Promoter acquired 20K shares since last two days. Any major reason why this is trading at discount.

It’s one of the most backward integrated companies in the listed agrochem universe - it only Procures the basic chemicals and all else is made in-house.

Although, this is only for Pyrethroids which is a significant Part of its turnover.

Only Meghmani i can think of who is as backward integrated as Heranba in terms of making their own intermediates.

All other Indian agchem Players are still heavily dependent on China while this company exports to China. Shows the strength in Production and scale of operations.

Even in such torrid times, the company was able to maintain its gross margins showing its strength.

Tailwinds are strong for the whole sector! Can’t comment on Promoter buying as anything would be just speculative.

6 Likes

It looks company is registering few molecules in US. Is there any website in US which we can check the filings to get more details ?

Lambda Cyhalothrin is the main Product for which they have gotten the license in USA.

It’s a big volume Product and it’s manufactured by several other agchem Players like Bharat Rasayan!

8 Likes

Yes it’s manufactured by multiple players. But it’s one of the biggest generic volume product, multiple players make it and no issue in terms of a demand constraint!

3 Likes

AR22 notes:

Miscellaneous

- Aggregate capacity: 15’224 MTPA

- Sent 1st consignment to USA in October 2021

- Incorporated Mikusu India Pvt Ltd

- CSR: 3.06 cr. (no unspent)

- Median salary: 4.06 lakhs (vs 4 lakhs in FY21)

- Permanent employees: 714 (vs 601 in FY21)

- Contract employees: 805

- Share price: 551.1 (low), 866.85 (high)

- Shareholders: 93’108 (vs 111’829 in FY21)

- Auditor remuneration: 40 lakhs (vs 40.5 lakhs in FY21)

- Cumulative receivable impairment: 22.45 cr. (vs 17.11 cr. in FY21)

R&D

- R&D team of 22 members (vs 22 in FY21), have been working on a product basket of 15-20 molecules

- In FY22, worked on developing 2 fungicides, 2 herbicides and 1 insecticide. 2 of these compounds are at an advanced R&D stage, and are being developed for sales in Europe and USA

- Will commercialize 3 molecules in FY23

- Plans to launch 5 molecules in FY24 (subject to getting registrations)

- Will expand pyrethroid product basket from 5 currently to the entire range of 10-14 molecule

Capex

- Had CAPEX of 80 cr. in FY22, 1/3rd towards on the Sarigam site. Spent 25 cr. to acquire land at Saykha

- 180 cr. has been earmarked for Sarigam technical expansion. This phased expansion will increase capacity by 5,000-6,000 tonnes in phase I by the end of Q4FY23, and 10,000 tonnes by the end of FY24.

- 50 cr. has been earmarked for the Sykha site. However, it will be given further priority in the coming years, upon complete commercialization of the Sarigam site

Manufacturing units

- Unit I (GIDC Vapi): Manufactures a wide range of synthetic pyrethroids, organophosphorus insecticides, and various pesticides intermediates. It is a large scale manufacturing unit for insecticides, herbicides, fungicides & their intermediates

- Unit II (GIDC Vapi): Manufactures Cypermethric Acid Chloride (CMAC) and all other Isomers/derivatives of CMAC. Also manufactures Cypermethrin, Alpha Cypermethrin and Permethrin technicals. The Company has acquired an industrial plot measuring 2702 sq. mt. adjacent to the existing unit which has enabled them to enhance production capacities and upgrade Unit II’s environmental pollution control facilities. Common Boiler System is also being explored on this newly acquired plot to cater to steam requirements for all the Company’s running Units at Vapi

- Unit III (Sarigam GIDC): Equipped with modern formulation and packing facilities capable of handling large capacities of Liquid, Powders and Granules. The formulation division was established to exclusively focus on manufacturing branded formulations and trading activities. In addition, this unit is involved in the manufacturing and distribution of agrochemicals for plant and public health segment. Company has installed and initiated its new setup of spray drying facilities for WDG formulations for various formulations of sulphur such as WDG and specific combination formulations of sulphur such as Sulphur/Imidacloprid 70WG/ COC WG, Sulphur/ Tebuconazole, and other such spray-dried granulated products. This unit is also equipped with a rooftop solar plant that generates 185.0 KW per annum energy, utilized for captive consumption, in addition to its DGVCL power connection of 750.0 KVA. Got EC approval for technical manufacturing, production should begin by FY23 end

