If the above is true, the brief lived hope will be reversed by Monday !! Looks to be the exact party pooper

Thank you everyone for the amazing insights here. I still have another query here. If I have not acquired units at IPO price but have rather acquired them randomly post the IPO and let’s say that my avg buying price is ‘X’ which could be less or more than the IPO unit issue price, how then would this tax rule imply to me ? Any help would be appreciated. Thank you in advance.

1 Like

Its an important unanswered query yet by Finance ministry. I believe it will be left for company/REIT/INVIT to start deducting TDS when their cumulative ROC from inception becomes more than their initial book value. For individual investors it may not be feasible to keep track as market value is mostly more/less than IPO issue price…

This scenario is anyways many years down the line and by that time more clarity may come.

1 Like

It is sad to see the administration making convoluted rules. The rules seem to be drafted to target someone or some specific transaction, without regard to simplicity. This makes it hard for retail investors to own REITs and invits. This is definitely not “ease of doing business”.

Disclosure : invested in multiple REITs. I may exit.

This has has become so complicated now to even think logically. How does IPO price matter? Should it not be your cost of acquisition of the unit? Looks ridiculous.

Remember that the original finance bill had typos with mismatching FY and AY numbers. How can they have typos in such an important doc? After that, there was confusion on what was passed in the amended finance bill…I myself posted links of various twitter statements that said that the tax on RoC has not gone away…thank God…some sense seems to hv prevailed but the fine print is so awful that it will take a sum total of CA + lawyers + co secys to figure this out !! but for now, forget the tax on RoC and move on… we will wake up after a decade !!

2 Likes

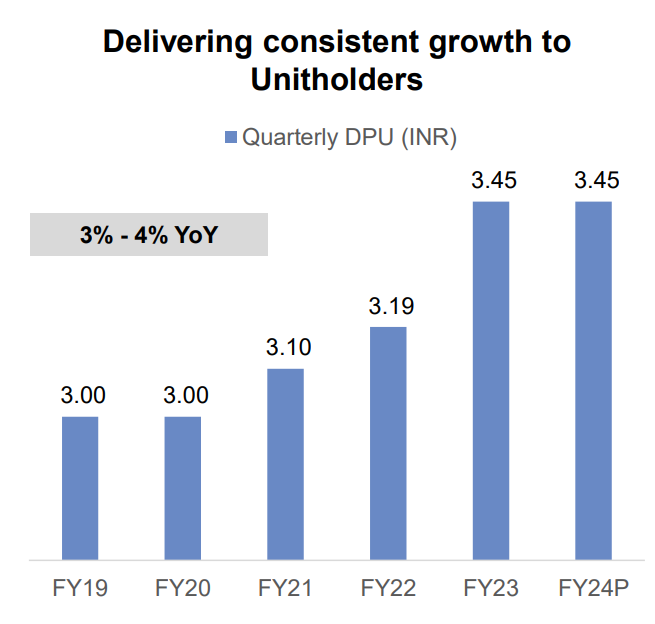

To date as per Harsh Shah statement, IndiGrid has given about 5/- rupees, as ROC.

Besides knee jerk reaction it’s good to add or hold at this juncture. Primary reason we have opted for IndiGrid is safe predictable returns.

