Astec came out with worse results than Heranba…income drop of 30% resulting in PAT loss of 97%… so it seems smaller agrochemical players are badly impacted this quarter… ![]()

3 Likes

Hi,

There has been a large spike in pyrethroid supplies from Chinese cos in past few months. At the same time, channel inventory is higher than average. As a result, realization in a number of these molecules have taken a bit hit. This has resulted in pressure on volumes and realizations.

I have been maintaining a journal of my thoughts on Heranba since they started reporting bad results in Q1FY23, you can read them below.

Thoughts on 16.08.2022

- Interaction with a few investors suggest that there will be de-growth in Chinese sales due to Chinese lockdown

- On further work, it seems Heranba’s molecules are similar to Meghmani and Bharat Rasayan. However, Heranba’s end markets are of lower quality (mostly Africa + Asia). So Meghmani and Bharat Rasayan score ahead in those terms

- Before increasing position size, it’s important to see if Q1 was just a China blip, if yes growth should come back in Q2 (albeit at lower margins as Chinese intermediate exports have low realizations)

Thoughts on 08.11.2022

- Growth looks optically higher due to lower base in Q2FY22. On 2-year basis, sales growth is 10%

- Have got 1 registration in EU, forecasting doubling of sales to US (to 30 cr. in FY23 vs 15 cr. in FY22), commercialized one new intermediate to China. So growth seems to be on track

- Sarigam facility Phase I will be commercialized in Q1FY24 and full benefit will be reflected in late FY24 and FY25.

- Although FY23 might be a bit soft (maybe 15% sales growth; 5-10% PAT growth), growth should come back strongly in FY24

- Domestic market growing very fast

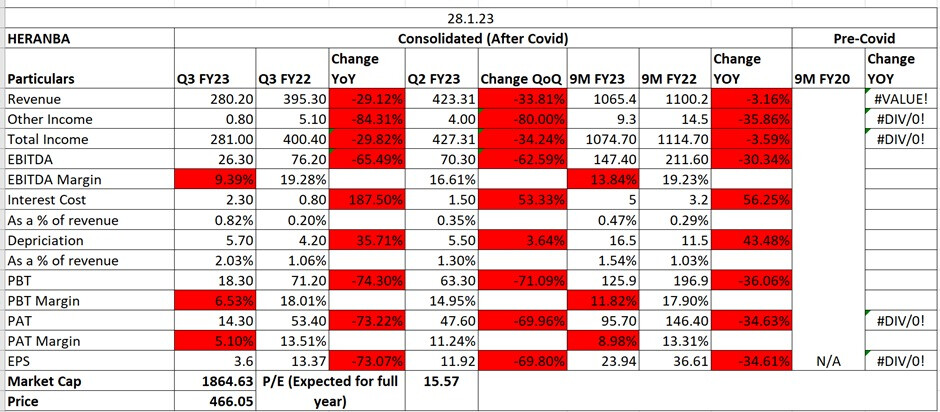

Thoughts on 29.01.2023

- Revenues have been very badly impacted due to pressure in Chinese market (technical + intermediate), it’s now clear that they were struggling with growth this year

- Management has clearly guided that FY23 will be a no growth year which suggest Q4 will also be a flat quarter. I personally think there might be 10-15% sales decline in FY23 given Q4 of a fiscal year records a jump in exports

- US/EU forey is not going to be a meaningful sales driver in FY23 or FY24. Chinese sales are 45-50% of exports and filling this gap is very hard

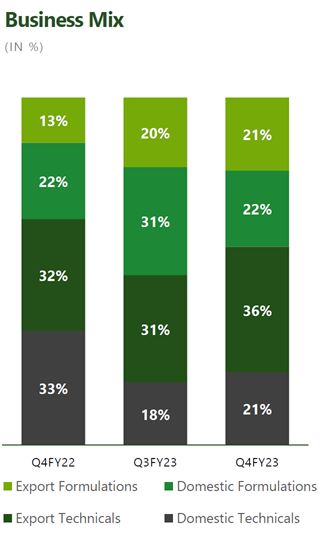

- Domestic formulation business has already done 330 cr. in 9MFY23 which is higher than FY22 (250 cr.)

