On comparable base…next two ICICI and SBI growth for same period is much much higher…with same velocity they may surpass.

Wondering what SBI has done well which HDFC couldn’t ( or chose not to). Would be good to understand segment growth equity/ liquid…as long as equity pie growth rate is leading by HDFC…likely to show better operating performance.

I used both sbimf investap and HDFC MF online apps for buying funds on android mobile. I felt SBI app is well designed and visually appealing than hdfc app.SBI mf team appears serious with frequent app updates with features such as fund recommendations , login by fingerprint etc.

No surprises.

HDFC AMC, ICICI Pru AMC, SBI AMC, and Kotak AMC growing because of strong branch and distribution network.

SBI AMC also benefited by ETF for EPF.

Nippon (Reliance) lost market share because of ADAG label Should bounce back next year.

Axis, IDFC and Mirae gained market share purely on superior performance. Their equity schemes performed better than those of market leaders - HDFC AMC, ICICI Pru AMC, SBI AMC.

Mahindra MF and PPFAS rose on small existing AUM base.

UTI has been losing for several years now as its four domestic shareholders — LIC, State Bank of India (SBI), Punjab National Bank (PNB) and Bank of Baroda (BoB) — who hold 18.5 per cent stake each also have their own AMCs.

PGIM (Earlier DHFL Pramerica) and JM lost market share because of un-certainty faced by their parent NBFC

Motilal Oswal and Invesco’s performance not listed.

Spot On! But you missed L&T! ![]() Whats your thought on it?

Whats your thought on it?

L&T had once intended to sell their MF business few years back but now seem to be holding it. Do they have focus and intention to grow hat business?

Any intention to sell by the AMC Board /Promoters will have adverse impact. Both Mutual Fund distributors and investors will shun such AMC. Hence L&T AMC nowhere in picture.

Also several AMCs affected because of their parentage : Edelweiss Mutual Fund, IIFL Mutual Fund, JM Financial Mutual Fund, Essel Mutual Fund, Shriram Mutual Fund and Indiabulls Mutual Fund.

Also more surprising is failure of BOI AXA Mutual Fund, Canara Robeco Mutual Fund, Baroda Mutual Fund, Union Mutual Fund and LIC Mutual Fund to capture any meaningful market share despite strong parentage, many years of existence, large branch network and their reach in B30 cities.

Ultimately, a mutual fund investor makes a smarter choice.

SIP book stands at Rs 8518 crore, up Rs 245 crore (MoM)

financial deepening continue

Thanks

HDFC AMC Q3FY20 Concall Summary

Business Update

- AUM of industry as on 31st Dec stood at Rs 26.5 trillion as against Rs 22.9 trillion yoy

- The SIP book for Dec 2019 stood at Rs 85 billion

- Market share remained flat at 14.3%

- Continue to maintain market leader position in actively managed equity funds

- Market share of 15.5% in individual investors in equity which is highest in industry

- During the quarter gone by all 7 branches were added in B30 locations

Participants

- Deutsche Bank

- HDFC Securities

- Nirmal Bang

- Motilal Oswal

- Sundaram Asset Management

- Kotak Securities

- Nomura Securities

- Morgan Stanley

- Philip Capital

- Yes Bank

QnA

- Since AS116 has kicked in have been accounting for leases is included in depreciation instead of being booked as rent

- Even today Indian investors are considerably underallocated to equity as an asset class so expecting flows to remain constant in the longer term

- The ETF AUM is considerably due to EPFO money and divestments of PSE’s through Bharat 22 and CPSE ETF. Apart from these three sources the money in ETF market is very minimal

- The quantitative approach to fund management has yet not picked up in the Indian space and the company is not yet using any algorithm based approach to fund management

- The bank deposit growth in last 5-6 years has been around 9-10% while growth in mutual fund AUM has been around 20% . This has been driven by retail investors

- Not looking at any specific acquisition target at the moment but will look at if there will be future synergies in any acquisition going forward

- Distributors are not moving away from HDFC products and marketing team on ground is working to maintain relationships

- The dividend payout ratio will continue to remain high

- The EPFO allocation of ETF money has a mandate of being given to publicly enterprises and not coming to private enterprises

- Will continue to work on growing international business and it currently stands at $1.8 billion and it is money from sovereign funds and pension funds

- The fees from international funds are very different in nature with every different transaction

- The redemption rate for the company is meaningfully lower than the industry redemption rate

- The opportunity to grow in B30 cities is very high and almost 65% of the branches of the company are in the B30 cities and towns

- The distribution strength and the brand value of the company are very high in B30 cities and towns. The market share is only behind SBI Mutual Funds

- The contribution from banking channel for sales from an industry perspective has dipped

- More and more individual investors have started investing directly

- Almost 18% of the gross flows of the industry is now coming from direct route but for the company this is as high as 23% for equity oriented AUM’s

- Margins in equity funds are around 80-90 bps while margin in debt funds are around 30 bps while in liquid funds they are around 7-8 bps

- The relationship with NJ continues to be robust and new products from their shelf will not be conflicting with products from HDFC stable of funds

- Have been investing heavily in technology and working on expanding the digital footprint by creating applications and processes to benefit customers in on boarding and making their experience seamless

Can you explain the impact of point no 1 in Q &S?

