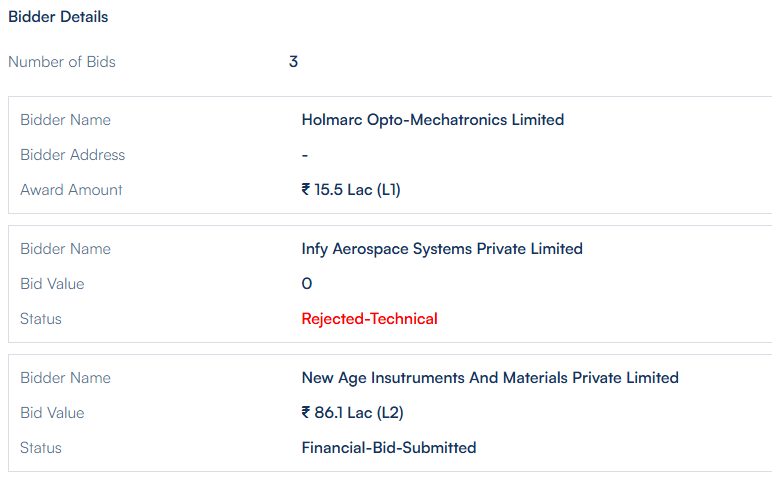

Nice discussion over last 10 odd posts that helps understand business better. Its clear that the high gross margins come from customisations. I have seen this tender after tender which they have won. All of them have lot of technical drawings attached (see the ones in my initial post as well for eg.) with clear spec and tolerances and acceptability criteria. I would hazard a guess that its not easy to do these customisations at the cost in which Holmarc operates in. At least in India it doesn’t look like there’s competition - for eg. 35-40% of the tenders they win, they are the sole bidder! This of course is because of “Make in India” and minimum 50% localisation requirement in these tenders which keeps international players out. I think that establishes the domestic moat Holmarc has.

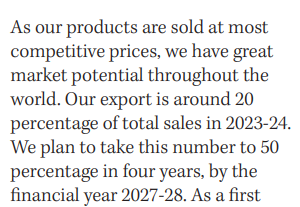

Internationally, 30% of the exports is to developed nations like US, UK, Germany, South Korea etc. Rest is to developing countries investing in research, like Indonesia, Romania, Morocco, Tunisia, Mexico etc. and easily 40% or so is fragmented over 20 other developing/poor countries. I think this is primarily still driven by cost. Exports are so strong that last two years the total was 5 Crs but this year that number is breached already.

