Background / Overview

- Was set up in 1991 – came up with IPO in June last year. IPO was oversubscribed by 41 times

- One of the largest manufacturers of bromine derivatives & lithium salts in India

- Has a diversified range of 205 products in pharmaceutical & agro chemical intermediates

- Strong R & D capabilities with dedicated in-house team. (10% of workforce in R & D)

- Promoters are pioneering technocrats with substantial domain expertise (chemical engineering background); cumulative experience of more than six decades.

Business verticals

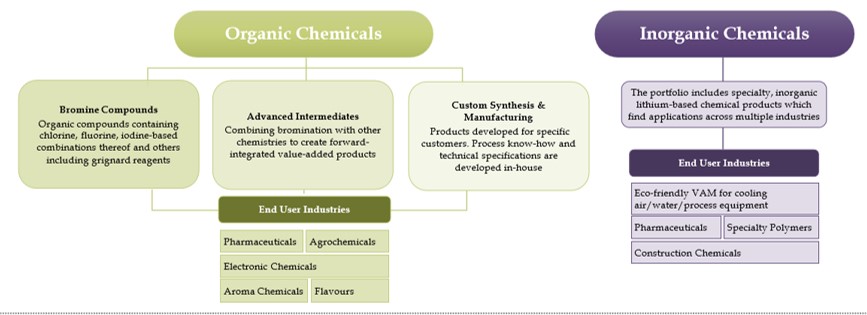

The company operates in 3 business segments

- Manufacturing of organic chemicals (Producing bromine-based and other value-added advanced intermediaries)

- Manufacturing of inorganic chemicals (Producing inorganic Lithium based chemicals)

- Custom synthesis and manufacturing

End user industries

- For Organic chemicals : Pharma, Agro chem, Aroma Chemicals, Favours

- For inorganic : Engineering companies (eg: Voltas, etc), pharma, specialty polymers, construction chemicals, etc

- Derives more than 80% of revenue from pharma & agrochemical industries

In-house capabilities

- Company has R&D expertise supported by two state-of-the-art R&D facilities

- 10% of workforce is in R & D. Total employees: around 240

Manufacturing capabilities

- It has 2 plants – 1 at Mahape and 1 at Vadodara.

- Upcoming unit in Dahej SEZ – which will build additional capacity

Revenue split (domestic vs exports)

- 64% revenue from domestic and 36% from exports as of FY 20

- Has been exporting to 27 countries.

High entry barriers

- Among handful of companies having expertise in the niche and specialised business area of bromine and lithium-based compounds

- Products necessitate meeting stringent quality and impurity specifications

Raw material sourcing

- For bromine – 75% to 80% sourcing is in India. Rest from Israel, Jordan & US. Company has stated in con-calls that Bromine is a bulk commodity. So there is no bargaining power as such for the suppliers.

- Lithium – Mainly from Argentina, Chile – Three suppliers there, who are world’s top 3 lithium producers

Stable relations with suppliers

- 10+ years of strong relationships with bromine and lithium producers

- Product supply and price stability

Clientele

- Clientele - Pharma clients include Sun Pharma, Hikal, Divis, Mylan, etc. Engineering – Voltas, Kirloskar, Austin, etc

- 70% business comes from customers who have been there for more than 5 years / long term stable relations with customers.

Capacity

Capacity utilization – 80 to 85% utilization.

Two major capacity expansion planned:

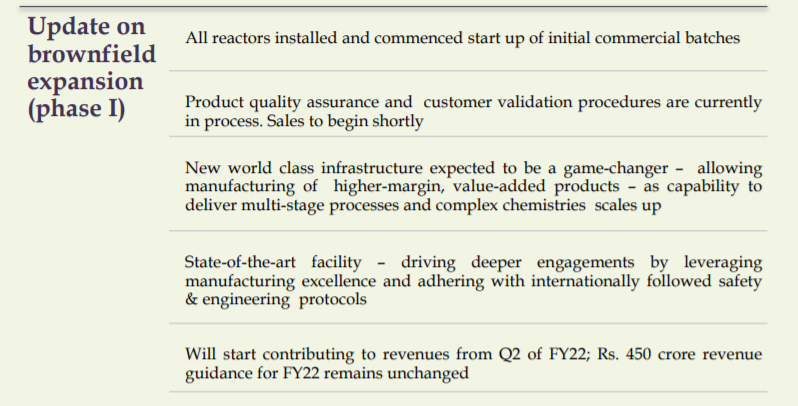

- 12,00, 000 kg inorganic specialty chemical greenfield project in Dahej SEZ. Has been operational recently.

