Listening to this call is not only about Gland doing very well and much brighter future ahead, it also brings in key characteristics of a leader and puts all the noises around RM cost and inputs cost pressure to rest - this is what separates men from boys IMO, part 51:45 onwards for Q&A by ASK folks is superb - operator didn’t intervene and this is sheer 10 minutes free flow non typical ones

Inferences

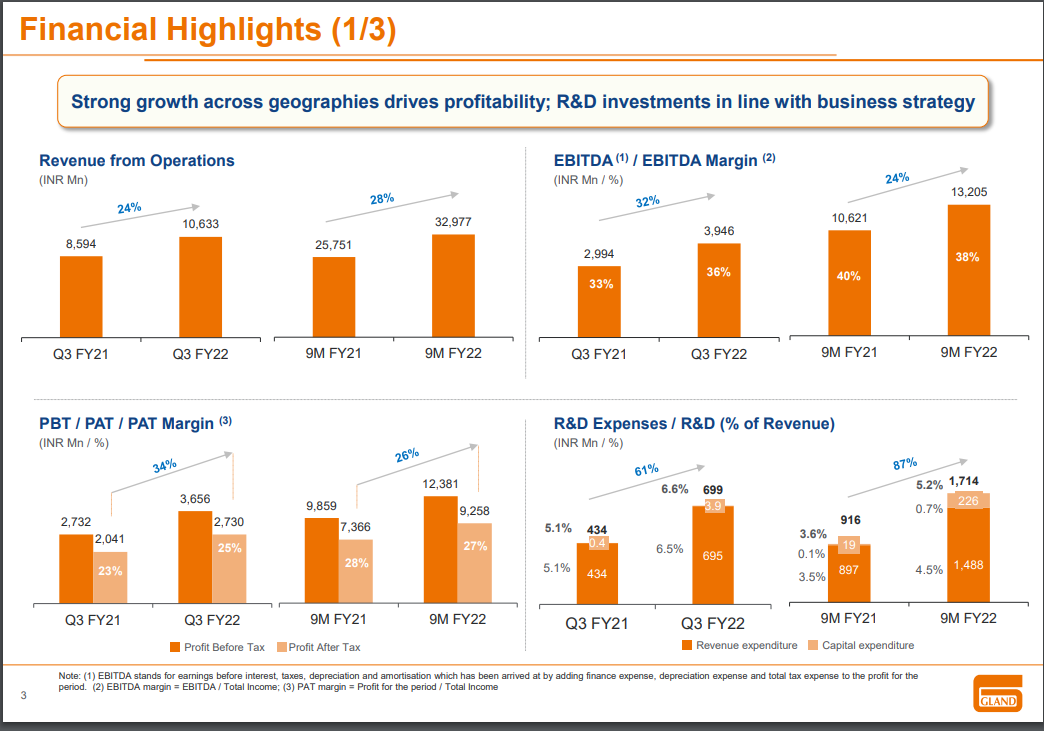

- Cost pressure - what cost pressure? We have enough levers to handle gross margin squeeze to cushion from reaching to EBDITA levels. How do they do it? Answer lies in the operating model and product mix - they work on three models - CDMO, Tech transfer and own license - CDMO is 100% GM vs license is where RM hit comes - even where RM hit comes we handle it with scale and operating leverage as B2B mfg. Logistics cost could hurt but that’s less than 1% at EBDITA level and it’s behind us with situations normalizing.

Net net they are confident of current EBDITA levels sustainability around 37-38%.

Key learning - it’s the operating model that makes one immune to risks where some players struggle and some excel under all circumstances

-

Often asked questions around competetion coming in Injectable space with more Indian players setting up the plant - Gland response - this is actually good for us - we can out license some of our work to them( one of their three model is own Licensed products) - again beauty of their operating model where industry disruption actually works to their advantage. They are well ahead in curve on next 5 years demand and have anticipated this coming in.

-

Future growth trajectory from filings - current commerlized molecules mkt scope is $7.5, already approved and awaiting approval is $7.5B - this second part is play for next 3-4 years itself, incremental opportunity is equal to their current size. This does not include biosimilar.

-

Sputnik twist and risks - while they have supplied batches for lite( single dose) as well as two doses batches as well - awaiting on results - per them commercialization at even a fraction of 250M contarct size covers the investment cost, plus it has fast forwarded the biosimilar CDMO foray that ws 2 years out per original plans, now they have infra+ tech + trained team to make it happen - and Biosimilars CDMO is currently $15B opportunity growing at 15% CAGR. There is no penalty clause in contract either.

