Harsh Shah — Chief Executive Officer and Whole-time Director

So I think the reason why we showcased that chart before was exactly that what can be done. However, whether the distribution is increase or not we historically taken a decision in the quarter for both we think for the [Indecipherable]. So we will be able to guide on that only in the next quarter, however. If you look at last five years track-record we have consistently done it. We applied two parameters. One parameter is that when we increase distribution, we want to increase it in a way that at least for next five-six years even if we go acquire anything distribution still remains at that level, right. And that is very important for our business model, because we may not acquire assets in some years. We may not acquire assets every quarter and our business should still provide enough headway to provide distribution visibility to investors and us the timing that when the market is right for acquisition, we acquired at the right price. So we keep that flexibility, but we compare and whenever there is an ability to increase distribution consistent and it will remain stable for next five to six years, we look-forward to increase that. That has been our strategy in that. And historically we have done it whether it gets done this quarter or not, it’s a Board decision and we’ll take it up in the next quarter.

The fall after the distribution , and presently IndiGrid at its NAV , makes me wonder if they Bit off more than they can chew… can any boarders shed more light on this

I have been mistaken about the fall , as DPU got timed with the Budget, IndiGrid still has a healthy net-debt to AUM is 58% , so they have some more space to grow.

Unfortunately in the Budget the Capital repayment portion which was tax Free upto now , will be taxed henceforth, although this is very insignificant portion ( perhaps this could be the reason for the Fall)

Are there any MF which invest exclusively in Reits/InVit ?

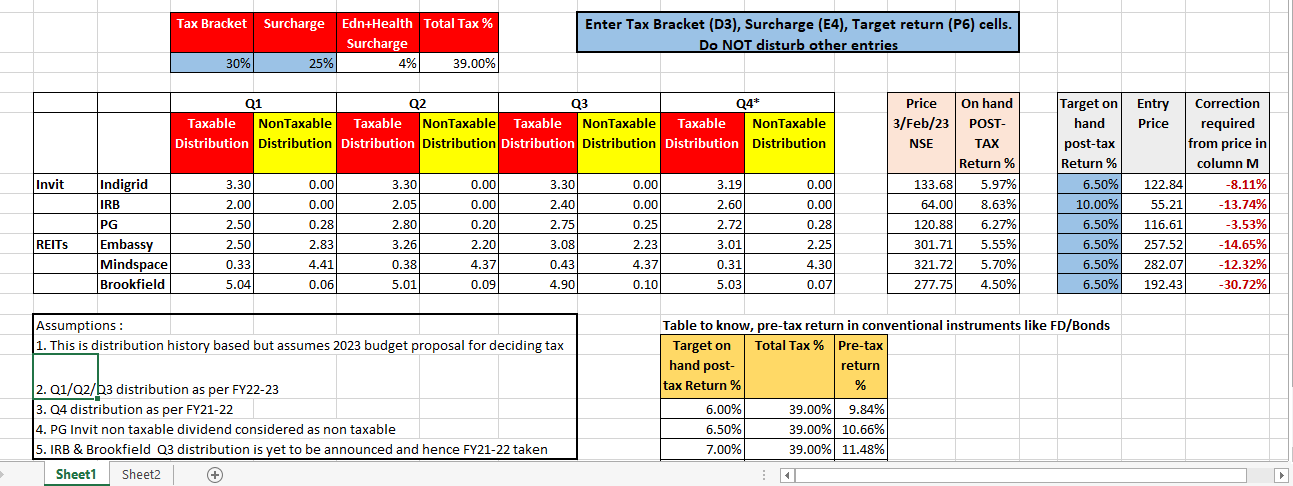

I have attempted to come out with a calculator that depicts the ravages of the 2023 budget taxationTarget entry price for a target return and current return %

All the assumptions are in the spreadsheet. A very point is that this is historical distribution based and assumes that if this distribution is continued as such, what will happen with the new budget proposal.

I have also included a table for comparison with conventional instruments like FD

The only input cells are tax bracket, surcharge and target return (all in blue accent)

Hi @KS16 thanks for sharing this. Would it not be better to have DCF analysis for invits and reits and then carry out subsequent steps in terms of taxation effects. Taking current yield does not look right way to calculate medium/long terms returns.

@rpasrija

Rahul…I have based the calculator based on the history of the distribution. Yes. The future can be different but if history has shown, the delta in distribution is marginal in the immediate quarters. If anything, the distribution has fallen in some cases and have marginally increased in some cases from immediate quarters…

The calculator is an attempt to bring in the reality to the mind of the common investor on what they are going to get, post the budget changes and one must know what is coming, especially for their instrument.

Finally, the fine print - the budget said, this is applicable from 1/4/24 but also said from AY24-25 (which is FY23-24) and hence from 1/4/23…I think, there was a typo in the 1/4/24 date and it should have been 1/4/23…considering that and the SPVs can’t be restructured quickly in a couple of months time, it is not easy to change the structure of distribution, in the immediate few quarters. And this calculator is an attempt to show , based on history, what you will get in immediate quarters…

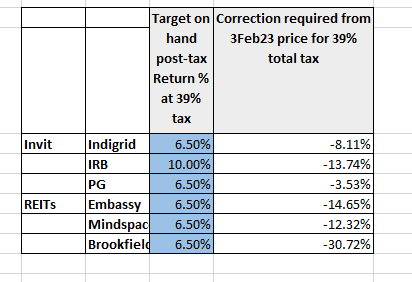

What shocked me was the amount of correction needed in Brookfield, post the budget change…how did it escape? is it held by entities who don’t have tax?

