Hi! I have tried to compile the information in a excel sheet. Hope it helps. I have updated the data till Q3FY23.

GFL.xlsx (14.6 KB)

Hi! I have tried to compile the information in a excel sheet. Hope it helps. I have updated the data till Q3FY23.

GFL.xlsx (14.6 KB)

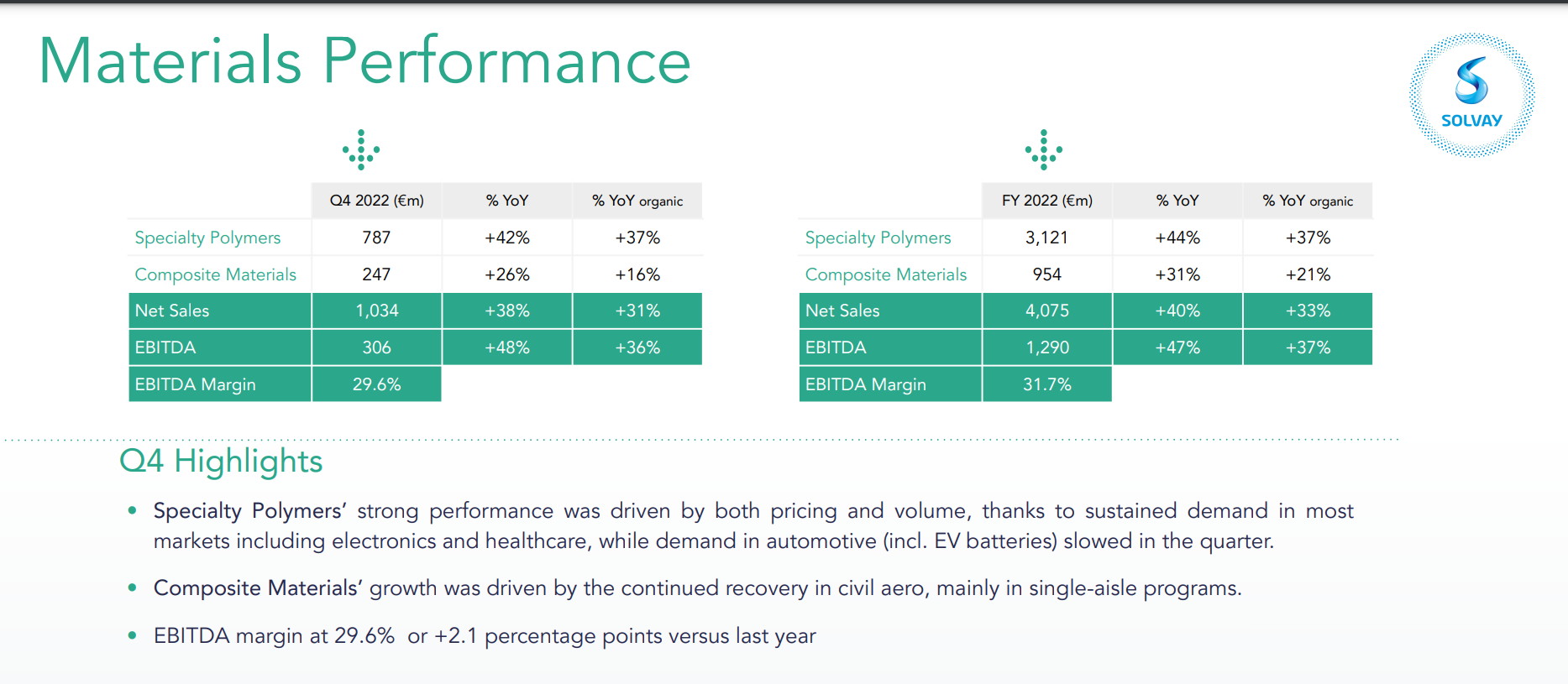

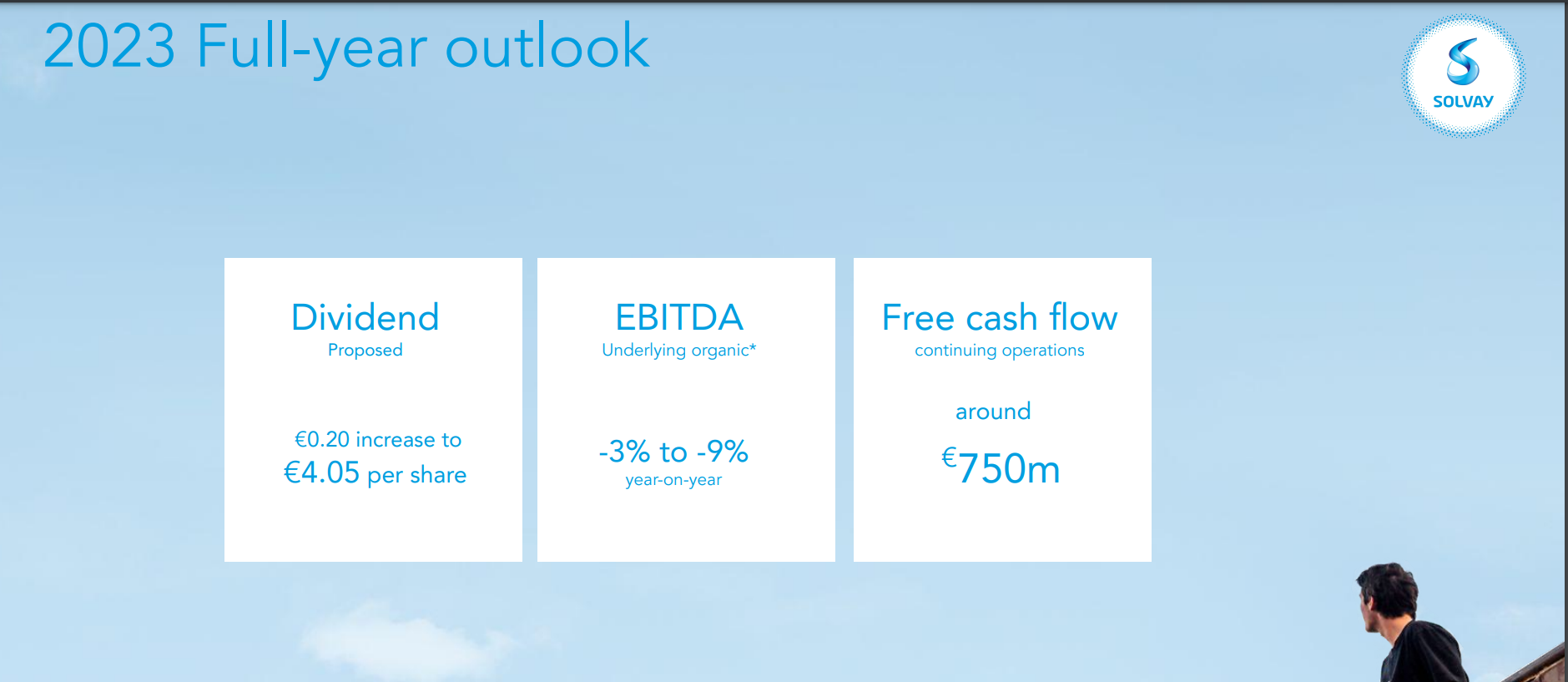

Solvay has posted good results for Q4 2022. However, has cut EBITDA by -3% to -9%

year-on-year for 2023, as it expects slow down in demand. Q4 2022 witnessed slowdown in automotive (incl batteries).

