Initiating coverage report from Dalal & Broacha

6 Likes

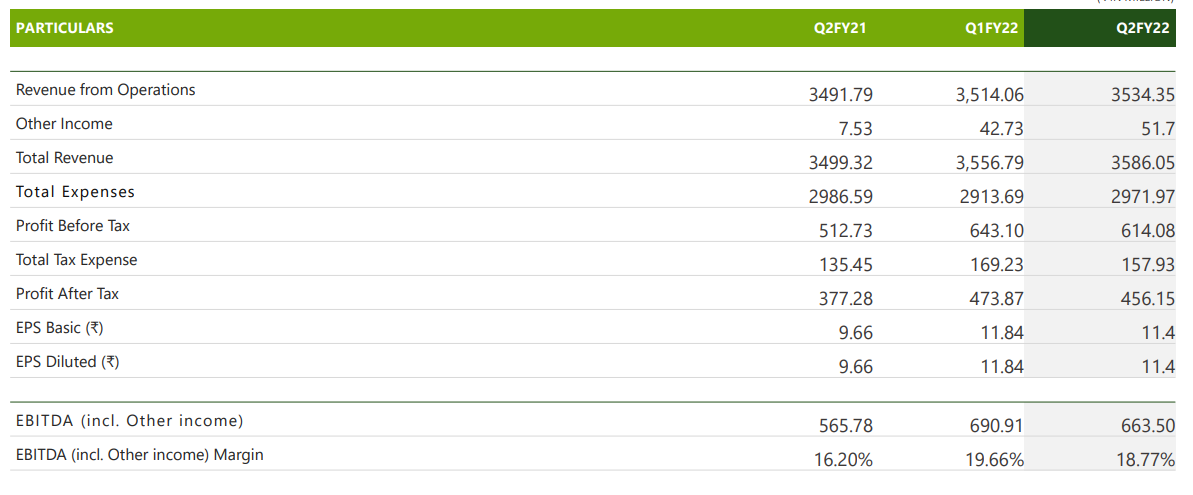

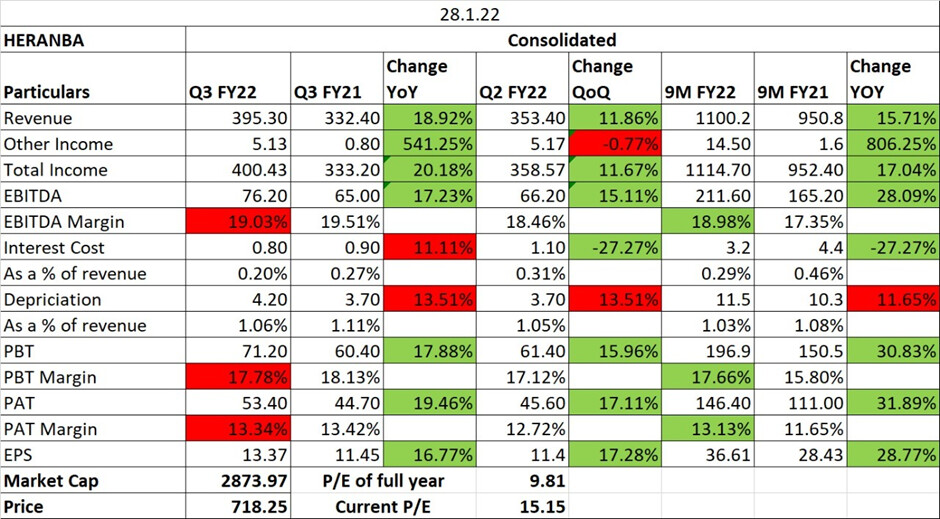

2QFY22

Revenue at INR 3,534.35 million up 1% YoY

EBITDA (incl. other income) at ₹663.50 million in Q2FY22 17% Y-o-Y

EBITDA margins were at 18.77% in Q2FY22 as compared to 16.20% in Q2FY21 Profit After Tax at ₹456.15 million in Q2FY22 +21% Y-o-Y

1HFY22

Revenue at INR 7,048.41 million +14%.

