An interesting article from BloombergQuint (free to access) showing how HDFC Bank have been growing their wholesale loan book more than their retail loan, classic countercycle attitude. When everyone wants to give money to retail, they move back to wholesale. However, its important to note that they are building up on SME book rather than large corporate book.

4 Likes

https://forum.valuepickr.com/t/hitesh-portfolio/658/4485?u=arunjacob

Do we have know whats the exposure of hdfc to different telecom players companywise .

The total exposure of hdfc to telecom sector is 3% of books & telecom sector is under stress.

1 Like

Please read this tweetstorm by @deevee how he compared the poor report and analyst quality of Berstein vs that of UBS analyst, the guy who exposed Yes bank as early as 2015(if I remember correctly) and then decide yourself which one to follow

It simply amazes me how Indian market is so vulnerable to any hoax news/report/sensation etc

https://twitter.com/deepakvenkatesh/status/1240874971674492928

13 Likes

I agree. Most of these downgrade/upgrade by analysts is garbage. But do you think the fall can be attributed to such reports?. I dont think retail buying/selling will impact a 5 lac crore market cap company. And I doubt institutes use brokerage reports for buy/sell decisions.

I would say let us not ho by market cap as companies with market cap as high as 50-1lac cr is yes bank/DHFL/P C JEWELLERS etcetc have gone to dust

No. I was referring about correlation between brokerage report and market reaction. (For such well researched large companies)

Remember reading in some investment book (think Peter Lynch?) to check if the mid-management team is selling the stock than a single person from senior management team.

With current uncertainty on CEO hire, did some analysis on HDFC Bank’s insider trades:

| Category | Q4FY20 | Q3FY20 | Q2FY20 | Q1FY20 | Q4FY19 | Q3FY19 | Q2FY19 | Q1FY19 | Q4FY18 | Q3FY18 | Q2FY18 | Q1FY18 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ESOP | 2532900 | 1761612 | 558900 | 2192740 | 3756227 | 1818196 | 8411281 | 9057100 | 4861050 | 5929700 | 9167000 | 11067900 |

| Purchase | 2815 | 0 | 0 | 0 | 1300 | 1000 | 4500 | 0 | 0 | 895 | 445 | 950 |

| Sale | 2207593 | 2957324 | 1173460 | 708773 | 1643766 | 1134312 | 562644 | 1352834 | 822770 | 783227 | 1240377 | 1552836 |

| Acquired - Sale | 328122 | -1195712 | -614560 | 1483967 | 2113761 | 684884 | 7853137 | 7704266 | 4038280 | 5147368 | 7927068 | 9516014 |

| Cumulative Shares Holded | 44986595 | 44658473 | 45854185 | 46468745 | 44984778 | 42871017 | 42186133 | 34332996 | 26628730 | 22590450 | 17443082 | 9516014 |

My inferences:

- Amount of ESOPs being given to employees is in the downtrend from FY18 to FY20

- There was a bit of selling Q3FY20 but doesn’t look alarming

- Cumulative shares (only from Q1FY18) to employees being hold throughout FY20. This can imply that the mid-level management employees are happy to stick with the growth of the company even after management change.

People interested in quarterly data can look up this sheet:

https://docs.google.com/spreadsheets/d/1506pRPjqeCgKUBID19cuQboko2cjUF1fPjNyOwHi4ak/edit?usp=sharing

Please excuse human errors while developing this data into above structured format.

Discl: Largest holding in my PF. This is not a buy / sell recommendation. Please do your own research.

14 Likes

Today’s interview

invested

6 Likes

The lock down will surely have negative impact. The trick is to estimate how significant and how much is reflected in the price. Investors should also look at likely impact on the subsidiary HDB Financial service which apparently has lower quality book to chase higher yield. This idea of “going one or two levels down to get higher yield with higher NPA to get right RoE” can be a matter of serious concern if there is large stress.

2 Likes

Study the Background of the analyst You will realise some biases.

Hi all

I thought of putting down my tweets on this thread but I guess my link is already here so you can read that. My intention was to show biases which all of us have. My family has held HDFC Bank for a long time so I too have a bias. So weight it with that in mind.

Also many folks wanted to read the UBS report on YES Bank. Here it is uploaded.

