Well, my comment was that even a hint of some hide and seek game being played here will have significant dislocation in the banks in general. You would agree that change in leadership after long tenure leads to kitchen sinking etc. This RBI deferment would lead some kind of confusion. I am not suggesting any impropriety here but even the best of companies are not immune to hiccups during changeover and the current scenario would make this an explosive mixture.

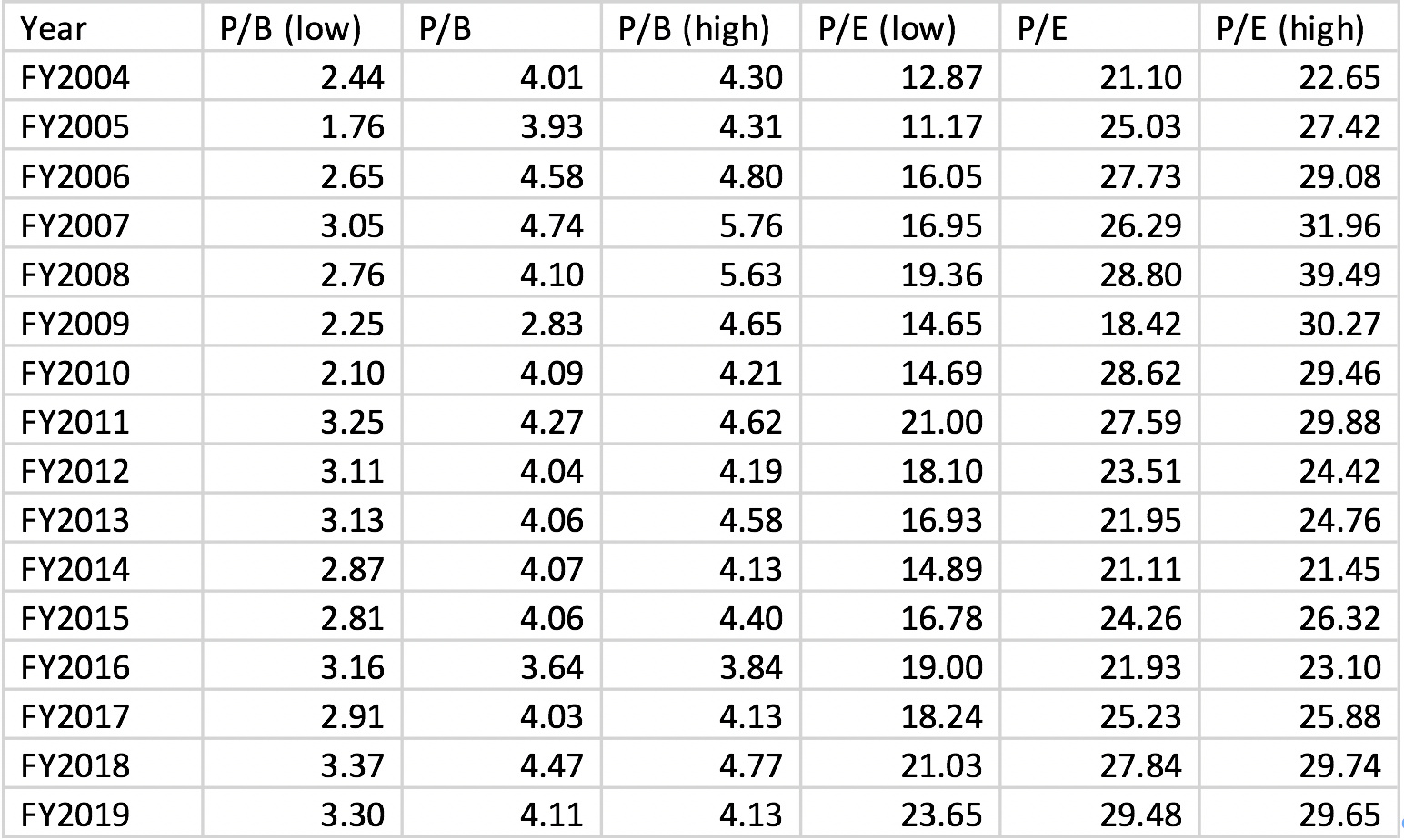

Here are the valuations going back to FY2004. Its clear that valuations < 2.5 is very attractive and doesn’t come about too often. On a P/E basis, anything below 16 times is attractive. This is assuming HDFC bank continues to maintain its lending prudence in the future.