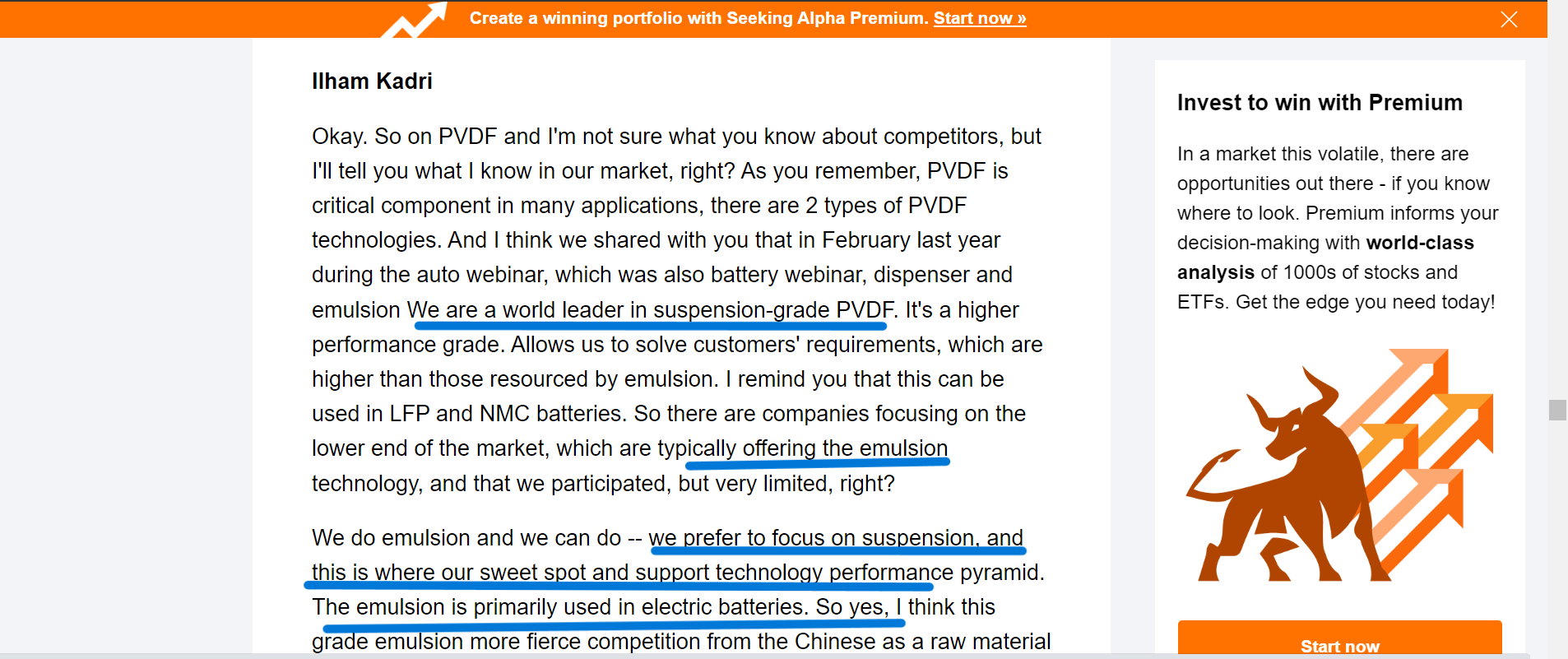

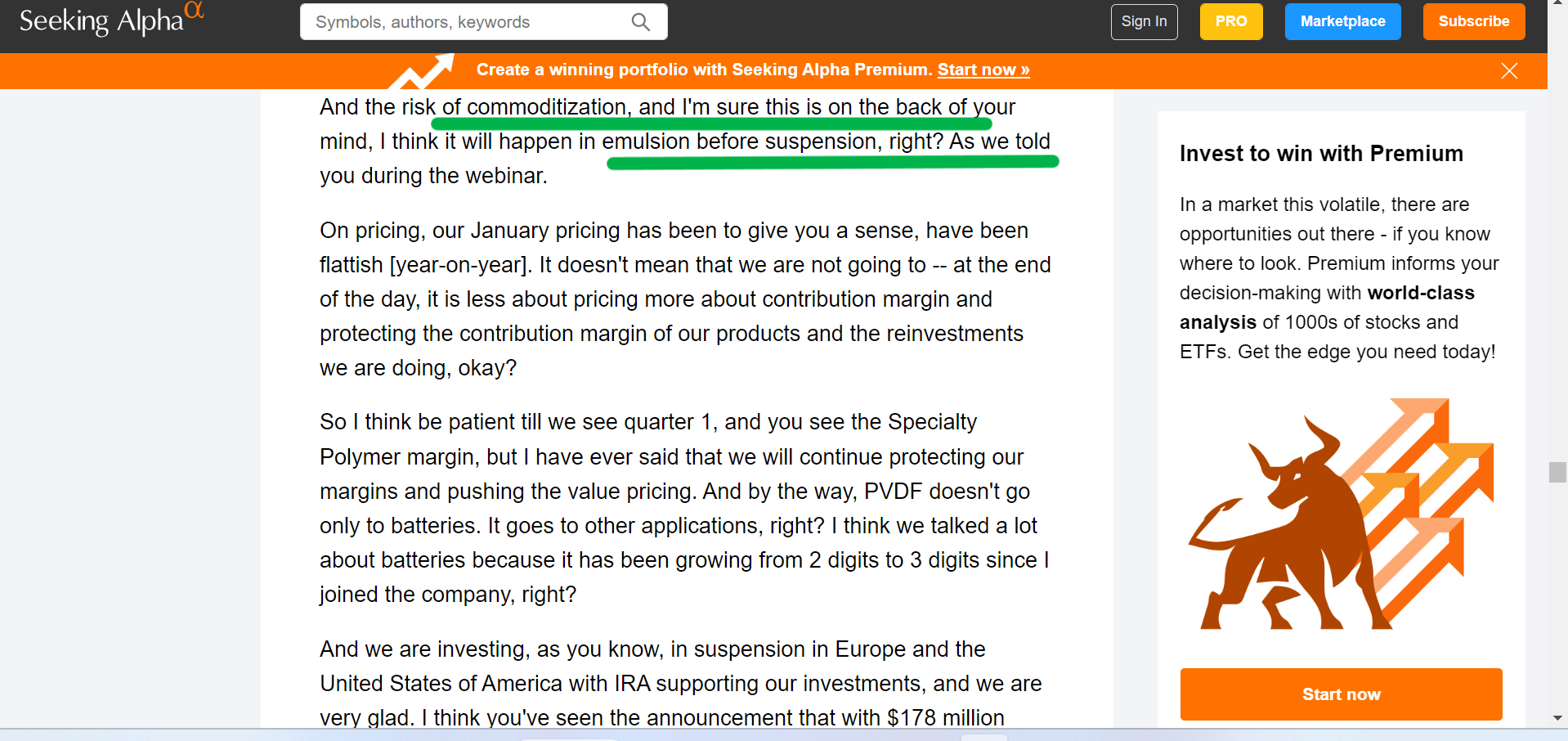

On asked about the outlook on PVDF during call, management has to say this -

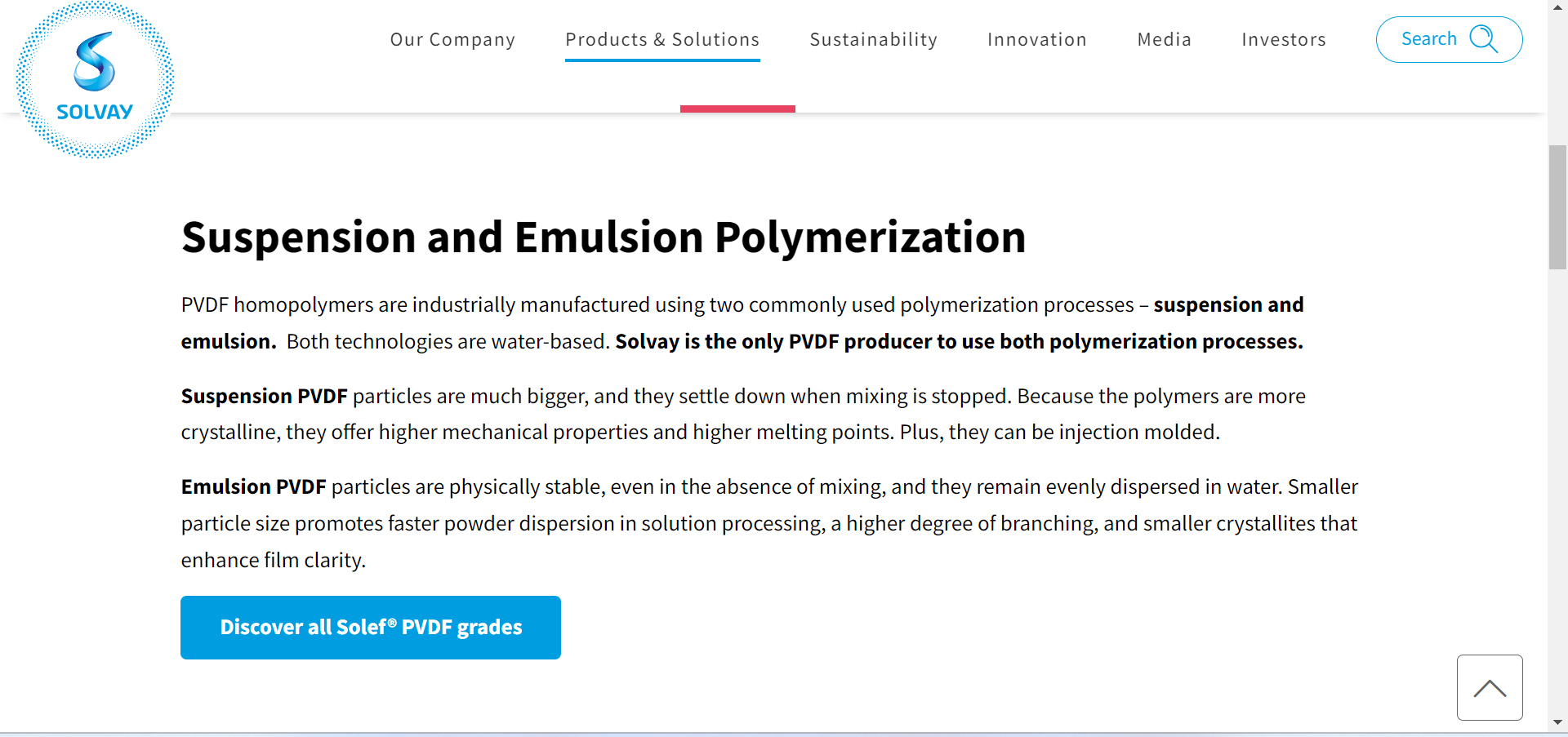

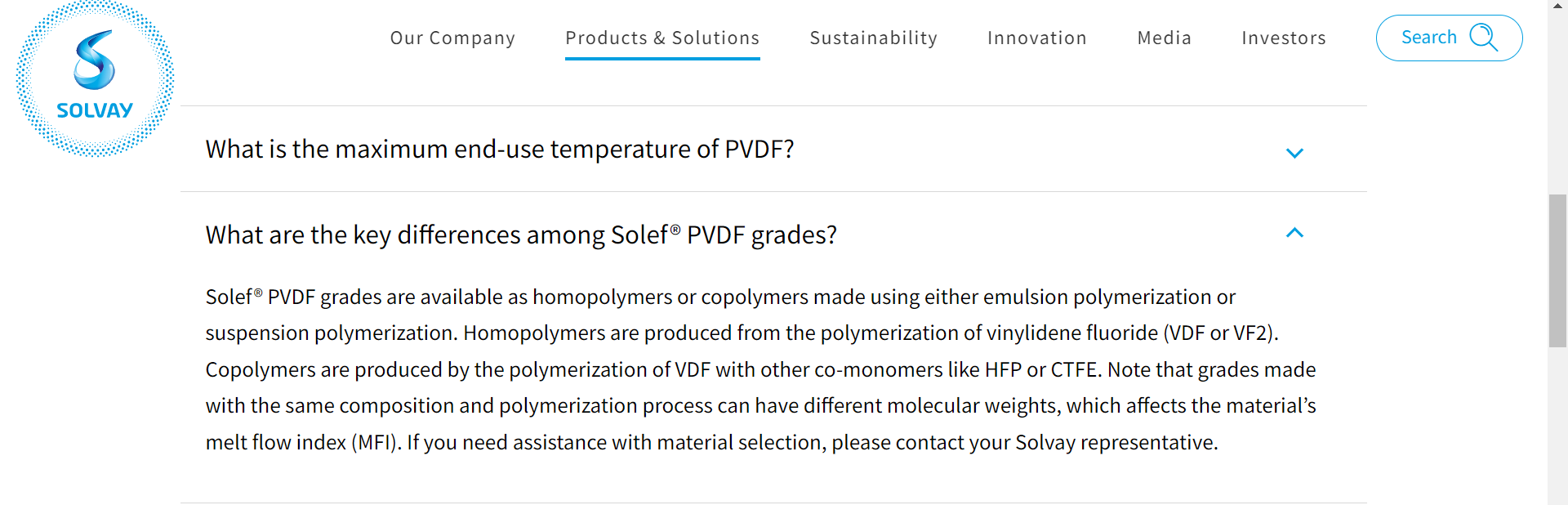

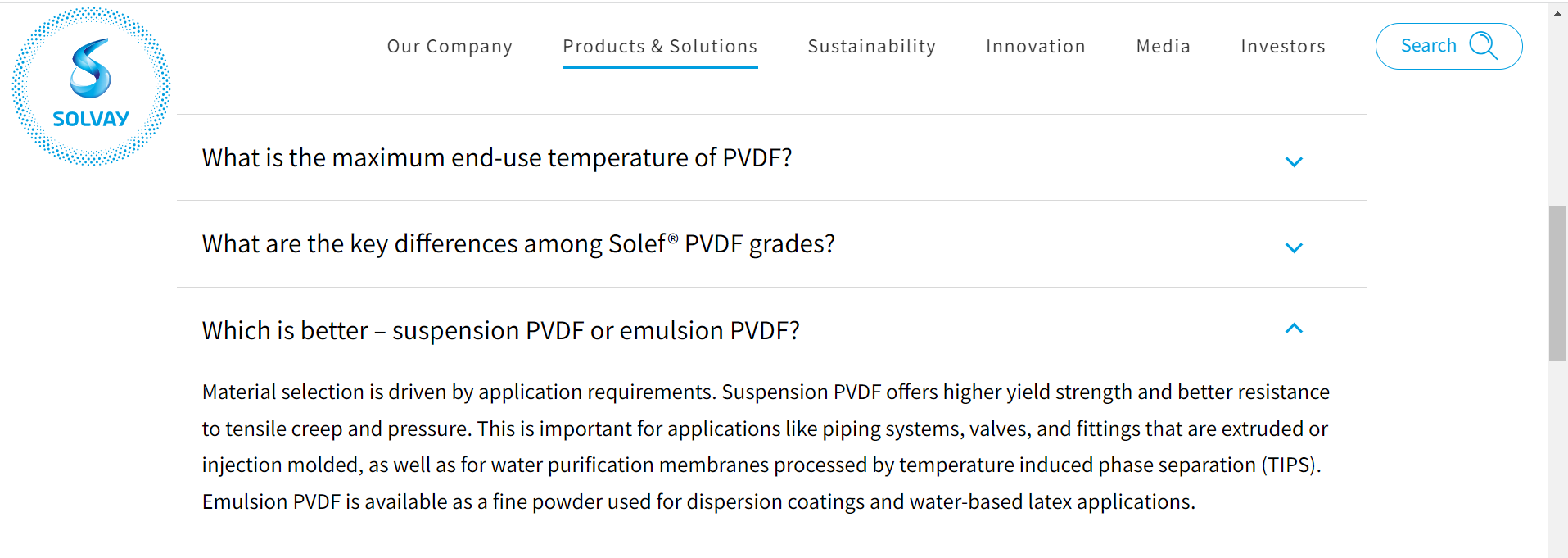

There seems to be two types of PVDF grades - emulsion grade and suspension grade. Both are used in electric batteries. So as per the management the risk of commoditization may be in emulsion first, where there is competition from China. Here it looks like so far the price is driven by R142b, which is in short supply and this in my view will continue.

