5 Likes

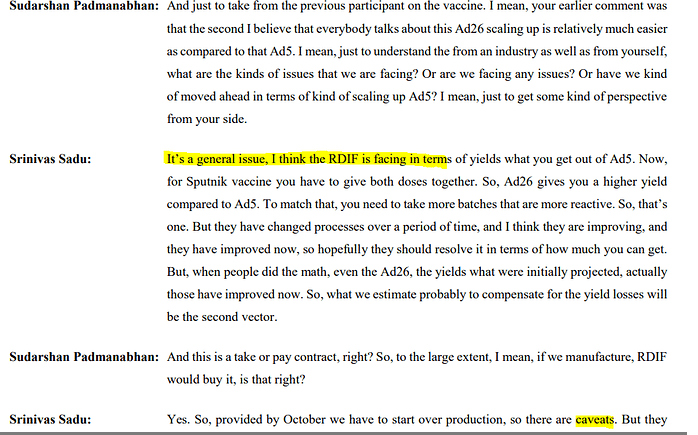

A good article on why it is so difficult to make adenovirus vector (Sputnik is based on this ) vaccines.

2 Likes

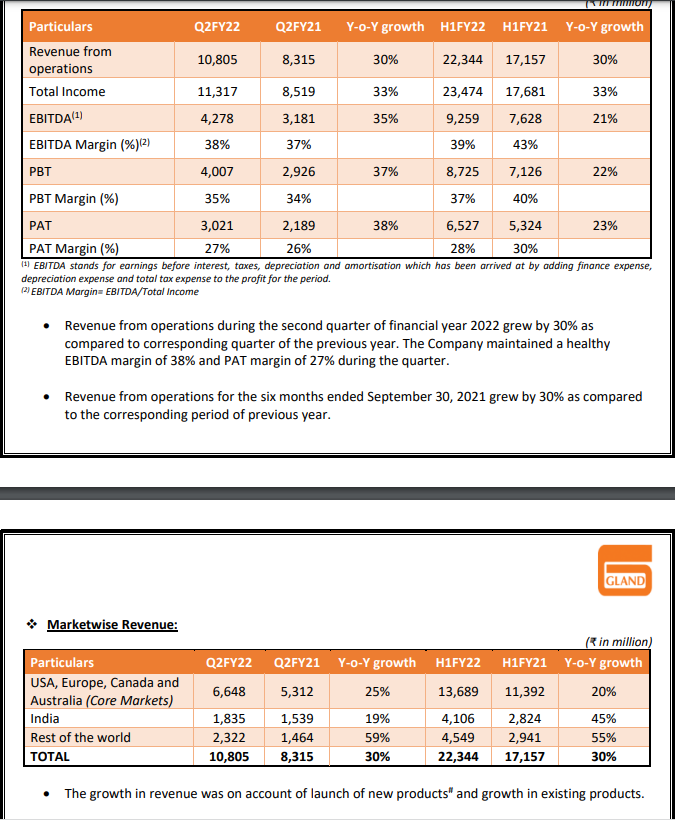

Zydus partners with CHEMI of Italy to launch Enoxaparin Sodium Injection in the United States. This is the beginning and I still maintain this space will get crowded and there can be price erosion in the coming years. I think major revenue and profits of Gland is coming from this space

1 Like

GOOD REPORT

1 Like

Tell alot about Aurobindo vs gland B2c vs B2B model

3 Likes

Gland Pharma AGM

Management Guidance

Biologics / Biosimilar

The biologics market is currently about USD 300 Bn in size, within which the biologics CDMO market is estimated at nearly USD 13 Bn, growing at a CAGR of 15% over last 5 years. The manufacturing of biopharmaceutical is complex and difficult to be transferred, requires higher investments. There are 80+ biological drugs which are going to lose exclusivity in the US and EU over 2021-25. Europe and the US still account for the majority of CDMOs market due to their vast experience and excellent R&D capabilities. The developing markets have seen companies build these capabilities, which is becoming a new engine for the growth of global biopharmaceutical CDMO industry. But the market is still at a nascent stage and very fragmented, leaving the field still wide open for new entrants to make a mark in the industry. The support we receive from our parent, Fosun Pharma, by virtue of them already having immense experience in biologics, will help us to accelerate

ramp-up. I believe this business diversification by entry in to a new class of molecules, is well aligned with our existing business and helps us leverage our strengths to open up avenues of growth.