6 Likes

Hi All,

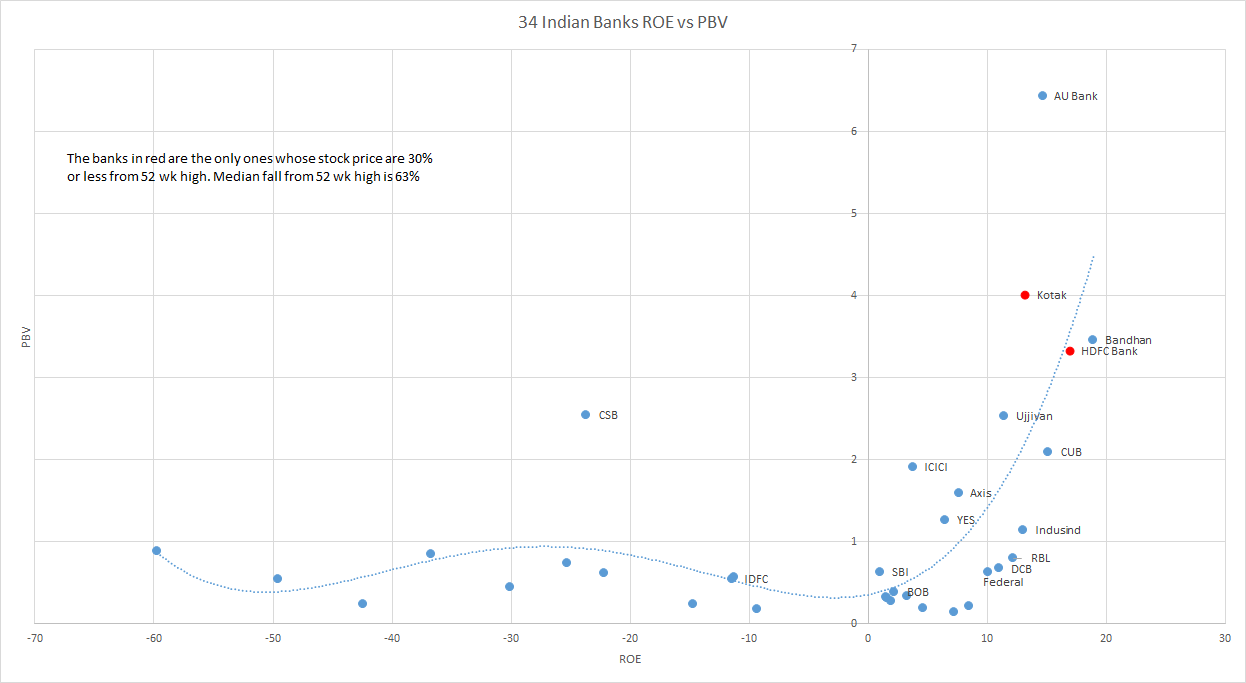

Any thoughts on HDFC Bank v/s Kotak Bank? Why is Kotak Mahindra Bank so much more expensive than HDFC Bank especially when HDFC Bank is the leader?

Disclosure : Invested.

Please go through the entire thread,it will give you amazing insights into this.

When it comes to the business of banking,HDFC Bank is second to none,All this has happened while one Mr. Aditya Puri has been at the helm from September 1994 to the time he turns 70 on October 26, 2020.

Like it or not,a cult following tends to build around bankers,and it is impossible to replace Mr. Puri and therefore the market participants are nervous about who will be the successor,being hit by the Covid crisis at the same time has complicated things further.

Kotak trades at a slight premium at the moment because:

1.Their Loan book is 1/4’th the size of HDFC Bank and thus means that they may be able to grow at higher rates for a longer period.

2.Uday Kotak will be 70 in March 2029.

3.Kotak has AMC,Life and general insurance business that comes along with the Bank.