Whereas in suspension Solvay seems to be way ahead of the league and is the only manufacturer which manufacturers PVDF using both suspension and emulsion polymerization processes .

Solvay manufacturers PVDF under the brand Solef -

Though both grades are in demand, it looks like suspension grade is superior.

GFL on the other hand seems to manufacture both emulsion and suspension grade PTFE (easily available in AR and product catalogue), but does not look like the same when it comes to PVDF. Both PTFE and PVDF in my view belong to the same family but are very different, involving complex chemistry especially where different grades are involved.

GFL does not seem to have developed the technology to manufacture PVDF using suspension polymerization. GFL manufactures PVDF under brand Inoflar and no where there is a reference to the process adopted.

https://www.inoflar.com/products.html

In my view, battery grade does not look like the differentiating factor as Solvay claims they are agnostic to battery technology. There are more finer nuances to this technology and its very complex to understand. Then again this is only one part, there are different grades among FKM, FPA etc. as ananth has put above. If someone has more info on this and my understanding above is wrong, happy to stand corrected.

Here’s a summary of discussions with a Industry source. (using the 10 Questions Template)

[Travelling, so please bear with me as I keep updating]

What can you tell us about GFCL Management?

From what I have seen Vivek Jain (Forbes Profile) is smart, educated (St Stephens, IIM A grad), widely travelled, and a genuine person. His vision from the starting was aiming for global success. Has built a team of dedicated professionals around him since inception of GFCL. He has travelled abroad and studied the market/industry extensively before starting GFCL PTFE factory in 2006/7 in Dahej. EOY 2022 ‘Business Transformation’ category winner. Contemporary business leaders call him “The Slog Overs Man” !

Anecdotally we know a set of 3-4 Key people were identified by Vivek in the early years, empowered and given a free hand -after taking a commitment – We are in for the long haul, this is a very long journey, you can’t leave midway! You will have the freedom to do things the way you want, build the organization, build the “Culture” and enable creative expression. Core Team has been with GFCL for 15+ years now I think.

Are you able to elaborate on GFCL Culture?

You might have seen the EOY Finalist Video - Vivek Jain’s advise to aspiring Entrepreneurs - No short cut to Success. Hard work, Perseverance, and Focus are pre-requisites.

GFCL Culture is about inculcating – hard work, commitment - come what may, persevere through adversity, remain totally focused on the job at hand – with “fearlessness”. Extensive training given for 6 months to new joinees – technical, commercial, behavioural by in-house leaders and outsourced agencies. Have heard that Sales guys for example are told "go out in the field, learn from customers, you can plan your own travels, don’t need to ask anyone; responsibility is yours – just meet the targets.

New recruits who have excelled in this environment by showing initiative – some have within 5 years been promoted to leadership positions.

What can you tell us about the Genesis of GFCL PTFE Ambitions?

Hindustan Organics started a fluorocarbon factory in 1987 for 500T. That time the Indian PTFE Market was ~1500T market. 1000T was imported, and rest supplied by HOC. They are probably still at that capacity. Never expanded, sold everything domestically. Never exported.

GFCL had been doing R22 from ‘1999-2000. That was a core competency. Everyone knew phase-out was going to happen in 20-25 years. They would have to compete with new molecules. Realised PTFE was a good upstream possibility.

When GFCL started PTFE in 2007-08, Indian demand was 1000T. Recognising that the chemical/polymer business requires scale economics – they straightaway put up a 5500T plant for the Global Market. The Chemical complex in Dahej had a captive power plant, caustic soda and chlorine plant, chloromethane plant, and a PTFE Plant. The carbon credits money had come in handy for them!

PTFE Grades

There are different PTFE Grades fro different applications. China Market Grades, and Developed Market grades. Will be great if you can throw some light on base grades and value-added grades, qualification/ approval process, and price realisations

Can’t comment on detailed segmentation.

They started in 2007/8, must have been selling base grades for first 2-3 years, and stabilising operations. Post 3-4 years, they started selling higher grade applications for Automobiles and others

From what we know, Qualification takes up to 6months to 1 year usually for basic grades; at the same time with a foot in the door, everyone starts pursuing Plus grades – that can take up to a year or two; and then Super+ grades it takes about 1.5 to 2.5 years plus of hard grind - rejections to repeat trials to passing performance benchmarks of customers. There are Simulators for performance testing that shorten timeframes (~say 3L Kms for automobile grades, needs 1000 hours simulation; similarly foir Aerospace)

Rough price realisations:

China Market: Base Grades $5-6/Kg; Plus grades $6-8/Kg

US/EU/Japan: Base Grades $8-10/Kg; Plus Grades $12-15/Kg; Super Plus Grades $15-18/Kg

(Incumbent realisations like those of - Dupont, 3M, Daikin, AGC, Solvay)

GFCL has 18000T PTFE capacity today, and expanding to 21000T by debottlenecking. Do they have to do this all over again?

Getting to full utilisation might take time based on how supply demand/pans out. Now that they have many grades qualified, next expansion is always easier.

Is there a lot of gap between value-added grades qualified by GFCL, and that of Incumbents?

It appears that there is some gap, passing higher-grades performance benchmarks is not easy. It takes repeated trials, enhanced R&D capabilities, dogged perseverance. There are probably 10-15 super plus grades, some $200/kg, $500/kg but are today niche applications.

Would you give more credit to GFCL In-house R&D? Or External Consultants might have played a big role?

Both are required. The perseverance/skills displayed by R&D Teams guided by External consultant’s experience/expertise and/or direction setting.

Would you know the profile of such consultants?

Ex-Incumbents would be a good guess

LiPF6 CS Report - global capacity growing @61% CAGR, but demand growth @34% CAGR

In 2022 utilisation rate 72%, utilisation to fall to 42% by 2025 ! Has GFCL got the Timing/Expansion off?

Yes, supply-demand in medium term may look iffy - if based only, on China expansions.

It seems CS Report talked about till 2025, right – 2-3 years from now. Did they talk about what is happening by 2030? Did they talk about who are the Battery Cell technology guys, what is happening there? They didn’t?

See a 2-3 years view is probably self-defeating.

Meanwhile in the near to medium term, better realisations are probably possible in US/EU/Japan markets, but not in China Market.

Chinese Fluorochemicals play

Why won’t the huge Capacities cause a problem down the line for GFCL. 2024 may be good, but post that, things can become worse?? Why have the Chinese NOT got into the more promising Fluoropolymers? PFA, FKM, et al. Is Technology a real barrier? Sourcing? What is preventing them?

You have to understand the Chinese way of working

PTFE – they were into – from 25 years back. China – will only go after – Mass consumption markets

Volumes Market/Base grades/Base Plus grades.

Would they have allowed someone like GFL or other Challenger to become 4th largest player globally?

They are NOT interested in Niche Markets and/or Specialised Applications. These are hard to Qualify, Long Term Markets. They dont want to get into any contractual-obligations type market. Almost all of Chinese produce is SPOT Sales, Distributors driven, Easy-Meat market.

Yes, should some of these products become mass market one day (say PFA), they for sure will get into it. Even if they don’t have the technology today, there are probably ways and means for that ![]() .

.

PTFE Scale up

3M exit opportunity. Is it a fair argument that GFCL is in the best position to get a bigger share of the pie from EU Market than Others

Probably, right. Remains to be seen if it can free up further capacity by de-bottlenecking (new capacities haven’t been announced) and also move up the value chain, with newer grades.

FKM Opportunities

It may be good to point out there are 3 FKM polymers - Co-polymer, Tar Polymer, Tar Polymer Peroxide. Domestic use of Tar Polymer FKM use is expected to go up significantly with enhanced Ethanol blending (20% from existing 10%) becoming widespread.