I tried to understand but could not make out much from concalls.can you list out positives/negatives fm it?

The expense line item has moved from rent to depreciation. The overall expenditure remains the same just that rent is now being shown as depreciation due to lease accounting. However cash flows from operations will increase by that amount shown under depreciation as depreciation is added back to calculate operating cash flow

Worth noticing, the expense is decreasing.

Margin are around 80%, as revenue keep or increasing and expenses are flat (or decreasing or marginally increasing) will lead to margin increase to 90-95% in next couple of years.

A pure cash generating machine.

No doubt valuation is quiet rich.

True, I wonder how HDFC Life is having a valuation of 92 PE whereas HDFC AMC is having valuation of 52.

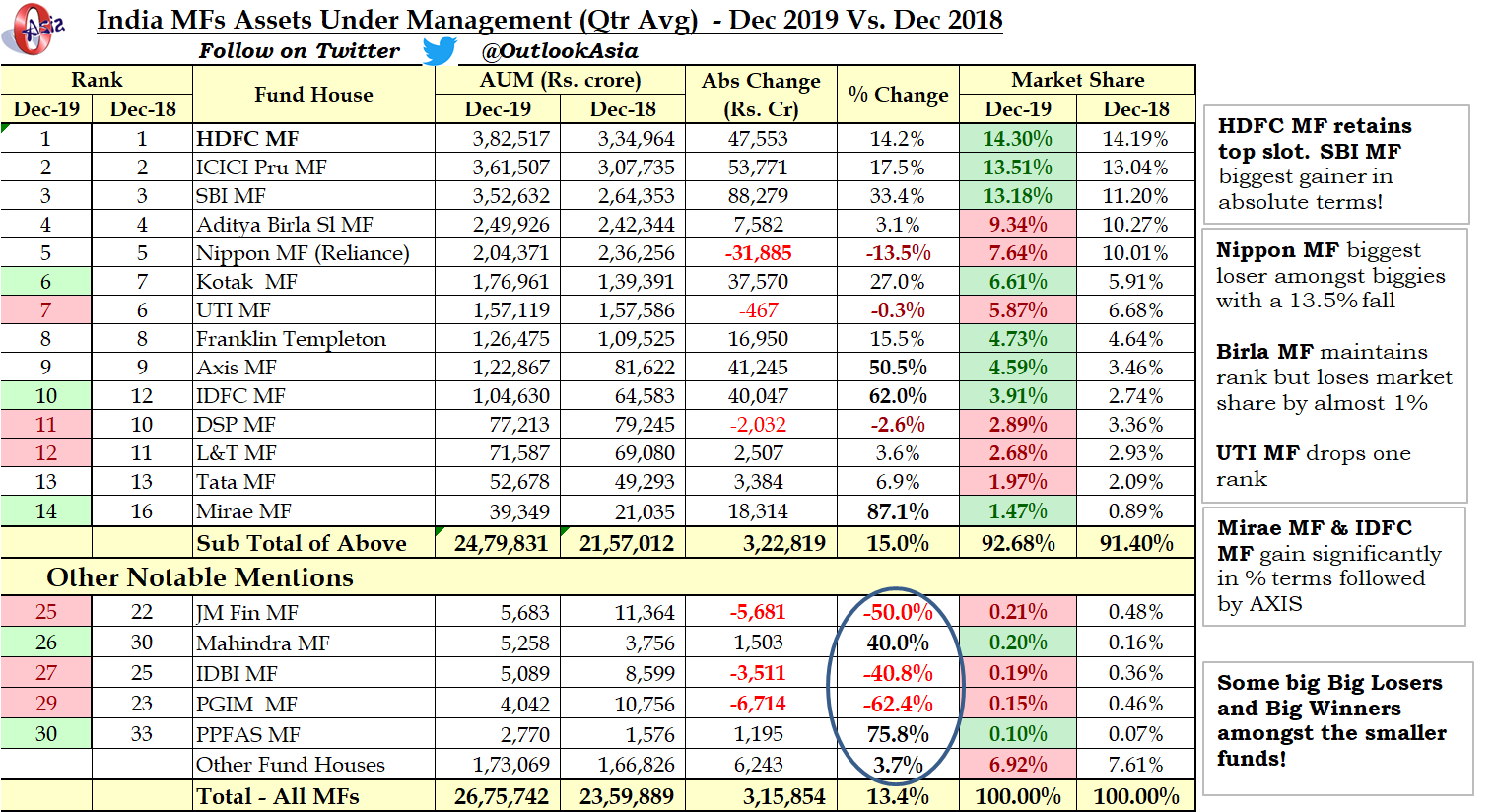

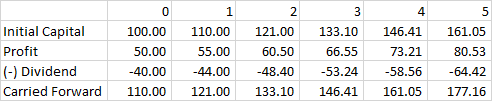

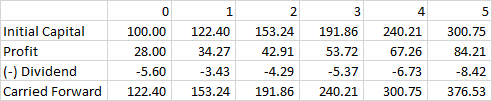

ROCE 29% vs 52%

Margin 3% vs 77%

I felt that risk is lower in AMC business than Life insurance as well (for unfortunate events then payout is required)

AMC only has a fund manager and advertising fees, maybe some fees to distributors for promotion.

In cases where fund manager is replaced by AI (thinking too much), costs can even reduce or sometimes increase.

Advantage is that HDFC AMC is the leader. Thats all. But that might be enough -> customer’s trust when compared to other AMC’s.

I don’t think valuation matrix like trailing PE fairly value Life Insurance companies… All the insurance players have said that they make money starting from the 3rd year of policy, that’s why consistency ratios are very important. If consistency ratios are higher like 85%+, you may think that the current profit is based on sale of 1.5 years back on average… so in case they stop the growth engine, still eps would still grow. So, this is kind of hidden profits in the books.

ROCE is great for AMC business, but they do not need capital.

See if I earn high rate on capital without being able to reinvest in the company at same rate, the compounding effects can not be achieved… However, in case of finance companies like banks, nbfcs where capital is always needed to expand, higher ROCE is always better due to compounding.

e.g. 50% ROCE with 80% dividend payout

vs a company with 28% ROCE and 20% dividend payout

The assumption is that they are able to invest incremental capital at same ROCE…

This is even true in case of ROCE improvement (which will take care of improving OPEX ratios).