- Unit IV (GIDC Vapi): Large volume production facility to produce highest purity products from by-products and Intermediates, which have agrochemical applications. This facility enables the Company to become self-dependent, mainly for Bromine recovery, without relying on external job workers. Commercialized in FY22 and expect 100 cr. revenues from this site

- Sakhya: Has land parcel of 34’600 sq.m for further expansion with EC approval for annual capacity of 10’680 MTPA. Company has also acquired an industrial plot measuring 57,248.29 sq. mt. at Saykha Industrial Estate for further expansion

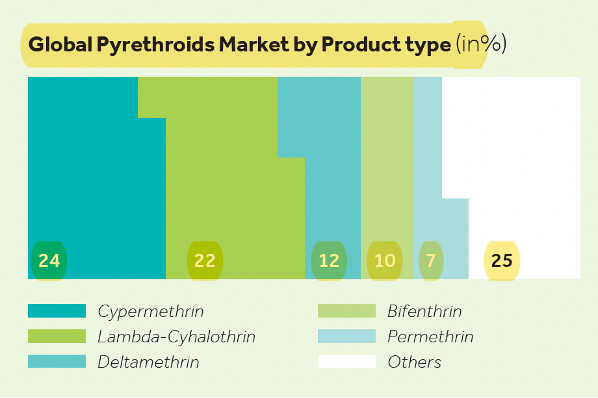

Pyrethroid molecule breakup

Disclosure: Invested (position size here, bought shares in last-30 days; still building up the full position)

15 Likes

sales to regulated markets can be game changer for this company. is there any update on that.

2 Likes

FY22 AGM notes

- Chinese business (20% of exports; 125-130 cr.) is slightly affected due to COVID lockdowns, have tried to push products to other markets

- Next generation family members are drawing very low salary (1 lakh / pm for a CA or a chemical engineer)

- Import ~ 12% of raw material

Disclosure: Invested (same as before)

12 Likes

Sep 20 quarter was the best. After that it had poor performance in most of the quarters. The sales are almost stagnant in 300 - 400 crs range. Same with profits.

TTM stock price is -27%

Also curious to know why there is very very less institutional participation.

This again got flagged in my screener run due to low PE but will not add further.

Disc: Invested.

2 Likes

I like the growth in revenues which is in line with management’s commentary.

However there are a few items in the AR which spook me.

