettes , cash used on agro and packaging (which will also provide revenues) and this in turn saving costs on Fmcg products. It’s the perfect business model. I’ve just never understood where the hotel’s came on. Maybe they want to sell their cigarettes and Fmcg products there lol but like you said it’s a small part of the revenue so for now it doesn’t matter. I’m scared by how big ITC can become.

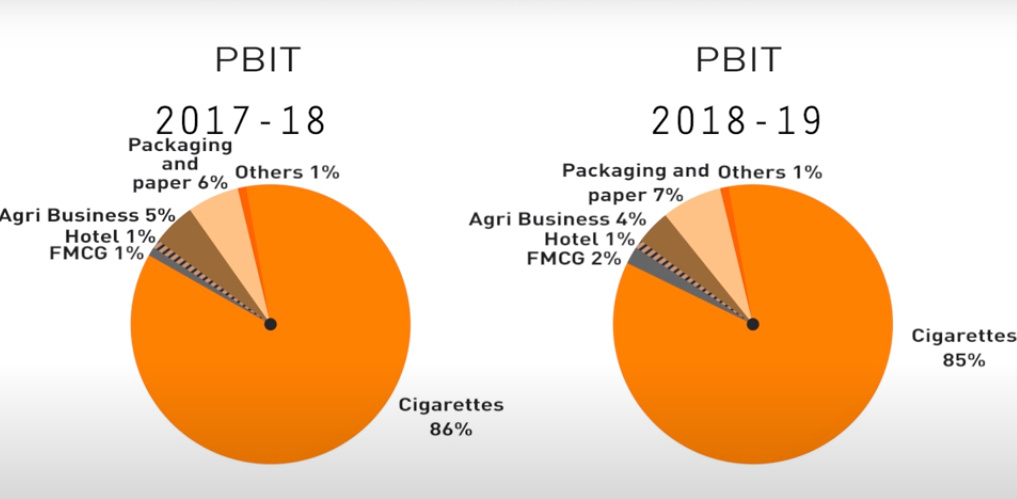

Yes I agree revenue form FMCG will surpass cigarette revenue at some point of time in future.But how much will it contribute to the bottom-line?Just to give you an example PBIT comparison for 2017-18 and 2018-19.In the said time period the revenue from cigarettes have decreased from 47% to 42%(approximate figures) to the overall revenue.So there was increase of 5% revenue of non cigarette business and how much it has attributed to increase in profits??only 1%.

so how much revenue and time will take for ITC to compensate the loss in profit from cigarette business by other businesses.Even if we consider the gestation period for many brands are over,1% effect in the bottomline can increase to 2% or Max 3%.So Just imagine how many years it will take for ITC to match the profits it gets from cigarette business to be matched by non cigarettes business.

As we all know the ROCE on an consolidated basis has decreased from 45.74(2015) to 31.88(2019) because of stagnating profits from cigarette business and non cigarettes business is in no way match to it at this juncture.This will reverse but not in near future,will take much more time in my opinion.

You have brought up a very interesting aspects from this data.If I say that even though cigarettes revenue had come down by 5%, the profitability has come down by only 1%.That simply means the smoking is not going to go away whatever the price of product and therefore major profits of this company from tis business would remain for much longer than any one believes.As a shareholder, we should only be concerned about the longevity of business with profitability. Is it a right conclusion to draw for the pictorial data provided by you ? Your views PL

In fact after reading various articles, data suggests that cigarette consumption has not gone down in INDIA.But there is a catch,the legal cigarette consumption has gone down and illegal cigarettes have gone up.and ITC,we all know operates in legal cigarettes only.the reasons for the decreasing trend in legal business is attributed to heavy taxation and more pictorial depict of being carcinogen.Rise in illegal cigarettes is not only a loss to ITC but also to exchequer and the farmers growing tobacco leaves and the subsequent supply chain.

I think this will correct in future(my assumption),even if it doesnot still ITC will have the cash cow business(cigarette) because of being the leader in legal cigarettes business in INDIA.As shareholders we will get a good pie as the profits will be shared by the way of dividends(at-least 80% of the profit).

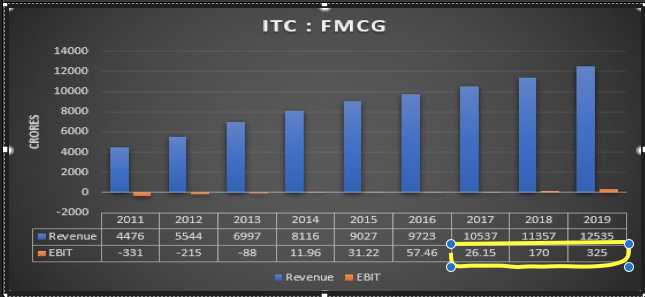

Great depiction but the investors should draw good solace from how fast the EBIT from the FMCG has been growing lately, exhibit below with numbers from 2011-19 :-

Top that up with the acquisitions Puri has been after like Sunrise who’re dominant players in their region, things augur well for the FMCG segment.

Just a general question, is anything being done to bring illegal cigarette smokers under legal radar?

As you mentioned, both the govt and ITC lose revenue due to the parallel illegal industry, it seems obvious that bringing more and more smokers under organised market makes sense.