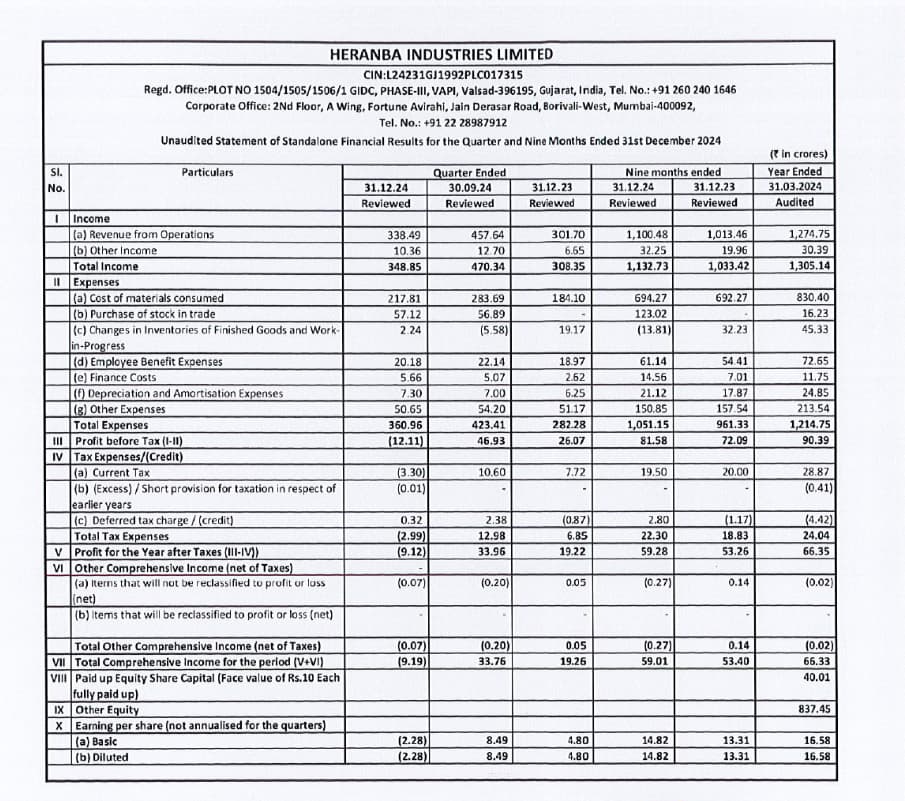

The subdued numbers is due to the challenges exports markets. Lot of business happens in Q2 (Hmm… if one goes through the previous concalls they were claiming that insecticides is something which is required through out the year and there is no much cyclicality in the business. Seeing the numbers / lower realizations it looks like the competition is catching up here. Recently Dharmaj crop care also started manufacturing pyrethroids. Also alluded that irrespective of the demand production can’t be curtailed. Everyone will try to clear the inventory by selling at lower prices.).

Meghmani Organics reported decent numbers. While 80%+ of its revenues from exports from regulated markets including US. As mentioned by @harsh.beria93 - the export markets of Heranba is more Asia specific and it doesn’t seems to command good realization compared to regulated markets

Current capacity utilization is 85% (excluding the newly commissioned plant in Sarigram-1 in Q3-FY25). Fixed costs ~15-20Cr was absorbed without much contribution to revenue.

To grow 30%+ in FY26 with revenue of 1800Cr with margins of 12-14%.

Some positives:

Sarigram-2 and Saykha facility to be commissioned in Q4FY25 (finally getting commissioned after a delay of 2 years)

Need to watch the capacity utilization levels. Management claims asset turnover 3x. I doubt as the margins are reverting to back to 10-12% range which is seen during pre-covid times.