Focus Areas

I have outlined four broad

focus areas for our teams to align strategic initiatives internally.

1.) Re-grouping and Consolidation by transferring and sharing of resources, expertise and assets across all manufacturing locations. This will enable us to operate a lean, flexible and effective organisation.

2.) Diversification of Product Portfolio, which implies investments to be made into technologies and R&D that drive portfolio expansion

3.) Streamlining of our Human Capital, avoid redundancies, support employees with all tools and skill trainings to be able to adapt and perform in this changing market environment

4.) Effective and Efficient Manufacturing, to ensure we don’t lose out on our key strength of high quality manufacturing at affordable price, as we continue to scale our manufacturing and build new capabilities. Always be agile to look for ways to achieve operational excellence in not just the new products but more on the life cycle management of the existing products.

Highlights of AGM

Number of employees 3,950 - Average age of employee is 33 years (young generation)

13% Women

96 Shareholders hold more than 1% with this there is only 6% float with small investors

Q&A Session

Competition

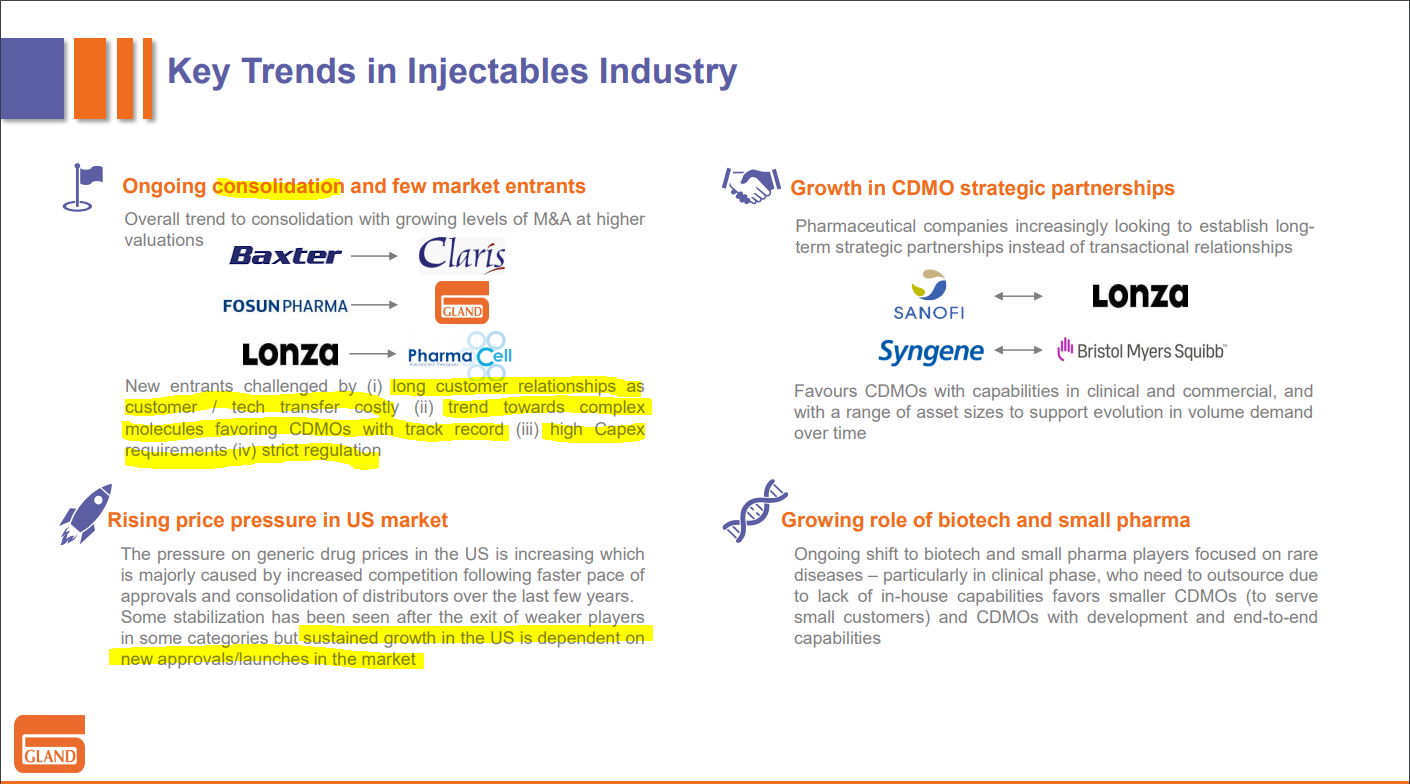

This increase in the competition what you are seeing this trend has been going on for some years now and we have been able to continue our growth path, despite competition. Over the years if you see we have gained immense experience of manufacturing sterile injectables at large scale, which is not easily replicable given the complexities in quality management. Our portfolio now spreads across diverse therapeutic areas and it helps us differentiate amongst upcoming competition and our business model also is unique and is a key attribute for our success. By focusing on B2B business, we are able to aggregate demand from multiple customers, resulting in benefits from economies of scale which is key in injectable manufacturing as a fixed cost for majority of cost overheads. So, I think we are covered in terms of competition and competition is a part of our business anyway.

M&A opportunities