-

Current capacities and utilization at consol is around 65% - have assets to support future growth- imagine operating leverage kick if this were to go up further- but believe they will contnue aggressive expansion

-

CFO to EBDITA- currently lower from historic levels, driven by working capital, higher Receivables days in New relationships in RoW markets and inventory for new launches - it will improve towards second half but tone suggested that aggressive growth requires some balancing till new relationships mature( read RoW expansion rates)

-

China opportunity- total 9 filings done, should materialize soon, return ratios and margins are better than current profile.

-

Current fixed asset turnover ratios are 2.5X, have room to go up in near future, they work with IRR of 20% and above internally on all investments

-

Covid share in current quarter is negligible be it India or exports - no worries is sustainability of growth and margins

All in all one of the good calls in Pharma gloom perceptions,

Invested

Extract from Emkay (Management Commentary )

The company has onboarded Fresenius Kabi for Enoxaparin and added a couple of partners for penems RoW is expected to grow faster than US Strong growth visibility is fueling capex, with a total planned capex of 800 crore in FY22 and FY23.

Biologics foray makes the company future ready: Biologics CDMO market is growing at a 13-15% CAGR with limited growth in capacities. The company remains upbeat about utilizing its initial capacity of 10KL in collaboration with Fosun’s subsidiary Shanghai Henlius, which has 19 biosimilars under development. A manufacturing contract for 2-3 biosimilars is expected in the next 12-18 months. The company is already planning for a 50KL capacity expansion. The operating margin in this business is expected to be in mid-thirties.

- Business model benefit

Gland Pharma will benefit from higher volumes in existing products. Apart from some existing Indian players such as DRL and Lupin, new entrants in the injectables space such as Alembic are also becoming Gland Pharma’s customers. The sheer focus on the injectables business helps the company maintain cost leadership through economies of scale and operational efficiencies. For example, Gland Pharma has the flexibility to choose a high-capacity or low-capacity line based on demand in order to keep the production cost minimum. Small injectable players do not have this flexibility.

Enoxaparin is a good example of how volume in existing therapies grows. The market size of ENoxaparing in the US is ~US$250mn. Current partner Apotex has a ~5% market share and Kabi has ~15%. So, with the Kabi contract coming to Gland, volumes are roughly going to triple. Moreover, the company now has an end-to-end supply chain starting from Crude heparin to Enoxaparin. While Gland’s competitor Nanjing King Friend (NPF) has relatively lower production costs due to its backward integration into a slaughter house, NKF’s direct selling through its front-end arm Meitheal limits its ability to onboard other B2C players and helps Gland Pharma.

Another example of volume growth in existing products is Penems. The company had set up the penem facility with a gross block of 700-720mn with 2 Lyophilizers. However, the company has onboarded two more B2C partners and secured orders for the next two years. It might also need to add Lyophilizers.

- US business

The company expects a mid to high-teens CAGR in the near term. Half of growth will be driven by new product launches and the other half by volume and pricing growth in the existing products. Historically, pricing growth for the company in the US has been in low single digits.

- Complex injectables

The company is working on 15 products of the total 40-45 complex injectables universe. Initially, the company will file four products in FY23, with a total addressable market size of ~US$850mn. These are hormones and suspension products. The company is investing in setting up capacity for hormones, suspension and microsphere tech. Assuming a 30-50% price erosion and a 10-15% market share in each products will be a good start. However, one needs to factor in that Gland is a B2B supplier, so the addressable market needs to be discounted by 30-40%. The remaining 11 projects have an addressable market size of US$9-10bn. This will include some peptides as well. Apart from inhouse development of complex injectables, the company is also evaluating a couple of M&A opportunities.

- RoW business

New markets, such as Saudi Arabia, have opened up for the company due to Covid. The company remains selective about product launches in RoW. It can flood the market, but it is not doing so to maintain profitability. Given that the company produces the products in the same facility as US, the cost of production is higher vs. producing them in a separate facility. The company is actively planning to enter the Africa market with the help of parent Fosun Pharma. Overall, the CAGR is expected to be in the range of forties. Pricing in some RoW geographies is lower, but sustaining a 36-38% margin is not an issue, thanks to opex leverage

- China injectables market

China’s generic injectables market offers a large addressable market, second only to the US market. The company has set up a separate team for China. It expects revenue from China to be 8-10% of total revenue by FY25E. China margin would be similar to overall margin as product selection is key here and the company has selected products with limited competition. A couple of products require production from the Chinese facility where the company has done tech transfer to Fosun and taken exhibit batches.