4.Kotak has a higher CASA but that was built with higher 6% rate which they have strategically cut to 4.5% recently,this has been done brilliantly and given the current circumstances I think they will still be able to maintain CASA above 50%.

Apart from interest rates coming down in the system the other major trigger for this is that they may be anticipating credit losses and have done this to give the balance sheet a further cushion to absorb this.

16 Likes

It’s strange to share video song on this platform

But it’s HDFC Bank official motivational song

Nice to see positive management attitude

2 Likes

There is no easy solution to valuation. As you rightly mentioned P/B < 2.5x is very attractive but comes once in probably 7-8 years? And company is compounding its profits by ~20%, so if one waits for right valuation, there is so much of compounding that is missed. And many a times, such growth company gives lower multiple when future growth is bleak. Recent examples >> Eicher, La Opala, Page Industries etc.

3 Likes

Another case in point is Microsoft, when Steve Ballmer was burning money left,right and centre. Microsoft became a big value trap from 2001-2014. Valuations collapse and come to steady state multiples when the growth stops or growth is temporarily impaired. Interesting case in point is PI industries, where growth was impaired from 2015-2018, yet company kept trading at high multiples. Entire value of a business lies in the growth that is ahead of us and management’s ability to execute. That is why some businesses will always be expensive (not asking you to buy), just looking at the multiples and not the competitive advantage period and companies ability to keep earning economic profits over a long period of time is bias which I have fallen for as well

