ITC:

The argument on other FMCG:

The argument is usually that ITC’s other FMCG & other businesses make no contribution to the bottom line and takes up bulk of the capital deployed by the firm. It is however contributing to the top-line as the years go by and now I believe it accounts for more than 50% of the top line.

Cigarettes do contribute more than 80% to the current earnings of the company (this should include tobacco business as well, will have to verify). That means out of some 18,000cr (check the exact numbers, all approximates from me) around 14,500cr would be from the cigarette business.

The conclusion is pretty simple, the other businesses would have to make around 10,000cr in earnings to meaningfully skew the %. Assuming the cigarette business grows its earnings slowly too.

So ITC really has to scale up its other businesses aggressively as there is no point in focusing on the bottom line at this stage. An Other FMCG business of 12k cr at industry standard margins simply will not hit the earnings profile at this juncture.

ITC’s problem is the cigarette business just makes too much money! Even if the contribution to top line decreases the margin profile of the cigarette business is much much higher.

Therefore, scaling the other FMCG business by constantly investing in growth and branding makes sense at this point, considering the objective is to decrease the cigarette business contribution.

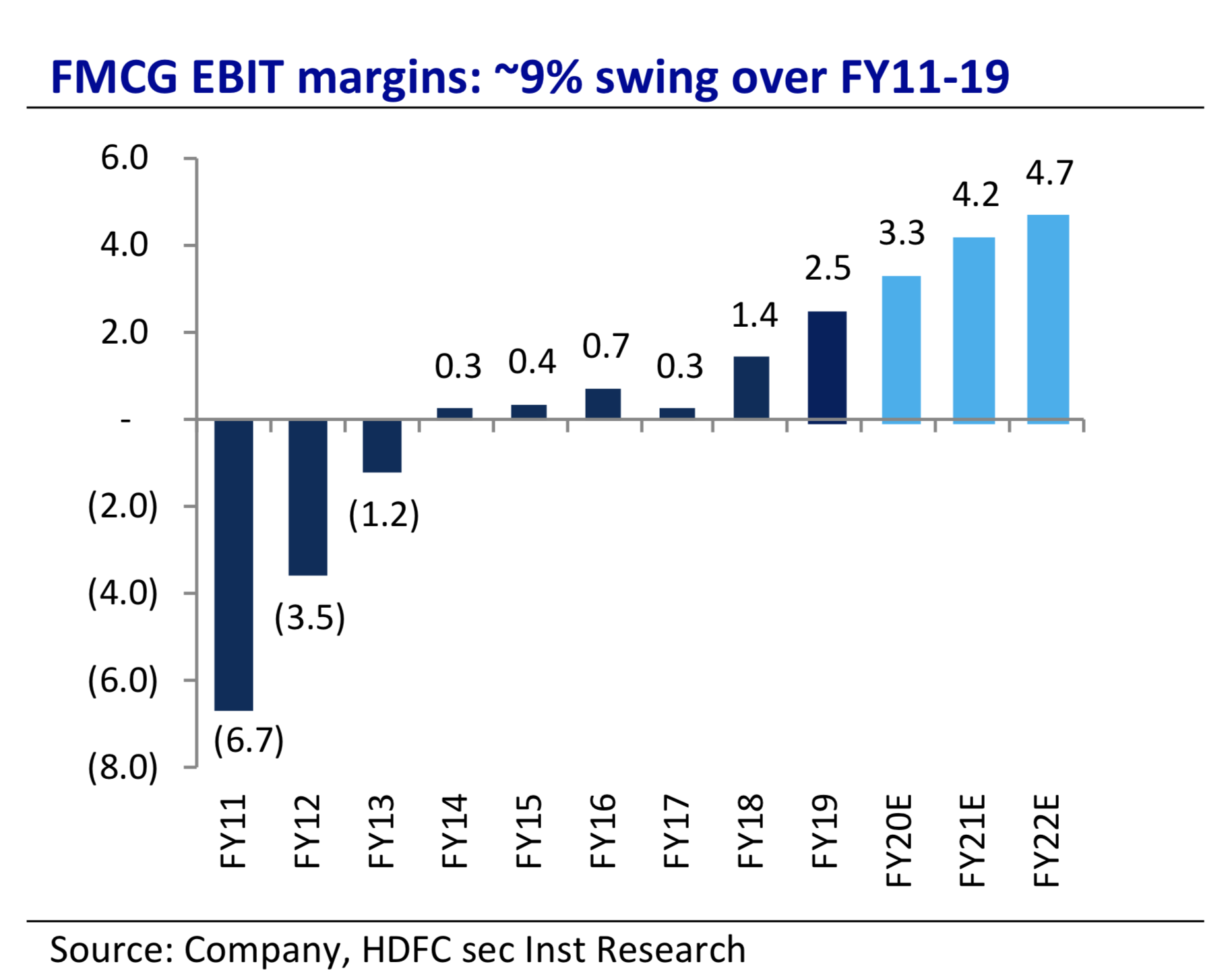

As per the HDFC Report (shared here) ITC’s gross margins of their FMCG other business is in line with industry standards at 40-45%. This shows that it is not unit level issues with the business, but investment in creating brands & new product launches. HUL also had a period like this as per the data on this thread.

This business went from some 2kcr to 12kcr in around 12 or 13 years for ITC. In the process they have built huge back-end infrastructure as well.

At 21x TTM, ITC is clearly being valued as only a cigarette business with some premium attached to it since its a nifty heavyweight, clean governance, dividend yield etc:. Globally 15-18x is what peers trade at. So basically you are buying a cigarette business which is what it is today. But you get this whole other business with very strong brands, infrastructure and supply chains for essentially nothing. All this along with a 2.5% dividend yield.

Question obviously is what about the govt. risk on the cigarette business?

-

Govt. Cannot increase taxes and destroy the industry, it is a cash cow for the govt.

-

If the govt. bans cigarettes or makes it exceedingly difficult to use them, citizens may not like this as it feels like they do not have a choice etc etc:

-

Vapourisers would be a big positive for ITC as they can brand effectively on the boxes and build an afforable indian vape. They can also innovate on the cartridges side with various indian flavours etc: ITC actually has/had its own vape called eon but they don’, it can be found on some ecommerce websites still.

-

There is a big reason Governments don’t openly allow e-cigarettes or impose bans/heavy restrictions, it is because it harms tax revenues.

-

Inspite of the heavy tax hikes over the past few years, ITC still managed to grow its earnings at a respectable pace. This shows the pricing power of the company and unfortunately the strength of the cigarette as a sin product.

-

The opportunity size of cigarettes in India can be researched online, data is readily available even on ITC’s presentations. In short, unfortunately there is head

With the above in mind does it make sense to buy ITC as a cigarette business today and treat the rest of its initiatives as optionalities? And can one hope for 8-10% earnings growth with 2.5% yield resulting in 10-12% cagr with lower risk? Can it be long term 12% compounder with growing dividends just as a cigarette business?

One would have to question their views on the long term future of the cigarette industry. Can ITC over the next decade significantly decrease cigarette dependence as a company, that is an endless debtate. It would be more productive in my view to take a call based on the cigarette business, because that is the valuation that you are getting today.