One increase during the year of excise duty is fine, atleast that’s how govt increases revenue. But now with GST, does the council recommend and increase gst/cess many times during the year? After gst has come in from 01.07.2017, how many times the gst/cess has been increased. Does anyone has figures. If the rate is tweaked several times during a year, then it’s a concern.

Price elasticity has been seen in case of cigarettes. And there is impact on vols. So people are worried. However, sheer valuation difference make ITC a good value buy.

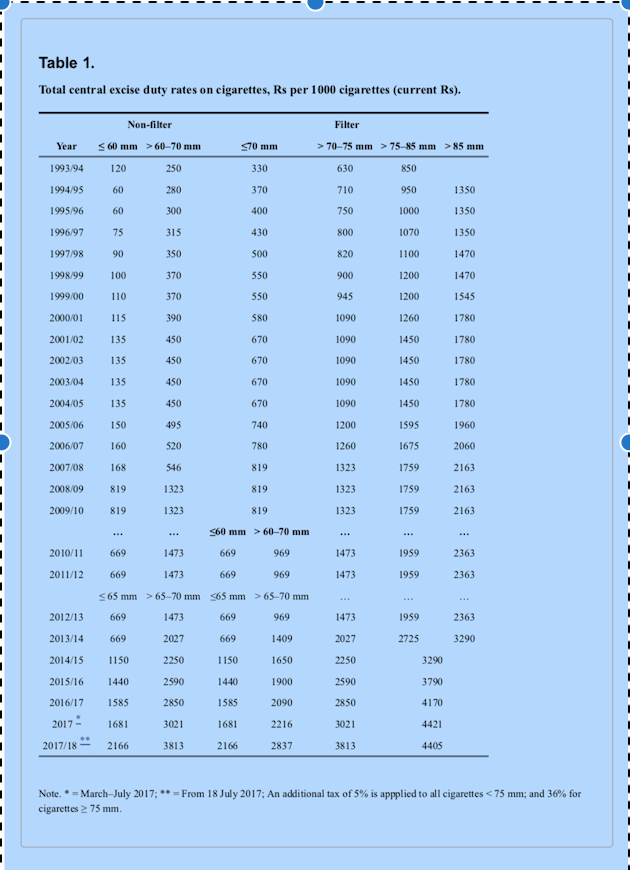

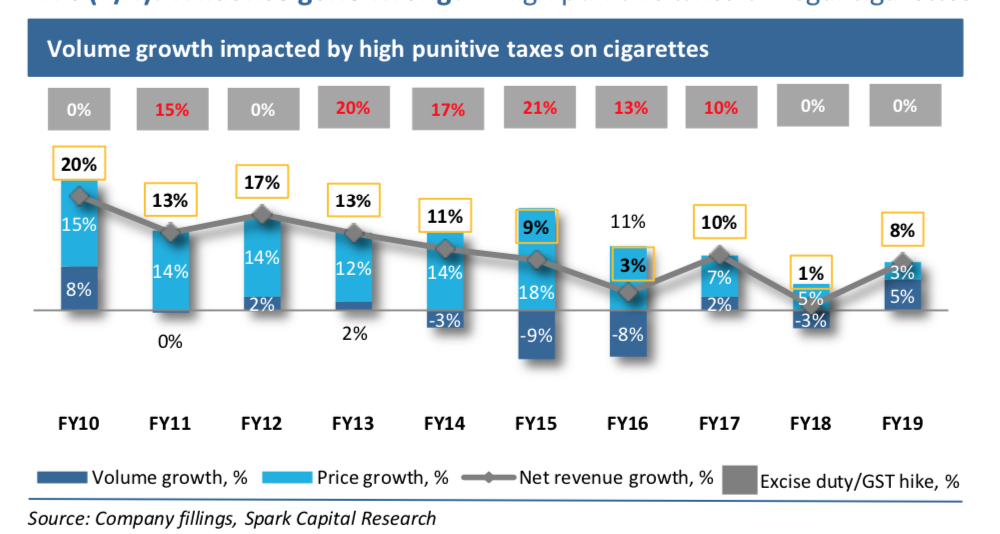

One of the interesting take he has, is related to cyclic nature of taxation on cigarettes (over 10 years). As per him, a tax increase of 6-8% can be absorbed by smokers (i.e it won’t distort price in-elasticity), but last few years has been seen more penalizing tax increase. On a overall level, smoking has not decreased over years. In-fact it has increased. Refer. It has basically shifted from legal to illegal market. As the government does not gain revenue from illegal market, rationality should prevail and the trend should reverse. But how will that happen? I don’t know. What happens if tax does not increase substantially for some years. Can legal market regain lost market share?

