Key risk is post merger some of the key deals that HDFC does like Land Financing, General Corporate Purposes to Real Estate developers will be out of bounds since they will have to follow the conservative guidelines of banks ( as dictated by the Regulator). So once some of the existing book runs off, it cannot be replenished easily.

Disclosure : Exited completely post deal announcement.

Views are personal and not a recommendation. Please do your own due diligence.

The entire Indian banking market even now predominantly dominated by PSU banks in comparison to private banks and foreign banks. HDFC Bank and other private banks have long runways for growth, IMHO. Details can be accessed here

As an investor, we have some bias and sometimes it starts to hurt us a little, and when things start to shift we mainly ignore that as a short-term pain and make our own returns look bad in long run.

As Hdfc bank is a sizable position of my portfolio and also have been a customer for the most part of my life may it be my own finance or with my family have seen it grow and now become this big but does this have made them a slow runner.

Have watched recent icici bank results and have compared them to hdfc bank and looking at for so many quarters icici is actually beating quite significantly and also closing the gap in valuation and have seen better both loan book growth and their own customer response is either very close to hdfc or better especially in there app front at least that what most of the people say who have used both for a long period of time.

So how do you all think is hdfc slowing down or just collecting to go big have some thesis around the latter part that why it might just be having its bad phase to run now due to all rbi issues and will have pain for some time.

If we see the main part of banking it is a leveraged business where both pain and gain come after the event has happened and not directly so can this be an issue that due to restriction hdfc was not able to grow at a good pace and may do better in near future.

This can be a good case as right now after beating both icici and hdfc are at very similar valuations as there both price to book that is very important in banking is very close and the difference is not more than 15% that can be easily be reached so the main upside of icici is now mainly in terms of better growth so what are your views on does icici looks a better deal in term of loan book growth then hdfc or not and also in term of profit increment.

I personally don’t want two large cap banking stock in my portfolio that have around 13-15 stocks only so will only pick one.

HDFC (both the twins combined) is an elephant and we can’t expect the same level of growth witnessed in the last decade. However, the slowness in my humble opinion is attributed to few reasons mentioned below (not in any particular order)

-Leadership transition was not handled properly

-Compliance issues with one of the directors family involved in cross selling of GPS products against loans

-Cross holding structure that negatively impacts the other company whenever there is such bad news. HDFC against HDFC Bank and vice versa

-RBI ban which restricted them issuing fresh credit cards when everyone else was utilizing this opportunity to add more clientele (during covid19 times when online sales increased manifold)

-ICICI tie up with market place like Amazon to issue new premium credit cards

-Macro economic factor which resulted in FII pull back which became negative for HDFC twins

-Slowness in general insurance and housing loans due to COVID19 and cascading effect due to the large wallet share of HDFC compared to peers

sometimes I wonder, the way Nifty Index is constructed on the basis of technical parameters, like Volumes of shares traded during certain times , free float etc…The constitution of index and the criteria of adding and removing companies in index , tend to promote short term trading view , instead of long term inveting rationale…Kindly elaborate on this

Exactly! Short term Volumes are everything exchanges care about.

Indexes are constructed such as to benefit the underlying exchange rather than the investor who uses it as reference. Use them for a cursory glance, rely on fundamentals and build your own index.

The Other Bank Mentioned has better Loan book. However, only after 3/4 years we will come to know the quality of Growth. Previous cycles indicate the other bank has made many mistakes. Hope this time they have got it right. Please Study the composition of incremental loans. You will get many clues.

Note: This is a marathon Analyst meet conducted by Bank with detailed sectional videos and ppts. I realize that the sheer length of the post is too big. If this is distracting, just drop me a DM and I will simply share the link of Bank’s webpage where all these will be available,

But reading this not as good as listening to the video, at least the overview video with shashi.

Some of it is a little exaggerated like “we have 50-100 years of runway” but with all the market noise and gloom and doom happening this brought me back to the fundamentals of the bank and the excellent team behind it.

