I was discussing suzlon with one of my fathers friend and he said that in my above analysis there were few points missing which are as follows:

Additional points:

- The amt by which debt reduces, enterprise value increases by 2-3 times in next 2-3 years. Debt has been reduced by nearly 10k cr in last 3 years

- Debt conversion to equity at Rs 71/share by some lenders (even with 75% haircut, it come to nearly Rs 18/share) I NEED TO VERIFY THIS

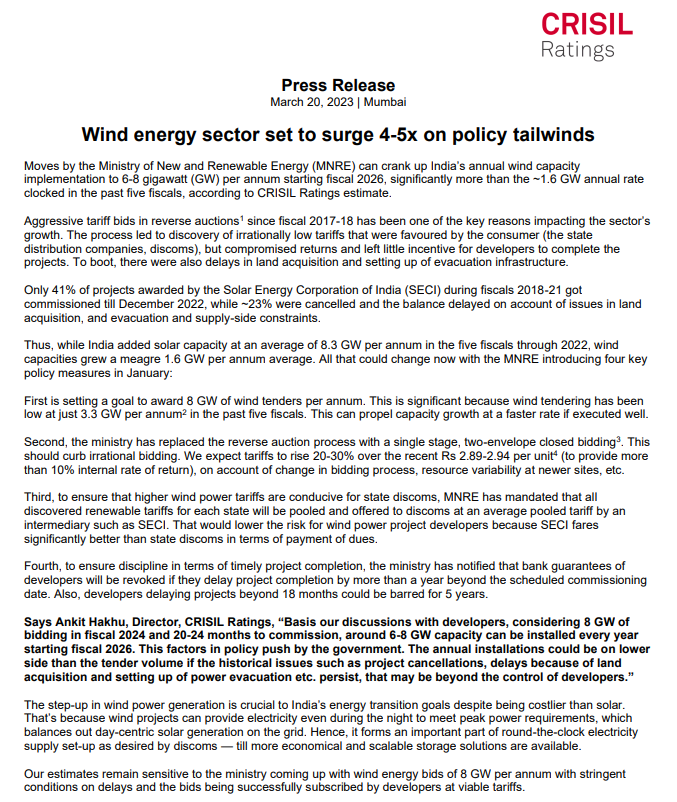

- Wind reverse auctioning scrapped as on 10 jan’23 (big plus. Back to pre 2017 days) big positive

- Govt auctioning n plg 8GW/yr over next 7-8 years.

- previous highest was 5.5 gw commissioned in fy 2016-17

- Wind repowering worth Rs 40k cr in pipeline

- Suppliers of suzlon have bought stake

- CEO ashwini kumar (harvard business school mba)has great experience in renewable

- Left over Debt refinanced by specialists REC n PFC

One last thing there is a new thread please read that it will help you understand the potential of AMC business.

Inox Green - O&M Spin off by @ganeshrpl

Hi guys

Will talk about concall, outlook and little bit of number crunching which I have tried

Concall Hilights

-

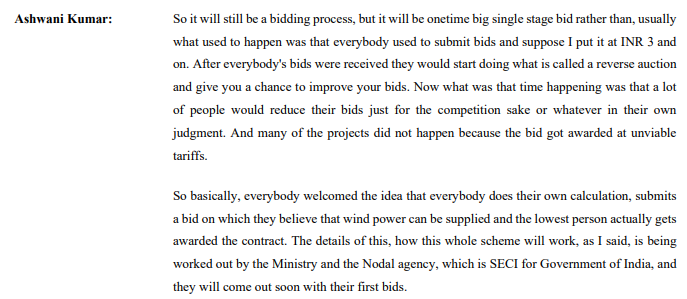

Going forward they will take order with good margins and will not want to build TOP line on the cost of bottom line. This option is available to them because of removing the Ereverse auction.