Regarding the risk part, we have seen there can be some risk in AMC business also (eg. Essel group bonds). Insurance is not that risky… Most risks are mitigated through geographical distribution and reinsurance. Again, the management should not be growth hungry… underwritten assets must have requisite value.

Disc: Invested in both HDFC AMC, HDFC Life.

Assets managed by the Indian mutual fund industry have grown from ₹24.09 trillion in December 2018 to ₹27.26 trillion in December 2019, representing a 13.18% growth in assets over December 2018. The proportionate share of equity-oriented schemes is now 42.3% of the industry assets in December 2019, up from 41.9% in December 2018. Individual investors primarily hold equity-oriented schemes while institutions hold liquid and debt oriented schemes. 69% of individual investor assets are held in equity oriented schemes, said Amfi.

Here are my 2 cents.

HDFC life is trading over higher PE than HDFC AMC, because of following reason. (assuming we don’t compare the industry)

-

In AMC, Income for company is expense ratio charged from customer. Investor have fear that these expense ratio will be reduced/decreased (by regulators ) in future. Investors in developed countries are moving towards passive investment like ETF, where expense ratio is too low. Whereas in Life insurance, the entire premium they don’t need to return to customer if its not claimed. Means profitability increase if underwriting is done properly. And life insurers are using advance technology to underwrite properly. HDFC life has maintaining old data of customers where risk can also be identified. So risky business can be avoided. In short, using technology claims in future can be reduced.

-

Life insurance also earn from investment as they have huge sum of money received as premium, which is absent in AMC.

-

AMC business has a lot of free cash flow and for same reason they are returning the cash to shareholders in form of dividend. HDFC AMC has dividend payout of 55%, means 55% of profit they are returning back, as they actually don’t need any cash to deploy. While Life insurers are putting their profits in acquiring new business. To some shareholders divided will a good option, i would prefer company should not give dividend, rather invest money in their business. One more example where profit is invested in business is D-Mart.

Disc: Invested in both. However ratio is 1:4. (X time in AMC and 4X time in Life insurance).

hii all,

i have one query. why ROE of IIFL wealth management is lower (Fy20E 9.3%) i.e in single digit and HDFC AMC (Fy20E 41) & Nippon asset mgt (Fy20E 21) co. is much higher than IIFL wealth ?