Structures like INVITs, REITs are seen as yield vehicles. In times of sharply rising rates (like we are in now), these tend to underperform. The surprise rate hike from the RBI signaled that they’re ready & willing to raise rates in the near term, which is a negative for REITs and INVITs in general. I doubt this has anything to do with CEO leaving or any IndiGrid specific issue.

2 Likes

Declaration of Q4 FY 22 distribution of INR 3.1875 per unit comprising INR 2.5508 per unit in the form of Interest and INR 0.6367 per unit in the form of Principal payment.

Key Highlights

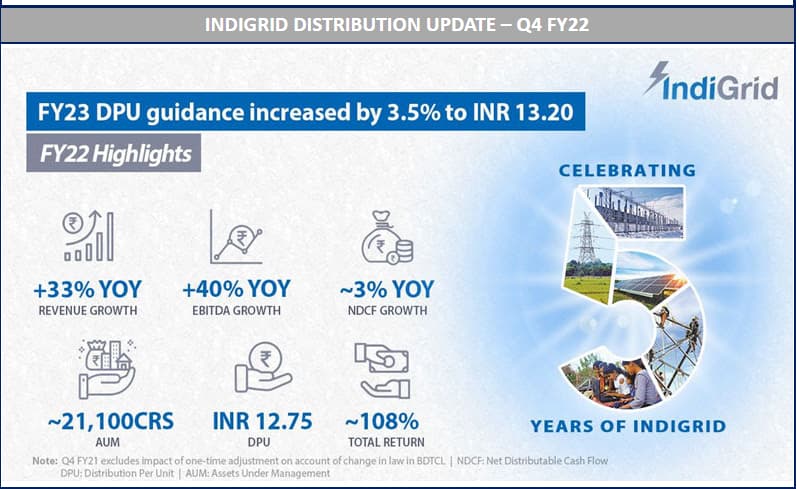

• FY22 Revenue and EBITDA up ~33% YoY and ~40% YoY respectively

• FY22 Distribution in line with guidance at INR 12.75 per unit

• Mr. Jyoti Kumar Agarwal to take over as the CEO and WTD of IndiGrid effective, July 1, 2022

1 Like

I did a quick comparison of the 2 invits IRB and INDIGRID for the pre-tax and post-tax yield calculation. Just input your average price and tax bracket (the 3 cells with yellow highlight) and you will be able to see what is the pre-tax and post-tax yields

Invit_Post Tax yield.xlsx (32.9 KB)

PS - These 2 invits are not directly comparable. Market has rewarded Indigrid and IRB invit has had a yo-yo journey in its history…but direct yield to yield comparison is given here based on FY22 distribution

3 Likes

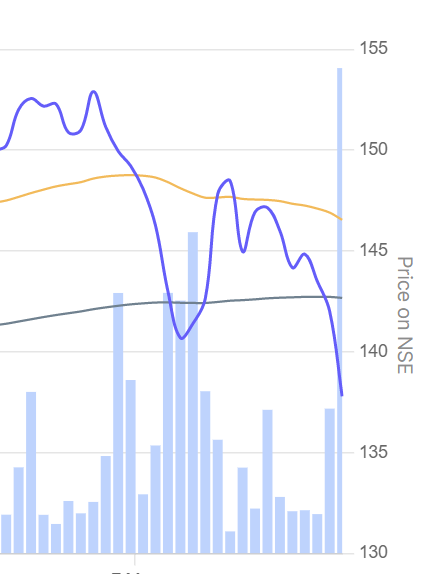

update 31-05-22 - another big wave of selling, pulling it down to 136s…even after factoring the rate hike coming (possibly) in June, this looked a big dip…since this started from 147…this did not look mere unwinding, post the Q4 distribution record date…Look at the spiking volume too (assume that it is also sell volume…highest ever volume in 6 months or so)…any insights?