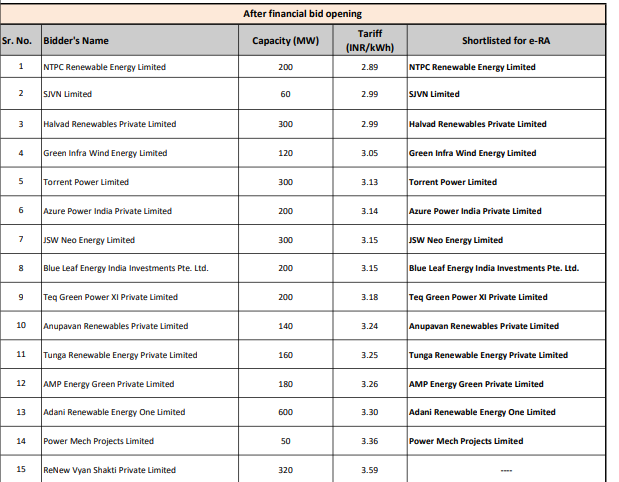

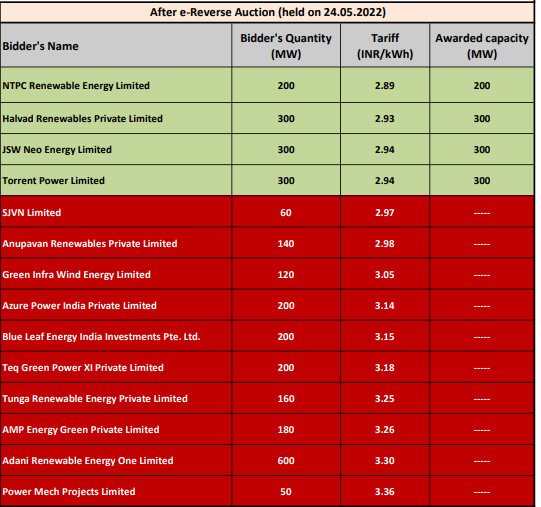

This is how bid is placed and after Ereverse it looks like this

Management Explanation

-

They have a positive book value of around 340cr this is almost of 600cr ++ jump than previous quarter (Don’t know how).

-

There is almost 3GW of back log from last year.

**WHY IS BACK LOG CREATED AND ENTIRE PROCESS

In short after signing PSA there is only 24months left to complete the project so developers don’t sign them until there is land availability or grid connection or if the price is not good.

- Last year on total installed capacity they had a market share of 42% (Big positive) current is 33%

OUTLOOK

-

8GW of order per year from central government is big positive. Management is saying that in next 3 to 6weeks there should be some update from here.

-

They have installed their first S144 this helps in reducing the LCOE

-

Their OEM business I am expecting to be flat or low single digit growth because after installation they provide 2years free warranty and only after this it comes to their OEM portfolio. Since the installation was low in FY21 I am not expecting lot of organic growth here.

-

The entire game is volumes here. If 8GW bids happen every year suzlon can get 2.5GW out of this then we have state bids and C&I also. In short demand is very strong we will have to see how much of this gets executed.