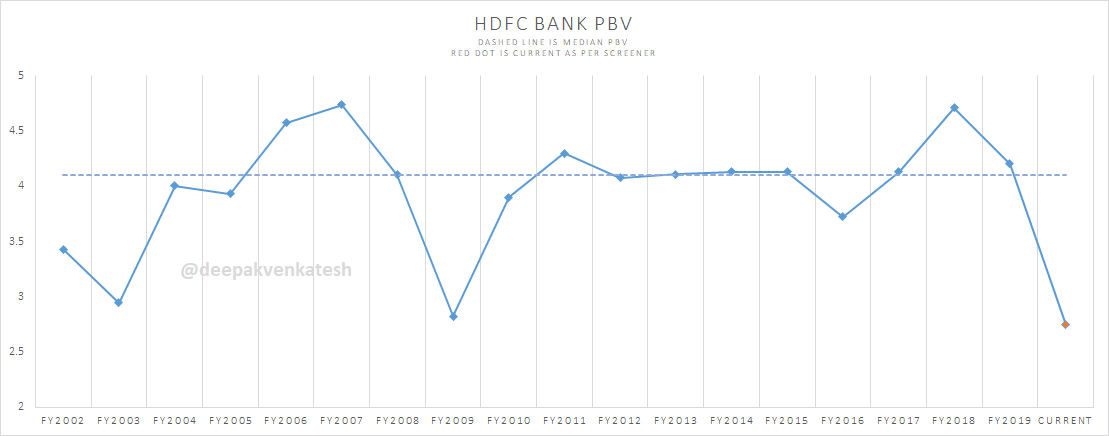

Aside, HDFC bank has gotten cheapest in the last 20 odd years on price to book terms. For a moment assume the book value holds and is true. Which I hope it is after my lucky escape from YBL.

The price has corrected over 40% from peak right now and lowest valuation. The price correction in early 2009 was 60%. So worst case no one knows but historical worst case we know is roughly at 560 per share.

Now coming to management change. We should be skeptical for sure. But being outright dismissive without factual knowledge is not called for. Infact journalist from Hindu Business Line asked Mr Puri yesterday on concall that the Bernstein report had something to say about leadership change. Mr Puri retorted saying that he should have contacted us and we would have told him. Lets see how it goes.

Yes Bank UBS July 2015.pdf (696.1 KB)

Rgds

Disc: As mentioned I have investments in HDFC Bank.

7 Likes

I am not sure the book value will hold. There are going to be wage cuts, downsizing. Non-essential items (real estate, consumer durables, automobiles, hospitality etc) will see a drastic fall in demand. Companies will have a cashflow crunch. We will see defaults in Commercial Paper, corporate loans, unsecured retails loans.

Yes there will, inevitably, be government intervention. But that will be to keep businesses afloat. Not to sustain high market valuations. That is my guess.

The problem is not even close to being at its peak. Historially, markets have taken anywhere between 1 month to 9 months to bottom out. For all we know, the problem may just have begun for India, rest of South/SE Asia, US and South America.

The situation that we are going through right now is unprecedented. You cannot compare this to the previous crises or valuations of markets.

2 Likes

@fabregas Agree with your assessment and views. Though HDFC Bank can be a major beneficiary in the Banking sector when Corona and related economic issues settle down. The economic damage of corona on India is unknown at this point of time and this can lead to retail defaults (will be lower for HDFC Bank as compared to other Banks), slow credit off-take can lead to lower revenues for the next 12-18 months. Leadership change is also a overhang.

There is a possibility of lower valuations. Banks & Financials have enjoyed high valuations between 2016 to early 2020. Post a market crash and when a new bull run commences, historically leaders / sectors of previous bull markets have always had a low valuations despite good financial performance, Ex. Tech in 2000, Infra in 2008 (GFC), Pharma in Mid 2010’s, etc. Will Banks, incl HDFC Bank’s valuations trade below current valuations?

Shall appreciate views from other boarders.

regards

Disc: Invested in HDFC Bank since 2016

2 Likes

Can somebody post both UBS and Bernstein reports so that we can see both sides of the investment argument?

Regarding management change, please note that there have been umpteen companies which have successfully done CEO succession. The hero worship of a “superstar CEO” is many times a result of media hype which is unwarranted. It is the larger team inside the company and the culture which matter a lot. Surely, there are capable leaders out there who can take HDFC Bank forward. Would rather like to see a low profile CEO who just delivers solid growth and profitability!