And who know when interest cycle turns this will give appreciation too

2 Likes

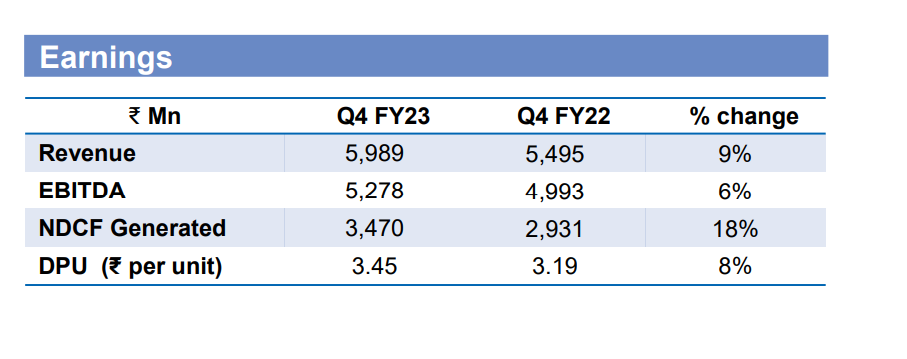

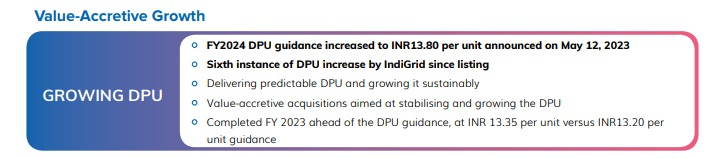

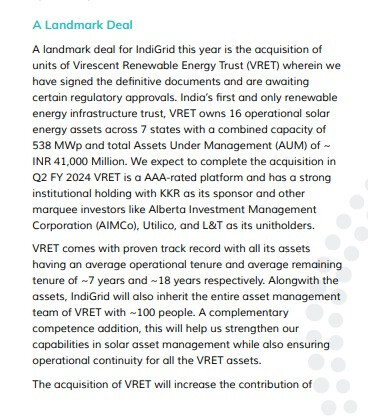

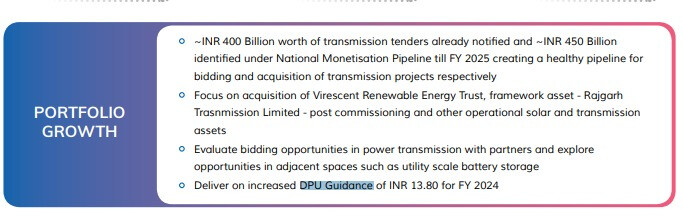

Indigrid has posted good results and increased payout to 3.45 and guided a similar amount per quarter for FY24. Lot of new developments to digest. 1. Huge 4000 cr acquisition of a renewables InvIT from KKR. This will be significant large acquisition in renewables space. Implications vis-a-vis a transmission asset need to be studied.

https://epaper.business-standard.com/bs_new/index.php?rt=main/mainpage#

2. Proposal to hike Investment Management fee. Details in presentation.

3. Money will be raised through equity or debt. In case of equity, not below 5% of prevailing price. That is what I gathered from presentation.

All the above will be taken up in EGM.

It will be interesting to attend concall on 15th.

6 Likes

non-taxable portion of the distribution, highest ever in recent qtrs…0.84 vs 0.49, 0.19, 0.24, in immediate 3 preceding qtrs

3 Likes

While you are right about the front loading of the tariffs, the maintenance cost of a transmission line is very small as compared to the capital cost → and hence the tariff quoted by the bidder. Nevertheless , the maintenance cost is potential source of cash leakage in this debt product. Indigrid assets are operational for some time now, and we should check 1. Whats is the trend in the cost operations / maintenance of each SPV. 2. The maintenance contract are given to third party contractors or the developer itslef.

Secondly , the model is very sensitive to Interest rates. Reset of Interest rate can affect the distributable cash significantly.