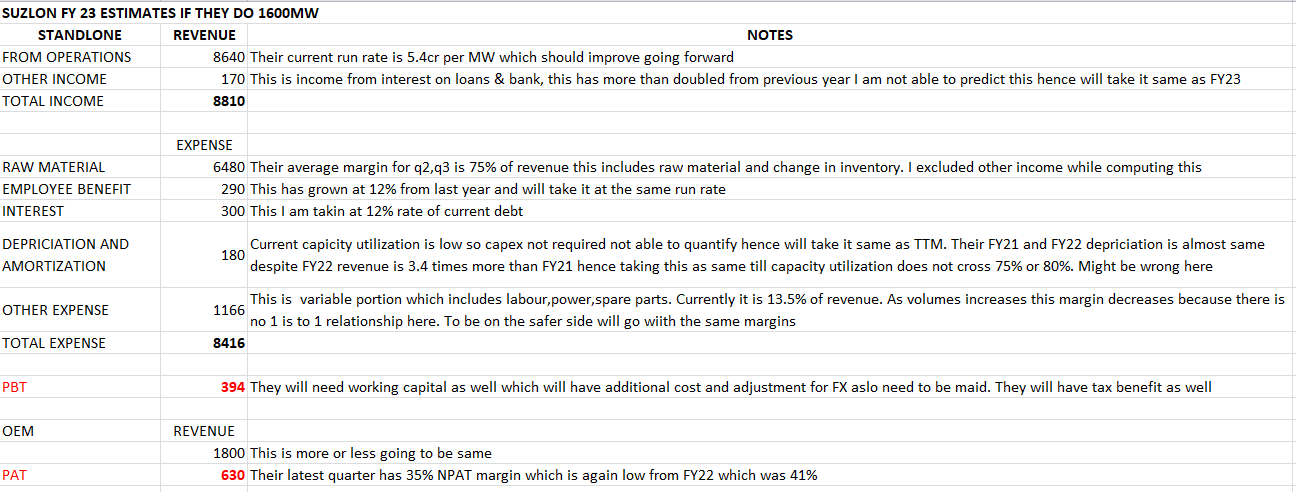

I have tried to calculate profit incase suzlon does 1.6GW next year. In my view there is a possibility of 0.80 to 1 rupee of EPS at those volumes.

Thankyou

- Almost 3GW of back log was there so out of this for 400MW we have signed PSA.

Odisha’s GRIDCO to Procure 400 MW Wind Power from SECI

MAIN POINTS

a) The wind tariff will range from ₹2.96/kWh to ₹3.01/kWh. ( Good price)

b) 390MW is of tranche XII rest is of tranche XI

c) Tranche XII winners are NTPC 200MW ,EDF 300MW , JSW 300MW, Torrent Power 300MW

So this 390MW has to be assigned to some developer in short we have 390MW with signed PSA ready to come in market.

- Tranche XIII status below

SJVN and other are yet to award those tenders to the developers

Under Tranche XIII we have close to 600MW.

- What I understand is only the Tranche XII backlog has a possibility to be executed in future rest all backlog have very low tariff( 9,10,11). So under Tranche XII we have 1.2GW of contract out of which 390MW has a signed PSA so balance 810MW still has a possibility to workout in future.

4.SECI Invites Bids for 1.2 GW of ISTS-Connected Wind Projects

MAIN POINTS

a) SECI has invited bids for 1.2GW under Tranche XIV

b) CUF should be above 22% ( very important point)

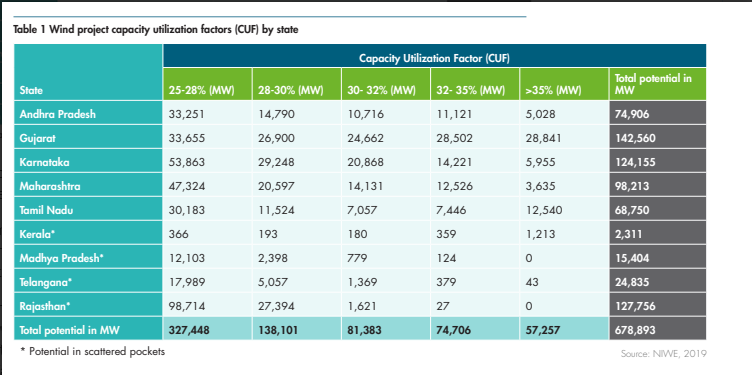

This is the land availability in india. I think as per national institute of wind energy.

MY TAKE

-

This Year First half might be a dull period for SUZLON. I expect volumes to pick up from H2 FY24 and H1FY26 being the peak.

-

Suzlon has a decent order book of 780MW ( this can last for 4 quarters)

-

We have total 3GW of orders to come in market ( Tranche XII,XIII,XIV)

-

Suzlon TTM finance cost 500cr and Suzlon expected finance cost FY24 200cr. ( clearly with same execution they save 300cr. After 2nd part of rights issue of 600cr their NET DEBT will come down to 1700cr hence 200cr interest cost )

-

Their OEM business will grow form FY24 which was flat from last 2yrs. FY24 will have low single digit growth but from FY25 we should see good growth.( will quantify later)

NOTE : Suzlon is a highly risky bet as good as calculated GAMBLING because there are too many moving parts in this kind of business. I see this as a medium term opportunity ( 2yrs to 3yrs to make 2x or 3x but highly risky. I have my own exit criteria and I would exit once I don’t see some decent progress in the industry.

GWIC has released their FY23 global wind report. I am yet to go through it which would further increase my understanding.

KEY RISK

RISK.docx (215.3 KB)

I am still understanding this industry and now I am slowly understanding that the ROOT cause of problem is not land but price. Once I develop decent understanding here I would share with you.