3 Likes

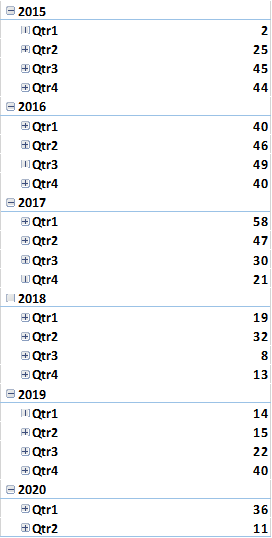

Hi

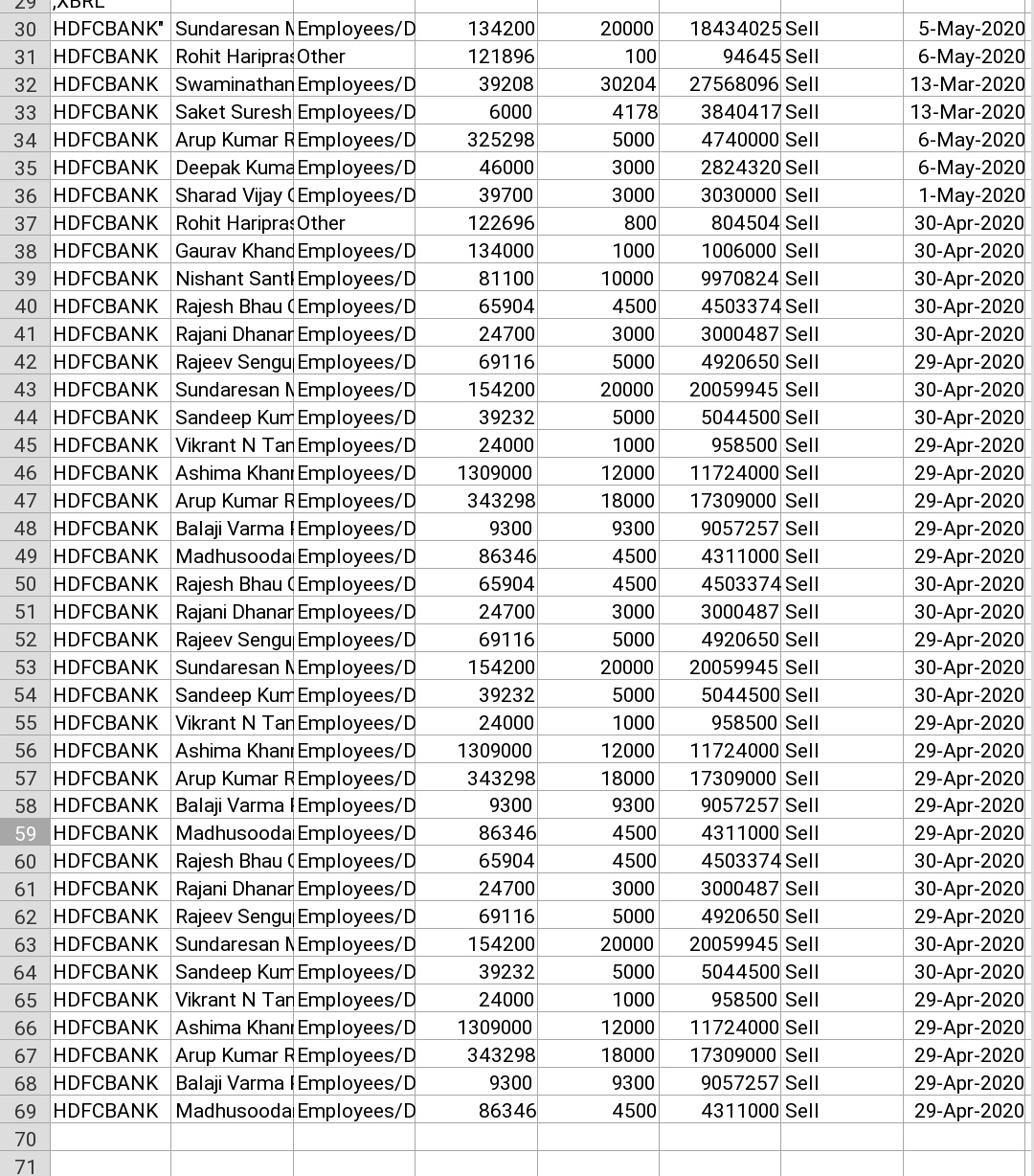

I did look into this. Here is the number of folks selling shares in the market each calendar quarter since 2015.

With a biased mind I would say its fine.

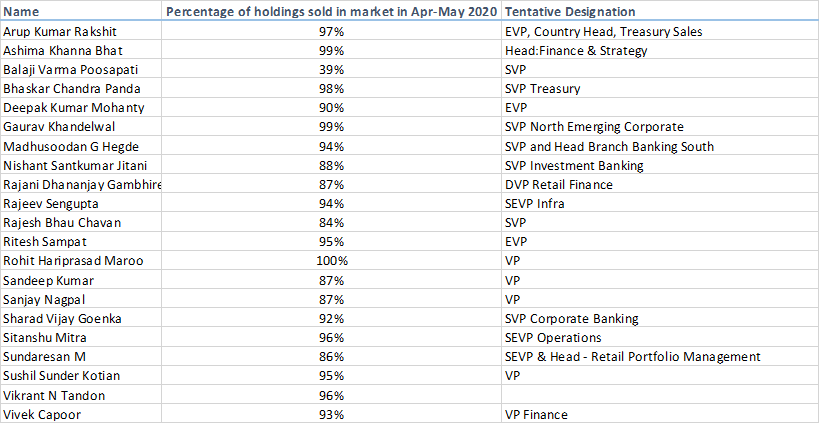

Also I looked into who all had sold. I tried to understand how senior they are. The exact designations could be different.

We had some folks acquire shares from the open market also.

Rgds

Disc: Biased since I am invested.

12 Likes

a lot of times they sell shares to acquire new Esops as well. recently even aditya puri did the same

1 Like

HDFC Bank subsidiary, HDB Financial Services sacks several during lockdown - https://www.livemint.com/companies/news/hdfc-bank-subsidiary-hdb-financial-services-sacks-several-during-lockdown-11589043618135.html Download mint app for latest in Business News - https://bit.ly/32XEfFE

HDB @150 branches are closed

/ In AP TS 25branches are closed

Overnight they had taken decision

Given 3 monthly salary n immediately relieving

Around 5000 employees affected.

@ Hyderabad 4 branches are closed

1 Like

Just received and sms from the bank today “Moratorium for loan xxxx is enabled.If Autopay is enabled,disable it via Net/Mobilebanking.we will enable it in Jun 2020.interest is applicable if moratorium is availed.”

