Hi All

I was looking at some historical rather since inception all holdings in HDFC Bank by Sanford C Bernstein Mutual Funds. This is the same Bernsetin which came out with the recent report.

They have 3 funds which hold HDFC Bank as per the data analysis I have done. They show 3 months holdings (Jan, Dec, Nov) on their website. But one can run a short python script and fetch data tweaking their URL to get data going back to 2010 and even beyond. They seem to have not taken their data tables offline. I did that to see how their holdings in HDFC Bank has evolved with respect to their ratings, target prices and stock price.

Before sharing that let me also call out that I might be biased as my family has held HDFC Bank since a decade before Bernstein initiated coverage. Also last time I tweeted on biases and factual inaccuracies I have been getting odd comments. Wont dig deep into those as I have sort of narrowed down on a few of these fake accounts myself which were created only for one purpose. A waste of time IMHO.

Bernstein (BRNSTN) today has 3 MFs which hold HDFC Bank -

- Emerging Market (EM F)

- Tax International Managed Fund (T F)

- International Funds (I F)

Emerging Fund was the first to add HDFC Bank in Aug 2010. The other two only added in May 2017.

These 3 funds have very poor performances. IMHO they are worse than term deposits and in some case savings account returns too. Here is a snapshot of their returns. These returns are as on 29 Feb 2020

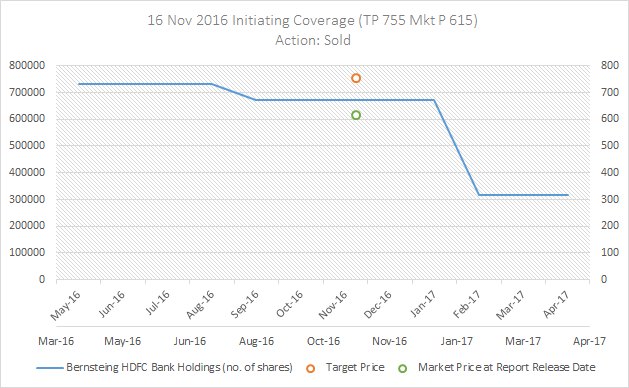

Nov 16: Initiated coverage at 755 when stock was at 615. By end of Feb 17 they cut their position by more than half in Emerging Market Fund. Target was achieved only in end of April.

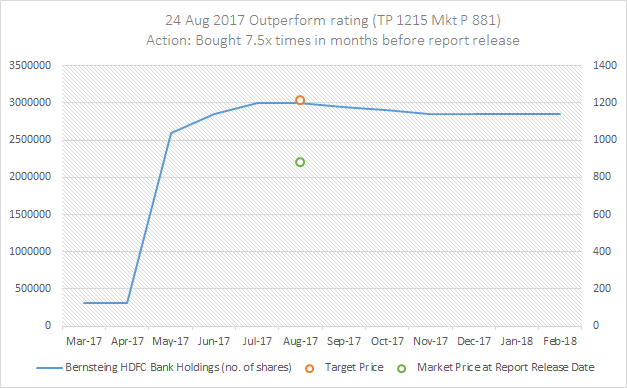

Tax Fund & International Fund added HDFC Bank in May 17. Both had more shares of HDFC Bank than Emerging Market Fund. In Aug 17 TP increased to 1215 when Price was 881. Before that for 3 months position was increased across all funds.

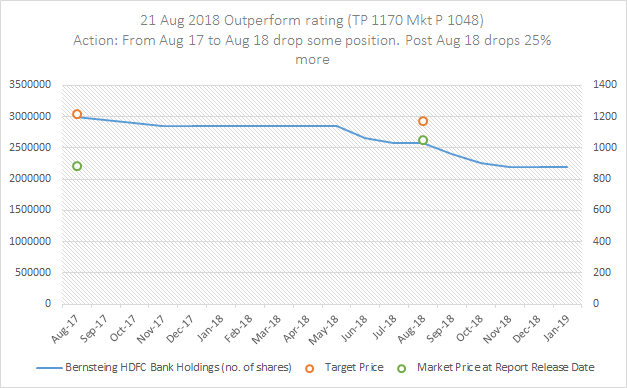

Then from Aug 17 again started dropping position till the next report in Aug 18. Target was 38% above market price & TP was never achieved.