Disclosure - Invested

Bro, we can discuss better scripts for 2-3x in 3 years…is suzlon worth the risk because i agree with your thesis and was also bullish…but is it wise to take a bet here rather than sane return expectations company

No Sir, It is not at all wise to bet here. There are way more better companies to invest in. It is not at all worth investing in this company.

Why am I doing ?

It is all Risk/Reward. If I have an exit criteria of lets say at 50% loss but the upside is 100% than the Risk/Reward is 1:2. I am mentally prepared that how much I am ready to loose at a portfolio level.

India has big aspirations in RE and wind is going to be a big contributor and I believe that this industry is consolidating as smaller companies are not able to generate cash. Like last year SUZLON market share on the basis of installation was 42% and historically it was 33%.

As they keep reducing debt their cash flow keep increasing and the entire game is about price and volumes.

I have clearly mentioned that it is Calculated GAMBELING so I am betting on Suzlon with keeping the RISK in my mind. If wind installation increases which I am hoping then there is a possibility that I can make money.

The bottom line is this is not worth an investment and we should not be putting our money in it.

Why I keep posting here is If I am Wrong that others can learn from my mistake and if I am right then I make money ![]()

@manhar positive for Suzlon!

So After going through almost 5 to 7 industry report available in india. What I understand is Even in the best year we wont have more than 4GW or 5GW installation. The peak installation as on date looks like will happen on H2 FY25 to H1FY26 ( This is when I plan to exit if things go right).

If the Price goes to lets say a 3.5 Rs or 4 Rs per KWH I believe 50% to 70% of the problem will be solved.

But what is happening on ground level in this industry is very difficult to judge hence it is very very risky like their CEO is resigning

So god know what is happening in reality. Hence portfolio allocation is very important as it is very risky.

This new type of turbine is doing wonders for them. The current order book of suzlon is close to 750MW and since the day the CEO has resigned 5th April they have won close to 550MW of order in just 1.5 months.

The good part is most of the new orders won are from new companies. So they are getting new customers specially for S144.

Most of them are form private company so this does not include big orders from NMDC type of companies which is yet to come.

Great analysis and inputs… I had done some independent study 2 weeks back, but yours is far more comprehensive…Thanks for sharing!

Few queries:

-

From asset monetization perspective, do you have any ball park range estimate on how much the land in Pune and the 100% subsidiary company might fetch them when they decide to dispose it off? That should help further improve the debt profile and hopefully reduce the pressure of high cost of working capital loans that they will need to execute order book

-

With recent order wins in last 3 weeks, order book size has grown nicely. However, management has said that execution of order book is dictated by when customer wants the order to be delivered (presumably due to the lead time to complete lot of other activities before installation). So in this scenario FY24 revenue growth might not be great…If O&M orders kick-in, it might help improve overall revenue and little bit on the margin profile (since O&M margins are much higher)

-

International order book is low margin business for them compared to domestic one, so the international order revenue will have to be discounted accordingly

-

As per the Q4 presentation - approx half of there order book is for new turbine (S144). Do you have any inputs on how much of revenue and margin lift will this new turbine deliver over earlier models?

Thanks again for sharing your research, really helpful!

Disclaimer: Invested, currently at 1.5% of portfolio…may take it up to 5% based on execution progress

Thankyou for your kind words.

I think they mentioned the size and location of this land in previous con call. I did not do the hard work. If we can spend some time on google we can get a broad range. Like if they have 25acre we can get the per acre cost.

Management has tried their best to not disclose any details on this I am clueless.

- Plz go through recent con call very interesting. I have a lot more to share but many people don’t take interest hence i don’t share much. If you see I have been very clear that volumes will pick up in H2FY24 and peak will be H2FY25( I revise this from H1FY26).

Next year they are confident of executing 50% to 60% of order book( Close to 800MW) and also see the per windmill realization is up form 4.9cr to 5.3cr. So next year I am expecting 20% to 30% sales growth on a standalone basis. 10% to 15% on consolidated basis.

Next year OMS is going to puck up 2021 installation comes in 2024 OMS we can quantify this but I have not done yet.

- They will not take any international order. Just see the recent order they have one is majorly from retail and I have made the tender post still there are huge amount of order in market.

They won the torrent power order which has the higest price. They are getting choosey in domestic market international is out of question now.