This study shows that even though there have been nominal price increase, but if adjusted for inflation and rising income level, Cigarettes and Bidis have become more affordable since 2000. I think this is the reason of increase in consumption of tobacco products.

Attaching the compiled central excise tax over long term.

At the same time, We can keep this in mind that volume growth stabilizes or recovers when taxation is benign.

3 Likes

Union Budget’s impact on ITC - by Nirmal Bang

Note: Ignore the price targets.

5 Likes

1 Like

ITC COO recent interview and my take on why ITC is poor man’s amazon(want to do everything) only upside down( They have premium focus in most products )

“We are the top players in all the categories that we have entered. Our ambition is to put ourselves in that position in [chocolates segment too over the next decade,”

Observation: It seems they want to play volume game once more the market as even after 2 decades they want to enter new and new categories

ITC is setting up kiosks in malls to increase the outreach of its luxury chocolate products which were only available at the company’s boutique hotels until now. It also has plans to take the kiosk model to airports as well.

So basically luxury chocolates and that too with overhead cost of setting up in malls and airports

The company is coming out with newer variants of chocolates to create a unique identity. Apart from dark, milk and white chocolate, it has brought a fourth variant of ruby chocolates which has a mild fruity taste and pink in colour. “We do not want to bring a ‘me too’ product but unique offerings,”

who want to eat pink fruity chocolate sometimes basic is better

ITC, which entered the mass premium chocolate range in October 2018 with a price point of Rs 70-200, is eyeing to widen its access through lower price points. Its luxury offerings cost anywhere between Rs 350 and Rs 15,000.

Another jargon mass premium

Cigarette business is good if they could allocate capital judiciously.As though they have pricing power there its defensive in nature.

The group capital allocation record has been very average till now went aggressively into capex heavy luxury hotel business (5star), wills lifestyle was also same kind of venture, John players another flop.

Farm land is selling premium potatoes with antioxidant etc etc,

Ready to cook ITC master chef and kitchens of india selling frozen kebabs fries etc .(As indian people get more health conscious and with ease of order with swiggy ready to cook concept market will remain small only)

Even juice and beverage market future growth expansion is not awesome first they are not market leader and second people can order fresh juice at click(Or via Alexa with voice in future) which was not an option earlier.

Though one of good thing is valuations are cheap currently.

Not invested .

5 Likes

Their distribution on all these categories you mentioned above are pathetic …I have been trying to look for ITC products at retailers but haven’t managed to find it anywhere…only set if categories that I could see are Ashirvad ,sunfeast , bingo etc.

Not others like Juice etc.

2 Likes

B2B juices are readily available in stores like “More”. They are focused on modern retail formats for premium products.

How many customer will go to such select stores to buy it …when Dabur real and Tropicana is available in neighborhood ?

At same price with better mindshare of consumers ?

Unless they make it available in Majority of retailers I don’t think In city like Mumbai people will drive down to pick up B natural so

I am sure management must be aware about it too.

I tried it couple of time by ordering it online on Amazon and loved the juices I wish to consume more but I can’t wait for 3 days for Amazon to deliver when I crave for it so

2 Likes

If you were to compare other FMCG companies (leave alone the profitability since they are very mature now, if you were to compare ITC mature cigarette business metrics with other cigarette peers, ITC is way ahead of them) such as:

Nestle: Main cash machines are baby food and maggi’s core products. Nestle did not manage to do well on Chocolates at all. Recently I see that they have begun foccussing on pushing the chocolates business. But I’m fairly certain that if one were to isolate the ROCE on their new launches, relaunches & poor categories you would have a very different ROCE.

Marico: Clearly the oils business is the main cash machine. The other brands are fairly new and they are constantly expanding. If you were to isolate them, again you would see a noteable difference.

Lever is of course the gold standard in FMCG in India in a sense, but there is a chart on this thread that tracks their expansion phase as well. And the numbers are very different than they are today.

Issue with ITC is that one isolates the other FMCG business that has been on a massive capex phase for a long time. From the infrastructure side to brand building to launching new products some that have failed and some that have become household names. If you were to isolate their winning brands you might get a solid ROCE.

If you take aashirvaad, classmate and perhaps biscuits. Cigarettes are an FMCG product as well and one should view them collectively.