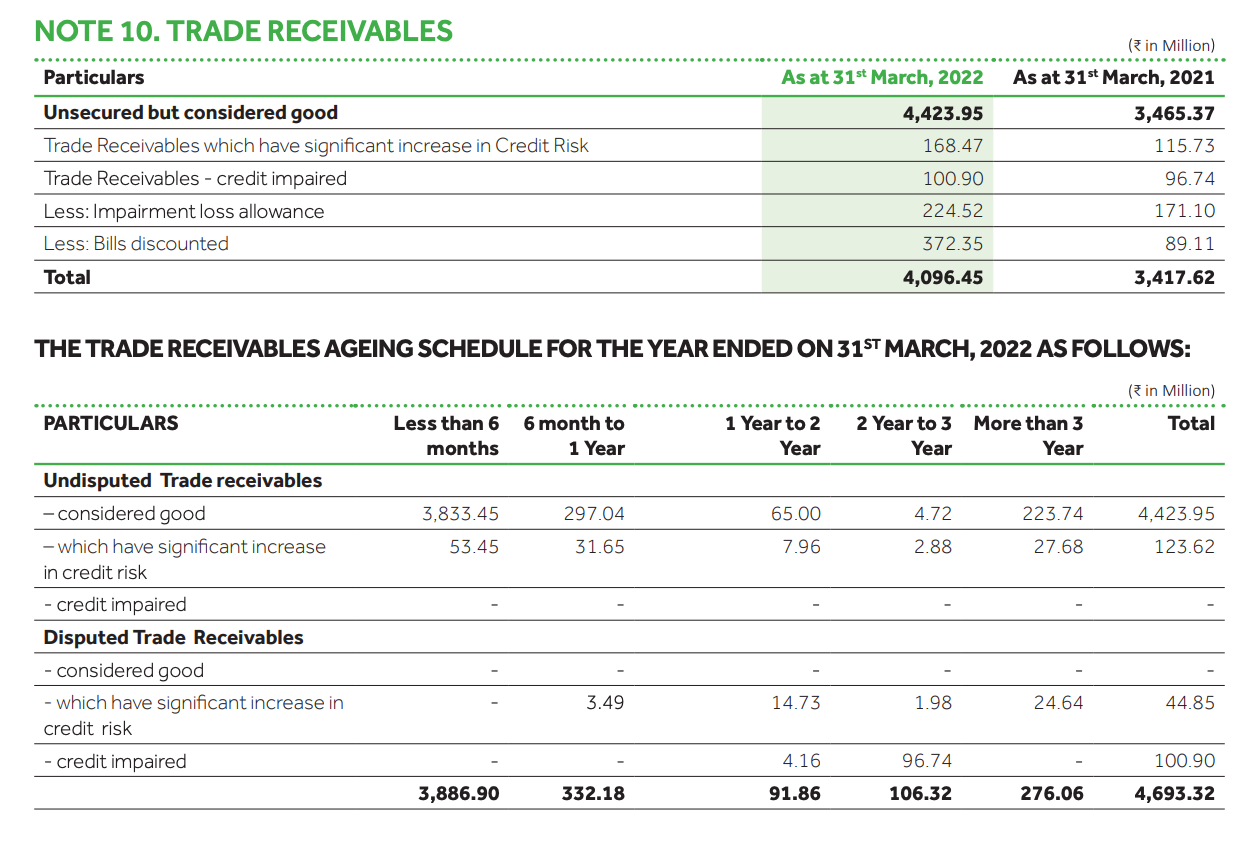

- Receivables: This is quite bad for Heranba and I read above in this VP thread that management has guided that issue will start correcting by end of FY22.

Net receivables increased from 341cr to 409cr. To put things in perspective, the PAT is 189cr.

Then there is 22cr credit impairment allowance, which is 11% of PAT.

Receivables with significant increase in credit risk + credit impaired = 27cr. This most likely will be next years credit impairment allowance.

Then there is bills discounted of 37.2cr. From what I understand the company sold receivables worth 37.2 cr to a third party/ bank. Will touch this again at the end of this post.

-

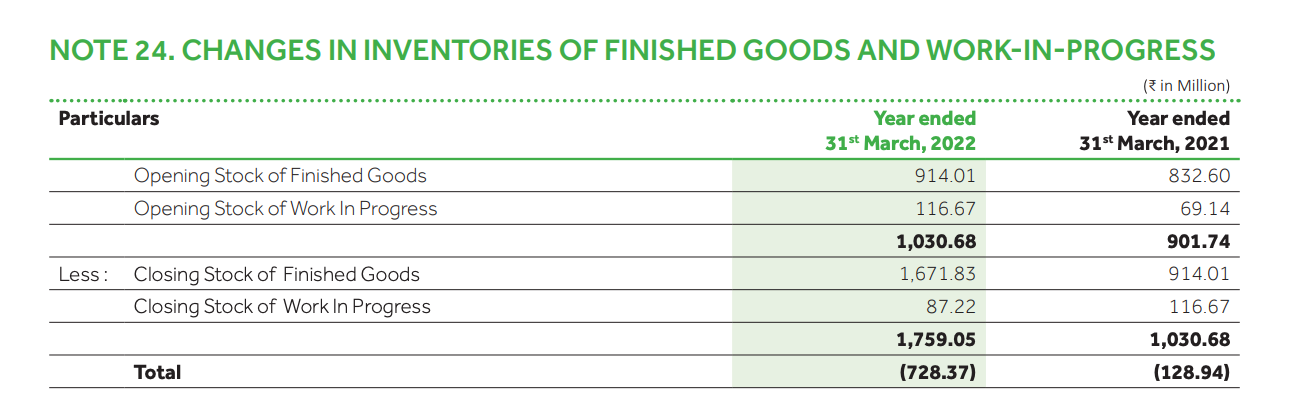

Inventory buildup of 73 cr. Is this inventory mismanagement?