- If I find a better opportunity, it might be better to sell Heranba and keep checking when sale revives and reinitiate position

- Heranba can be a very interesting opportunity when exports revive as their domestic formulation business is likely to cross 400 cr. in FY23

Hope this clarifies my thought process.

Disclosure: Invested (position size here, no transactions in last-30 days)

16 Likes

Hi Dev,

The current market cap is 1300 cr. What is the view now?

regards

Disc: Studying the company may or may not invest.

2 Likes

HI Harsh,

Astec also suffered similar fate like Heranba in Q3. Isnt is a better opportunity than Heranba given that Heranba promoters have blemished past?

regards

Disc: Studying the company. May or may not invest

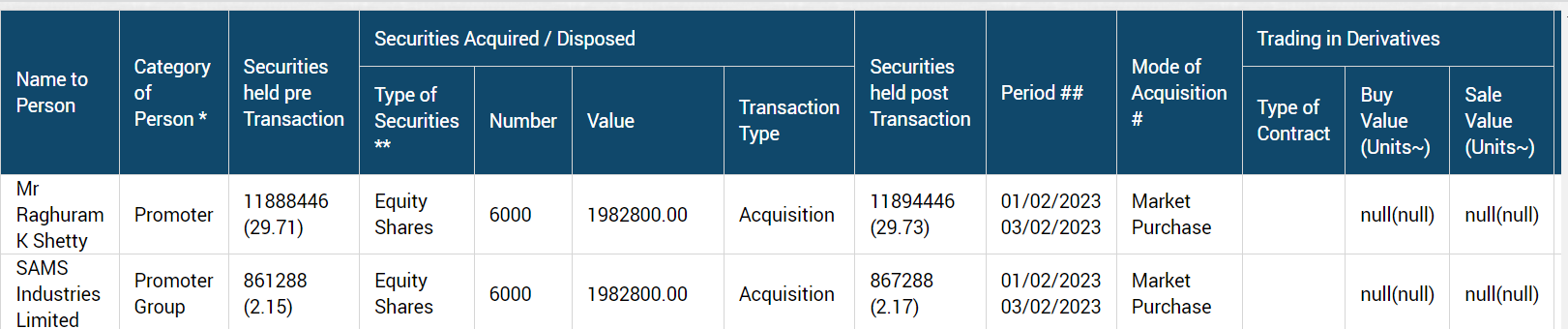

Promoters increasing their stake.

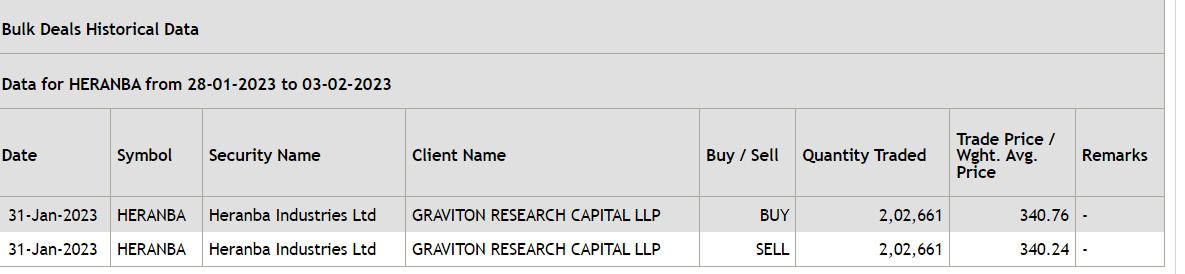

Can someone clarify as per NSE data buyer and seller is same for bulk deal happened recently.

Change in name of promoter entity

Pls refer post # 8 in this thread.

