Because an AMC business is different from a wealth management business. IIFL Wealth does have an AMC component but it is primarily a wealth management player. HDFC AMC and Nippon Life AMC are pure play asset management companies. The differences have been covered in detail on this thread, happy reading

Let’s arrive at the answer from basic unit economics and first principles…

ROE = Profit After Tax/Net Worth of the Company

Assume that an asset management company and wealth management company are both created on the same day with equity capital of 100 Cr and both have the same AUM of 1,00,000 Cr

For the asset management company the yield to AUM is say 0.55% which means the revenue will be 550 Cr. For the wealth management company assume the yield to AUA is 0.7% which means the revenue will be 700 Cr

Now look at profitability of an AMC vs wealth management company from what you observe practically. HDFC AMC is working at a PAT margin of 55% while IIFL Wealth is working at a PAT margin of 25%. These are actual FY20 ballpark numbers. So if you calculate the ROE, you can see why asset management is way more than wealth management for the same scale of business.

The more pertinent question is - why is AMC doing much higher profitability than the wealth management company? Both are not capital intensive but the unit economics for an AMC are way more superior beyond a threshold scale.

ROE is the final culmination of business economics, it should never be seen as the starting data point by itself for any kind of analysis

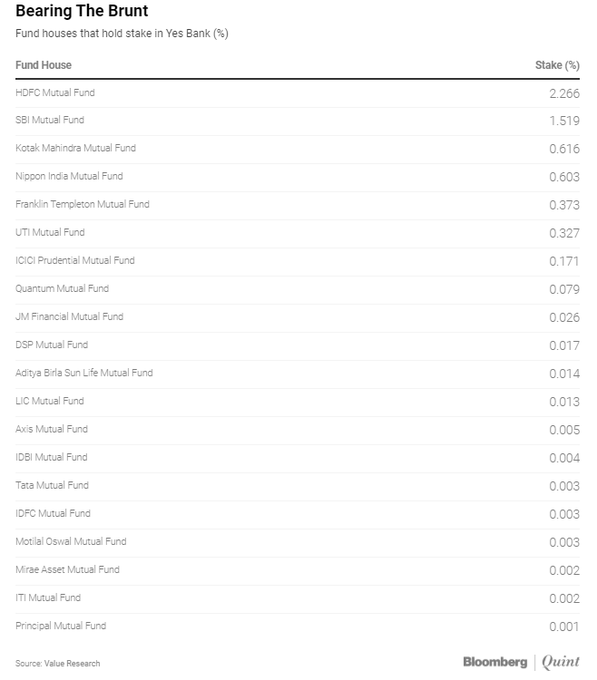

HDFC MF (Balanced Advantage Scheme) had invested 23.70 lakhs shares in Yes Bank QIP in August 2019 at a price of Rs. 83.55 (Rs. 2.00 FV + Rs. 81.55 Premium).

From my personal experience, never ever bet on parent for the liking of its child. If you like SBI AMC, wait for it to list seperately or don’t buy anything else. Never buy SBI because of SBI AMC. The revenues/profits/risks of SBI is humungous as compared to its AMC which is insignificant to it. Moreover, if at all sbi lists it’s AMC, it will definitely be an IPO rather than a demerger as that will give the parent access to the money that banks always are hungry for.

This is not a buy sell advice. Only fundamental suggestion from my own experience. Thanks

