Don’t think it’s fair to compare ITC with hum/Nestle/Gillette when ITC has barely been in the fmcg market for 10-15 years while the others have been thfor more than 5-6 decades. Despite being a relatively new entrant in the market, ITC is among the top 2-3 players in numerous fmcg segments, for which some credit surely should go to their marketing.

Surely, they had been struggling on the bottom line front(possibly due to continuous new product launches and the associated additional spendings) on the fmcg side till 2 years back. But even there, the story seems to be changing in the last 4-5 quarters.

5 Likes

ITC Consistently growing its FMCG Business.

Established some brand very Strongly.

Share of FMCG in overall now gained around 27-28% of total Revenue, which may increase around 40% in 2-3 Years and may surpass Cigarette Business in terms of Revenue.

Currently Margins are the only drag in FMCG Business which may improve significantly going forward.

9 Likes

Interesting comparison b/w HUL & ITC ( FMCG Division-Non Tobacco)

Revenue growth for 16 years:

ITC ~ CAGR 34.5%

HUL~ CAGR 8%

EBITDA Margin:

ITC ~ 5.5%

HUL~ 22.9%

MCAP/EBITDA:

HUL ~ 48.7X

MCAP of ITC’s (FMCG Division-Non Tobacco) at 48.7X would be ₹ 33518

Crores.

Being Optimist on ITC, Got a Fwd from friend

3 Likes

2 Likes

I happened to hear some news on TV on 1st Jan 2020 wherein they mentioned that Sanjiv Puri, CEO of ITC tweeted something on the lines that his this year’s goal is to create value for ITC shareholders.

I am unable to find him on twitter. Has anyone read/heard about this? Any plans described along with it? Might be a very simple tweet but just curious to know if there is something more to it.

Are you referring to the last line of Resolution for 2020?

2 Likes

Guess ITC will have to languish for much more time. With expectations of tax increase on cigarettes this budget, our hope was growth in FMCG to counter that. But they have even paused new FMCG product launches. Capital allocation seems to continue to be a problem. Cigarette volume growth hasn’t received any attention since many years inspite of relatively stable tax regime. It was quite some time back that the company even did any surrogate marketing.

Snippets from article below:

Compared to last year, the growth rate is a little bit lower.