EBITDA (incl. other income) at ₹1354.41 million in H1FY22 +35% YoY

EBIDTA margin at 19.22%, compared to 16.20% in H1FY21,

PAT at Rs. 930.01 million +41% YoY

Mr. Raghuram K. Shetty, Managing Director of Heranba Industries Limited, commented, “I am pleased to report that we have maintained our growth momentum in the first half of FY22 by reporting a strong set of numbers. We saw an increase of 14% in our revenues and an increase of 40% in our PAT in H1FY22. Our continued growth trajectory in yet another half year and quarter shows the strong and resilient DNA that we are built on. We are dedicated to accelerating revenue growth and productivity efforts in order to achieve significant margin expansion, and we continue to view FY22 as a crucial acceleration point in Heranba’s trajectory.”

3 Likes

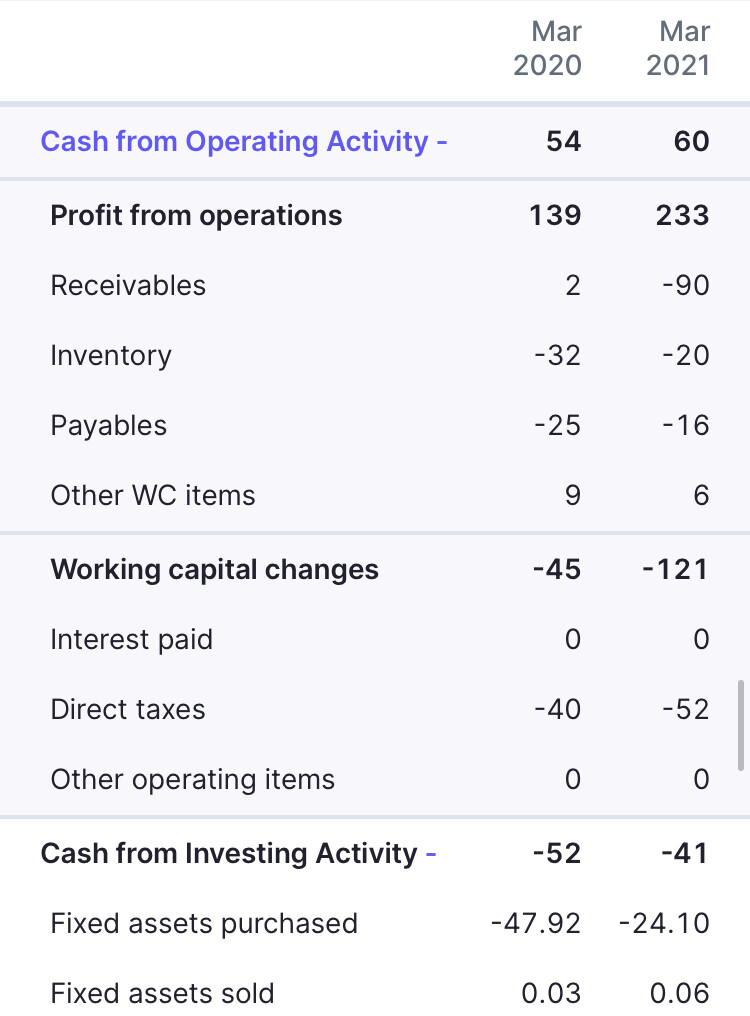

Look at the cash flow from operations!

Regarding your CFO obserrvation, following is the management response from the call, "There are logistical issues across the board in the industry due to paucity of containers.

So there is some pile of inventory. Q2 end usually receivables are higher. Both issues should get resolved by the end of the year"

Company has maintained the guidance of 18-20% revenue growth and 18-20% EBITDA margins for the full year.