-

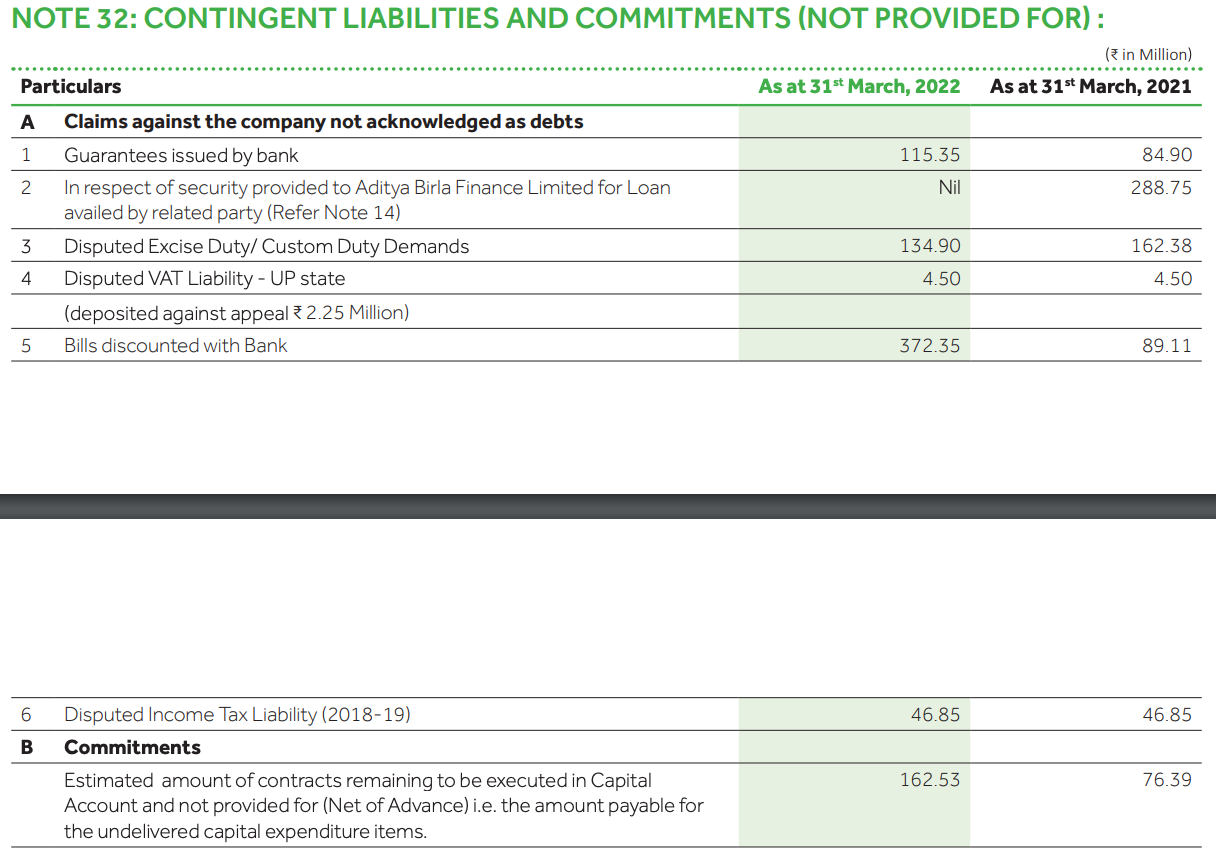

Contingent liabilities & discounted bills

#5 reads that there is a contingent liability on the Co for 37.235cr. This means that the company is still liable for recovery of this amount even though it sold the receivable to a bank.