The strategic and M&A forms part of our business strategy, I have also mentioned in my initial speech, as mentioned earlier in the speech, we have outlined areas that help us in building niche product capabilities on the both the API and formulation front and it also help us achieve backward integration of critical products and gain geographical traction. We have evaluated multiple opportunities but we do not want to compromise on two key aspects, culture and quality, we are committed to ensure we build shareholder value, through any acquisition which we do. In terms of valuation, yes there are assets available but at high valuations, so we have to balance between how much we pay and how much we gain and it has to fit into our strategic goal.

Complex Injectables

Gland has a portfolio of complex injectables as part of the R&D pipeline, if you look at complex portfolio there are almost 35-40 products, we have already started working on portfolio in products and we are filing about 4 products end of this year or beginning of next year. Typically, it takes about a couple of years to commercialise since filing but this is subject to receiving approvals, we are also evaluating opportunities to acquire products in this space to reduce go to market time for some of the technologies which we do not have in house capabilities.

CAPEX

We are expanding our

capacities in Pashamylaram facility in Hyderabad, where we are adding new lines. To scale up the backward integration as well we are expanding our API capacity at Vizag facility, where we are adding a new block and there is a new R&D facility coming up at Pashamylaram. Overall, on the CAPEX plan for FY’22-23 we would be spending about Rs. 800 crore and out of that about Rs. 300 crore would be on the new biotech vaccine facility.

R&D

( 3.5% R&D is less ? )

GLAND is B2B model business, so basically compared to a B2C company actually our R&D is also shared by our partners because they also have rights to market, so that is why it looks little lower than other companies but this is in line with other B2B companies and because our base is increasing and we are growing at a faster rate, so 3.5-4% is normal rate which we are thinking will be there even moving forward.

CDMO opportunity from the Innovator companies

We are looking at getting into this space, we are working with innovator companies on the CDMO side. USFDA inspection last time it happened in 2019, there is no recent inspection still, so I think they have started to comeback later part of this year, so as of now I think we do not have any dates from them for audit.

11 Likes

This reduces the concern of price erosion in injectables. good.