1 Like

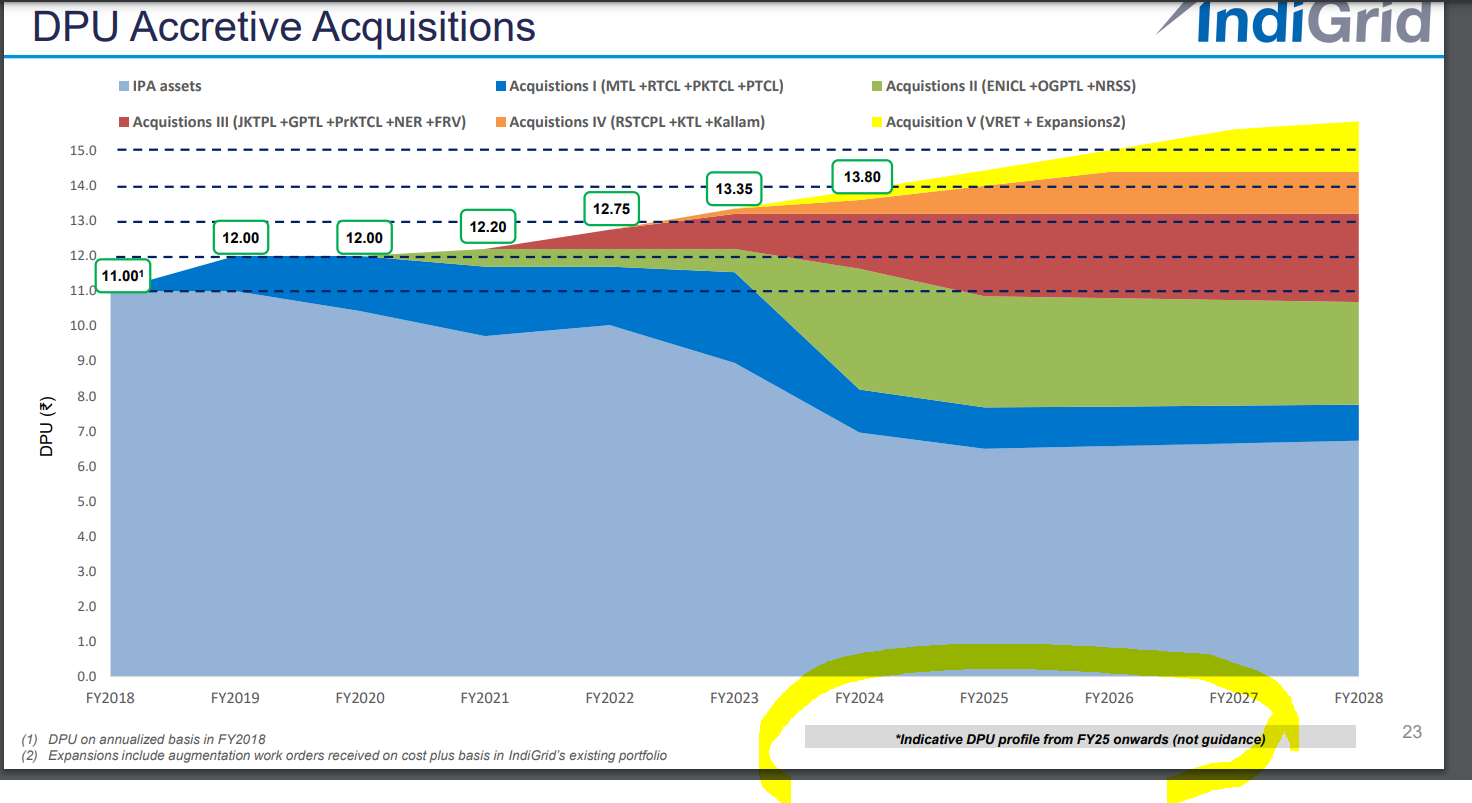

Here is the investor presentation.