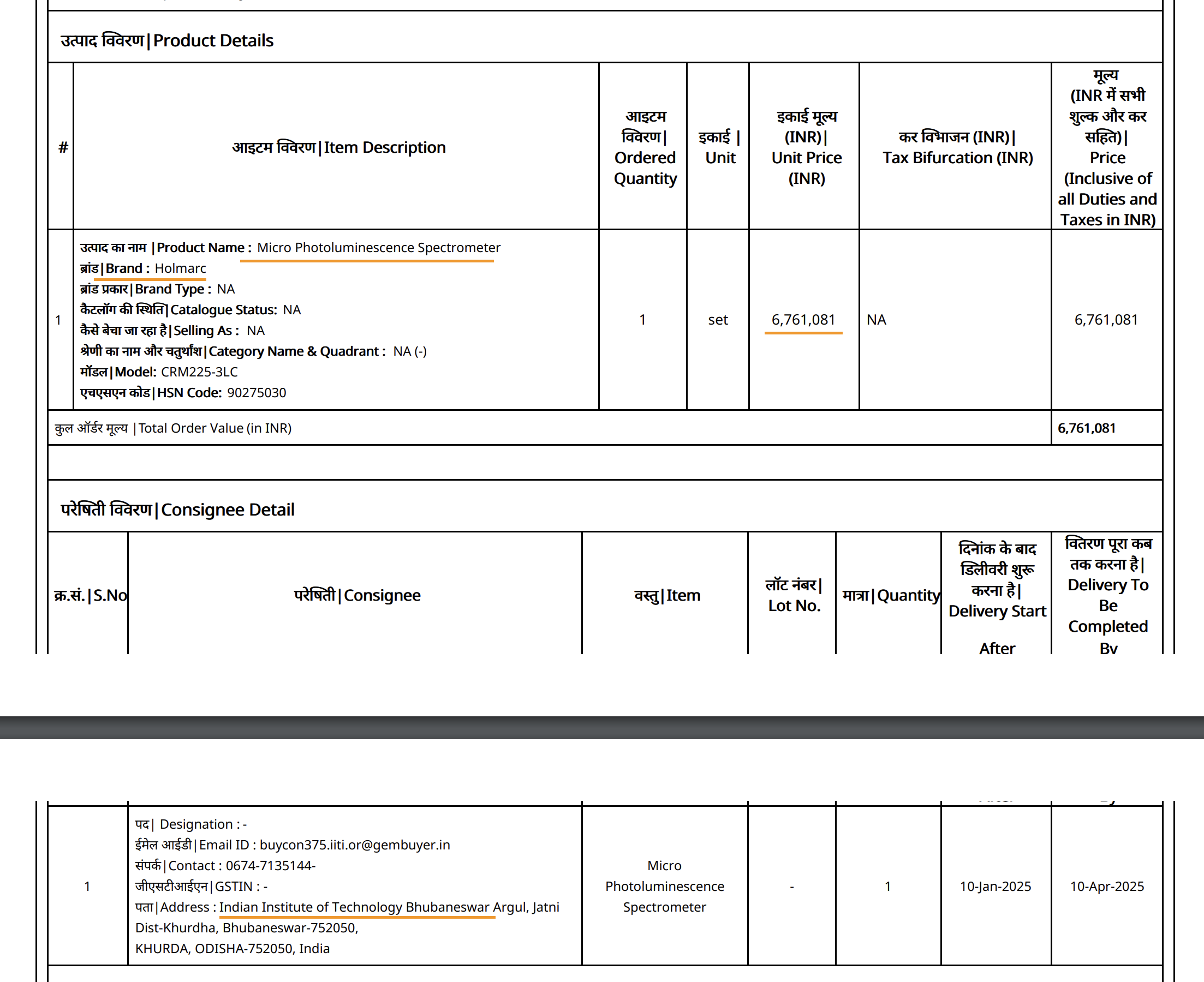

Industrial Automation bit - what they are currently doing itself is akin to industrial automation - see this tender for eg. (This is for ISRO)

This is the technical spec for this tender

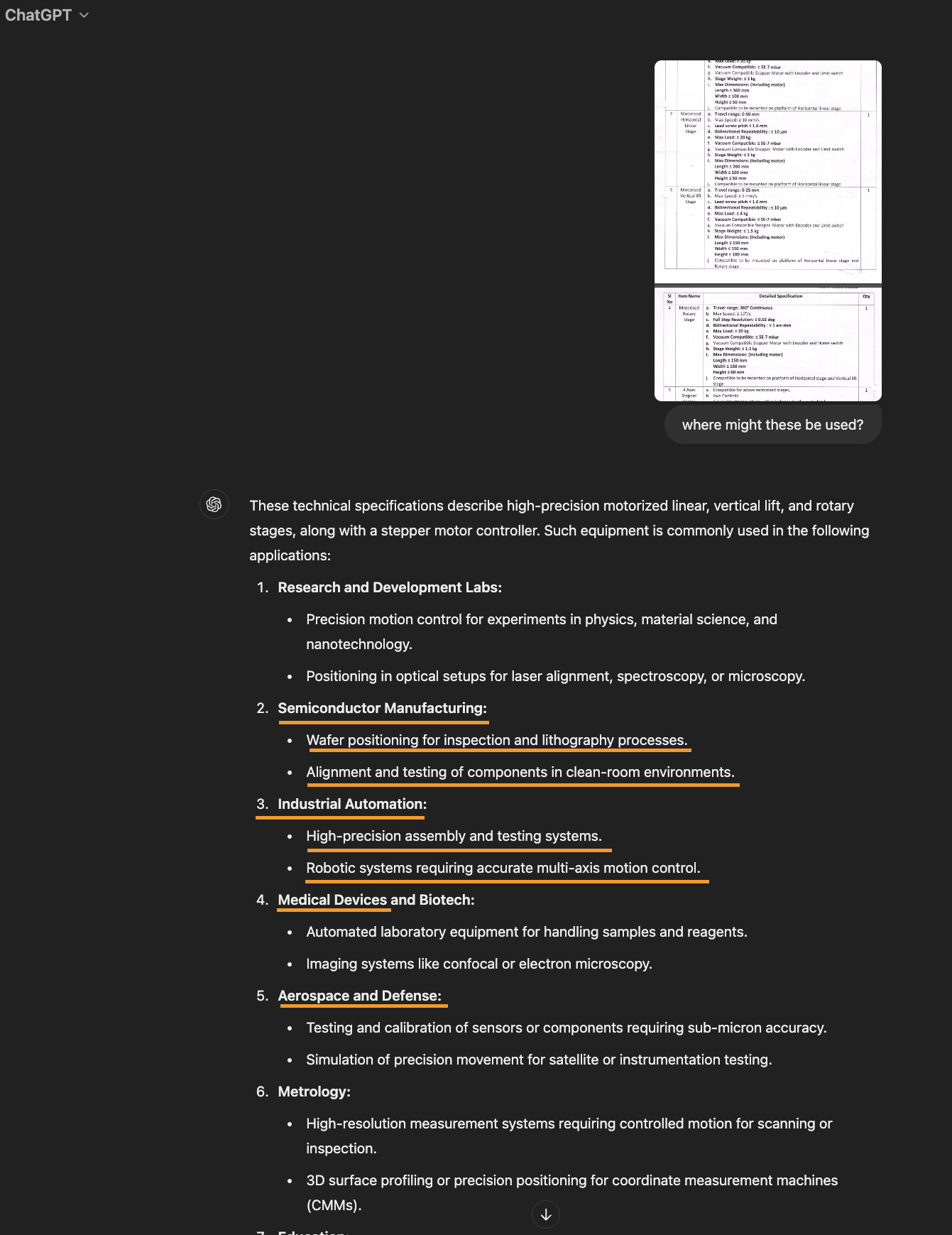

To me it looked like these aren’t very different from what might be used in industrial automation for precision manufacturing. Since I am no expert, I just asked ChatGPT where this might be used

You can see that these sort of generic components can find use across sectors including industrial automation and semi-conductor manufacturing. Of course you can argue that a simple screw will find use across sectors as well but its still a commodity - but this tender value was 29.7 lakhs, unlike a screw. I think the capability comes across more and more, the more I look. The main thing we need to see is hunger for growth.

Another thing to note is that the design and research roles make up 30% of the payroll by headcount and very likely 50% of total employee cost. This should go down over time as the company hires more workers in fabrication, finishing, assembly, lathe, milling etc. which will also help margins. I don’t believe there’s inherent operating leverage in this business considering the amount of customisations involved in higher value products, but getting to 20% EBITDA margins should be possible over next 2 yrs.

Disc: Invested