3 Likes

Good to see the AGM transcript being published. I am really impressed by the transparency of this company. Even the Annual Report is far more transparent and informative than most other companies. For example, granular details of manufacturing facilities, production capabilities, number of lines & quantity for each, regulatory approvals etc. are given which you don’t get to see elsewhere. IMHO, willingness to share information shows the management has a high degree of confidence in what they are doing and respect for minority shareholders as well.

6 Likes

it seems panacea biotech solved the 2nd vector puzzle for everybody else including Gland

2 Likes

I dont think so, the message says second component AD26 which is relatively easy but the complex one is AD5 .

Check the update from the Gland concall. (Correct if I am wrong )

Vaccine is two shots AD5 + AD26 , not sure what they are trying to convey by saying they shipped

2 Likes

AD 5 is Vector II Which is complex to make as per Gland concall. You can read here that 2nd vector is AD5 was supplied by panacea . https://www.moneycontrol.com/news/business/stocks/panacea-biotec-share-price-jumps-10-on-shipment-of-sputnik-v-vaccine-7439481.html so i think the matter is resolved ! let me know if any divergence is still there

““Panacea Biotec is pleased to have successfully produced and dispatched the first batch of Component II (Ad5) of Sputnik V vaccine. More batches are currently under production at our manufacturing facility in Himachal Pradesh,” said Rajesh Jain, Managing Director of Panacea Biotec.”

3 Likes

The communication is not clear. Anyway, my assessment is that Sputnik dont have a chance in India to sell more quantities and abroad also I have my own doubts. I dont see much upside for any company because of Sputnik. This is my assessment but not supported by any data.

1 Like

Divi’s being a poster boy of India API CDMO, would be interesting to see how Gland stands being a B2B mfg in Pharma sector and identify common patterns

- Similar working capital days - 150 to 160 days

- Similar op margin profile

- Similar valuations ( PE or price to sales)

- Returns ratio in similar range - RoCE, RoE - upper quartile in sector

Note that Valuations are better off analyzed in a future looking manner, I.e. Q1 22 Annualized numbers as well as factor CWIP for FY23 onwards as both are on very sizable Capex spree( >50% of current Gross block over next 6- 8 Qtrs, Infact Divi’s have upped the Capex guidance in recent times outside current Expansion)