This year bidding plan. There is huge amount of order and the ISTS waiver will end in june 2025 so all C&I, retail are in a rush to complete before june 2025 hence I say peak is H2FY25. I wont be surprised if they don’t take any more order form central auction

- They did explain this in concall I did not understand. Waiting for transcript. What I understood is the entire project cost reduces but not the per turbine cost.( margins are the same but headache reduces) So just think for setting up 300MW capacity with 2MW wind mill I need 150 of them.(more logistic, more land, more operations) but with 3MW I need only 100 wind mill.

My thesis.

They are somewhat getting the same 2016 valuation ( little bit higher) where as 2016 their debt was 11000cr and today it is 2000cr and the entire situation today is more positive than 2016. So they should be valued more.

Technically they look very strong. I am expecting 15 to 20rs by march 2024.( They just need to wind 2 to 3 more order and price will trigger)

I am expecting 300cr to 500cr PAT next year ( I think it is 160 for current year) this can go to 1000 easily if they execute 1.8GW I have done the math above so with my avg price of 8rs I am very well placed and my thesis was 100% in 1year to 1.5year which looks very possible now.

EDIT

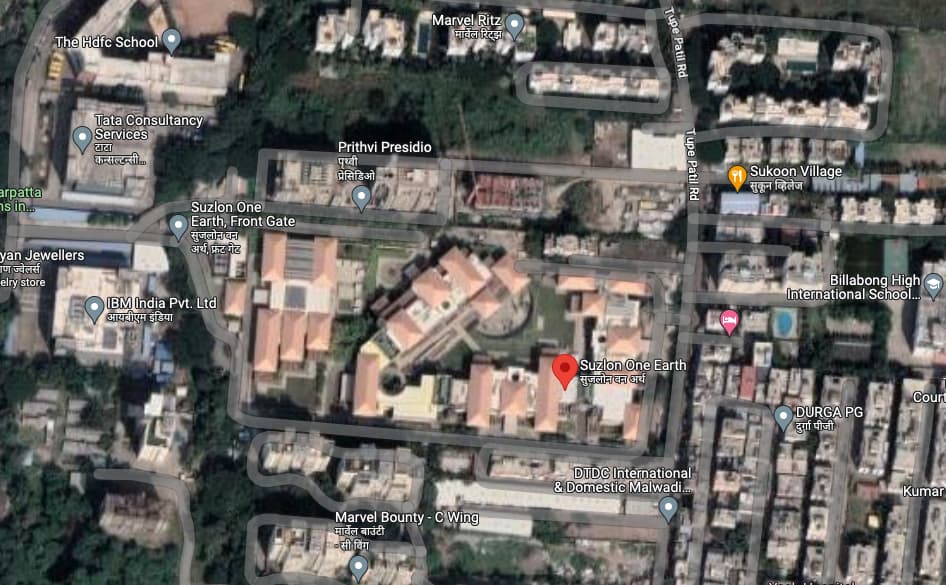

@scr thankyou for putting this up

MAGARPATTA is a gated community and this area in HADAPSAR looks to be a very expensive area. Saw few websites some are coting 40k per sq some 5k very difficult to guess if you take 10k then the entire cost of land is 500cr then they have infrastructure on it. I think @The_Seeker you can get a broad idea that it is huge.

Dic- Invested 7.5% at 8.2

I think they have mentioned 11 acre as land in Nov 22 concall.

If I am right it is in magarpatta pune. I assume that location is very decent, not sure of the going rates there. Attached google maps sceenshot.

It’s between Magarpatta and Amanora township.

The cost of land there is 15k-20k per sq feet.

Look at the Projects of Amanora Gateway tower per flat cost and size.

Power sale agreements between SECI and discoms should be a good leading indicator to track and estimate how much of wind energy potential can convert in to real orders for Suzlon and other players (with a lag of course). This particular one is even more interesting (enabled by Govt policy change) as it allows Odisha to procure wind power which will be generated in far off states like Gujarat, Maharastra, Tamilnadu etc. (only 8 states in India have potential for setting up windmills and Odisha is not one of them).