- 1,26,000 litres organic reactor capacity . Will be operational by end of this FY. This will double their capacity for organic.

- With this doubling of capacity expects to generate revenue of close to 450 cr in FY22

- Capacity expansion for inorganic is completed and the capex amount of approx. 15 cr was through internal accruals

- Capex amount for organic this FY is likely to be around 75 to 80 cr .

Seasonality

- Second half of year (H2) is usually better than H1 (Apr to Sep), owing to strong demand from Europe in 2nd half of the year – orders tend to scale up in latter part of the year. Lithium based chemical demand tends to be strong in Q4 as demand from Ventilation & AC segment is linked to capital expenditure that enjoys 100% depreciation benefits for air-conditioning/cooling machines.

- Therefore results not comparable on QoQ basis to an extent. However they have more or less maintained their operating margins – last 4 quarters

Forward integration

- Company has been trying to leverage expertise and innovation capabilities to forward integrate

- And enter areas of custom synthesis and contract manufacturing to provide more value-added products and services to customers.

Competition - Most of their competitors are based in Europe, Japan and China

Financials

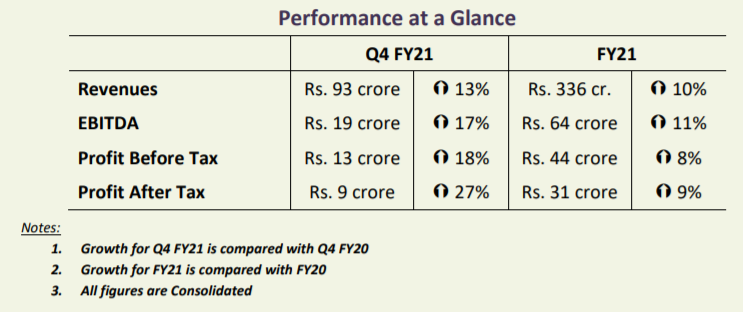

- Last 5 years Revenue CAGR: 29%

- Last 5 years PAT CAGR: 42%

- Annual sales for FY 20: 306 Cr

- Profit After tax : 28 Cr

- Earnings per share: 12.28

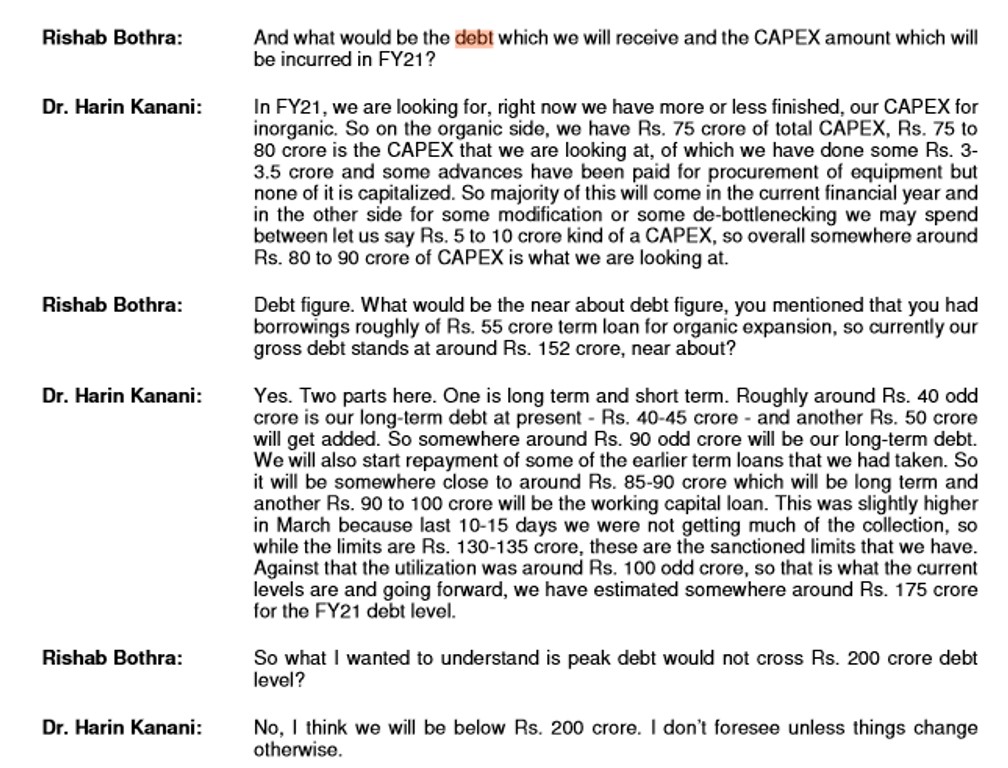

- Debt to equity: 0.85. Has taken 55 cr term loan last FY for the organic capacity expansion.

- Dividend Yield: 0.3%

- Healthy Return on Capital Employed for last 5 years: between 23% to 26%