Can anybody please educate me if this is the correct understanding?

disc: invested, not a large position

3 Likes

Hi Nimit,

I can try explaining some points raised by you.

Receivables: This should be looked as a % of sales and not as a % of profits. Broadly, receivables have stayed around 90-100 days which makes sense as they are exporting to unregulated markets. If you look at like to like peers, here are the statistics for receivables/PAT based on FY22 nos

Bharat rasayan ~ 2.64x

India Pesticides ~ 1.57x

Insecticides India ~ 3.07x

Heranba ~ 2.17x

So Heranba receivables are very much in-line with similar sized companies. Also, we should take into account quality of receivables as a majority of Heranba’s exports are into unregulated markets. If you can do a peer wise comparison, it will be very value additive.

Inventory: Again we should look at this in reference to similar sized peers. Here is the March 2022 inventory nos for Heranba’s peers, Heranba’s inventory nos are one of the lowest.

Bharat rasayan ~ 120 days

India Pesticides ~ 165 days

Insecticides India ~ 208 days

Heranba ~ 100 days

Also, building up inventory can be a business strategy. If you look at quarterly results of agchem cos, almost everyone is reporting fall in margins as cost of intermediates have shot up significantly. In this context, Heranba’s inventory positioning makes sense.

About securitization of receivables: I do not have much expertise in this, so will refrain from commenting. Maybe someone with better understanding can help.

Disclosure: Invested (position size here, no transactions in last-30 days)

10 Likes

Sales growth was subdued due to Chinese lockdown, supplies have already started reviving in July. Company faced pressure on gross margins and on power and fuel. Concall notes below.

Guidance: Lower sales growth to 15-17% (vs 18-20% earlier) with 16-18% EBITDA margins (vs 18-20% earlier). There was decline in exports to China due to lockdown, which should recover in next 2 quarters. Already have seen strong recovery in July and August

- On annualized basis, 12% of sales are from China

- Gross margins of 32% should increase going forward

- Expecting 25 cr. of revenues in FY23 from Mikusu India Private Limited and 75 cr.+ in FY24. Currently setting up dealer network

- Power & fuel costs are around 5 cr. per month

Capex:

- First block of Sarigam facility will come onstream in Q4FY23, there are 5 molecules that should be launched from this facility

- Planned capex of 130 cr. in FY23 + 120 cr. in FY24 (250 cr. in next 2-years)

- On newer capex, expect 3.5-4x fixed asset turns

Pyrethroid

- Top 3 molecules account for 30-35% of sales

- Total contribution from pyrethroids are 57-58% of sales

- Regulated markets

- Generally markets open in Q3 and Q4 of fiscal years

- Will get to know about new order to USA in Q3, have sent trial batches

- Have not been able to get business in Europe due to travel restrictions

R&D

- 2 planned launches in FY23, 1 has been launched and 1 will be launched

- 5 out of 15 products are in registration phase

Disclosure: Invested (position size here, no transactions in last-30 days)

7 Likes

index.pdf (54.6 KB)

China has issued its first national drought alert of the year - rainfall is down and the country’s fields are suffering from scorching heat.

Can be bad for all Players tending to the chinese agrochemical market. Heranba has 12.5% of it’s revenue from the chinese market.

Disc - recently sold all Positions in the company

6 Likes

Future Commentary by Management:

- Export is expected to regain strength as China sees demand pickup in Oct-Mar due to season.

- Good demand for technical/formulations is seen in the domestic markets.

- US market operations ramping up and one product registered. Stream of revenue will increase.

- 2 more products for registration in US are in the pipeline, one herbicide and one insecticide.

- Revenues will double from US in FY23 and targeting 50 crores from USA in FY24.

- Phase -1 of Sarigam Facility will commission in Q4 FY23. And Phase-2 in Q2 FY24.

