Don’t you think you should use p/b ratio for valuation instead of pe ratio for banks.

PB is a good proxy if there are large provisions/opex that are going to mask the real earnings of the bank, eg axis and icici from 2015-2019. In a steady state we will have to look at a lot of factors, a bank with a pb < 1 is not really cheaper than a bank with a pb = 2 if the latter has better RoA and RoE as it can compound book at a faster rate.

15 years later when credit starts to saturate and things slow down and banks dont grow as fast it will be the PE that determines the dividend payout, whereas unless the bank is getting acquired the book value will never actually be realised be investors

7 Likes

50/- arbitrage opened up on the swap ratio again for anyone who wants to make a free 3.5-4%

disc: converted remaining hdfc bank holding to hdfc

1 Like

What if by the time swap is recorded, hdfc bank falls the gap percentage instead? No arbitrage then…how can we know if ever there is an arbitrage as we never know which ones out of 2 would rise or fall in future to bridge the gap?

3 Likes

Only two ways for the arbitrage to get filled

Ltd rises more than the bank

Bank falls more than Ltd

In both cases it is better to be with Ltd. Doesn’t matter how we own it.

Then your holding are not falling while the company is getting cheaper. Not falling while the other is, is an arbitrage

Considering Mr. Market’s current mood, HDFC combined entity is available at a P/B of 2.6. By the time planned merger completes (projected 18 months), Book Value would have grown by ~23% (assuming 15% annual ROE for each entity) and P/B would be 2.1 basis today’s Mkt. Cap. Let’s see how it unfolds.

Basic Maths as below:

| Items | Today: Combined |

+18 Mths: On Merger Completion |

Remarks |

|---|---|---|---|

| No. of Equity Shares | 736 | 754 | 1- Post the effective date, HDFC’s shareholding of 21% in HDFC Bank will be cancelled. 2- HDFC Ltd shares will be converted to 42 shares of HDFC Bank for 25 shares 3- Assumed 1.5% dilution(ESOP) |

| Mcap | 1085200 | @ Today’s Mkt Value | |

| Book Value | 419640 | 516157 | Assumed Book Value Growth @ 15% in 12 Months, which would become ~23% in 18 months |

| P/B | 2.6 | 2.1 | |

| 16/06/2022 | |||

| HDFC Bank Ltd | |||

| No. of Equity Shares | 555 | 438.45 | |

| Mcap | 711200 | ||

| Book Value | 240093 | ||

| P/B | 2.96 | ||

| Dilution | |||

| HDFC Ltd | |||

| No. of Equity Shares | 181 | 304.08 | |

| Mcap | 374000 | ||

| Book Value | 179547 | ||

| P/B | 2.08 |

6 Likes

This might be due to the merger of HDFC LTD and HDFC banks which is yet not completed.

Some of the deals that HDFC Ltd currently does (like RE Land Financing) will be difficult in the merged scenario since they will have to adhere to bank regulatory norms. Hence the base will itself will be different ( lower) in such a scenario and any growth assumptions will need to be taken from that lower base and not the present consolidated base.

PS : No holdings.

1 Like

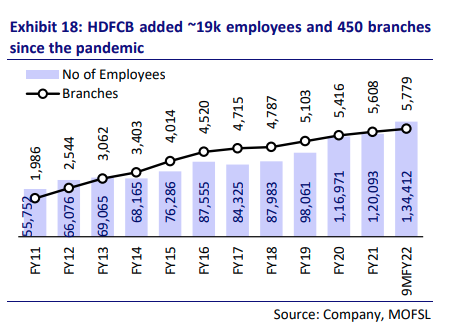

Market seems to be downplaying the branch expansion driven lending growth that should occur in the bank. From the current 6,000 odd branches, HDFC bank plans to add 1500 to 2000 branches a year, or 25% to 30% growth in distribution. These branch managers will be expected to bring in business for the bank, hence the loan growth should also mirror these numbers somewhat (although with some lag), not considering the same store growth from existing branches that should add to the growth.