In Aug 18 TP lowered to 1170 but above market price of 1048. Drops another 25% of position in this period.

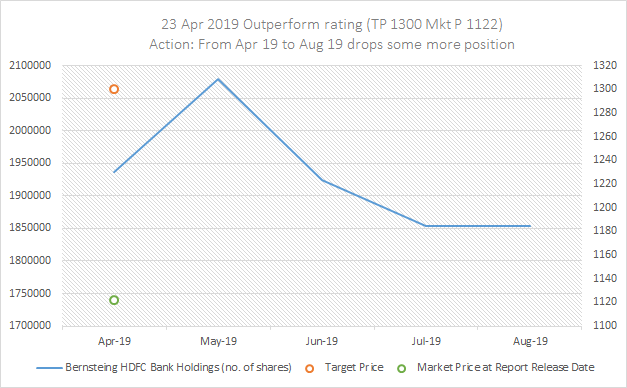

In Apr 19 TP increased to 1300, market price at 1122. Drops a little more position till release of next report. TP not achieved in this period too.

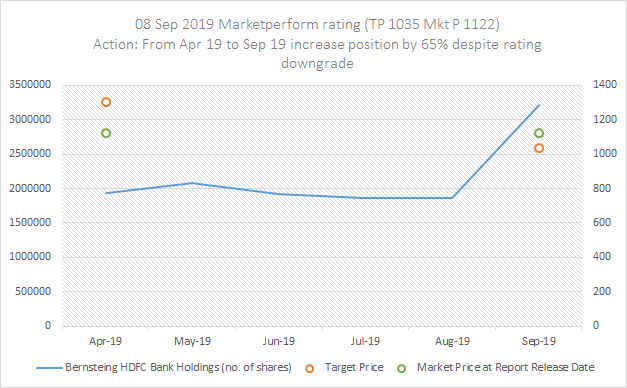

In Sep 19 TP slashed to 1035 when market price is 1122. And they increase their position in a month’s time. TP not achieved too.

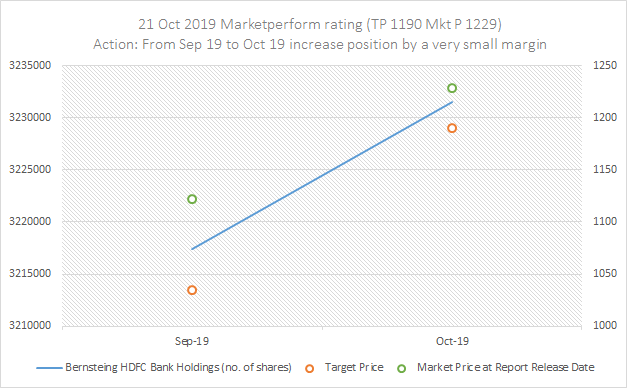

In Oct 19 TP increased to 1190 & position increased by a mere 0.4%. TP is achieved in this period.

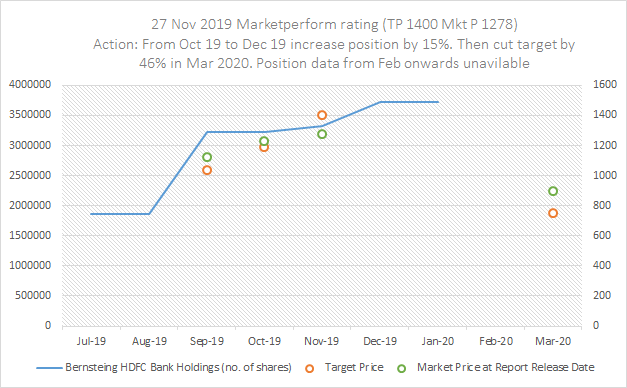

Next month Nov 19 TP further increased & position also increased by 15% by year end. TP not achieved in this period. 3 reports in successive months pushing TP up & buying in that period.

Mar 20 TP slashed by almost 45% from 1400 to 750. Position not disclosed beyond end of January 2020. Lets see when the data comes how this looks.

There is a Chinese wall between the sides I believe in every such organisation.

My personal learning over the years is try to read between the lines, understand biases which people underestimate greatly, also understand the bias I personally have.

Rgds

Deepak

Note: I didnt even know such an organisation existed so I dont know anything about them other than that and some numbers. Dont want to waste anymore time on it.