-

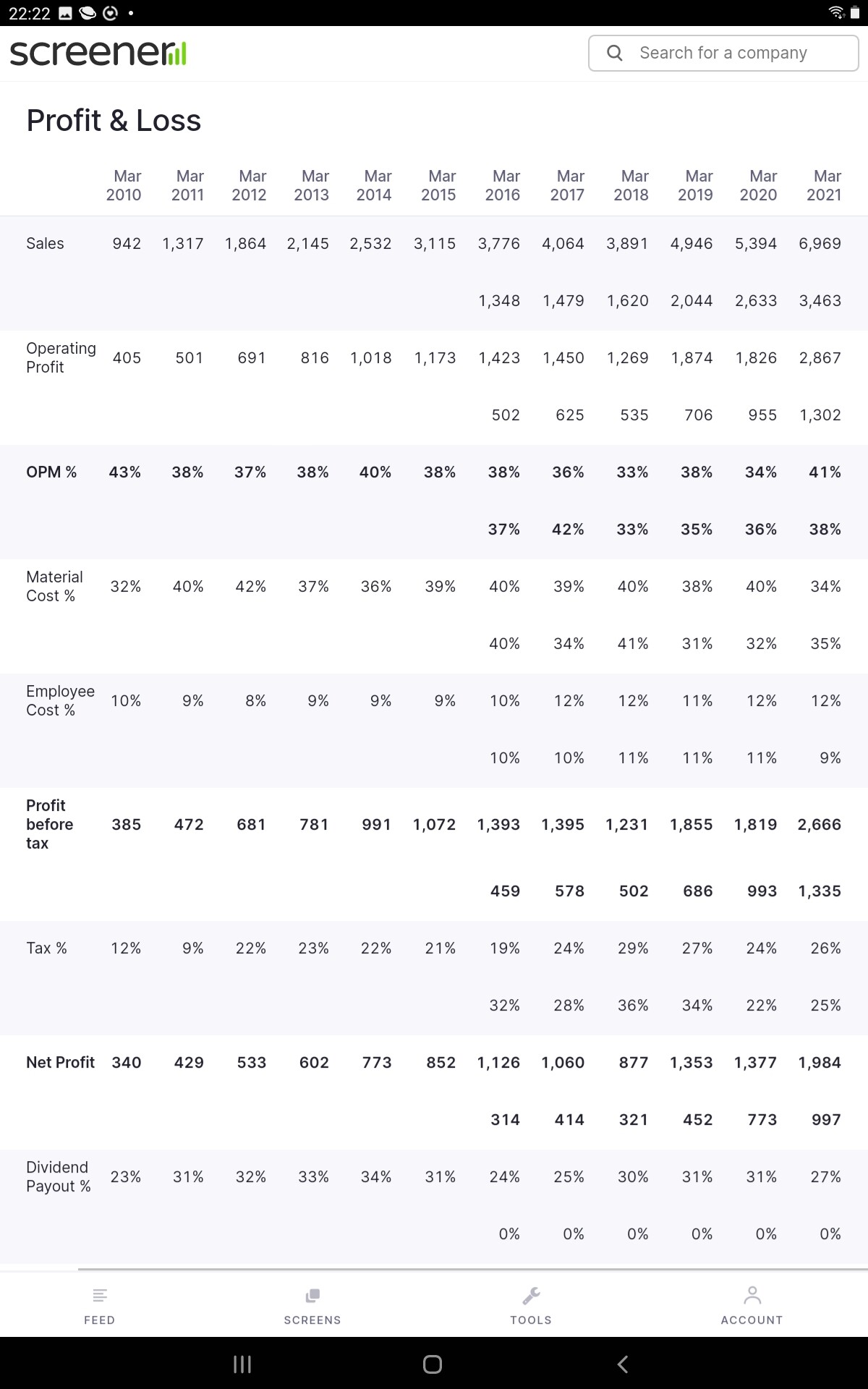

Growth - FY16 to FY21, where most of Pharma sector large caps have struggled to deliver growth- Divis has doubled revenue from 3700 cr to 7000 cr, Gland has almost tripled from 1300 cr to 3900 cr

-

Margins have been robust for both players and guidance is good as well (36 to 40% has been a trend over last many quarters/ years) - can they better it? With scale comes operating leverage for manufacturing setups and Divis is $1B+ and Gland $0.5B with 25-30% organic growth , cost leadership with volumes and backward integration- reasons to belive they have enough levers.

-

Both have clearly articulated next set of growth levers for near to med term in Annual Report 21( Geo expansion/products basket/RoW/ tech and process innovation/ cost leadership/ backward integration / scale benefits etc)

-

Both have a good compliance record, a key aspect in Pharma - infact Gland has been spotless that too in Sterile and Injectable space

Valuation both seems to be very well placed to grow at 20%+ growth, very sizable CWIP/Capex, Solid client credentials, compliance track record - came out with flying colors in FY21, Valuations need to be viewed in light with growth visibility and where future lies in over med term. ( for example Gland was called out expensive at 17X price to sales in July on some Twitter threads based on FY 21 numbers, but if one Annualized Q122 numbers it would come down to 14X, at FY22 they will be around 12 X, add CWIP factor and looks much more reasonable- all of it a high growth and margin thesis)

Invested in both from lower levels and Gland has good potential and visible patterns to be on a compounder trajectory as Divis has been. These two are by far be the largest and high growth India CDMO play now as well as potential to coninue to lead the sector in forseeable future.

Usual sector risk management and growth momentum is key.