4 Likes

1 Like

Another incident which proves that HDFC still has a long way to make their systems and infrastructure more stable and reliable

Quarterly business update for Q1 FY23.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/667a4818-9c38-43a6-a0e7-02da0225d5f5.pdf

4 Likes

Hi All,

In the annual report, the CEO has said “The enhanced capital position of the Bank post the merger also means that we can take bigger exposures in leading corporates and power the country’s infrastructure build out”.

Wholesale banking contributes to 55% of the total domestic loans. If going forward they plan to focus more on corporates and infra lending, I was wondering, arent these sectors which create the most pain in banking. They would be prudent in lending to these segments, but this part is something which concerned me a bit.

What the other members think about it? Thank you!

5 Likes

I think they ment to say they can now do it more easily without hurting much.

Like in the case of sbi most pain was there but still no effect on fundamentals due to their enormous book same could happen in hdfc where some more exposure to more core segments that are more secure so they can handle larger pain.

So they might sacrifice on NPA but will gain heavily in loan growth potential that might be very helpful in strong economic growth.

Historically it is been one management that has walked the talk to near perfection and if we look they prefer lower growth over a higher chance of NPA so is there any underlying in the whole economy that most banks might not be focusing on that is high stability and growth in MSME and big enterprises as if the growth story of export is even half correct there gain could be even greater then there past where they strategically avoided wholesale lending.

Also to note in the last few hits ie Gst,2008, Covid has already derailed a much-overleveraged business and if we just look at nifty even after having Adani stocks which have increased there borrowing but still the whole nifty borrowing is at there lowest with giants like Ril are very heavily in cash right then they have ever been.

Being an investor in the bank you need to know one thing exposure can turn sour quite quickly so being a little conscious could be good.

1 Like

I think otherwise:

- Considering the segment results from FY17 till FY22, retail segment’s average NPA [of total NPA Provision] is at 53% whereas Wholesale Banking’s average NPA is at 19%.

- Wholesale Banking’s contribution to PBT is also way higher than it’s revenue contribution [Data below].

- Retail’s CAGR contribution to the profitability has been way below double digit for a period of 3Yr. , 5 Yr. ,and 7Yr. [Data below].

In my opinion, the real game might be to source CASA from retail and maximize profitability with wholesale banking expertise.

Note - Attached the spreadsheet that I populated from past AR’s. Apologies as the data is in crude form but still usable.

Data [Base from AR with Author’s Calculation] for Point-2

| Revenue % Terms | ||||

|---|---|---|---|---|

| 2022 | 2019 | 2017 | 2015 | |

| Treasury | 14% | 12% | 15% | 14% |

| Retail Bank | 46% | 47% | 50% | 52% |

| Wholesale Bank | 27% | 29% | 25% | 25% |

| Others | 13% | 12% | 10% | 10% |

| Total | 100% | 100% | 100% | 100% |

| PBT % Terms | ||||

| 2022 | 2019 | 2017 | 2015 | |

| Treasury | 17% | 4% | 7% | 4% |

| Retail Bank | 18% | 33% | 34% | 35% |

| Wholesale Bank | 48% | 39% | 41% | 43% |

| Others | 18% | 25% | 19% | 18% |

| Total | 100% | 100% | 100% | 100% |

Data [Base from AR with Author’s Calculation] for Point-3

| 3 Yr CAGR | 5Yr Cagr | 7Yr Cagr | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Treasury | Retail Bank | Wholesale Bank | Others | Total | Treasury | Retail Bank | Wholesale Bank | Others | Total | Treasury | Retail Bank | Wholesale Bank | Others | Total | |

| Revenue | 13% | 9% | 7% | 12% | 9% | 11% | 12% | 15% | 19% | 13% | 15% | 13% | 16% | 20% | 15% |

| PBT | 90% | -8% | 21% | 1% | 13% | 40% | 2% | 20% | 15% | 16% | 46% | 6% | 19% | 16% | 17% |

Segment Results.xlsx (22.3 KB)

6 Likes

Curious why sudden change of heart as earlier focus used to be on retail advances as they were considered lesser risk. The percentage of npa you share seem to be for hdfc bank alone …what if we look at the overall retail vs wholesale percentages to see which is actually lesser risk as if hdfc bank grows the wholesale piece, it might have to venture into relatively higher risk pieces within the wholesale …they may have much better risk management in wholesale but if the overall piece is higher risk,sooner or later they may face it?