- API backward integration

The company’s current backward integration into API stands at ~30%. It only focuses on APIs, which are low volume and critical. It never focuses on high-volume APIs where oral formulation is also available. The company derives 30% of its revenue from Anti-infective but doesn’t have fermentation capability, and hence not backward integrated. The company is looking to acquire a fermentation plant in China or Europe, as those are more suitable for fermentation. This is expected to boost profitability of these products further.

- Capacity utilization and Capex

Current total capacity utilization is ~60%. However, format-wise capacity utilization may vary. For example, Lyophillizers are at 80% utilization, while the Ampoules line is utilized only 30%.

The company has budgeted a total capex of ~Rs8bn in FY22 and FY23. Of this, the company has already spent ~Rs3bn capex on setting up a 10KL biologics facility. The remaining Rs5bn will be spent on the generic injectables business, which will make the company good on the capacity front for the next 2-3 years. This capex includes 1) set-up of lines for hormones, suspension and microsphere, 2) additional investments in Lyophilizer in Penem facility, and 2) increase in API capacity. Capex for an additional 50KL biologics capacity will be over and above the budgeted spend.

I am presently invested in ‘Gland’ from IPO stage.

Even though company is fundamentally strong and performance in key parameters like Revenue and earnings growth is consistent; valuations seem to be on a higher side because of following reasons.

- Company is in generic space and higher margins may not be sustainable over medium to long term.

- The companies plans to venture into Bio-similars, will not add much of pricing powers and soon becomes commoditized space.

- Too much dependency on parent (Fosun pharma) for venturing into Bio-similars & may not materialize as high margin business segment if they act as backward integration to ‘Henlius’ products and services.

My first reply here, will improve going forward!

Thanks

Anand

Then what is keeping you invested ?

-

Sputnik lite Vaccine success may boost prospects (at least the perception about company) in short to medium term!

-

Expected (Approved ANDA) product launches in few months may give clarity on their future margins profile.

-

If any good M&A activity which can be a bonus!

Please do guide if I need to course correct.

https://asia.nikkei.com/static/vdata/infographics/chinavaccine-2/

“Or consider Fosun Pharma, one of the biggest drugmakers in China. In March 2020 it partnered with BioNTech, the German company that co-developed an mRNA jab with Pfizer, to advance the development and commercialization of the vaccine in China.”

Does Gland report the B2B revenue split between IP led, Tech transfer and CMO?

Yes indeed they have continued their good run with numbers.

But, the key monitorable was Vaccine and biosimilar opportunities.

Good to see; finally they are about to start manufacturing. (With delay of few months for sure)

As per the commentary, they have received NOC for the facilities and final license is process formality.

Which definitely opening new doors of opportunity.

Negative is, they are still continuing their look for acquisition opportunity in bio-CDMO. Which they are doing from last 3 quarters. Nothing concrete happening.

China opportunity is also being dragged in similar lines, may be china approvals will also take long times, like in india. Or they may not do it! geo politics? ![]()