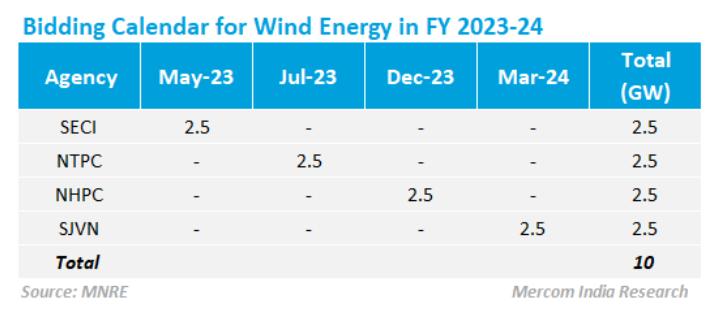

Let me give an Idea of total demand in the market (JUST FROM CENTER)

- Tranche XII I think we are done with this hence we now are left with XIII and XIV

-

This 600MW we now have a sign PSA. This is what @The_Seeker you have shared. So this is ready to come in market and suzlon will aim to get that 2.95 kwh one.

-

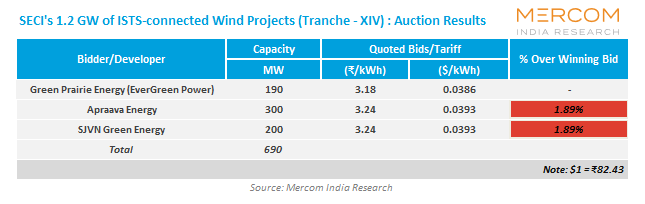

Tranche XIV this one has been an eye opener for me.

Only 690MW of bids were qualified rest were not qualified because the price was above the L1 tariff. Just see the price for XIV(almost 10% up) So I think suzlon will aim to get the 3.24Kwh one from here instead of the XIII which has a signed PSA.

4.Next month we have auction for Tranche XV 1.2GW let us assume there also only 700MW qualify.

So now in next one months we should have close to 2GW of projects which have to be allocated to the developers and this is just Center then we have state and C&I as well. After this we will have a 5 to 6 months gap.

Suzlon can wind close to 600MW from all of this 2GW.

Now Suzlon at this price does not have a good RR if anybody is taking a new entry check out for some more wind companies who are yet to deliver. I repeat that I dont like the industry but next 2 years are going to be golden years for wind. The demand is more than enough for every person to win tenders the only difference is Sulzon will be able to take the best one out of these.

For all wind related stuff use the website below they are the best

SUZLON: 18/06/2023

No of share diluted basis: 1260 cr DEBT : net debt 1200 cr

Some key takeaways from the management meet on 16/06/2023

10 gw total opportunity each year, 2.5 from SECI, NTPC,NHPC,SJVN each……plus private sector opportunity.

3 plus mw turbines which are currently 30 % sales will go to 70 percent from FY25.

Technician to turbine ratio is currently 1:4.

700 cash , gross debt 1900 cr and net debt 1200 cr.

After all ocds, cpps and all restructuring our equity will be max 1260 cr nos of shares.

Fixed cost is almost 500 cr and break even is 600 mw.

There is no problem in land availability and potential land available is for 700gw. Requirement is only 2.5 acre per installation at 3 plus mw turbine.

For Suzlon margin remains same even if we sell 3 plus mw of turbine. However for the buyer the advantage is more.

Topline is 5.5 to 7 cr per MW. 15 % is contribution margin, 10 lakhs plus o&m charge per mw, per year.

While storage of electricity can be a risk to the longevity of business but currently its 5 rs per unit in case of pumps and 7/8 rs per unit in battery.

We import 20 to 30 percent RM.

Competitors currently are

Big guys: gamesa siemens and envision ( Chinese guy ) with 2000 mw of order book each

Medium: Inox etc.

As we move towards 3.2 GW turbines capacity will automatically become 4500MW from current capacity.

Almost 60 % of order book shall be executed in fy 24 I,e 900 mw

Disclosure: Invested

What constitutes the Rs 2721 crore exceptional gain that the company recorded in FY23? That is helping the PAT figure look inflated versus FY22.

I saw the following in their Q1FY23 presentation:

Exceptional gain primarily on account of conversion of financial instruments pursuant to refinancing

I should have paid more attention in my accounting classes, but given Suzlon’s history, can someone explain what may have happened here?

Gain on de-recognition of OCDs and CCPS.

OCD and CCPS (debt) was replaced by equity