Resignation of CEO is one of the trigger points - but why a drop of ~7% of an instrument yielding ~9%. Mgmt is indicating 3% increase in DPU for next 3 years so current yield is close to 10%

Disc: Substantial % of my networth is tied to this at cost of Rs86

1 Like

This was already known, and discussed in concall, and Jyoti was to take over

Seems the outgoing CEO, Harsh Shah bought ~25000 units worth Rs. 34 lac via market purchase today.

1 Like

Although Harsh Buying shows a good sign, unlike Mr Puri who sold his ESOPs , but what I dont get is how can some insider buying bring the prices down

screenshot from payout email sent by Indigrid. Guidance is Rs 13.2. Current share price is 140 or so. Do your own research on investing in this.

Have a small tracking position on this. Will probably invest more on dips

3 Likes

Q1 results are out,came out, post market today

“Declaration of Q1 FY 23 distribution of INR 3.3 per unit comprising INR 3.0556 per unit in the form of Interest and INR 0.2444 per unit in the form of Principal payment.

The record date for this distribution will be August 01, 2022, and payment will be made on or before August 10, 2022”

Here is the media release (Co sec too is leaving ! but a sub has been found)

13.2 was the guidance and 3.3 in the 1st qtr, augurs well, I guess !! but they have to maintain this run rate (unlike last year, where Q1 was higher but it tapered off but within the guidance)

What if someone buys at current price and takes in all the promised 13.2 distribution?..their pre-tax yield at CMP, will work, close to ~ 9.25%

6 Likes

CEO has resigned. Little surprising given that he took the job just two months back. Had originally joined as CFO in Sept 2020. Don’t think there’s any implications for the INVIT but something to keep an eye on maybe?

3 Likes

Harsh Shah is back as CEO after a two month stint at Azure Power ![]() !

!

7 Likes

Quarterly results came out on 10th Nov, post market (which means that market has digested the info on Friday, 11th Nov and there was no change on either direction !)

++++++++++++++++++++++++

Key Highlights

• Acquired Raichur Sholapur Transmission Limited (RSTCPL) for ~₹ 2,500 million

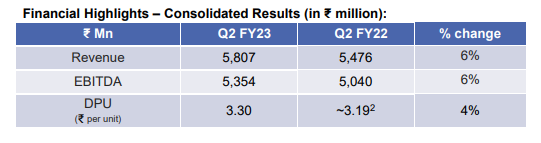

• Q2 FY23 Revenue and EBITDA up 6% YoY

• Q2 FY23 Distribution at ₹ 3.30 per unit, up 3.5% YoY

IndiGrid reports robust Q2 performance

On track to deliver FY23 DPU guidance of ₹ 13.20

https://www.bseindia.com/xml-data/corpfiling/AttachHis/538f1566-1e3e-4b7b-8d40-d273ab477394.pdf

The record date for the distribution is November 16, 2022 and shall be paid as ~₹ 3.11 per unit in the form of interest and ~₹ 0.19 per unit as capital repayment.

++++++++++++++++++++++++++++++++

Comment by me ![]()

With current price of 140, if someone has to buy it today, the 13.20 guidance will give a distribution of ‘on-hand’ pretax return of 9.45%

7 Likes

Will this be part of IndiGrid InvIT t ?

This is Sterlite Power and now that has got nothing to do Indigrid.

Disclosure - I run a SEBI registered PMS. Views are personal.

2 Likes

I would not say that…Indigrid has first right of refusal for Sterlite powers pipeline of assets (Being the original sponsor for INdigrid Invit-now the sponsor is KKR). Most assets from sterlite with 3+ years of operations gets transferred to Indigrid

Execution of binding agreement for acquisition of shares of Khargone Transmission Limited

Announcement of Quarterly results today (25th Jan)

1 Like

Q3 results

Declaration of Q3 FY 23 distribution of INR 3.30 per unit comprising INR 2.8042 per unit in the form of Interest and INR 0.4958 per unit in the form of Principal payment.

The record date for this distribution will be January 31, 2023, and payment will be made on or before February 09, 2023.

1 Like

I am not clear about the effect of principal repayment on NAV? Will NAV go down after this payment? If all the principal is repaid does the stock become delisted?