I have not requested any moratorium,so am surprised that the bank has now sent this message.

The bank had earlier said that less than 10% customers had availed the moratorium,so now they have by default enabled it across the board?

1 Like

Have they switched from opt in to opt out?

A few customers may have been unable to pay but did not avail moratorium.

Also the message itself says that If autopay is enabled it needs to be disabled and they will enable it back in June,so that customers who cannot pay are nudged to avail the moratorium.

But since the bank does not comment on these things we will come to know only when the results for Q1 are declared in July.

Interesting video on how Risk management team work and second video on daily operations and technology use in COVID time for HDFC Bank

2 Likes

Not directly related to HDFC Bank - but banks in general - for amount in moratorium.

discl - invested in hdfc bank.

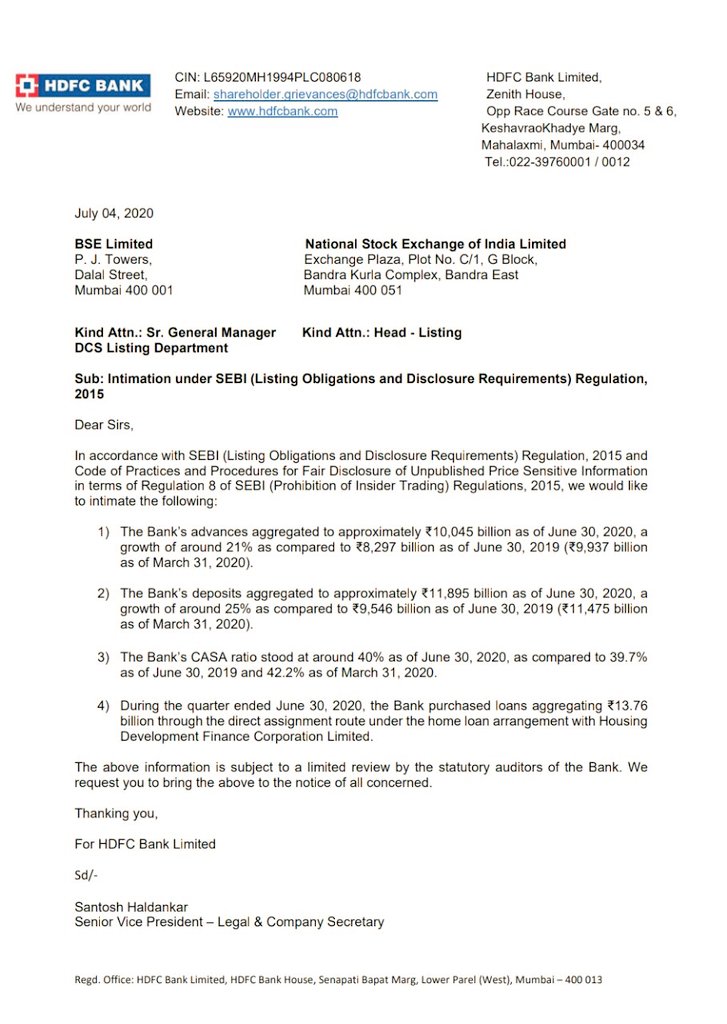

From BSE announcement

- The Bank’s advances aggregated to approximately ₹10,045 billion as of June 30, 2020, a

growth of around 21% as compared to ₹8,297 billion as of June 30, 2019 (₹9,937 billion

as of March 31, 2020). - The Bank’s deposits aggregated to approximately ₹11,895 billion as of June 30, 2020, a

growth of around 25% as compared to ₹9,546 billion as of June 30, 2019 (₹11,475 billion

as of March 31, 2020). - The Bank’s CASA ratio stood at around 40% as of June 30, 2020, as compared to 39.7%

as of June 30, 2019 and 42.2% as of March 31, 2020. - During the quarter ended June 30, 2020, the Bank purchased loans aggregating ₹13.76

billion through the direct assignment route under the home loan arrangement with Housing

Development Finance Corporation Limited.

Fairy reasonable performance in lockdown situation

3 Likes