If you were to isolate Nestle between MSG FMCG and Non-MSG FMCG I’m sure you would get a different metric haha!

And on swiggy and alexa, let us just understand that you get alot more food for alot less money when you buy a pack of frozen food and its easy to cook. Millennials want both, convenience and cost benefits. It is not the same as ordering from a restaurant. The same applies to juices or most other categories.

When the stock price goes down it influences the thought process of investors. If Swiggy etc is to put RTC and frozen foods out of business then in that case Nestle is in trouble as maggi will be impacted heavily. Who would want to buy things like peanut butter when you could just swiggy a peanut butter or nutella sandwich for a few hundred rupees!

However it is not like ITC have been a runaway success in the FMCG space. Majority of Indian investors started during the 2000s and by then these big FMCG companies had created household brands and garnered shelf space a long time back. We really do not have as much data on their investment phases. And this perhaps clouds one’s judgement on FMCG being an easy space. We have seen household brands die, such as uncle chips, Danone has pretty much failed in India, Bisleri had a few drinks like pina colada etc:, sunfeast pasta to a large extent, globally even companies like pepsico & coca cola have had multiple failures from vanilla coke to crystal pepsi. Patanjali came in with a big bang but slowly faded away on most of its initiatives, lever failed with ponds toothpaste, knorr noodles, ayush as a brand has not performed upto the mark

It is not at all an easy business and it is perhaps why the winners are rewarded so handsomely with such levels of free cash generation.

here is a dated article with some views

21 Likes

Very well written note. Everyone needs to remember that HUL has been in India for over 100 years now and many of their brands were created when there was little or no competition. They were the pioneers in most categories. Our grandparents, parents and we have been using those brands. Majority of people won’t even know which company makes those. However, it’s not easy to shift from something you have seen and used for ever.

Also as ITC started out as a cigarette business, company culture to deliver successful FMCG would need to be developed, it may be already there, not sure.

In any case it would be a tough and interesting journey to follow, and if they really succeed, a very rewarding one.

At last Govt/ITC started cracking down on illegal market… in one of interview CEO mentioned that his main worry is illegal market, not the competition and obviously both Govt & ITC benefits by curbing illegal market.

2 Likes

It’s a 3 lac crore market cap company. Multibagger may not be, but a compounder in the 12% CAGR range.

Unlike the FAANG and Tesla which has the globe to conquer, ITC targets the potential 400 million in India. Geographically restricted.

It all depends on the entry price and if management can turn the FMCG significantly profitable.

Cigarette is dying - health, ESG, no longer fashionable and socially acceptable.

Focus on agri, fmcg, paper.

6 Likes

Hi Friends,

I had been researching ITC and as a part of research, had conversation with an employee. Few Pointers I got.

- It is very employee friendly company and HR policies are good.

- It is having very good relations with the Distributors and many old distributors are associated with them. They are fair in dealing with distributors.

- I was surprised to know that there is rampant corruption in the company. All the forged expenses are being claimed by management for Sales Promotion and others.

- While the Sales guy to whom I talked is handling their food division, he is on the payroll of their tobacco business and all his expenses are claimed under tobacco business.

- They have practice of reimbursing distributors in the heading of tobacco even for the food business.

- Margins given to the distributors are very high compared to other FMCG companies to get the market penetration.

- There has been continuous product launches till last 4-5 months. It has slowed down since then. Some of the products have been successful and some of the products has failed spectacularly.

- There has been cost control for past few months. Earlier there used to be complete freedom.

- People are dis-aligned after new CEO taking over as many agendas are floated simultaneously and nothing gets executed properly.

7 Likes

This means the return ratios and the margins for their Non tobacco products are even lower than what they have been reporting (which by the way was not so good in the first place).

3 Likes

I doubt Auditors would let such practices run wide in an organization the size of ITC. Even BAT which is a majority stakeholder would not let this happen.

It is possible that many employees are part of multiple sales channels and hence the costs are routed to Tobacco. This cannot be termed corruption… Others may disagree.

Where is it… how sure are we that its only one distributor issue or across the board… could it be localised to one district/section alone ? Its difficult to make wider conclusion from a smaller sample size…

any inputs regarding this would be helpful. Thanks for the effort.

Got to understand from the person that these practices are prevalent in West and North Zone but we should not make any conclusion on the basis of opinion of one person. I am trying to connect with more. It would be great if some of us try reaching out to more people to be sure.

3 Likes