Interesting the way Articles are titled.

Aug and Sept 19 also had 66% closure rates. Avg has been around 55%.

March new registration would have impacted with lockdown hence number might be looking elevated in co-relation.

March SIP flow was healthy, let’s see how April spans out.

With the reform in income tax structure and the possibility of section 80C investments reducing in importance for a section of tax payers, will insurance as an investment vehicle see an increase or decrease in the pecking order? Will that be beneficial or detrimental to MF industry prospects over the next 4-5 years?

With residential real estate expected to go into further troubled waters, will the shift from physical savings towards financial savings pick up pace? Gold will be an obvious beneficiary if the move away from investment demand for real estate picks up pace, how much can the mutual fund industry benefit from this?

Has the current market correction actually impacted the investor view on MF and SIP over the medium/long term? Is there anything in the data that points to slowing momentum yet?

The key is to quantify the impact rather than just hypothesizing if the situation can materialize.

Job losses and salary cuts are a reality now. This is well evident in the SIP Closure Ratio of 70% in the month of March which can worsen further going into April. This is the data of the performance of top five schemes of HDFC AMC on 12 March 2020 accounting for 80% of their AUM. None of their schemes have beaten the benchmark performance as seen below:

Particulars (in cr)

Performance of Fund in Past 3 Years

Benchmark Performance of Past 3 Years

Average Perofrmance of Funds in Similar Category in Past Three Years

Performance of Fund in Past 5 Yrs

Benchmark Performance of Past 5 Years

Average Perofrmance of Funds in Similar Category

HDFC Top 100

-5.0

-1.7

-1.5

0.1

1.5

1.2

HDFC Mid-Cap Opportunities

-7.8

-6.4

-6.2

1.2

1.9

0.8

HDFC Balance Advantage

-4.0

0.6

0.5

1.5

2.6

2.9

HDFC Hybrid Equity Fund

-2.4

0.6

0.5

2.5

2.6

2.9

HDFC Tax Saver Fund

-8.8

-3.0

-3.8

-2.2

1.4

0.9

HDFC Equity Funds

-5.57

-2.98

-3.25

-0.52

1.41

1.09

If performance is some indicator for IFAs/National Distributors to distribute their schemes, then shoudn’t HDFC AMC be losing market share in the equity segment?

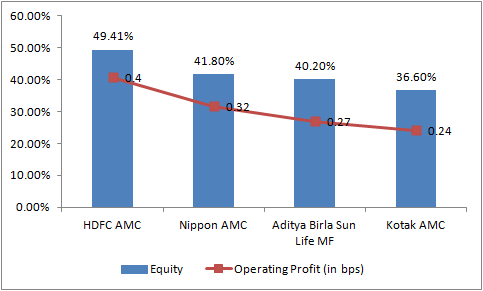

HDFC AMC profitability is best in the industry because of the fact that they have the highest proportion of equity component wherein yields are much higher as compared to debt and equity.

Equity as a Proportion of Overall AUM and Operating Margins

Can the equity component and margins reduce on the basis of the performance of their schemes?

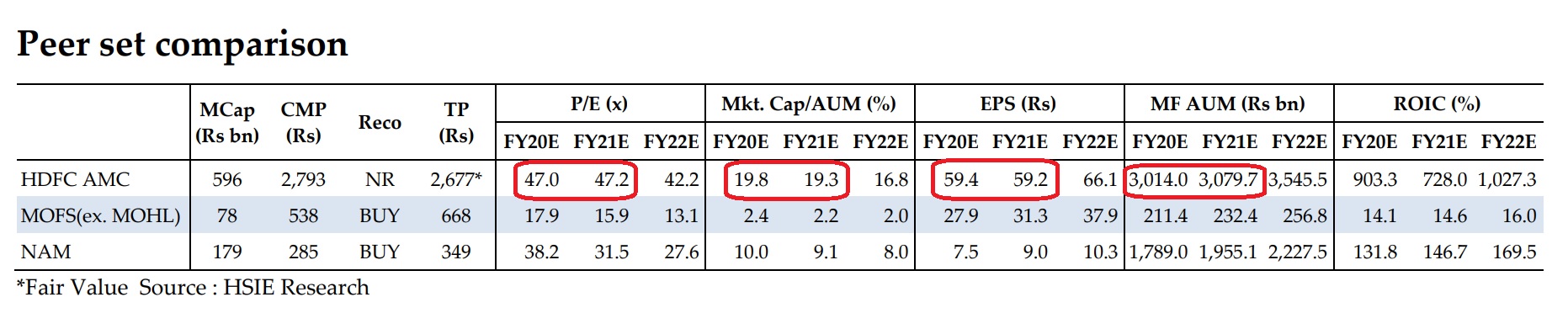

And given the scenario we are in wherein household savings can take a hit, does it makes sense for the stock to command a MarketCap to AUM ratio of around 16%? Globally, the M&A deals have taken place somewhere around 5-7% Market Cap to AUM ratio. What is the valuation one should give while acquiring this business given that there are uncertainties pertaining to the AUM growth for FY21…