1 Like

Hi

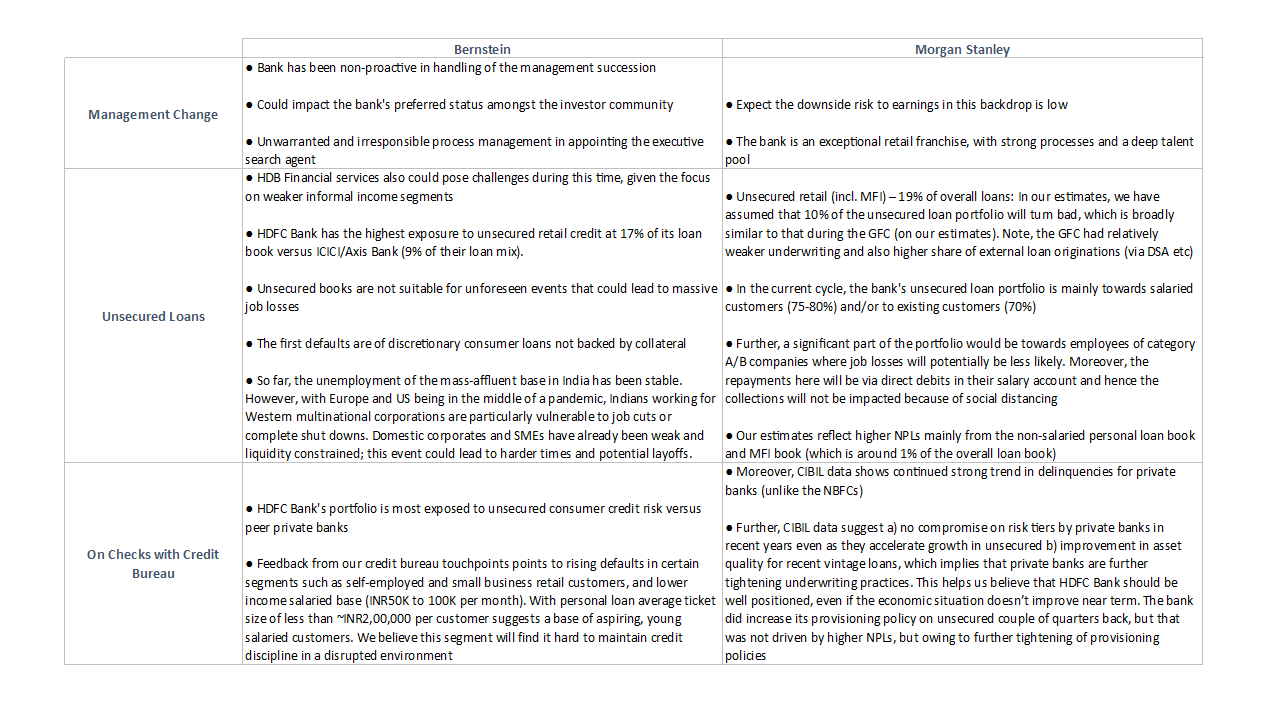

Some notes from both the Bernstein report and the recent Morgan Stanley report below. One feels like a second order thinking & the other slightly superficial. My viewpoints. You may choose to differ.

Rgds

Deepak

8 Likes

I am fairly new to the investing & HDFC Bank hold >10% of PF.

In this particular case I believe, even HDFC is not prepared for the kind of impact Corona might have. In Aditya Puri invterview, he has asked for forbearance & also HDFC is expediting the process of naming the successor , seems to me they are trying to placate the market,which has been unseen in the past, I hope I am wrong. just my thoughts. I dont have any data to support it.

These are black swan types of events and not one can be prepared enough. If you are prepared too much for something like this then you can not grow at reasonable pace.

2 Likes

If stock market has to be alive and companies have to survive, the companies like HDFC bank, Colgate,Asian paints, Bajaj finance,Britannia, pidilite,Nestle etc or the best of companies would come back to life. If we feel that even these companies will not survive, then we are dead as an investor and stock market is buried with us for ever.

I have passed through 2008 crisis too wherein my holding value came down to around 20%, but zoomed back in 2009 when no one expected.I hope that top companies will survive and become much stronger but do not have the courage till the situation clears after seeing my holding going down to 50% in a month.views invited

Dics:Invested but hardly did any transaction in last 30 days out of fear

7 Likes