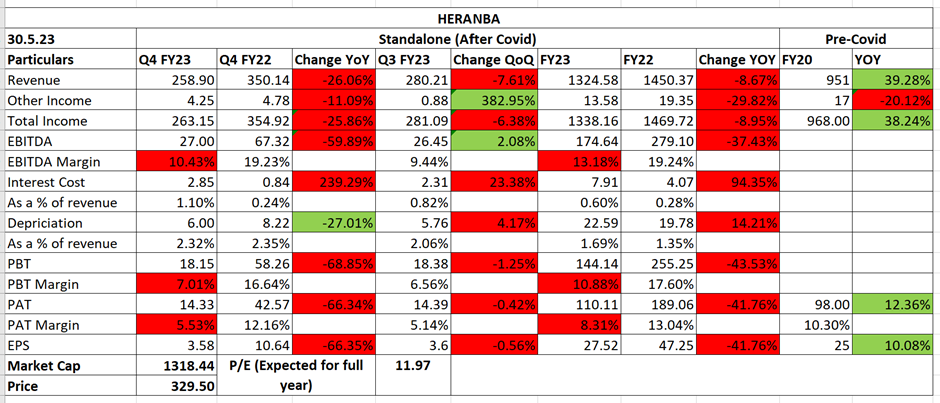

Guidance: Targeting 18-20% revenue growth in FY24 & FY25. Capacity utilization of 65% to be achieved by Sept, 2023. Want to match last year’s turnover this year of 1450 crores (can be achieved) and 1850 crores in FY24. EBITDA margin expected to be 12-14% in FY23.

HERANBA Insider Acquisition: In Feb/March 2023, total acquisition by Directors/Promoters or Promoter Group is of about 29000 shares (approx 87.59 lakhs)

Any idea why this is up so much today ?

Heranba Industries Limited receives six CIB registrations. This news might have triggered price up.

Disclosure: I am not having any exposure to this counter.

- Unfavourable global economic scenario, inventory built up in the system, sluggish demand from key export regions.

- Witnessing decent traction for our formulation products in both domestic and export markets.

- EBITDA margins and remained muted during FY23 due to lower price realization & higher power & fuel costs.

- Balance sheet continues to remain strong with Net Debt Free status along with cash of INR 118.6 crores.

- Heranba’s has aptly responded to the recent Gujarat Pollution Control Board (GPCB) closure notice for its Vapi plant. The management is confident to resume the commercial production from the Vapi unit in the coming days and the GPCB’s temporary Vapi plant’s closure notice has no impact on Heranba’s future business operations.

3 Likes

Do we know if the company has started operations for its Sarigram plant phase 1 yet?

Disclosure: Not invested

Hello,

Has anyone been tracking the company recently?

I wanted to know how the company margins are affected by freight costs.

Further, in terms of technicals, the company looks better.

3 Likes

Hello,

Has anyone attended the AGM?

Do we have an idea about the status of the ongoing capex and estimated time of completion for all the phases and units.

Hi,

This photo was taken in the month of June’24 during my outside visit to the plant. The left side building is the new wing in GIDC Sarigam, Valsad, GJ.

Dont have any update if it operational yet or not and details about the other ongoing CAPEX

Disclosure: I’ve active position in the said scrip

5 Likes

Heranba Organics Private Limited has started Commercial Production from our Sarigam Unit situated at GIDC, Sarigam,

Taluka-Umbergaon, District-Valsad, Gujarat.

1 Like

Have started learning about different companies. Picked up Heranba as suggested by one of my mentors.

Posting the researched content here just in case if it helps anyone.

Industry Overview:

- The global agrochemical market is sizable and growing. By 2025, it’s projected to generate revenues of approximately $250-260 billion, growing at a CAGR of 5.5% to 6% from 2020 to 2025.

- The global pesticide industry is segmented into herbicides, fungicides, insecticides, and other products for non-crop applications. Herbicides dominate the market, accounting for the largest share of revenue.

- Global speciality chemicals market to grow from USD 847 billion in 2020 to USD 1,090 billion by 2025, at a Compound Annual Growth Rate (CAGR) of 6.2%. The global pesticide market, a subset of the agrochemicals market, was approximately USD 69 billion in 2022 and is expected to reach USD 82 billion by 2028, growing at a CAGR of 3.5%.