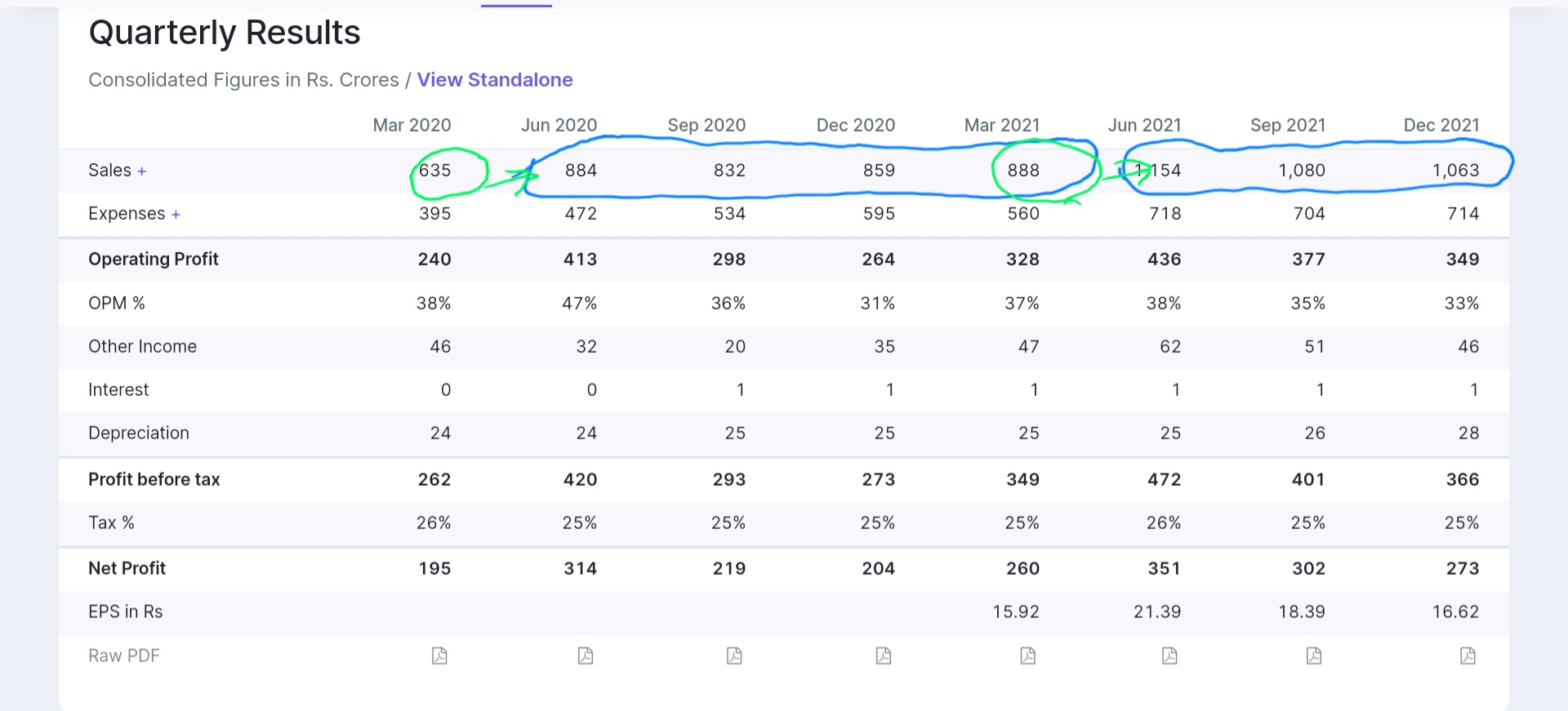

Gland numbers seem to show an interesting pattern

March to June is a sizable bump up, both in FY 21 and FY 22 and rest of year is kinda flat on QoQ for remaining quarters. Ofcourse limited data and Covid periods included.

One possibility on above pattern

- Meaningful Lanuchs concentrated in early part of year, for example. Q3 22 also they filed more Anda/dmf than they did in Q1+Q2 Together. Which will get approvals in 6 mo+. Not a fully convincing explanation but happy to hear others tracking it.

- Clear pattern of core markets contribution declining in overall pie and RoW increasing - inline to their long term ambitions of 60:40 - quick thought would be that this will dilute margins - not the case because they being B2B - capacity utilization matters more than gross margins to get similar EBDITA, RoW engine provides that lever.

- Competetitive landscape on Injectable- FY 23 will see lot of Indian players see capacity coming online, mgmt response was clear that we have 300+ approval, new players will take lot of time to build a meaningful approval base. Infact Gland can use their capacity as well ( assume they have good order backlog and chose to outsource some)

Growth areas-

- Complex Injectable - filing for four complex Injectable, seems lengthy and complex process and took them time higher than anticipated.

- Biosimilar CDMO as next growth engine - lot hinges on it, mgmt seem to be looking at development for now, no commercialization ready molecules. Going to be lumpy.

- Sputnik - Gland is ready but Gamelia and country specific production approval needed to start mfg - Q1 23 probably given didn’t sound sense of urgency yet.

- Capex of approx 500 cr by end of year - at historical 3X assets turn could add 1500 cr next year

- Peptide Foray - some APIs internal, mostly outsourced, looking at acquisition

Key monitorable

- Fosun related biz on biosimilar not materialized yet, delaying biosimilar ambitions

- RoW push shows developed mkt saturation in their approved 300+ molecules, new launch universe in Developed mkt may slow down growth

- Capabilty gaps to be filled on longer term growth drivers- biosimilar, Vaccine, complex Injectable, peptide etc.

- Competetion catching up faster than anticipated in Injectable and pricing erosion

- Being a B2B player - operating leverage is key, have delivered so far well. Smartly using RoW space to achieve it.

Valuations seem rich given upcoming competetion in generic Injectable and required capability built up around future growth areas being work in progress, will market start factoring transition risks to new era? As it is Pharma sector seems out of favor with stalwarts like Divis etc comfortably breaking key support levels. Gland key support levels being around 3400. Though long term story seems intact as long as they successfully transition to Futuristic bio tech landscape.