- Another pesticide facility in Saykha will get commissioned in FY24/FY25.

6 Likes

Sales growth revived in Q2, company is putting up capex in Sarigam and Saykha which should start contributing from FY24. Interestingly, they are doing exceptionally well in domestic formulations business which gives a good cashflow stream to invest in technical plants. Concall notes below

FY23Q2

- Guidance: Maintain sales growth guidance of 15-17% with 16-18% EBITDA margins. Exports were impacted due to China lockdown. Currently operating at 89-90% utilization

- Witnessed 35-37% increase in fuel costs and 20% increase in labor costs

- One of promoter family member resigned from board to reduce family representation on board as advised by investors

- Chinese contribution was 18% of H1FY23 sales (vs 22% earlier). Have lots of products registered in China and have started exporting a new intermediate to China

- China exports: bromine intermediate, insecticide intermediate, and pyrethroids

- China: Sell to companies that make formulations or to traders. Don’t sell directly to distributors (so B2B and not B2C)

- Make 13-14 products, out of which 7 are pyrethroids in which they are fully backward integrated making their own intermediates

Regulated markets

- US: FY22 revenues was 15 cr., expect 30 cr. in FY23 and 50 cr. in FY24

- Received 1 registration in Europe in Q2FY23

- Hoping to receive 2 registrations in USA by Q4FY23 (1 herbicide + 1 pyrethroid)

Domestic market - 60% contribution for them comes from Kharif and 40% from Rabi

- Launched 10-12 formulations

- Will potentially reach 400 cr. in formulation sales in FY23

- Formulation business: though gross margins are lower, its a fixed cost business where EBITDA margins increase due to larger volumes

- Currently present in 21 states and sell to 8000 dealer

Capex:

- Spent 41 cr. on Sarigam in H1FY23 and will spend 100 cr. more in H2FY23 and Phase I (5000 MPTA capacity) will commercialize in Q4FY23 and give 3x asset turns by FY25. Phase 2 should commercialize in Q3FY24

- Saykha unit expansion (technical herbicides plant) will be 150 cr. and will occur in FY24 and FY25. Expect 3-3.5x fixed asset turns and commercialization in Q1FY25

Disclosure: Invested (position size here, no transactions in last-30 days)

12 Likes

One of Heranba’s group companies, Shakti Bioscience Ltd (Shakti), was declared as a wilful defaulter by Cosmos Co-op Bank Ltd (Cosmos) in FY16-17. Heranba acts as a co-borrower for a Rs35 crore term-loan issued to a group firm, Insunt Trading Pvt Ltd (Insunt). Heranba will have to bear the liability in case of default by Insunt in future. Heranba’s promoters were disqualified from acting as directors of its group entities for failing to file annual returns. Moreover, SEBI has issued some administrative orders against Heranba’s promoters in the past.

7 Likes

Very bad Q3 results. All parameters are nearly halved YoY! Stock tanked -20% today.

If anyone had attended the concall then please share in brief the feedback. Will other agro chem companies meet same fate?

https://www.heranba.co.in/wp-content/uploads/2023/01/05-Investor-Presentation_-Q3FY2023.pdf

1 Like

Disastrous results indeed ! 73% drop in PAT (YoY), Revenue declined by almost 30%. Poor operational performance overall. Management just blamed everything on geo-political concerns, macro economic conditions etc. “Revenue is impacted by challenging global macros including prolonged geopolitical concerns, rising inflation in major economies and slowdown in demand. The domestic technical business witnessed lower demand due to challenging market conditions coupled with higher inventory. The company’s export business was impacted by volatile global macroeconomics. The Ebitda margins were suppressed during the period due to higher raw material prices and an increase in power & fuel costs. The near-term outlook is challenging for the entire agrochemical industry. However, Heranba will continue to diversify its product portfolio, widen its distribution network and sharpen its R&D focus for creating sustainable growth, the management said.”

Wondering if other agro-chemical companies are also expecting similar dismal results or is it just a one off for Heranba. @Experts - please share your analysis of these results.

1 Like