Or do they want to play this as a cyclical change for now which later they might run down when retails growth picks up?

Reason being is that they will get a huge housing(retail) loan book from merger with HDFC. So loan book becomes retail focused with lower margins. They will need to grow corporate book to maintain the balance and margins.

This is uncertainty which market is pricing in. Should get resolved over next 2-3 years for valuations to settle higher.

4 Likes

Q1FY23 Results are out.

1 Like

HDFC Bank FY23Q1 Results Summary

Revenue

- Rev: 27KCr UP 20% (exl trading & MTM losses)

- NII + OI: 26KCr

- NII: 19.5KCr UP 15%

- OI: (FY23Q1) ← (FY22Q1) UP 35% (excl Trading & MTM)

- Fees & comm: 5.4KCr ← 3.9KCr

- Forex & drv: 1.3KCr ← 1.2KCr

- Trading P&L & MTM: -1.3KCr ← 0.6KCr

- Misc(recovery & div):1.0KCr ← 0.6KCr

Expenses & Profit

- Operating expense: 10.5KCr ← 8.2KCr UP 29%

- CIR(excl-T&MTM): 38.6%

- PPOP: 15.4KCr (excl-T&MTM): UP 14.7%

- PBT: 12.2KCr UP 18%

- PAT: 9.2KCr UP 19%

- NP(cons): 9.6KCr UP 21%

- NIM(core): 4% / NIM(int brearing): 4.2%

Balance Sheet

- BS: 21LCr ← 18LCr UP 20%

Liability

- Deposit: 16LCr UP 19%

- CA: 2.2LCr / SA: 5.1LCr / TD: 8.7LCr

- CASA UP 20% / TD UP: 19% / CASA ratio: 46%

- New liability customers added: 26L

Asset

- Advances: 14LCr UP 21.6%

- incl transfers: Advance UP 22.5%

- Retail loan: UP 21.7%

- commercial & rural: UP 28.9%

- corp & wholesale: UP 15.7%

- overseas/total advance: 3.5%

- Advance(cons): 14.5LCr ← 12LCr UP 21%

- Risk-weighted Assets: 14LCr ← 11.5LCr

Capital

- CAR: 18.1% ← 19.1%

- regulatory requirement: 11.7%, incl:

- Capital Conservation Buffer: 2.5%

- D-SIB requirement: 0.2%

- T1 CAR: 17.1% ← 17.9%

- Common Equity T1 CAR: 16.5%

Branches & Employees

- new branches: 36 (T: 6,378)

- new employees: 11K (T: 152.5K <–123.5K)

- ATM/CDM: 18.6K ← 16.3K

- Cities/Towns: 3.2K ← 2.9K / 50% are in semi-urban & rural

- CSC business correspondents: 15.6K

Risk Profile

- GNPA: 1.28% ← 1.47%

- GNPA (Excl: seasonal agri): 1.06% ← 1.26%

- NNPA: 0.35%

- Floating provision: 1.5KCr

- Contigent provision: 9.3KCr

- Total Provision: 170% of GNPA

- Provisions and contingencies: 3.2KCr ← 4.8KCr

- credit cost: 0.9% ← 1.7%

HDFC Securities Limited (HSL) [96% holding]

- Rev: 432Cr ← 456Cr

- PAT: 189Cr ← 251Cr

- Branches: 216 / cities&Towns: 147

HDB Financial Services Limited (HDBFSL) [95% holding]

- ND-NBFC

- Rev: 2.2KCr ← 1.9KCr UP 13%

- PAT: 441Cr ← 88Cr

- Loan book: 62KCr

- S3/Gross Loan: 4.95%

- Total CAR: 20.3% / T1 CAR: 15.4%

- branches: 1403 / cities&towns: 1007

12 Likes