- The Asia Pacific and Latin America regions are the largest consumers of pesticides, accounting for nearly 60% of global demand in 2020. The Asia Pacific region is also the largest manufacturer and supplier of pyrethroids, a type of insecticide.

- Pyrethroids are projected to experience significant growth. The global pyrethroids market was valued at USD 3.3 billion in 2020 and is expected to reach USD 4.5 billion by 2025, growing at a CAGR of 6.4%.

- the Indian pesticide market has grown significantly. From 2013-14 to 2022-23, the market grew at a CAGR of 6.6% in INR terms and 3.0% in USD terms.

- Insecticides hold the largest market share in India (around 40%), followed by fungicides (34%) and herbicides (23%).

- India, as a key player in the Asia Pacific region, holds a prominent position in the global agrochemicals market. The Indian agrochemicals market is expected to benefit from factors like:

- Increasing food consumption due to population growth.

- Government support for agriculture.

- Demand from export markets, horticulture, and floriculture.

Heranba Industries:

Company is vertically integrated in the agrochemical sector, encompassing the entire value chain from the production of intermediates to the distribution of branded formulations.

Heranba’s Business Verticals/Segments:

- Technicals (Domestic & Exports)

- Formulations (Branded & Exports

- Contract Research and Manufacturing Services (CRAMS): Entered into this with the acquisition of Daikaffil Chemicals India Limited.

Heranba’s focus on pyrethroids, a segment expected to grow significantly, is a key aspect of its business strategy. The company aims to become a leading player in this segment, particularly as pyrethroids are considered more environmentally friendly than other insecticides like organophosphorus.

In FY24, Heranba’s revenue from exports constituted 35% of its total sales, with technical exports representing 63% of total export revenue and formulation exports accounting for 37%

Government Support:

- The Indian government provides support to the agricultural sector, indirectly benefiting the pesticide industry, including Heranba.

- Government initiatives aimed at increasing food production and promoting agricultural exports create growth opportunities for pesticide companies.

- Government regulations and policies, particularly environmental regulations and the CIB&RC, influence the operations of pesticide companies in India, ensuring responsible practices and product safety.

Heranba’s plus points include:

- Vertical integration across the entire value chain of synthetic pyrethroids.

- Robust R&D capabilities focused on product development and process improvement.

- Extensive distribution network of 10000 dealers in India and a growing international presence in around 70 countries.

- Strong financial position, enabling investments in future growth and strategic acquisitions

- Actively pursuing expansion into developed markets like US and Europe.

- company aims to achieve $25 million in sales in the US within the next few years.

- company enters into CRAMS:

- Higher EBITDA Margins: The CRAMS business is known for its higher EBITDA margins compared to traditional manufacturing. Heranba’s entry into this segment can contribute to overall margin expansion.

- Operating Leverage: As Heranba scales its CRAMS operations and utilizes its capacity efficiently, it can benefit from operating leverage, leading to even higher margins

- Trends:

- Outsourcing by Innovators: Agrochemical innovators, mainly multinational companies, are increasingly outsourcing the production of intermediates and active ingredients to become asset-light. This trend benefits companies in developing countries like India, which have the manufacturing capabilities and cost advantages.

- Focus on Product Development: Innovators are increasingly focusing on product development, marketing, and distribution while relying on partners for manufacturing. This shift creates opportunities for contract research and manufacturing organizations (CRAMS). Company has newly entered into this segment.

- “China plus one” strategy by many countries

- The Indian market is driven by factors like rising food demand, government support for agriculture, and demand from export markets, horticulture, and floriculture

R&D Infrastructure:

- Heranba has 3 dedicated, state-of-the-art R&D centers. The company also recently acquired Daikaffil Chemicals India Limited, and is using this acquisition to build a world-class R&D center in Tarapur, Maharastra.

- Uses advanced equipment such as High-performance Liquid Chromatography (HPLC), Gas chromatograph (GC), UV spectro-photometer, Moisture analyzer, Particle Size analyzer, and Electron Microscopes.