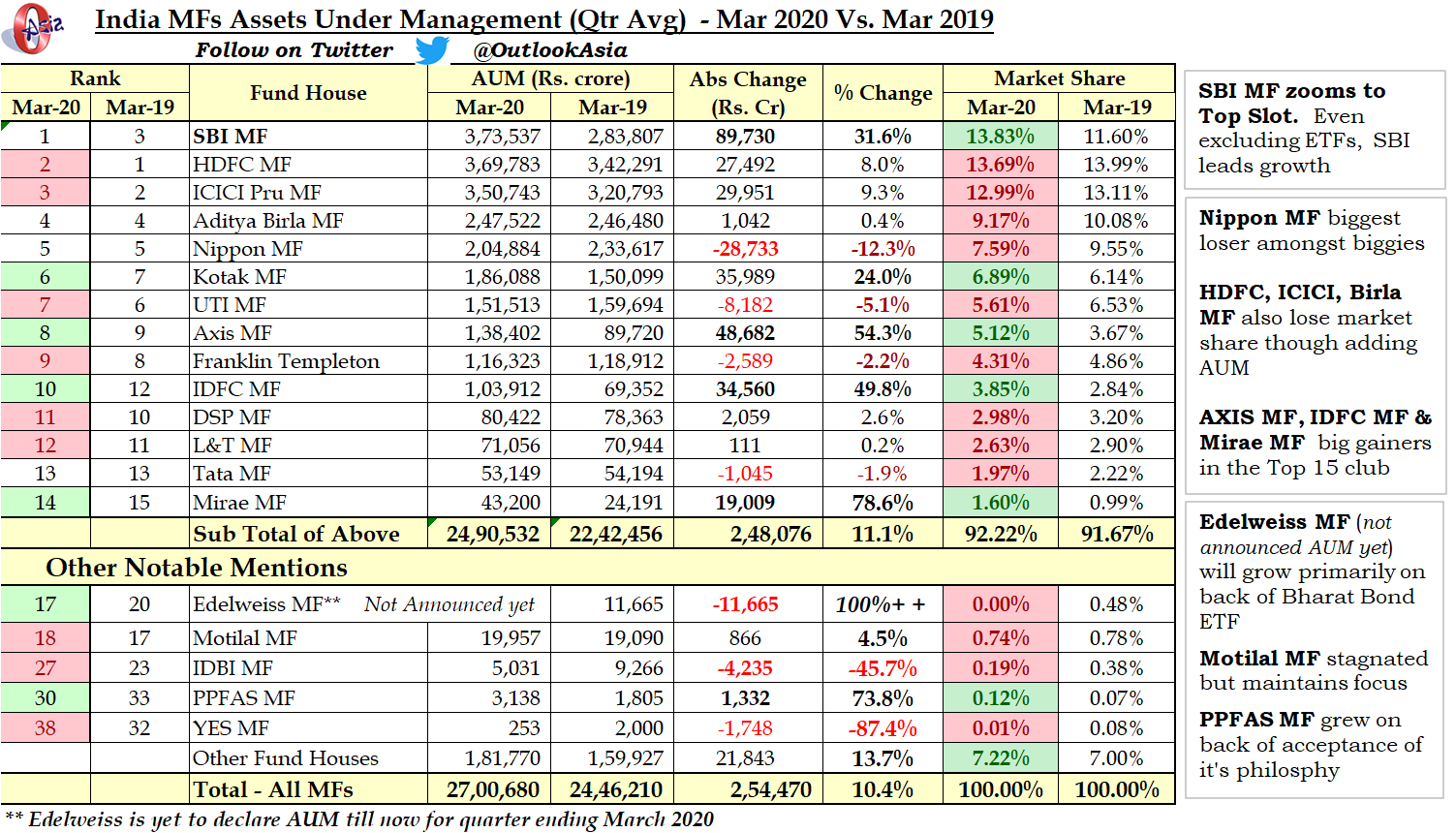

This data needs further digging. I would be keen to see a breakdown of government/institutions/retail inflow for all of these Asset Management companies. Unfortunately AMFI website doesn’t have the March data yet. It might be EPFO money that is playing out. One can see the real market share changes after excluding government/EPFO inflows.

As new structures evolve which are more cost efficient, in addition to regulatory expense cuts, the traditional product earnings will probably continue to be gradually impacted.

AUM is key the revenue source for HDFC AMC.

Compared AUM disclosures made by company across historic time periods, I focussed on equity , hybrid (in past balance) & ELSS AUM as expense ratio is highest in these categories and this represents 40-45% of total AUM. ( Avoided going into minute calculations to save time)

Key observations on equity AUM :

In past AUM on last day qtr > Avg. AUM for the qtr, this is exactly reverse for latest qtr.

AUM last day becomes base for next qtr hence this very much important growth indicator

Now monthly AUM is less than Dec-2018.

Also compare the stock price at those AUMs in past, current valuation could be highest and uncertainty is also highest!

March SIP Equity flow have been robust - stress test for AMC - passed in flying colors as of now

AMC have TER to play as levers as needed( within range though). Also avg AUM for qtr will work for comm calculations- AFAIK.

HDFC has demonstrated its pricing power in past over distributors ( commissions etc)

PMS limits raised to 50L, some spillover towards SIP likely.

One of very few high ROCE and asset light company performing well , with super long runway

Bounced back well in recent come back( supports some studies in VP that strongest bounce back first and deliver better CAGR when mkt recovers - though might see downfall again in tandem with mkt.

Contrary - ppl saving more with lockdown and near future post lockdown may eventually find ways into SIP

Outside typical quality basket this one seem to be holding well and valuations ( with growth runway and RoCE etc) seems reasonable.

Largest portfolio holding - would add more on dips as long as SIP flows( financialization theme) runs well.

Stock prices have fallen a lot in the month of March, which is one of the reasons for fall in equity AUM. In April, so far, prices have risen a lot from the March lows. Just few days left in April, so equity AUM for April can be much higher than that of March (assuming no big fall in the next few days). Also liquid funds inflow / outflow is always volatile. We need to see the April month AUM