- Valuations: currently trading at around 60 PE.

- Free cash flows negative

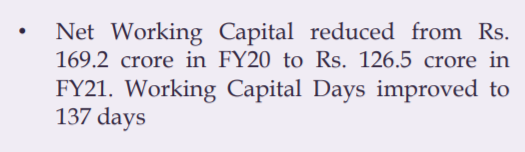

- Largest part of working capital is WIP inventory. Company has to maintain certain inventory levels to meet key client requirements. Hence free cash flows are negative currently.

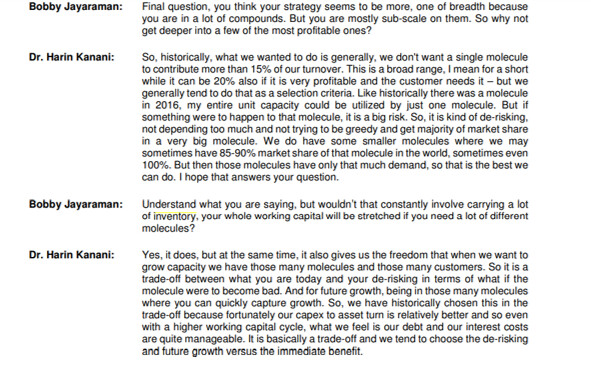

- Inventory turnover requirement will change with higher capacities coming in. The need to hold large amount of working cap inventory will go down, thereby working cap days will go down. Resulting in improved free cash flows.

- Promoter shareholding: 64.3%; Has got revised from 70% in last quarter owing to Malabar India Fund entering the scrip with 4.4% stake No pledge.

- Low Float scrip

Key Points from last 2 con-calls

- Revenue mix : 50% from bromine compounds business, 30% from speciality intermediates & custom synthesis , 20% from lithium chemicals business. Company plans to maintain the ratio, may not got altered significantly in next 1-2 years.

- Revenue guidance: The company has given revenue guidance of approx. 350 cr for FY 21 and little less than 450 Cr for the year after (once the new capacities come into picture).

- Operating Margin guidance: Margin has been 18% to 19% for last 3 years. Management has guided to maintain Operating margins: 18.5 +/- 1% in near term.

- Lithium chemicals find applications in pharma industry (anti HIV molecules), eco-friendly methane (VAM) for cooling equipment, etc

- Pharma business in the anti-HIV space likely to be a good driver for growth.

- Once Dahej capacity comes in by end of the year, it will lead to more revenue from advanced specialty intermediates.

- In a way, revenue is somewhat constrained more by supply / capacity than by demand.