Formulation business is growing with most of the technicals backward integrated it should help for margin improvement

With capex of 70Cr planned in FY26, no more capex planned, its only maintenance capex

Certain products prices going up slightly in Q4. Expect improvement in Q4FY25

Key things to be monitored - Capacity utilization of new plants, new registrations

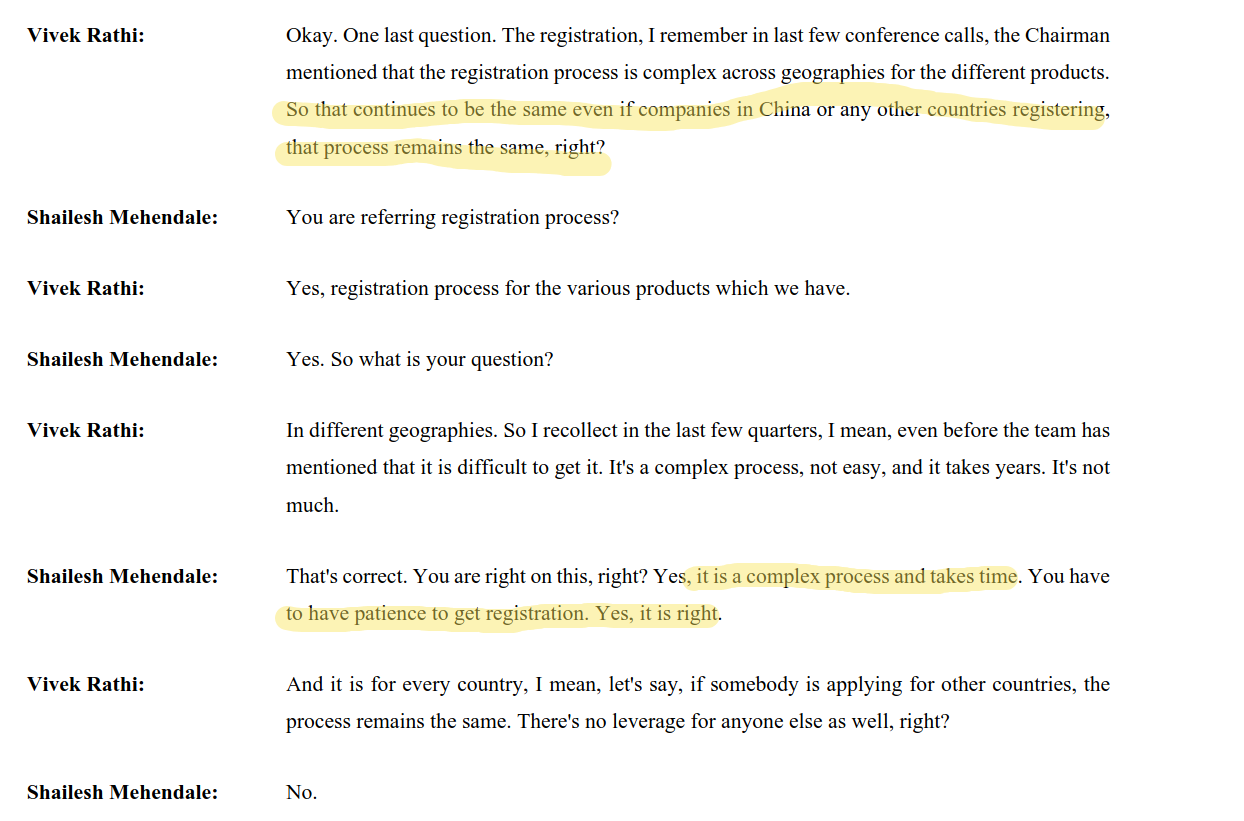

From Sharda Crop chem about registration complexity:

Any idea how long will this stock be in ESM stage2? What is the outlook overall as the new facility is operational now. Mgmt did not do a concall post results. Disastereous performace this quarter.

Discl- Invested

Heranba Organics Private Limited, A Wholly Owned Subsidiary

Company of Heranba Industries commences Commercial

Production at its Sarigam Unit, Phase-II.