- Center is also accredited and certified.

- As of fiscal year 2023, the R&D team consisted of 25 scientists, engineers, and chemists. The team grew to 37 scientists, engineers, analysts, and chemists in fiscal year 2024.

- Plans to further increase the R&D team by employing 60 additional scientists as part of the new R&D center in Tarapur, Maharastra.

- FY23

- The R&D team focused on developing 3 herbicides, 3 fungicides, and 3 insecticides.

- 3 of these compounds were developed for sales in export markets such as the USA & Brazil.

- R&D Spending was 3.9 Crores.

- FY24

- Developed 3 herbicides and launched 2 of them.

- Launched 2 fungicides.

- Developed 2 insecticides, piloted 1, and launched the same for different geographies.

- Despite the fall in PAT from 110 crores to 66 crores, Increased R&D spending to ₹4.25 crore.

Tarapur Center:

- Heranba Industries acquired Daikaffil Chemicals India Limited in FY24 to gain access to land and infrastructure in Tarapur, Maharashtra, for a world-class R&D center.

- Two-phase development plan:

- Phase 1 (Planned for FY26):

- Budget: ₹50 crore

- Purpose: Revamp existing capabilities and develop the R&D center

- Establishment of specialized divisions:

- Synthetic Chemistry

- Custom and Specialty Chemical Division

- Performance Chemical Division

- Pilot plant facility with 15 reactors: To enable small-scale batch manufacturing and process validation

- Phase 2:

- Budget: Not specified.

- Purpose: Further expansion of capabilities

- Exploration of GLP Facility Setup:

- Establishment of specialized divisions:

- Fermentation Technology and Bio-catalysis Platform

- Phase 1 (Planned for FY26):

- CRAMS Business Segment’s High EBITDA Margins: Heranba expects the CRAMS business to generate high EBITDA margins.

- Expected Increase in Revenue: The company anticipates the labs to operate at full capacity, leading to increased revenue.

- Ambitious Plans: Heranba has set aside a significant budget for this project, highlighting the company’s strong belief in its potential.

CAPEX Plans:

- Expansion of the Sarigam Facility

- Phase-I:

- This phase focuses on expanding Heranba’s technicals and intermediates production capacity at the Sarigam facility.

- Expected commissioning by H1FY25.

- This phase will add a capacity of 9,600 MTPA of intermediates and technical products.

- Phase-II:

- Planned for commissioning by H2FY25.

- Will add capacity of 4,500 MTPA of advanced agrochemical technicals

- Phase-I:

- New Technical Plant at Saykha

- Phase-I:

- Commissioning expected in H1FY25.

- Capacity of approximately 5,500 MTPA.

- Future Expansion:

- Heranba has acquired an additional industrial plot at the Saykha Industrial Estate for further expansion.

- Phase-I:

- New R&D Center at Tarapur

- Phase-I:

- Planned for FY26.

- Budget of ₹50 crore.

- Focuses on revamping existing R&D capabilities, establishing specialized divisions (Synthetic Chemistry, Custom and Specialty Chemical Division, Performance Chemical Division), and setting up a pilot plant facility with 15 reactors for small-scale batch manufacturing and process validation.

- Phase-II:

- No specific timeline provided.

- Includes exploring the setup of a Good Laboratory Practice (GLP) facility and further expansion of manufacturing capabilities.

- Aims to establish additional specialized divisions, including a Fermentation Technology and Bio-catalysis Platform

- Phase-I:

- Sarigam (Phase 1 & 2): 9,600 MTPA + 4,500 MTPA = 14,100 MTPA

- Saykha (Phase 1): 5,500 MTPA

- Total: 14,100 MTPA + 5,500 MTPA = 19,600 MTPA

- 12,900 MTPA (current) + 19,600 MTPA (expansion) = 32,500 MTPA

- This represents a significant increase of approximately 152% from the current capacity.

Valuations and Forecasting:

Not sure how to do this valuation and forecasting?

5 Likes