A standout statement for me was (paraphrasing) “we are focusing on the junior employees and work culture, senior managers are not allowed to fire people for not meeting performance goals or use abusive language. Managers are expected to hand hold employees and if needed give them two days of hands on training so they can improve”.

Marcellus had put out a stat that because of the short tenure of hdfc bank loans, 40% runoff ever year so to grow at 20% they need to disburse 60% more loans. The home loans will help the bank breathe and i think there will be a huge change in employee behaviour over time

I was going through the screener data. and saw that bank has consistently performed very well. Profit growth has been phenomenal , considering the size of the bank.

Profit growth 10 yr CAGR =22%, 5yr CAGR = 20%,

3 yr CAGR=19%, TTM =20%

but stock price performance has been consistently going down

Stock Price 10 yr CAGR= 19%, 5 yr CAGR= 11 % ,

3 yr CAGR = 5 %, 1Yr CAGR = -8%

Last 5 yrs or more it has not been at par even with Nifty Index performance. So my question is, are the good old days of HDFC Bank over ? Or at best we can expect bare minimum Index performance in coming decade? Will it be a Mercedes without growth engine going forward…where one can feel that they are riding a Merc, but its actually going no-where? Kindly guide.

some nice performance figures that you stated and the point of no growth actually have been proven by your post only around 19% cagr in profit don’t like growth is slowing.

The main reason for the stock not performing is only for a key reason that is not to do with its own growth or fundamentals but the whole picture what investors want to see.

Firstly the premium that hdfc enjoy of been a bank that perform good over time if you look at most other like axis or even icici there are some blowup in the past that made hdfc trade at a better valuation as for most investors if you want to invest in banking then hdfc is the best choice and the most consistent second is Kotak but is it still the case the icici, axis,au of the world are they catching up to the loan quality and the PSU like sbi and and have learned their lesson so can perform better.

The problem can be that now investor are more risk-friendly and also see equivalent options with much better valuation this is the question as a shareholder you should do is still hdfc is a better more mature and stable bank than others and will you pay a premium for that if yes then you can see a pe or pb increase over time and will make you earn better returns over-time if the answer is no then it would be very hard for hdfc to even get index level return in next 3-5 years as the downward pe rerating will hurt the better growth.

I personally think hdfc management is still better then most banks and should trade at a premium so new pe will not come and will gain better over time.

So as a rational investor if we see both the cases and assume around 18-20% cagr profit growth in hdfc what will be the future returns.

hdfc is still the better pick:-

future pe ratio is around 25 current is 20 so we see that eps will jump from 68 to around 172 if eps grow by around 20% cagr so the stock will return around 28%-30% cagr growth

hdfc will get a downgrade

future pe would be around 16 from the current 20 the we see a rate of return of around 16-18% cagr.

if we account for any slow-down in the economy then we will also deduct around 2-3% from this either we will miss the index by 1-2% or will beat by 3-4%.

Here i think it is the opposite, there are a lot of uncertainties around HDFC, timeline of merger, cost of SLR, PSL, integration and the overhand of MSCI selling so a lot of institutional investors are switching to ICICI.

Doubtful, on a post merger basis HDFC is ~18PE. That is a 5.5% earnings yield with a growth of 13-15%. I don’t see it falling much more especially once the merger is out of the way

Possible but 13-15% is much more likely given the size of the balance sheet

Over the long term index should give nominal GDP (gdp + inflation) + 1/2%

Currently hdfc long term growth is also nominal GDP + 1/2%

Only difference is index is slightly on the expensive side with bajaj(with low cost borrowing and low competition behind), asian paints ( with benign oil prices behind), reliance (at peak refining margins), titan, HUL, etc while hdfc is on the the cheaper side with the capex and housing cycle ahead

This will eventually have to normalize which could add 1/2% alpha

But honestly the entire large banking sector is looking cheap so for anyone on the fence and unsure about hdfc or icici or axis or whatever, even just buying the banking index will generate alpha

I personally will not judge the future pe of the merged entity to be the same as past hdfc bank so still in bear case the pe shrink can still get into the picture in my opinion.