Some important slides that I could relate to (in screenshots below) (3 rd screen shot below is very interesting…given the projection (not a guideline)…given their track record, and the recent acquisition news is encouraging, DPU 15 looks doable by FY26

2 Likes

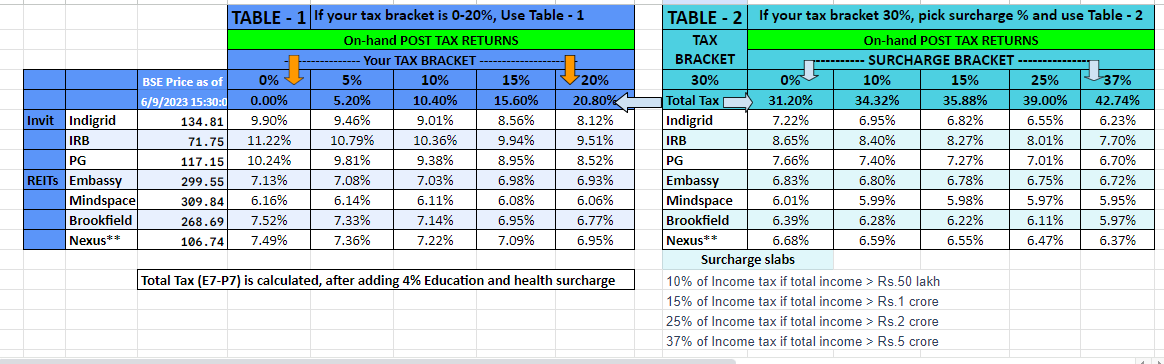

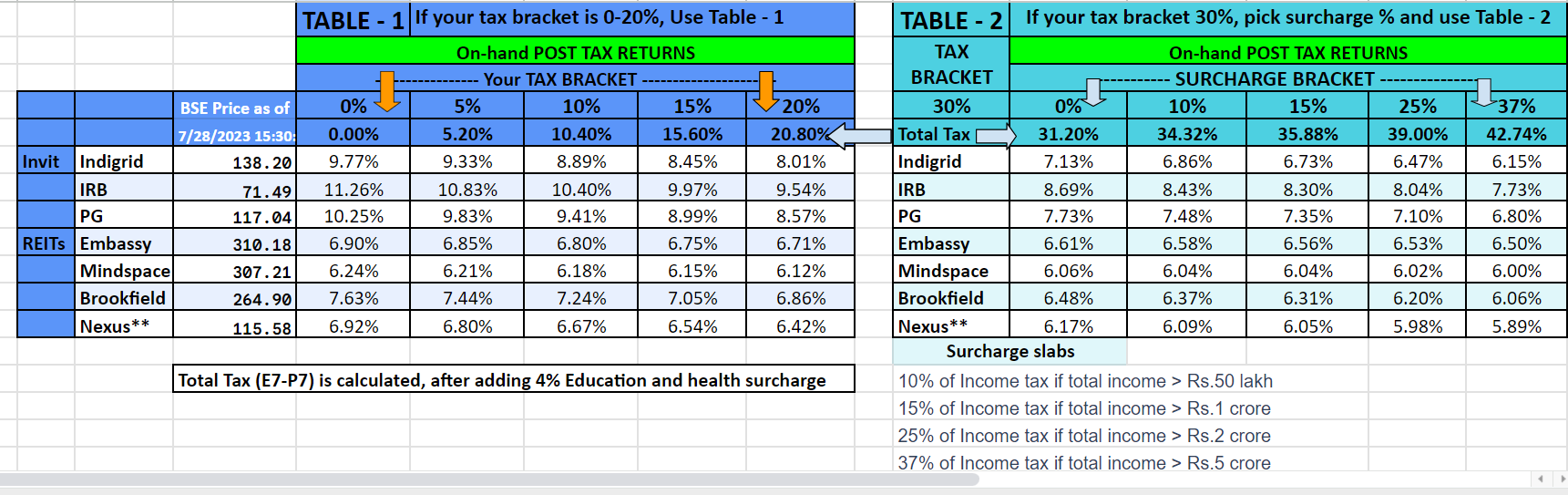

Wanted to give a comparative view of yields, on the prices as of 9th June 2023 (earlier I had shared it on 2nd June. There was a minor error in DPU of PG and I fixed it…won’t change anything drastically and it is a 2nd decimal correction)), and this is based on the rolling 4 quarters DPUs…Obviously, yield will differ for your tax bracket and hence pick the right slab below…

REMEMBER that these are POST TAX, ON HAND Yields for the Invits/Reits, for the price shown. **Nexus yield is based on projections gleaned out from various interviews, during IPO.