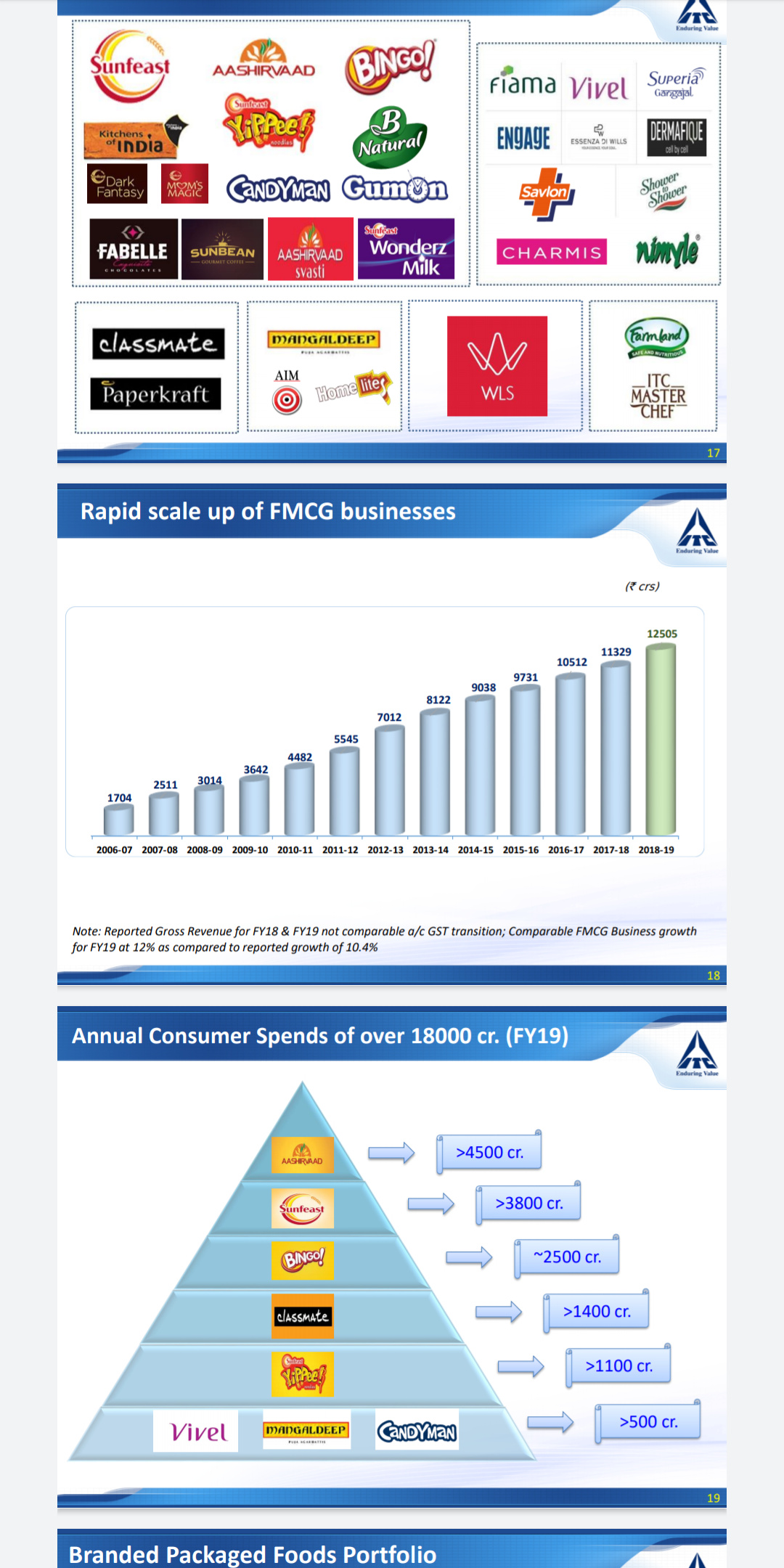

Owing to the muted offtake and slowdown, The company does not plan to make any big-bang launches in its FMCG business. Over the last couple of quarters, it has added 12 categories and 13 new brands. The focus at this point in time is to consolidate these categories and get into adjacencies within existing brands. ITC has been able to scale up existing brands like Aashirwaad to a Rs 4,500-crore brand, Sunfeast to a Rs 3,800 crore and Bingo to a Rs 2,500 crore brand.

ITC is currently investing in hospitality assets and food processing faciltities to increase its competitiveness.

We have an ongoing investment of Rs 25,000 crore entailing food processing facilities in phase one.

On cigarettes

The biggest challenge is the illegal segment which is 25 percent of the market

On its hotels business, ITC is working on an asset-light strategy. Out of the 20 hotels that ITC plans to open in the next few years, 75 percent will be through management contracts.

1 Like

I think not making new launches should be positive. They first need to consolidate and grow existing categories.

Except few top brands AATA , biscuits , fiama and noodles can’t find any products in chololate , dairy , juices , other - personal care categories in Andheri West Mumbai.

Seems there are issues related to distribution for these categories

An FMCG co derives it’s PE, not because of just the opportunity size or success of products, but also from the Free Cash Flow nature of business and assumption that either co will use FreeCash Flow to breed new lines of growth or give dividend back.

In case of ITC, the FreeCash Flow has been partially not used in best growth opportunities. The last 10 year ROE on FMCG has been less than 3%.

Similarly for Hotels

Agri and Paper do above 15% ROE

2 Likes

One positive out of the interview is that they already commissioned 9 ICML (Consumer Goods Manufacturing and Logistics facilities ) and 2 more is near completion. This initiative is supposed to bring products close to the consumer and increase the margin.

Agreed that its gonna take longer. But investing now and making it ready for next cycle of consumption boom is prudent. ITC is still growing ( revenue wise ) similar to other mainstream FMCG cos… Paper and Agri were also laggards in the past and they started yielding decent margin now…

Lets hope that FMCG also start giving similar returns in the coming years. I also think that expected hike in tax/cess is prices in already…

Discl: I hold a large chuck of ITC. my views could be biased.

1 Like

How will it help improve margin for fmcg ? Would appreciate if you can share it pls

This is the from the company…

ITC is investing in 20 state-of-the-art Integrated Consumer Goods Manufacturing and Logistics facilities (ICML) across the length and breadth of the country to enable the FMCG Businesses to rapidly scale up. These ICMLs would enable ITC to constantly craft and deliver best-in-class products, enhance cost efficiency whilst enabling greater value realisation to the farmer, help reduce India’s Agri wastage and provide ITC’s brands a competitive edge in terms of scale, freshness and close-to-market distribution.