PVDF

Is it correct to say that PVDF Separator is a commoditised business, while PVDF Binder is a protected (2-3 player) market?

Well definitely commercially available PVDF Binders there are very few players.

But it will be wrong to infer that PVDF Separator is a commoditised business. That anybody can make it. Not at all.

What has happened though is that Margins have normalised back. It is still a healthy 30%, though.

One way to appreciate better what has really happened. Say PVDF was being initially sold at 100. Raw Material (R142B+) was 40, and other costs 30, leaving a margin of 30%

Now RM price went through the roof due shortages. Progressively from 40 to 400 (10x). PVDF prices went upto 550, beyond that pass-through was not possible. This was NOT sustainable, anyways! Subsequently RM comes back to 80, and PVDF corrects to 200. Gross margins are still 60%. Other expenses take away 30%; Margins back to 30%

It’s NOT as if the whole PVDF (battery grades) opportunity has gone away. Just that Peak Margins have moderated.

PTFE Binder vs PVDF Binder

Is it correct to say PTFE Binder is becoming more preferred route, as it has advantages?

As far as we know there are 2 technologies. Wet Electrolyte Tech - PVDF binder. Dry Coating Tech - PTFE Binder. Demand for both exists.

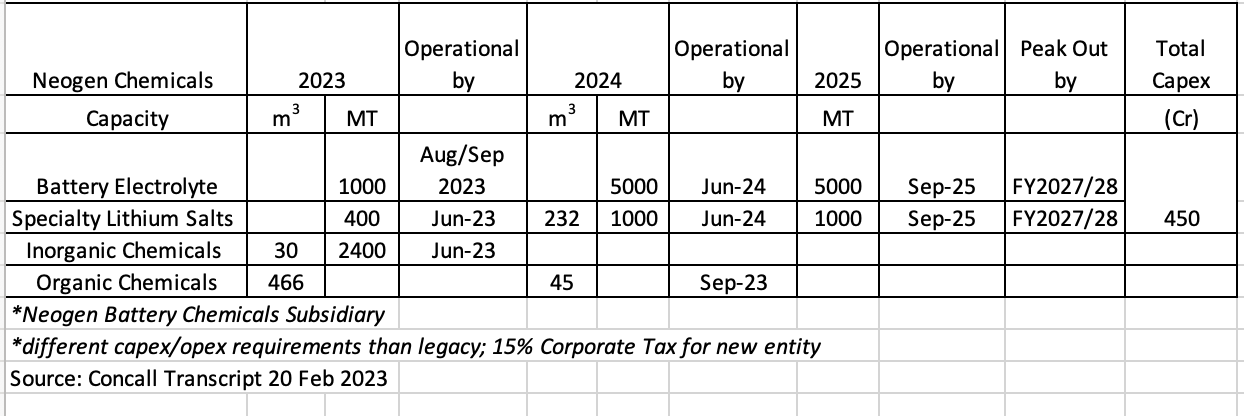

Battery Chemicals Subsidiary

On one hand this holds out exemplary opportunities to harness. On the other, there are many who claim to be setting up say Battery Electrolyte factory as the “formulation” is easy?. Neogen (Lithium Carbonate manufacturer) is one such Indian player. Is GFCL biting off more than it can chew? Can there be margins sustainability as more and more players enter the field?

At the moment the Industry needs capacities build up, and there is room for more players. India itself has plans for 280GW by 2030 as mentioned before, whereas installed is less than 1 GW. There are 3-4 players who have applied and got PLI Approvals for batteries in India. And there is ample scope for global supply (3000-4000 GW by 2030) on scale efficiencies.

But the question is valid - can everyone go on a spree of adding Electrolyte capacities (easy to do as you say from efficient sourcing) since LiPF6+ Lithium Carbonate are say in abundant supply?

My sense is at some point this will come down to shortage of flourspar mining. The Battery Cell technology guys must be taking that into account while scouting/securing end-to-end supply chains (which is the new imperative).

You guys could do more work on Battery Cell technology guys - to get a clearer picture. Who are they? And what are they doing?

PFAS/Non-PFAS polymerisation technology

Lot of noise made out on the above. On the one hand Incumbents like Arkema are on record saying new Fluoropolymers are central to modern industry, ecological and energy transition. Complete phase out is impossible/impractical and NOT necessary as fluoropolymers produced without fluorosurfactants should be exempted from proposed restriction. On the other hand PFAS Master List by US EPA now lists 12034 fluorochemicals currently ![]() . Even PTFE, PFA, and FEP seem to be on the list, but not FKM or PVDF. What is the Reality - Business as usual, Or?

. Even PTFE, PFA, and FEP seem to be on the list, but not FKM or PVDF. What is the Reality - Business as usual, Or?

The proposed ban to phase out between 18 months to 12 years starting 2027, is a joint EU proposal by 5 collaborating countries - Germany, the Netherlands, Denmark, Sweden and non-EU state Norway.

As far as the fluorochemcial industry is concerned, we find it short on relevance/ feasibility aspects. Whether you take the EU ban List (10000 chemicals) or the US EPA lists (430 chemicals) - the relevant chemicals are probably only 35 or 43.

Its like preparing a list with historical known pollutants (many of which are not even in existing use today). Its almost like saying we are banning memory sticks, but we must also ban CD ROMs, floppy disks, and wait Kodak Films too.

The consultative process that is on should restore balance, as feasibility/alternatives are investigated more thoroughly, more practically.

Process Chemistry

We know multi-Step Reaction Yields generally improve over time in Chemicals (e.g.Divi’s in Pharma, PI Industries in AgChem). Does the same apply for Flurochemicals process industry?

Any chemical process that would apply. Yield improvements are a constant quest and give us better yield from the same capacities over the years as we gain experience with the process. We use new additives, new surfactants, better catalysts and recipes, or reaction initiators, better control systems, washing cycles, drop by drop release, and the like.

[forgot to ask range of typical yield improvements possible over years - 25%, 50%??]

Disclosure: Invested (read probably biased)

PS1: fully transcribed now from my Notes

PS2: Let’s use this what we learnt here, with the next domain/industry expert we get access to

PS3: Over to you @sahil_vi and other young turks

Some more perspective/data-points to think about the Battery Electrolyte Market in India till 2030

[“Electrolyte”/“Battery Electrolyte” search powered by Needl.ai]

Source: Neogen Chemicals Con call Transcript Feb 2023

Tattva Chintan Con call Jan 2023

Ami Organics Con Call Feb 2023

Gujarat Fluorochemicals acquired 26% stake in GFL GM fluorspar (morocco based mining & selling company of fluorspar), a subsidiary company of GFL singapore.

GFL singapore is wholly subsidiary company of Gujarat Fluorochemicals.

Basically morocco based company is a step down subsidiary company of a Gujarat Fluorochemicals.

Earlier it was 74% stake, and now acquired fully.

Cost of acquisition is INR ~3.72 crores (USD 4,52,954).

Orbia Q4CY22 concall snippets (on PVDF and LiPF6)

Two of the most significant announcements that we made in this call are on our projects, the PVDF joint venture with Solvay that we are kicking off. And the LiPF6, which is 100% or be own venture that is also being kicked off. These are transformational and very significant, right? And so we are putting up 20,000 tons of PVDF and 10,000 tonnes of LiPF6. But the market potential for these over the course of the next 10 years, you’re looking at a 5 to 10x expansion in these markets in the course of the decade. And in terms of investment, the PVDF investment is an $850 million investment with – of course, we have a 49% stake, so it will be proportional. And the LiPF6 investment is roughly $300 million investment with a $100 million grant from the Department of Energy. Now if you remember, Frank, at the Investor Day, we had shared that most of our growth will come from organic growth projects. 80% or more of a growth is coming from organic growth projects in this 5-year period with investment to EBITDA ratios of 2 to 4x. And what I can say to all of our investors and the analyst community that the economics on these 2 projects are on the more favorable and more attractive side of that range. Which is a huge deal, right? And of course, it’s going to take 3 years to deploy that capital and kick that off and then plan for subsequent expansions. But especially given the near shoring of supply chains and the United States desire to have security of supply for both battery and semiconductor value chains and the fact that we are fully integrated from my end to market from Mexico to the United States. This is a big, big deal, okay? So I just wanted to make sure we get that out there.