4 Likes

This is an industry trend. The technical agrochemical industry always has a long working capital cycle and money is stuck but it is nothing to be skeptical of as you will see this in any company in the industry

1 Like

Isn’t that a con for industry, lower cashflow conversion means lower free cashflow hence lower valuation for the companies

Would you have ignored Bharat Rasayan for the same reason? It’s in the same industry and so is Astec Life sciences. The growth in this industry is excellent and for a long term. Cant look at many industries and say high growth for next 3-5 years atleast. According to me, this company will compound sales at 18-20% easily for the next 5 years. I can’t find many companies who can do that. The growth trajectory is very clear here.

3 Likes

CFO conversion could be the key monitor able ahead . Else on growth & margin fronts they are doing good .its a candidate for rerating whenever the CFO numbers starts to deliver . Management has guided that issues of CFO will be resolved by year end in their last concall post Q2 results .

3 Likes

Heranba purchased 14 acres of land. Any idea as to the cash out flow for the purchase of land? Co has not disclosed any details about the consideration.

2 Likes

Heranba Notes:

Introduction:

- Leading agrochemical player in India.

- HERANBA’s mission is to improve Crop Productivity and Public Health. It is committed to the wellness of world citizens.

- Manufacture Synthetic Pyrethroids and its intermediaries.

- Heranba has three independent manufacturing units. Two of these units are are involved in production of various Technicals and intermediates, while the third plant is purely a Formulation and Packing facility.

Advantages:

- Fully integrated facility for pyrethroids and limited dependence on China for raw material procurement, should ensure operating profitability stabilizing at 15-18 percent.

- Might incur capex of 150 cr in 2-3 years (from internal accrual). The manufacturing facilities are located in Vapi and at Sarigam near Vapi. It is currently expanding its capacity at Sarigam and also possess additional land bank at Saykha, Dahej for future capacity expansion.

- Present in the entire value chain of products in the agro chemical industry

- Market share of 20%

- Continuous addition of new products is being done

- No debt obligations

- Liquidity will remain strong

Disadvantage: Large working capital requirement, High debtor days

Future: Revenue will grow 18-20 CAGR, can also take up contract manufacturing, focusing on regulated market for better margins, debtors days will be reduced. In November 2021, the company added 1,200 MTPA to its original capacity of 14,024 MTPA. The new capacity will be gradually ramped up and the revenue potential is about INR 1,000 Mn at 100% capacity utilization. Additionally, it is expanding its capacity at Sarigam near Vapi, in a phased manner. About 5,000 MTPA will come on board by September 2022. The margin profile of the expanded product portfolio is similar to the current margin.

Management expects to maintain operating margin in the 18%-20% range going forward. We believe that higher exposure to exports will facilitate margins to remain in the higher range of the guidance band.

News:

22 Nov: Ann: Commencement of Commercial Production from New Unit-IV.

- Heranba expects this new Unit IV to generate annual revenue of Rs.100 Cr.

- The Production Capacity and Capacity Utilisation of this new Unit-IV will be 1200 MTPA at maximum capacity.

- Further no more Capital Expenditure will be required in near future for this Unit-IV.

- Company is dedicated to accelerate revenue growth and to improve productivity in order to achieve significant margin expansion.

- It continues to view FY22 as a crucial acceleration point in Heranba’s growth trajectory.

Financials:

- Ratios are good. Export margins are higher by about 3-4%.