Idea is to go close the farmers and minimise the wastage during transport and others. Also ITC is also integrating cold chain storage along with them. To store longer and minimise the wastage. Also ITC wanted to reach out the retail outlets directly…

These ICML are supposed to be located at strategic places so that it would be easy to reach the retails. Its a 4 year old article but this was idea to start building the ICMLs…

In short to bring in better efficiency, scale and calibration according to the market need.

3 Likes

25000 crore is a huge investment as per my limited knowledge for food processing and that too phase 1. Even one of largest food processing companies in india like Nestle, Britannia would nowhere be investing close to that much amount. Anyone knows what big they are planning in food processing? What exactly is this investment for? Thanks

1 Like

I remember reading that 25000 Cr across all segments and 80 % of that is on non cigarette business investment. The following video ( 2016 ) gives best inputs about the ICML facilities that they are building up… They want to cover the farm to product pipeline.

Theses ICMLs will also have cold chain storage…

4 Likes

Hello,

Can somebody with knowledge of technical analysis share what the technicals say about ITC.

Thanks

1 Like

The problem with ITC has been that despite being in FMCG segment for a decade, their products are more a push product (driven by sales commissions and advertisements) than a pull product, which can be surmised from the segmental margins across the decade which hasn’t even crossed 2-3%.

At 2% you are a trading entity at best.

The company still keeps on announcing grand plans to enter dairy one day, chocolates other day, hospitals third day.

Truth is Tobacco is the mainstay of profits.

And for all practical purposes ITC is a tobacco co

Even that would have been okay, because ITC tobacco division does almost 14000 odd crores of PAT and should be enough to justify a valuation of at least current market cap with all other businesses being free

Problem however has been the ESG Commitment of various funds.

Globally ESG Investing has gained ground, and ITC with virtually 90% of profits from Tobacco segment is a no go for these ESG Funds.

26% of Total Assets Globally are managed under ESG.

Over 2000 funds are signatories of UN based Principles of Responsible Investing, that attempts to integrate ESG investing . The funds have total AUm of close to 100 trillion dollars.

For stocks like ITC to move, Global Flows are a must and 100 trillion dollars worth of money can’t invest in ITC.

Question now is how will that change.

Would valuations get too ridiculously low for people to again take a bet.

A buy back by management could announce cheapness

A few hit products which lead to growth in FMCG segment can tilt the favour.

I’m also evaluation regularly.

Disclosure : No investment

11 Likes

To my limited understanding, one of the major reasons for lower margins of ITC in FMCG was continuously launching new products and categories. If that is right, the chairman saying they want to pause new product launches in FMCG should be music to shareholders’ ears.

Would love to understand from fellow members what are the other reasons for lower FMCG margins of ITC.

Thanks

1 Like

ITC basically have not stopped investing in creating new brands pretty much. You can draw comparisons from the early days of Relaxo or even the old theses of listed broadcasters. As long as you keep building the brand/newer brands/newer channels, bottom line stays depressed.

It is tough to imagine that ITC with all its distribution strength and backward integration will be failing at unit level numbers for their FMCG business.

This is just my bird’s eye view. One would have to dissect each brand and see if the mature brands are generating decent margins for them.

Until then, just value them as a dividend paying cigarette monopoly.

Possible outcomes being

Base case: 8-10% earnings growth plus 2.5% yield that should slowly grow. A lower risk 10-12% compounder.

Worst Case: low single digit earnings growth with a 2.5% yield and a long time correction and de-rating. Opportunity cost mostly. Dividends should cover downside somewhat in this case.

Optimistic Case: Turnaround in FMCG business. FMCG business hits at least 50,000cr (mgmt. targets 1 Lakh crore by 2030 I believe) over time and makes around 8-10kcr in Profits thereby making a reasonable contribution to bottom line.

I do not think over analysis is needed on ITC, unless of course we have the ability to dissect their Other FMCG business brand by brand. We all know their products, their capital allocation skills and cigarette businesses cash strength. The GoI will not hurt the industry heavily as it is a cash cow for them as well. Vapes will be a great thing if it happens as with ITC’s distribution, a low cost Vape with reusable catridges would be good for them, especially because it can be better branded, unlike cigarette boxes these days.

Here is a link to ITC vape brand that is basically discontinued I think due to obvious legal issues.

https://www.rstore.in/product/buy-online-compare-itc-eon-evape-rich-flavour/715155017

https://www.snapdeal.com/product/itc-eon-evape-rich-and/1039280260/reviews

3 Likes