9 Likes

1 Like

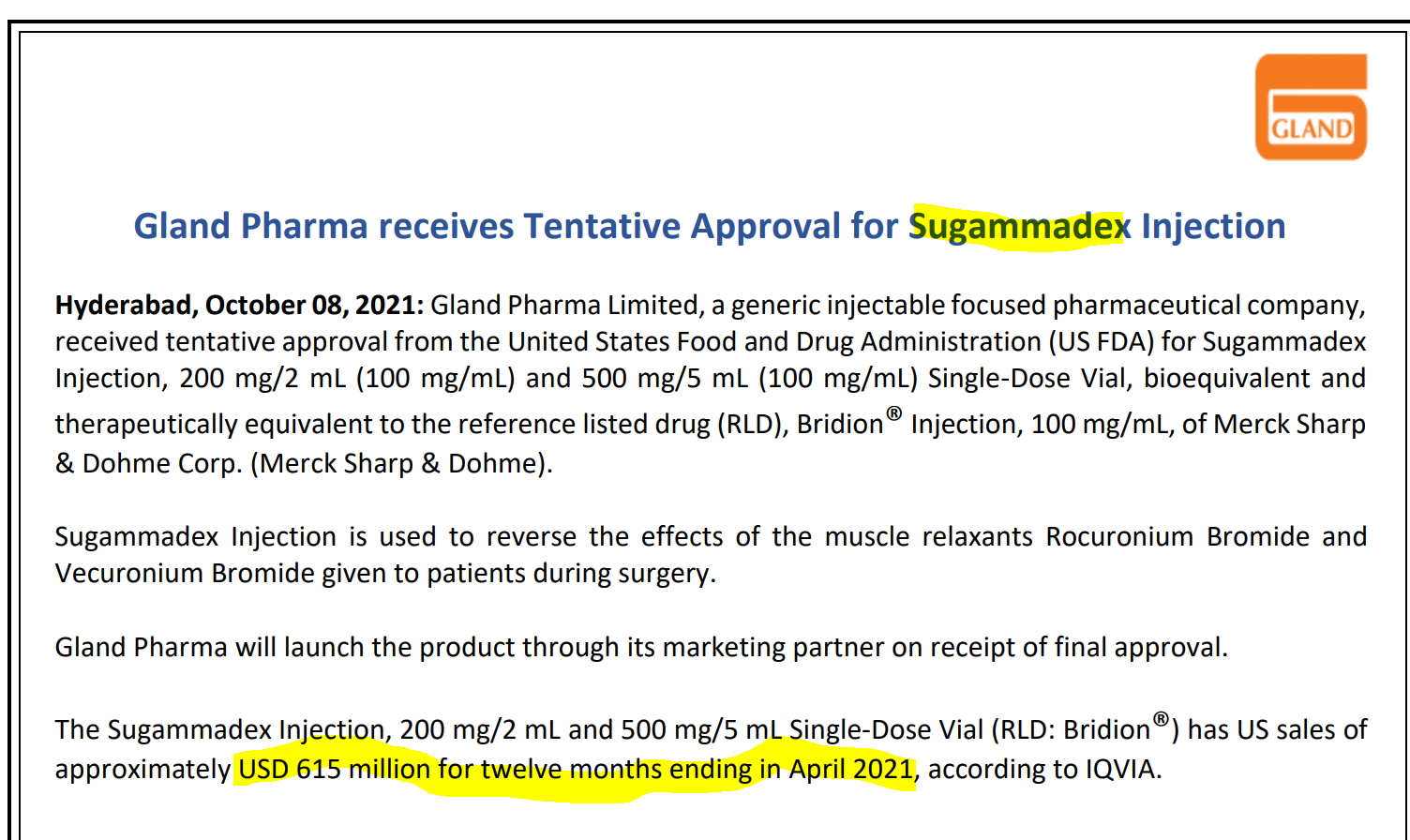

Does anyone know about other Generic manufacturers of this drug and if company can acquire a big share of this 650 million USD market?

1 Like

4 Likes