This is absolutely great business to own given the following reasons:

a. Shift in household savings from physical assets (i.e real estate) to financial assets.

b. Within financial assets, there is a shift from fixed deposits to better tax savvy products such as PPF, Shares and MF

c. Growing acceptability of equity/MF as an asset class in the Bottom 30 cities wherein penetration is still low.

d. Highest proportion of equity component in the overall AUM amidst the top eight-ten players leading to better profitability.

e. AMC having the largest Market Share of Individual AUM. As, business for individuals is a bit sticky in nature, revenues & AUM is more sustainable.

f. Operating leverage is pretty high as large part of the cost line is fixed in nature. Main costs are rent, salary costs and travelling expenses. Further, business is scalable without incuring capital expenditure and hence business generates huge cash flows.

g. Can expect stable dividends for the company year after year.

Having said that, the only confusion I have is the value at which this business can be bought. Appreciate the view of the house.

Till now there was ample liquidity available with the mutual fund investors. Hence, distributors were able to push HDFC MF schemes. Despite this, you would see that for last year, the AMCs such as Mirae Asset, Kotak, Axis and SBI, were gaining at the expense of HDFC. With liquidity drying up, we should see even more divergence in the fund flow to HDFC AMC.

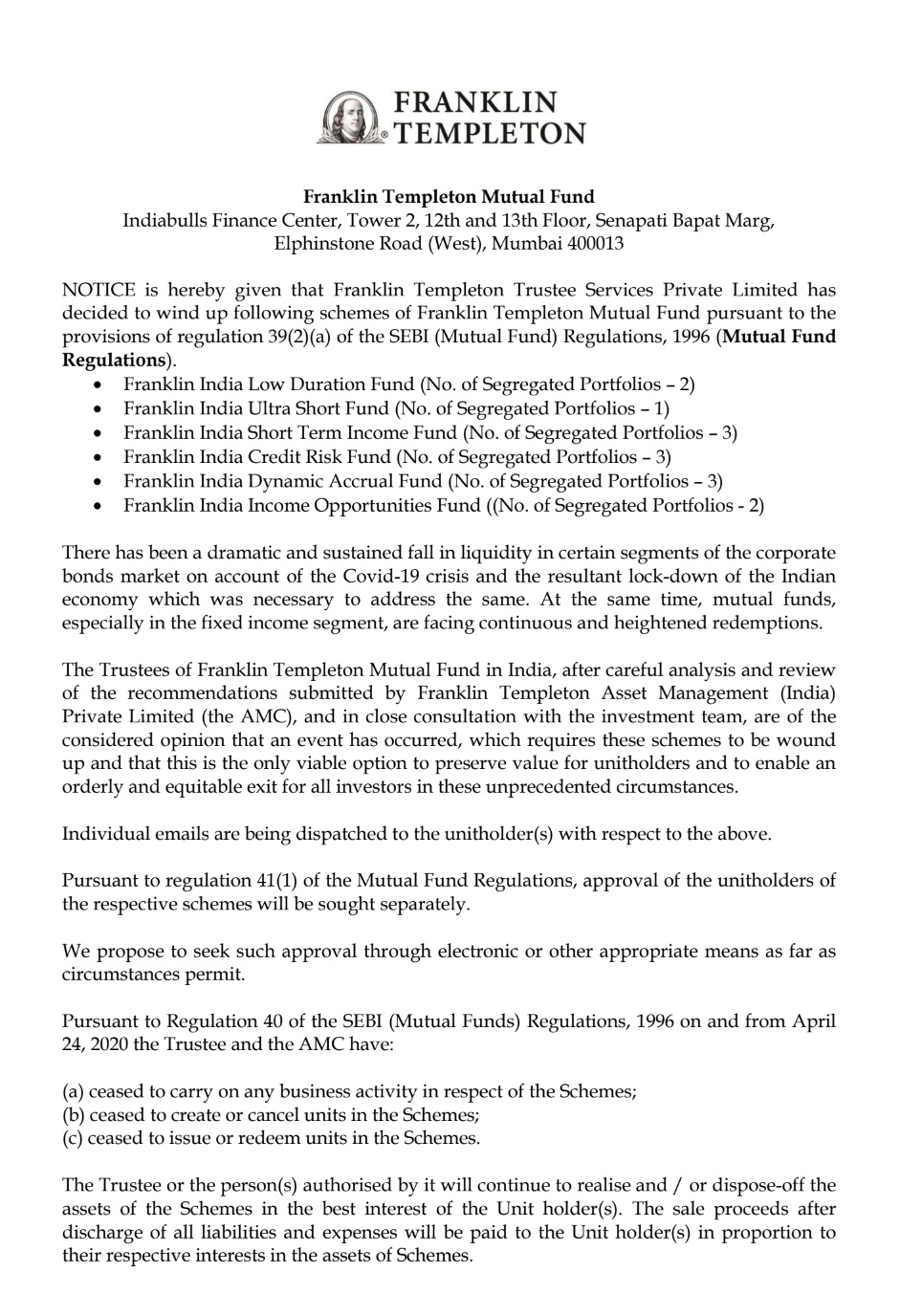

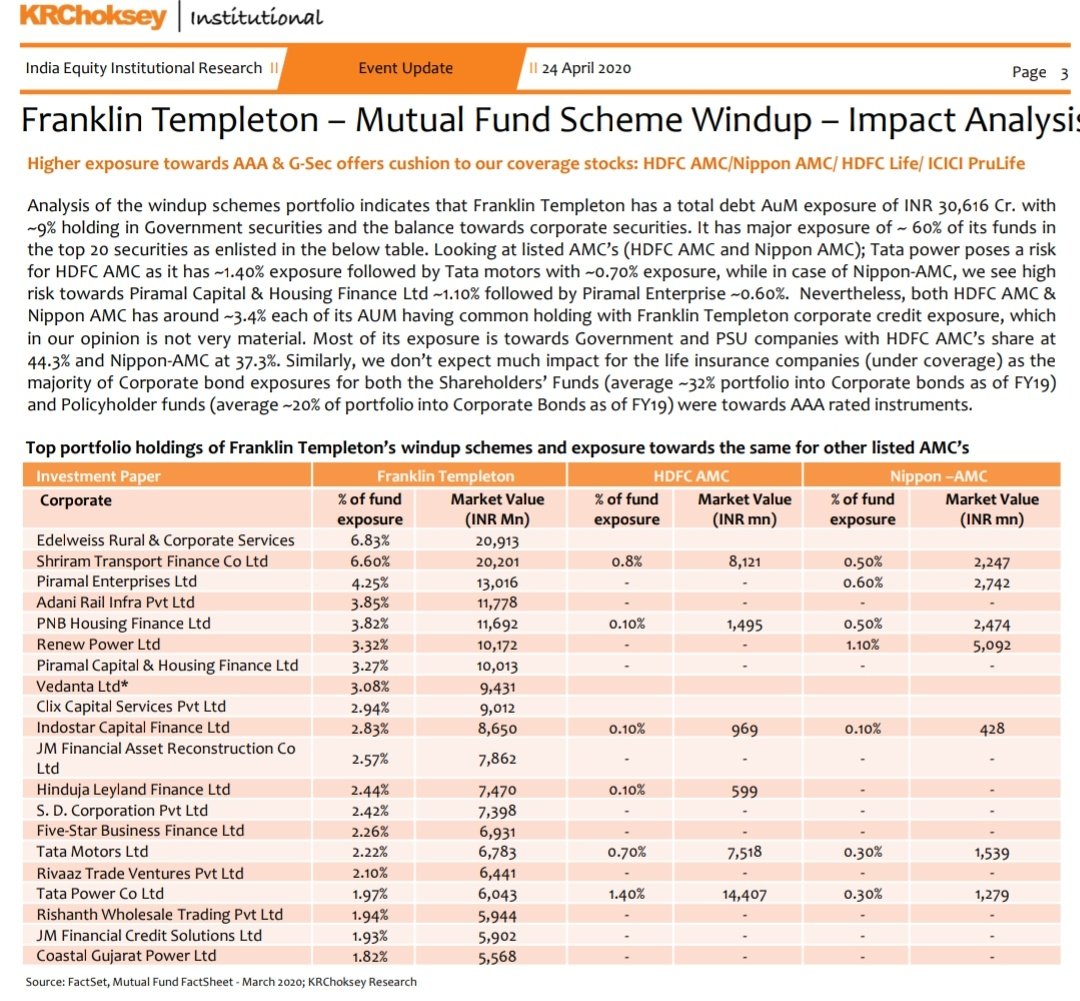

If there are defaults from corporate over next year, we should see lot of bad news on the debt portfolios of these funds. See performance of Franklin funds.