- Trade Payables are high and increasing

- Inventory increasing and high

- Debtors also increasing and high

- Increase in promoter shareholding

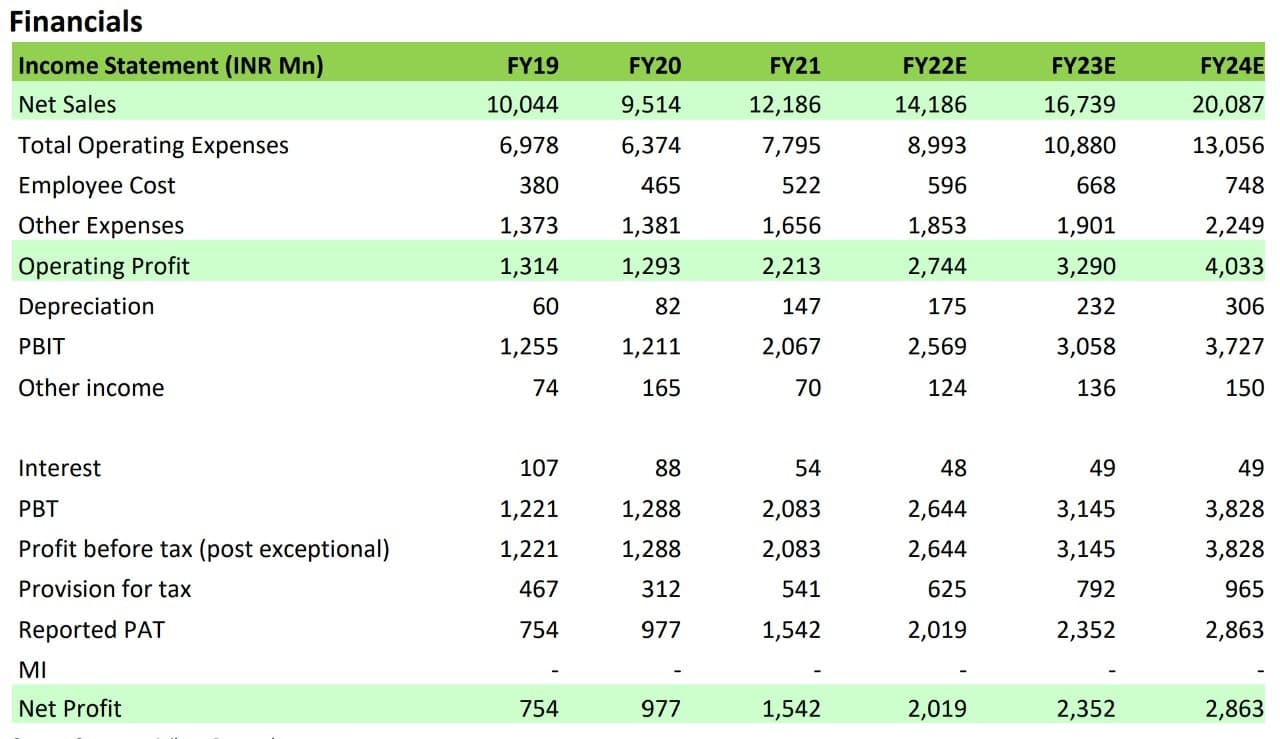

Estimates of Heranba P&L by Arihant. For full year thier estimate is 1418.6 cr. By H1FY22, they have already achieved 704 cr. PAT also they have estimated 201 cr. By H1FY22, they have achieved 93 cr. Q3 results on 29th Jan.

4 Likes

http://arihantcapital.co.in/research/19-01-2022/Heranba%20Industries%20Ltd_Initiating%20Coverage.pdf

1 Like

Q3 Result.

Great Results by Heranba Industries! Seeing a good future as well!

Lets see how things pan out for the future of the company.

9 Likes

Can you share the link to concal… I couldnt find it anywhere

2 Likes

I would to get input from experience members that what can be reason to create the below subsidiary which will work in field of agro-chemical. Isn’t that Heranba in agro-chemical. Any red flag?

4 Likes

it is a wholly owned subsidiary so there is nothing to worry about.

Corporates create wholly owned subsidiaries for entering into a new business or location without putting parent company at risk.

1 Like

Anyone having notes on Concall please help share

1 Like

Heranba_Q4FY22_Result_Update.pdf (357.0 KB)

2 Likes

Growth can be much faster than their guidance of 18-20%. As their third phase which is the last phase capex gets completed by Q2FY23.

Management mentioned that it takes a year to ramp up utilization to 75-80%.

By end of FY24, can easily do 80% utilization.

So, growth can be 25% + if they deliver.

Key risk - capex being completed on time

1 Like