PS - Questions/Feedback, welcome

10 Likes

Annual report and a few (most of them are known already) highlights

https://www.bseindia.com/xml-data/corpfiling/AttachLive/78c74e2d-cb01-408f-b9dd-719b750da567.pdf

2 Likes

Any news how do they plan to raise additional Funds for this Aquisition?

Will existing Unit holders be given a chance to participate.?

Better to do it on FY24, FY25 and FY26 expected returns and show these numbers as a mean of the same - this is what is important for someone to understand the kind of yield he may be getting by investing in these. Assume similar ratio of all streams as FY23 unless any other guidance has been given specifically by the company. Also, add the long term growth guidance in DPU as a separate column.

Disclosure : This is not an investment recommendation. The author runs a PMS and may have long term investments for self and clients in the PMS.

Sarvesh…Thanks. As I said before, I go by historical DPU of the immediate 4 preceding quarters and not on future/proposed guidance of what is ahead. What is in hand is what I believe and if someone wants to take the guidance for the future, they can factor in the figures in the annual report/investor presentation.

As far as Indigrid is concerned, it will be a minor uptick and the users can use my table, as worst case, minimum yield. Also, I take the finer aspects of taxable and non-taxable portion of DPU, to arrive at the effective yield and they don’t work well on projections. Suppose, Indigrid says 5% increase in DPU, it can go to either of the 2 components above; if it is uniform increase, then it is a simple math to add that % to the yields

1 Like

In Q4 conference call, management said there will be a rights issue to bring down the leverage from 69% to 63-65%.

1 Like

Q1 results came at 19.21 hours today and here are the results…but more important, here is the DPU news

Declaration of Q1 FY 24 distribution of INR 3.45 per unit comprising INR 3.1759 per unit in the form of Interest, INR 0.0611 per unit in the form of Dividend, INR 0.2010 per unit in the form of Principal payment and INR 0.0120 in the form of Other Income.

3.45 is the same DPU as Q4 but the mix is very different, putting a lot more on the taxable form since the interest component has gone up, compared to Q4

I will update the yield table but before I do that, I have to determine, where to put this dividend (in taxable or not)…it was not there in recent prior qtrs…depends on whether the concessional regime is adopted or not…if some one knows for sure (absolutely sure), pl respond below.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/18b5527b-e9ac-4d33-96f6-13751759be6a.pdf

Results look good, at 1st glance.

Update….Q2 Presentation from 2022 says that they have NOT opted for concessional regime and hence I am taking it as Exempt dividend

Here is the Yield table after Q1 updates of Indigrid, Mindspace and Embassy. For others, the Q1 figures are from last year. Remember, I calculate this for running 4 Qtrs