For last 7-8 years, the equity returns have been only seen upside, evident from consistent EPS growth. People don’t realize that it is a cyclical industry. So, not sure for how long this stock can command FMCG kind of multiples.

Seniors on this forum should help us in identifying the right valuation multiples and the right value for this stock.

AMC is not cyclical. It will be impacted like all businesses and that’s normal …but its dynamics and model is rather anti-cyclical…the behaviour of its unmatured customers tend to make it or rather look like cyclical.

Financial services comes under cyclical super sector in morningstar classification.

AMC will have 2 cycles according to its risk factors mentioned above.

Market risk - its AUM will increase in bull market and decrease in bear market. No need to blame maturity of customers as they will have higher employment in good times and invest more and poor employment at bad times and withdraw more.

Alpha risk - money will move from one AMC to other depending on their recent performance. Here you can blame the customer for being greedy and immature.

This is so arbitrary given that there is no real credit event. Especially considering that some products are sold to people with higher age saying balance between debt and equity basis age. We are not even sure about any collateral damage yet. Shakes confidence in the entire financial system and potentially threatens financial stability. Hopefully SEBI/RBI will step in.

HDFC AMC suffering from both market risk and alpha risk

Most of their top funds (specially Prashant jain managed) are worst performers in their category in this carnage. Irony is so called famous value type fund manager was avoiding all expensive stocks and was expected to outperform during big crash.Just check out some of his stocks and u will understand .

Eg max allocation to financials/ energy/ construction /metals & PSUs.

Was great fan of HDFC brand but sold out after individually checking all their top funds stocks.

disclosure: Not invested

People are taking funds out from Debt funds left and right and returns will start turning negative for these funds, and corporates would be taking funds out now too. If the debt fund market gets severely impacted, and equity funds are anyways not performing, what does it mean for an AMC business in the near future?

I wish the Indian investors are as knowledgable and informed like the folks out here

Irrespective of whether Prashant Jain buys wealth destroying PSUs or quality companies, I think 90% of mutual fund investors do not understand this.It is the reach, supply chain and distributor channels of the fund houses that enables them to sell whatever. At the end of the day, it is INCENTIVE BIAS.

Lets take for example the latest Franklin Debt funds saga.

Out of Rs 36000 AUM under those 6 Franklin Schemes, Rs 27000 crore funds were regular plans while remaining 9000 crores was thru direct plans.So, almost 75% through distributors.

Why would the distributors care as long as they are getting incentivised fully

One more example, in January I went to my HDFC Bank branch. One of the officer started selling me tax saving mutual fund(of course HDFC tax saver). I asked her what she has bought- direct or regular? she was clueless!!! I was also in the same boat in my early years in 2010.I had a SIP in reliance MF; During 2010,SEBI abolished entry load on mutual funds, still reliance kept on charging me for the next 2 years. When I woke up and realised the anomaly, they told me that I did not fill up form, so it was running like no change In the process, I drained more than 5% on every SIP(2.5% entry load and around 2.5 regular plan charges since I bought through some agent).

Even while the direct plans have been in existence for the last 8 years, such is the plight and ignorance of Indian investors, who would want to bargain with Sabjiwala to save Rs 20, or waste more than 2 hours browsing thru multiple flight booking platforms to save that Rs 400; but would not care to enhance their knowledge and prevent the huge money drain subscribing to regular plans.

I agree in long term HDFC AMC will do well , just that their are some near headwinds against the business on top of that your funds not performing and even people are scared about debt funds after Franklin episode. And to pay these valuations for all those headwinds when opportunities in market are plenty.

And to counter my own earlier argument even after all these complains we keep hearing about HDFC bank overcharging customers HDFC Bank continue to do exceptionally well.

Disclosure: Have HDFC Bank in portfolio plus HDFC Ltd but no HDFC AMC direct holding.

HDFC AMC equity funds have been under performing since 2012, I do not see how this trend can drastically reverse in the near future. This is something one needs to factor into the investment and valuation thesis. An AMC business gets impacted in a market correction since you cannot separate the business of asset management from capital market performance, this is an investment which is likely to show higher crests and troughs during volatile capital market cycles.