Will a large balance sheet will hurt its growth look not that much as it is not like hdfc is growing at around 15-16% in sales that is very close to hdfc bank growth and with added jump in margins it could also have better eps growth rate in short term in my opinion

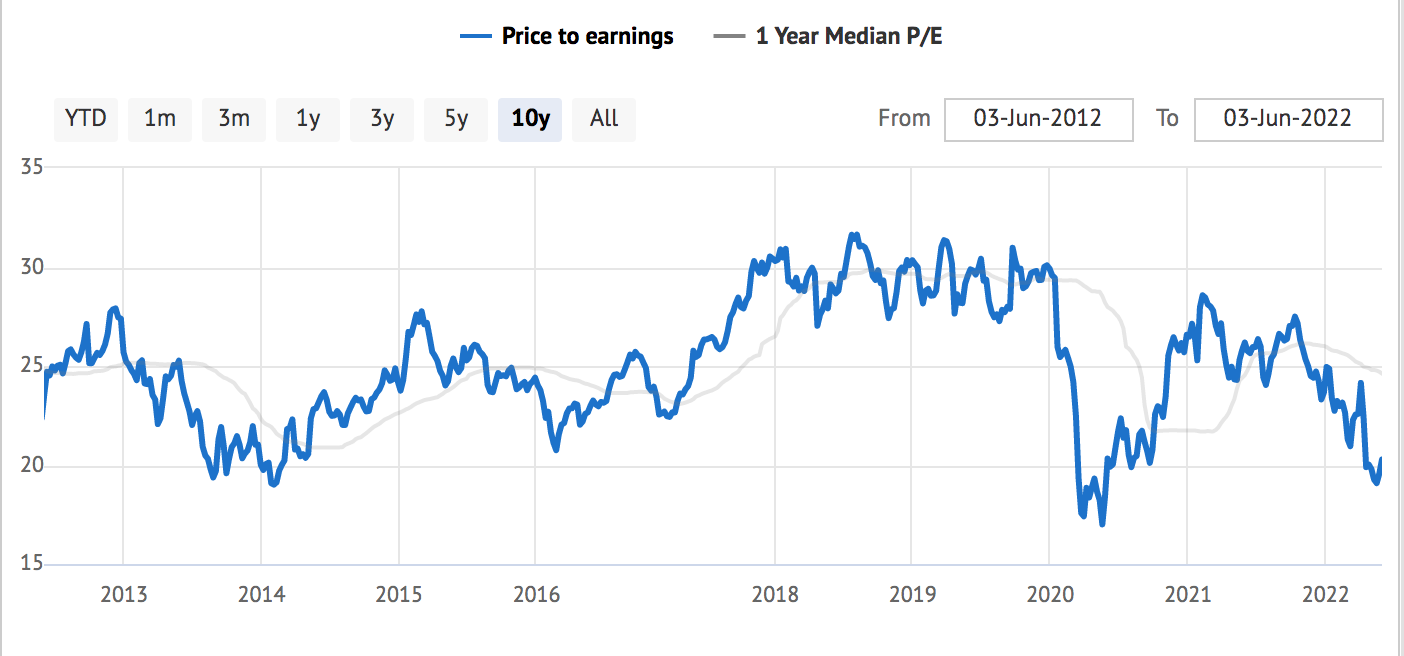

Agreed but the historical range is 25-30. At 18 PE post merger it is very unlikely to go down further. And if it does, then the entire banking sector has to get derated as well.

If a bank this good goes to 10 or 15 PE, why would anyone buy an axis or an AU or ICICI at double and triple the valuation.

I dont think it will purely be because of the merge but because of the massive size of just HDFC bank. To grown on that base at 20% while maintaining asset quality would be close to impossible.

That is probably why the management is guiding to double every 5 years, ie 14.5%. They will probably grow slightly faster but eventually they have to slow down, not significantly but closer to 15% then 20%