3 Likes

Here is the link to investor presentation Q1 2024

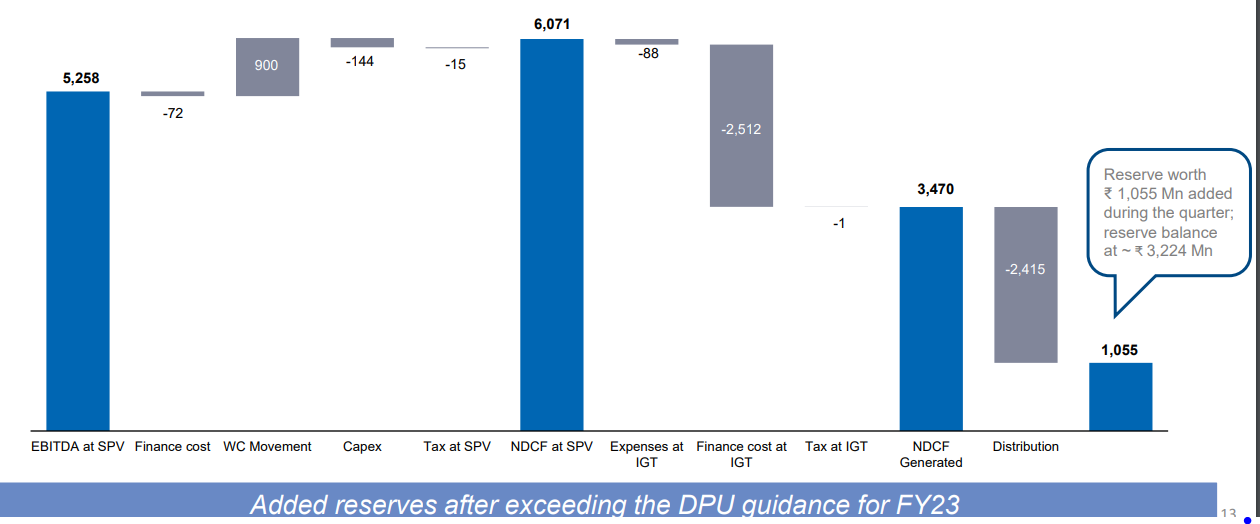

Things that need debate

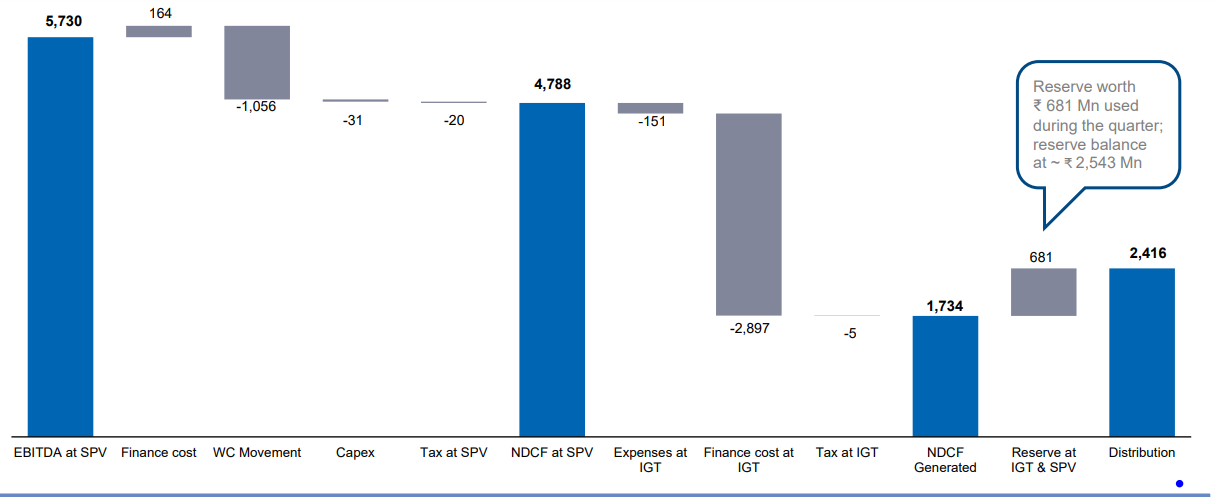

- 20% of the reserves used to shore up DPU commitment. Does not look right to me…but this is not new…had happened earlier in corresponding Q1 of last year too (at that time, it was almost 50%)

This is how it was in FY23 Q4

-

with 83% of debt locked in fixed rate, interest rate hike regime change in market, is not going to bring an immediate relief. It may take years to play out, with a lag effect…Please note that this used to be 78% before in Q4

-

Higher financing cost is take the sheen off, in general

3 Likes

131/- is the pref allotment , nothing for retail unit holders.

Shows strength of Management to issue at this high price.