And then later on in this year, we’ll start deploying the early phase of the capital for the LiPF6 and the PVDF projects.

Update on Lithium Prices

An interesting article on PFAS

Article: https://cen.acs.org/materials/polymers/fluoropolymer-makers-trying-hold-business/101/i8

Interesting view points:

European Chemicals Agency published a proposal from five member countries to ban per- and polyfluoroalkyl substances (PFAS) containing at least one fully fluorinated carbon atom—an estimated 10,000 molecules in all, including popular fluoropolymers. Member states would vote on a ban in 2025; if it’s enacted, exceptions for fluorinated chemicals that cannot be replaced with alternative chemistries would expire in 7–12 years.

You’re talking about replacing a chemistry that’s been around for 60, 70, 80 years.

The European proposal, if it stands unchanged, would spell the eventual end for common fluoropolymers like PTFE and PVDF.

Arkema:

Ever since fluoropolymers were introduced, in the middle of the 20th century, making many of them has required using fluorosurfactants. These processing aids are critical to the emulsion polymerization process, in which a polymer is built in water from fluorinated monomers. The surfactant stabilizes the growing emulsion particle during polymerization, so you don’t get agglomeration or coagulation. When the polymerization is done, the surfactant is washed out of the polymer mixture, but some residual surfactant remains. Fluorosurfactants have minimal impact on the polymer’s final properties, he says.

The task is trickier than merely swapping one fluorinated surfactant for another, Gaboury says. “It’s relatively easy to make the emulsion polymer with a nonfluorinated surfactant,” he says. “It’s difficult to make products with a nonfluorinated surfactant that have the same performance profile at the very end. When chemists change to a nonfluorinated surfactant, they usually change other ingredients as well, such as the initiator and the transfer agent. “You have a little bit different profile of reactor materials, and ultimately there’s a little bit different residual profile in the product.” That can cause performance problems.

new surfactants are typically hydrocarbon-based. But the hydrogen-carbon bond isn’t as strong as the fluorine-carbon bond. “The presence of that hydrogen results in side reactions that you don’t want when you’re making a fluoropolymer.

PTFE is made with a highly reactive monomer, tetrafluoroethylene, that creates many unintended fluorinated by-products. Chemours hasn’t found fluorosurfactant alternatives for PTFE or for similar polymers such as fluorinated ethylene propylene and PFA copolymers that don’t result in such by-products.

DONGYUE GROUP LIMITED

Financial reports for year ended 31.12.2022.

Page 28 - 29 speaks about the performance of fluoropolymers and Refrigerant gases

Couple of points that caught my eye:

However, judging from the overall market situation of the year,

the price trend of PVDF products went from high to low, and unable to maintain at the

high level compared with the beginning of the year.

R22 has been one of the key raw materials for the production of the fluoropolymers (i.e.

PTFE, HFP and other downstream fluorinated chemicals) and R125. R125 and R32 are

the key refrigerant mixture for other types of green refrigerants (such as R410a) to

replace R22. Currently, R410a has been the principal replacing refrigerant which has

been widely applied in inverter air conditioners and other green home appliances

According to Elara capital Q4 FY23 preview: Gujarat Fluorochemicals (FLUOROCH IN) is likely to report PAT contraction of 24% QoQ on a 67% dip in PTFE spread and a 30% decrease in PVDF spread.

ICICI Securities: Gujarat Fluorochemicals’ EBITDA may rise 52% YoY to Rs5bn. Bulk commodity revenues are likely to dip 18% YoY due to fall in caustic soda and chloromethane prices. Fluorochemicals revenue to benefit from ramp-up in R-125. Fluoropolymers revenue to benefit from higher realisation in PTFE; and volume ramp-up in new fluoropolymers. Revenue to grow 34% YoY to Rs14bn. Gross profit margin may dip 230bps QoQ to 70.2% on lower bulk commodity revenue.

EBITDA margin to be at 35% (down 190bps QoQ). Net profit may rise 50% YoY / up 1.1% QoQ to Rs3.3bn.

I was reading a report by elara on srf which says that HFO R1234YF patents are expiring in 2025 & that SRF is only co in india which has the capabilities to manufacture R1234YF already.

I also read in parallel that Navin was manufacturing HFOs for Honeywell in crams :

https://cen.acs.org/business/specialty-chemicals/Honeywell-taps-Navin-make-HFOs/100/i5

This makes me wonder where GFL stands on HFO since patent expiry in 2025 can shift the adoption curve towards the greener R1234YF (An HFO) away from the current R32 / R125 (replacement demand might still remain but OEM might go away)

If we don’t know, then this might be a reasonable question to ask in concalls to understand GFL plans around R1234YF

GFL has indicated plans to enter 4th Generation ref. gases (HFOs). Some excerpts from DAM capital’s 21Sep2022 report:

Just to add Navin isn’t doing R1234YF

They’re are doing this one instead + GFL plans to enter HFOs. Srf has the tech and pilot plant already ready ![]()

No Navin is Producing HFO 1234yf for Honeywell (CRAMS) and they have now added HFO 1234zd again for Honeywell.

Gujarat Fluorochem Concall: Q4FY23

-YOY growth of 40%+ in topline.

-EBITDA growth for FY23-71% and for Q4 it was 61%.

-Q4PAT growth of 52% YOY.

-ROE and ROCE crossed 20%.

-D/e at 0.23 times.

-By Q1FY24, adding 1300-1500 tonnes of capacity. New capex we put in, takes almost a year to give full capacity.

-FY24 and FY25 expect growth due to New age fluoropolymers and Battery chemicals.

-Expecting Ref gas revenues to be subdued in Q1FY24 due to the weather in Delhi and other parts of India.

-In Fluoropolymers, prices have corrected marginally.

-Optimistic on PVDF, FKM, PFA for growth and looking at entire bouquet of battery chemicals. Will be making Electrolyte, commissioning plant by Q2FY23.

-New site for future expansions.

-Expect ref gas prices to remain stable. Demand can be subdued in Q1FY24.

-Growth will be led by New age fluoropolymers, and revenue will go up.

-1500 crores of Capex this year. 1000 crores in Fluoropolymers and Battery Chemicals. FKM, PFA and PVDF will come up by Q1 and Q2 FY24. Capacity utilisation will take several quarters from there on. FY25- We will see full utilisation.

Margins will be at 30%+.

-If prices are constant, in fluoropolymers. We see 1000-1200+ crore per Quarter once all capacities for Fluoropolymers are utilised.

-1100 tonnes per month, 1500 per month in Q1 and further capacities will be added. By end of the year will be 1700-1900 tonnes per month

.

-PTFE capacity is coming by Q3FY24 end. 3M will be in operation till end of CY24. Impact on volumes will be seen by the beginning of next FY.

-FY25, we will see revenues in battery chemicals. Qualification times are 4-6months.

-On Working capital:- bought down from 155 to 120 days. Currently at 128 days. Lag effect of inventory we are building up for new capacities.

-Marginal Price correction in New age Fluoropolymers, not seeing much impact on volumes side.

-Corporate guarantees, reducing it on QOQ basis. See the reduction on a continuous basis. Guarantees have never been invoked or triggered.

-2 Applications of PEM: Making electrolyzers, ad second for Fuel cell for electricity. Present in both segments, tied up with ONGC for one segment and in the other doing our own tech development.

-Straight away going for a commercial scale plant in Battery chemicals. Not going for a lab scale. Commercial sales will happen by Q3 and Q4.

-Qualification for Solar panel back sheet is currently ongoing. PVDF films plant will go live in Q2. PFA for semiconductor, going through various stages of qualififactions.