Thanks for sharing this. But, I am not able to understand rationale for 6.5% post-tax yield. At 39% tax , this turns out to be 10.65% pre-tax yield. Even in current environment , this seems to be a very high. Is there any secured investments where I can get such pre-tax return. Also, pls consider the fact that REITs are owning appreciating assets, value of which should increase over a period of time.

This is a variable. You can choose what return is target for you. That’s why it’s an excel. It’s for u to change what is required.

Personally , that’s the return I wanted. For others , they can input what’s comfortable for them.

Also, this is not a 100% debt - it’s more like a quasi debt , with a tinge of equity. Given the probability of capital loss ( however minor it is), this figure will give me comfort. Remember when the market jumps, this is not going to be a multiplying quick. I factor in that too and go with a figure that will make me feel at ease.

I will keep my comments limited to Indigrid since this is a company specific thread

While initially I was also thinking on the same lines as you, I now think it is not a very accurate way of looking at it as tax rates differ for various investors and the price would be set by the marginal investor. In this case it could be a mutual fund or retailer for whom the tax changes have no impact or is a pass through. Or even an FII with tax exemptions due to investing from GIFT city or some other low tax jurisidction.

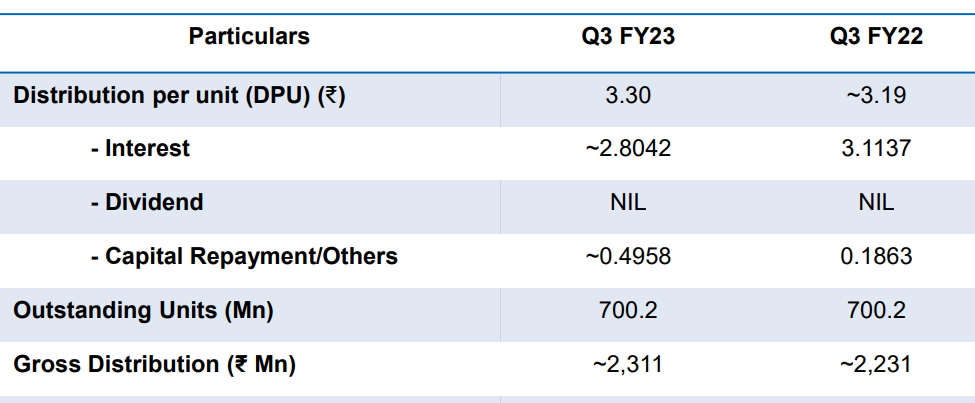

In the table above it shows that all distribution from Indigird was fully taxable even before the Budget, so I dont understand why the post tax return would be higher after the Budget than before the Budget. In reality there is a 10% capital repayment in the overall distribution of IndiGrid so this could be reflecting that.

Tax rates differ and that is the whole purpose of the Parameterization of Tax rates in the Excel. People can put what is applicable or what they are comfortable with. Price is rarely set by marginal investor. It is the biggies like FIIs that decide the price and that is the reason, the correction is not as much as the one in the table that I had given. But looking at the rates, if the regular investor buys, without knowing where the tax impact is, he will be in trouble and the Excel is supposed to create the awareness.

The table is a replica of what was in the past but post tax, what will happen, if they stick to the same method of distribution. History if anything has revealed that there is not much change in the distribution. This view is needed since SPVs will take time to restructure, and whereas I expect the tax to be immediately implantable from coming FY. My assumptions state these clearly

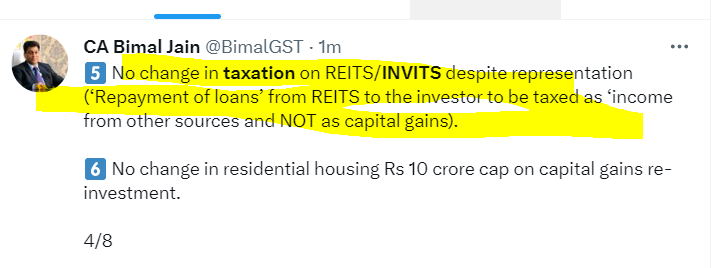

If this is true ( I mean the Dividend will also be subjected to dividend distribution tax too), my calculator above will need some tweaking. And the returns will fall further and correction needed for target returns will become steeper. Let me read through this

I think its for debt repayment and not dividend distribution. Dividend distribution seems not clear untill now requested author to correct. Till then, better wait for disclosure or clarity from REITs.

DDT is not applicable if the reit spv claims tax deduction as per old income tax regime…and if I recall right these REITs (When I say, these, I mean only Embassy and Mindspace),do use the old regime. let me check on Indigrid

Also, this budget is very specific about killing the loop hole of tax avoidance in both ends (as in the case of Return of capital or amoritsation)…and not about double taxation