Invested

- China

About 5 molecules ( I am yet to listen to the concall but based on previous commentary ) in China, after USA china is the biggest market size wise, Fosun always enjoyed big pie in China government contracts. For me this is the key trigger.

One risk is CFO , it looks very much stretched along with high receivable days , this is mainly due to non regulated markets, management said that is the nature of these markets.

In my opinion they will grow even stronger in rest of the world markets in future due to the kind of complex product basket that they have.

Regarding competition from other players, there are plenty of reports that says there is huge shortage in injectables segment all over the world. I don’t think the reason not because of supply, could be because of complexity to manufacture generic injectables.

The Gland has an advantage of strong FDA compliance, technical know how along with state of the art facilities.

Bio - Gestation period is very very high, just to manufacture one vaccine ( they were supposed to manufacture the initial Sputnik version but now they have settled with Sptunik light ) it took almost two years (yet to commercialize )

Acquisitions : This is the space we have to watch out for

There is one listed player ( I forgot the name ) who does contract manufacturing for Gland.

- They are yet to share wealth with investors in the form of dividend. They have huge cash on the books

This is because some order of row is via tender. This is year on yr process. Co expects some win in April this yr.

Source: Con call…

Needs subscription to read full article

Market is waiting to hear some triggers from almost 6 months! Will be interesting to hear some positive progress in key triggers like,

- Product approval in china

- vaccine exports

- Progress on Bio facility acquisition.

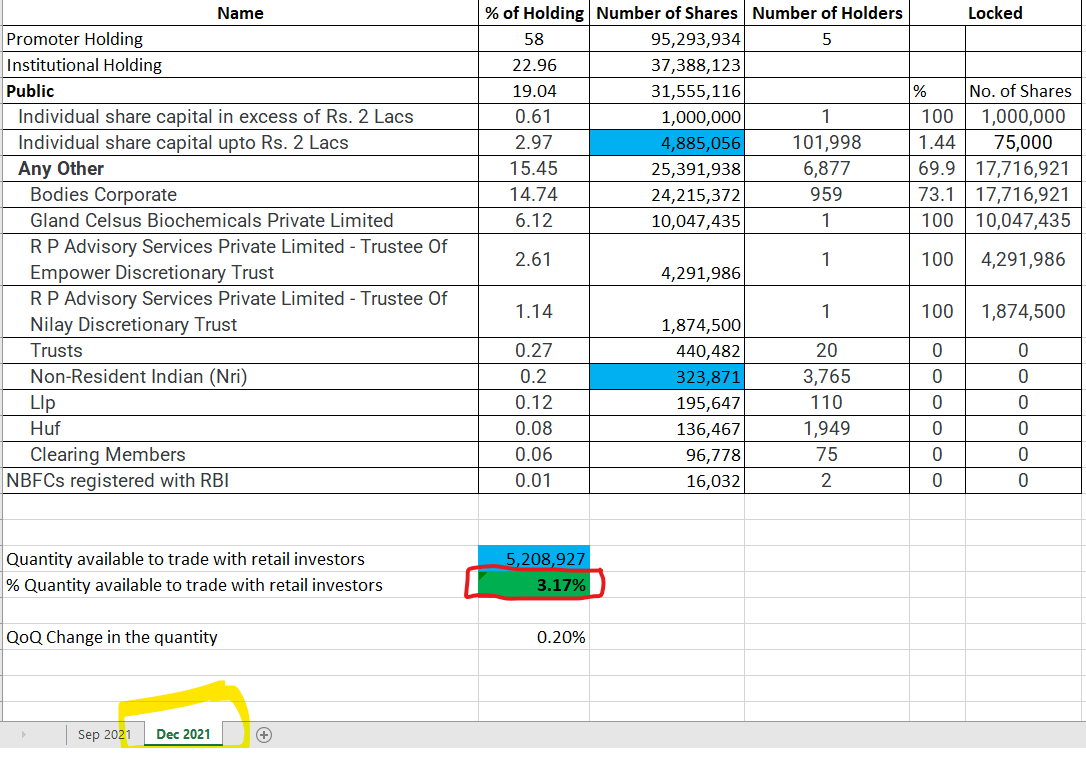

Interesting to watch, who bought stakes in block deals accounting 66,70,910 shares or 4.06% of stake!

It is huge🧐

Citigroup was book running partner!

We don’t hear much news about them other than in quarterly con calls and AGMs.