-Expect full utilisation of New age Fluoropolymers capacities by the end of this Financial Year.

-Qualification period for New age fluoropolymers like PVDF for EV, and Semiconductor take at least minimum of 6months. PFA qualification we are expecting earlier.

-Q1FY24: Purely shutdown for PTFE. Annual shutdown we do every year. PTFE only.

-In our case: not seeing significant impact on PVDF. As PVDF capacities will go live in Q2FY24. Due to Chinese slow down in EV, prices might have declined in the short term.

-Confidence in Electrolytes and Salts is coming due to the growth in the sector. Volumes and capacity will be small vs the market potential.

-FY24: Top-line is expected to grow by 20%.

-Transition to PFAS free. Already converted 80%, and by end of this FY expect complete conversion. 100% PFAS free by end of this Financial Year.

-18 crores: Part of renumeration paid to MD and the Chairman. Note 3. Not a red flag.

Disc: same as before.

Chemours Q1CY23 Concall Snippets

On TSS (Refrigerants) business which consist of HFC and HFO

You kind of mentioned in passing that you kind of expected some really strong demand in the second half of the year going into that 2024 step-down in HFCs. Your volumes are pretty darn strong actually in the first quarter. I guess, are you seeing any – or earlier pull than expected for Opteon in some of your HFOs ahead of that step down? Or is this something else?

I think what’s driving volume – what’s helping to drive volume in Q1 was the strong automotive SAAR that we saw. Auto volumes were strong in both Europe and the U.S. And so I think as we think of the full year, one question for us would be where do auto volumes go? Clearly, the automotive companies are building cars with the supply chain more normalized. The question is with higher interest rates, does that continue throughout the year?

So I’d say our record Q1 performance in TSS is in part driven by strong auto, but it’s also being driven by continued adoption of Opteon in the stationary side. And then as we said earlier, strong HFCs based on an effective AIM and F-gas framework working as well.

So listen, TSS is really, out of the starting block, very strong. And we expect TSS to have a great yearYou mentioned the potential pull forward in refrigerants ahead of the step down. How much of an impact do you think that would have on your volumes after the regulation change?

So we’ll have to wait and see, to see what kind of summer we have? I think – my sense is, and we’ve indicated this on prior calls, is that the step down is likely to generate some level of buying activity as people sort of look, how much of my quota have I used up in the year, again based on how much demand there is this summer, how much do I have remaining and using that up towards the end of the year.

Clearly, in a market that’s restricted on volume based on a quota, that could drive more robust price in the second half. It may also have some impact on seasonal demand patterns throughout the year in terms of HFC demand as people look at their use of quota versus actual demand in the marketplace. So we’ll have to wait and see. But obviously, net-net, it’s a favorable impact on the business ahead of the step down next year.

On Advance Material Fluoropolymer business

APM is kind of a mix – well, APM has two distinct portfolios. Performance Solutions and Advanced Materials. And Advanced Materials tends to be “more economically sensitive.” These are broad industrial applications, where we saw some volume fade. There are also markets, candidly, we are deemphasizing as we free up inputs to drive the growth on Performance Solutions.

In terms of areas of strength, our Teflon PFA is integral to any new semicon fab. So while there’s some softness in electronics broadly speaking, there’s still a lot of focus on building new fabs for higher quality, lower node size chips, where our high-purity PFA is key.

And actually, the limiting factor for us on both things like PFA and Nafion membranes for hydrogen where again, we’re sold out is how quickly we can relieve capacity and, in some cases, get permits to expand capacity at some of our plants.

So there’s kind of a push and a pull within the APM segment this year where the advanced materials is more subject to sort of global macro, which you saw in our results in Q1. And Performance Solutions is really tied mainly to our ability to unlock capacity, which the team is really focused on.

as we said at the beginning of the year, for APM, this is a year of transition, right? You saw that in Performance Solutions is up 20%. Advanced Materials down 8%. And Advanced Materials are more economically sensitive business. So that’s kind of reflected as you’re going to think about overall seasonality into the year, have that overlay of the APM transition as well as you kind of think about overall guide for the full year.

There’s a large chunk of fluoropolymer and related chemistries market share available after 2025. Can you give a sense of how much of that Chemours should be able to pick up? And do you need to do any investments in 2024 on either in terms of new formulations, qualifications, customer service cost or CapEx to pick up that share?

We obviously believe that fluoropolymers are essential for modern living, but they are also key to renew economy whether we’re talking about high-speed data, AI, electric vehicles, hydrogen. And our big investments in APM today are focused on hydrogen, where we are wanting to do a significant expansion of our Nafion membrane capacity and capabilities.

We’re also expanding our Teflon PFA line in our Washington Works plant in West Virginia, which, by the way, we’re the only PFA supplier in the U.S. So if there’s a U.S. onshoring of chips, we’re key to that whole activity.

So the investments that we’ve announced today are both in Teflon PFA as well as the hydrogen facility, which we would like to cite in Villers-Saint-Paul in France, and we continue to be focused on those near-term opportunities. But the team is also very focused on debottlenecking a number of our plants.

Again, whether it’s demand for materials on the EV side, we’re really focused on the growth in our Performance Solutions business, which as you saw in the quarter, was up 20% and really is subject to more of our ability to bring capacity online more quickly.

Interestingly, Performance Solutions was 31% of the portfolio last year. In this recent quarter, it’s 39%. So that higher CAGR is making the APM segment a lot more specialized as we move forward in time. And candidly, when I look at our TSS and APM business, I really would agree with the sentiment that our multiple doesn’t reflect the power of the earnings of those businesses over time. So we’re very excited about where we go from here, and the team is very focused on delivering.

Solvay Q1CY23 Concall Snippets

Specialty Polymer (Fluoropolymer) Business

Sales in Specialty Polymers improved 15% driven by higher prices as customers continue to value what we bring are lightweighting solutions because these are mission-critical and they also have to reduce CO2 emissions. Volumes were slightly down mainly because of reduced demand in EV batteries as customers continue to reduce their high inventory levels. And that impacted the demand for our PVDF, but it’s important to note that our PVDF suspension technology offered a differentiated value proposition, specifically for the high-end battery applications like NMC. And this supports margins even in the current inflationary environment. Elsewhere, sales grew most notably in the electronics market, where our polymers are used in semiconductors and also grew in our Life Solutions sector where our polymers are used in pharmaceutical packaging and hemodialysis.

On the PVDF market dynamics. Can you maybe indicate how far the destocking has gone at the customer level? And also what’s that destocking trend has maybe caused to pricing dynamics in the market? I know you have different technology in the mainstream and you’re in the high rents, but can you maybe also elaborate on the pricing dynamics for your products and the market overall in PVDF?

There has been a destocking which will continue probably to quarter 2 as well in general, in batteries in automotive. But as you’ve seen, frankly, and I will come back to batteries, our business is not only PVDF battery, right? I mean you’ve seen Specialty Polymer really doing well, including in other applications in auto under the hood, right? So we’re in business of lightweighting, electrification, but please do not forget lightweighting.

On PVDF, yes, there has been a destocking on EV batteries and you’ve seen it in many other publications. We expect it again to continue in over quarter 2 this year. On the differences, and I think we’ve tried to do some education on emissions versus suspension, Karim alluded to that again. There are 2 types of PVDF technologies for EV battery suspension emulsion. No one material is inherently better or worse than the other, but we produce both. But the reality is that suspension-grade PVDF in which Solvay is the world leader, has a set of properties that make it better suited for nickel-rich high-energy density cathode like in lithium-ion batteries and specifically with NMC, which is the high-end batteries in the market, right?

So the suspension is the reference binder material in the production of those NMC material. There is basically no emulsion PVDF used in NMC today. I know people are still trying to get there, but this is mainly suspension. And the emulsion PVDF, it’s commercial products available worldwide with Chinese competition. We expect that to be more commoditized in the midterm and with very little again and no significant penetration in the high end in NMC.