Q1 results

- 18% increase in revenue in Q1 ; EPS 2.62 v 2.32 on year or year basis

- Revenue from organic chemical business is up 36% in Q1 FY 21

- Revenue from Inorganic chemicals (lithium based) is down 33% in Q1 YoY; since engineering companies took some more time to start operations. They were almost shut in April & May.

- Post June, have started getting regular POs. So demand has resumed and inorganic business for Q2 this FY should be on par with last year

Neogen Q1 result.pdf (1.2 MB)

Possible Risks

Raw material price fluctuations

In the recent con-call – there was a point regarding drop in lithium prices. Lithium prices have dropped about 45% in last 6 months (Link:https://www.reuters.com/article/us-chile-lithium-sqm/chile-lithium-producer-sqm-posts-record-sales-profits-plagued-by-low-prices-idUSKBN25G140) )

The management acknowledged this and mentioned that they would be able to maintain per kg margin in that business segment. However this fluctuation in RM prices is a risk one needs to be wary of.

Negative free cash flow:

Not able to generate free cash flow currently owing to high operating costs (detailed earlier in the note)

Delay in capacity expansion – The Company has guided for capacity expansion in organic chemicals to be completed by end of this FY. But this is a possible risk as any delay in cap expansion would mean inability to meet additional demand and can dampen next year’s revenue target.

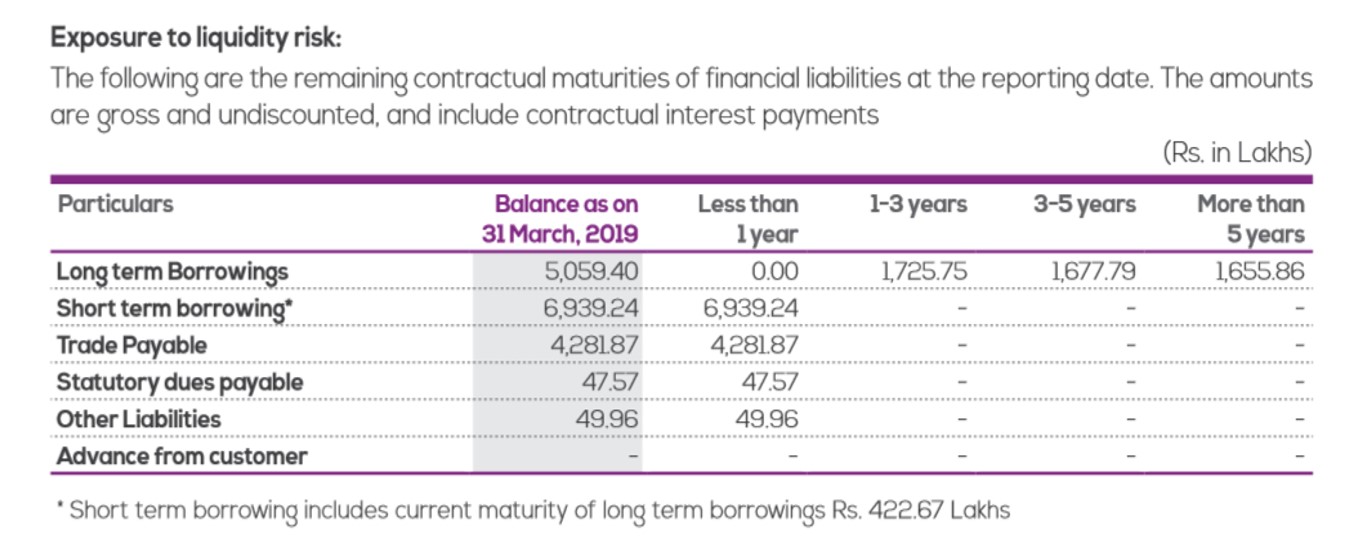

Liquidity Risk

Long term borrowing ~ 90 Cr. This includes the 50 Cr term loan availed recently for capacity expansion.

Short term borrowing 102 cr up from 65 Cr last FY.

In case of any delay in planned capacity expansion – might necessitate the need of further borrowings - short term or long term.

References:

Low float - Low float scrip

Disc: Invested; at sub 400 levels.