At the same time, one needs to also see if the market position is getting weaker or stronger for the AMC in question. After this FT incident, where are investors likely to invest incremental funds? With safe bank banked AMC’s like HDFC AMC, ICICI Pru AMC, SBI AMC, Kotak AMC, Axis AMC or are they likely to invest with smaller AMC’s which may show better relative performance? An FT like situation would might have been handled differently by any of these bank backed AMC’s

Other factors to be considered especially in the current environment -

Operational business of an AMC can continue in the digital mode, this is one of the industries to be least impacted due to lockdown in that sense

Assume that net sales for FY21 is zero, will the AMC revenue drop significantly? The calculation is very simple - multiply your estimate of AUM by the yield to AUM. Will the revenue (for any AMC) drop drastically if the net AUM growth for FY21 is flat?

Which of the operating expense components can grow if revenue does not grow? What proportion of the expenses is discretionary for an AMC?

What is the extent of balance sheet risk in an AMC business? This is a business where you neither have fixed asset investments nor working capital investments (inventory, AR).

What further compounds the valuation problem for this particular business is the fact that we do not have enough history to see what the median P/E has been. One has to do his own independent thinking to have a view on what valuation multiple is justified for this business.

Thanks @zygo23554 for pointing strength of AMC business specially below 2 points

Operational business of an AMC can continue in the digital mode, this is one of the industries to be least impacted due to lockdown in that sense*

Assume that net sales for FY21 is zero, will the AMC revenue drop significantly? The calculation is very simple - multiply your estimate of AUM by the yield to AUM. Will the revenue (for any AMC) drop drastically if the net AUM growth for FY21 is flat?*

I have no doubt about strength of AMC business but was finding Non Performing equity+Debt segment general fear+ relative High valuations combination difficult for me personally. Might take position in Nippon as they could have some predictable surprise + Valuation comfort.

Below is KR Choksey report on Franklin impact analysis on listed AMC

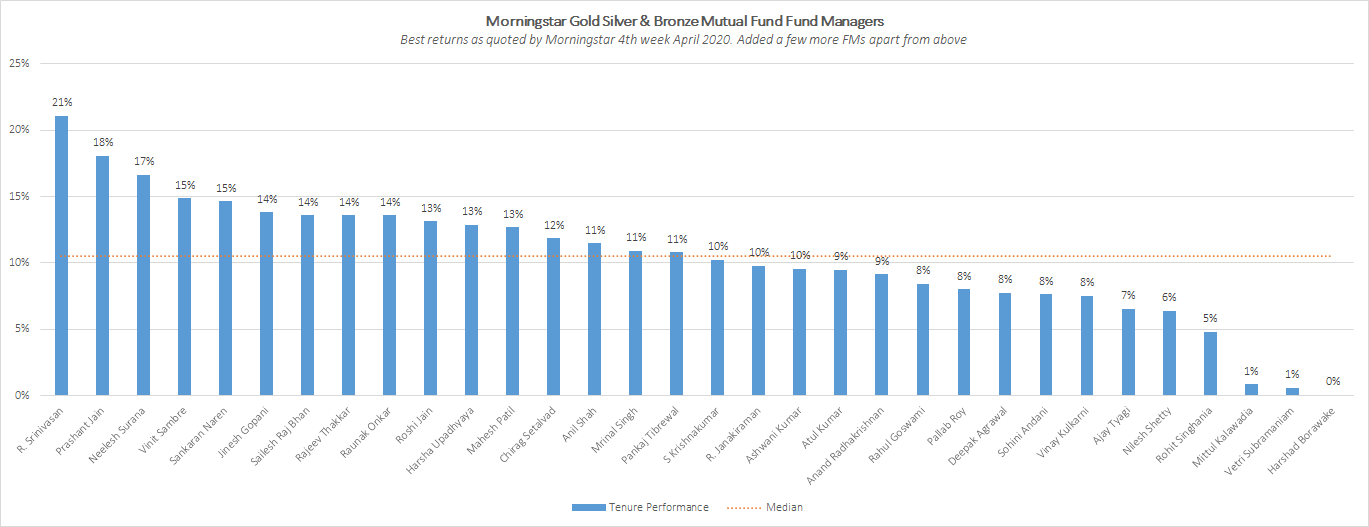

Data Source: Morningstar India has Gold, Silver and Bronze rated funds. For each fund (I looked at only equity funds) they have the respective fund managers, their returns, aum, investment career etc. I added PPFAS & Quantum to the list to these funds. I have removed all FMs who had negative returns. And considered only the best returns (tenure returns is what morningstar gives) of every fund manager. Below is the snapshot.

Having said that I echo what @abhijain has said. Very true on ground.

For the moment I am not very concerned with what alpha each AMC generates. We on VP might think so that this factor is important but the common man perhaps doesn’t think so.