So what has happened, I think, for us, obviously, there is a raw material cost decrease. For us, we just kept our margin constant and even as compared to the end of last year. So without giving you that much number and sensitive competitive information, our Q1 PVDF battery margins have been stable compared to the end of last year.

So I think that’s the message that’s how we ask our team to fight for value pricing on PVDF. So we are more resilient than the other technologies. And definitely, we like our – the investments we are doing in Europe and in the U.S. in the suspension because the barrier to entry for imports, for example, from China, like in the United States of America are pretty higher. The tariffs are high, more than 30%. So all of this makes our strategy very sound for future growth CapEx.

I think the volumes, and I talked about the destocking right on the PVDF side. And we are more resilient than others because, again, our Specialty Polymer portfolio generally is not only automotive, by the way – is only one sector that in automotive, is not only batteries. So I think the diversification which investors do like in the Specialty Polymers is really a good thing. We had many markets with Materials delivering volume growth with only batteries down. So in Specialty Polymers, we have a new fab equipment supported growth for our polymers using electronics. We also delivered volume growth, for example, in health care applications, such as pharma packaging.

Something important to note is while polymer demand for EV batteries was low due to destocking. Again, the polymers auto and non batteries grew in the quarter under-the-hood application. .

So the pricing level versus last year, the business has demonstrated its ability to maintain higher pricing which was the main driver of the growth. So that’s value pricing. I’m not going to repeat my favorite case and story of replaced metal under-the-hood.

Customers, they come to us when they have many ends, like they need chemical resistance, bridging resistance, et cetera. So as many ends needed they come to us. So that makes us very differentiated. And even, by the way, when you look at our batteries products, right. In the destocking, we kept the margins, right. The percentage sales – the EBITDA margins for those products or gross margins for those products became stable.

So over time, we will continue value pricing our solution. While in some applications, we will get back pricing when raw materials are favorable, right? By the way, we did it somewhat in batteries because 142B, for example, as the raw material prices for those who are – they know the Level 2 or 3 of the formula of batteries and PVDF we gave away, but we protected our margins, right? We sustained margins when – even when the batteries volume and destocking is happening.

And longer term, we have Speciality margins here. That’s what we are talking about. And we will look for more profitable volumes because given lightweight and electrification, we will continue penetrating with those technologies, like in composite, whatever the market that. So it’s value pricing, right, not value based on cost plus, right, or cost plus? And I think that’s what you can expect from us in the specialties and in Specialty polymers, specifically.

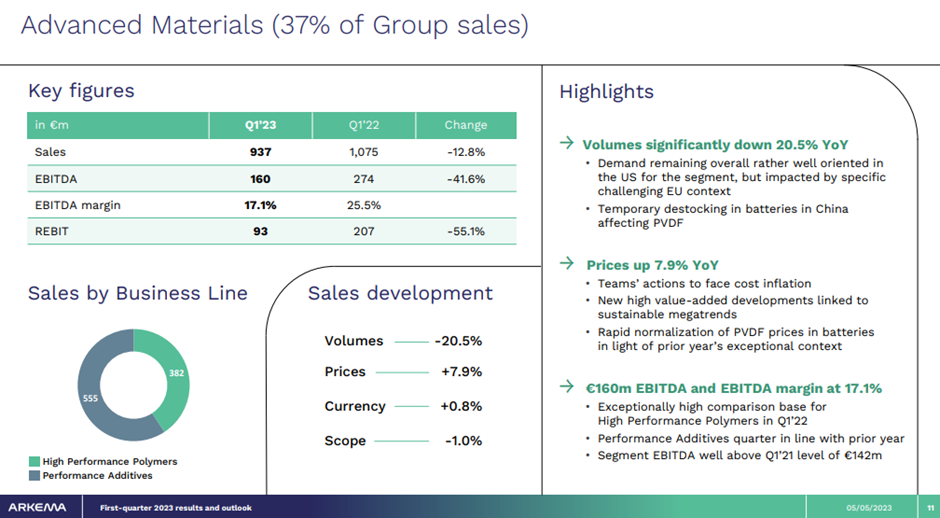

Arkema Q1CY23 Concall Snippets

Advance Materials (Fluoropolymer) Business

Our volumes were lower year-on-year due to poor demand in Europe, slowdown in construction in the U.S. and significant destocking in batteries chain, temporary but significant in China, which impacted PVDF.

Excluding PVDF volume in China are pretty much in line with last year level for our Specialty Market’s Materials against a rather low comparison base.

The 20% volume decline in materials looks like something you perhaps would have seen at the depths of the financial crisis. I appreciate you’ve got a diverse portfolio going into lots of applications and markets, but can you just elaborate a little bit on why the volumes are so bad? And I think in your introductory comments, you did mention some impact of strikes in France. Is it possible to isolate perhaps what the impact of that was within the volumes?

On the first front, I would say strikes is incremental, but we would say in this kind of environment, even incremental could cost EBITDA. So this is why we mentioned it, but we did not mention it as a broad topic, but I think in our transparency, it was important to mention it. But I would say it’s quite an incremental number inside the 20%. So I would not make it a big topic at your level. No, the 20% is mostly coming from destocking. This means that it’s not reflecting the true GDP.

It’s clear that it takes time and I agree that the numbers are big, not only for us, but for other peers, which are positioned in the same end market. And – which my interpretation beyond the macro that you know – as we know, is that after the COVID, after the tension on the raw material side, which happened in the first half last year and in the end of '21 and also on the transportation limitation, a lot of stock has been built along certain value chain. We still need to be digested. This is my explanation. As you have a long history in this industry, that you have so long destocking. So you have to put that in the context of the post-COVID and also this element, which creates a supply chain disruption last year and the year before the last. And we are still to a certain extent being impacted with that on top of the macro, so we have the double paying.

Now, as you know, we have seen different situation in the past. We are – we work on our self-help. We are patient. At the end, it will change. I think the good news is that if you look at the kind of EBITDA, we have been able to deliver with this low volume as the end is solid, but I agree with you. There is some frustration there because normally, you don’t get hit by so little volume for such a long period. Now it will come back and maybe there will be in the second half, restocking that will also support delivering the result on the full year. So you know me, we work on – we don’t compliant. We work and we believe that it will come back. We have just to be patient.

We are not losing market share, So it’s really the end market. Maybe they have been helping us well in the past 2 years. So we have some counter back, but no specific answer beyond stopping and also macro, which is not overall supportive currently. But – so this is why we really work very strongly on the short term, mitigating the impact, but we continue to invest in the long run, which is part of your second question because we believe that at the end, it will come back and sustainability, at least for the one we are well positioned and Arkema is one of them will be really a key driver of growth for the coming years.

And the second question is really on PVDF. Could you just tell us like fundamentally, if you have the technology to make suspension-grade PVDF. And if so, you could actually compete at the highest end, if possible? Or is it that you guys have a genuine technological gap with one of your listed peers?

With regard – I don’t want to enter too much in the detail of the PVDF, but I will make a couple of comments. First of all, PVDF, you have different technologies. Some are better for certain applications and some are better for other applications. So I don’t think that there is only one by far. And even in batteries, for certain applications, suspension is better, for other emulsion better.

With regard to Arkema, as everybody know now because it was communicated by one of our competitors, we are a company, which is – which has been focused on the emission. And I think we are glad about it. We are very strong in that. Can we make suspension not now because of tools, we’ll be able to make suspension in the midterm. The answer is yes. Do we have beyond what we are making today, evolution of our products, including emission, which will address the market in batteries for different applications, new generation, et cetera? The answer is yes. Is PVDF sufficient to address the battery market? The answer is no. You need to have other technologies and other technologies? The answer is also yes. So I think we have plenty of cards to play. You have not one a company, which is positioned like the other was. This is the beauty of this incredible – incredibly growing market. I think we have a position with some very strong strengths and some weaknesses the sale for our competitors, but we have really enough to be the fantastic story. So don’t worry about that.