Commenting on the results, Mr. Srinivas Sadu, MD & CEO of Gland Pharma said “Our foray into

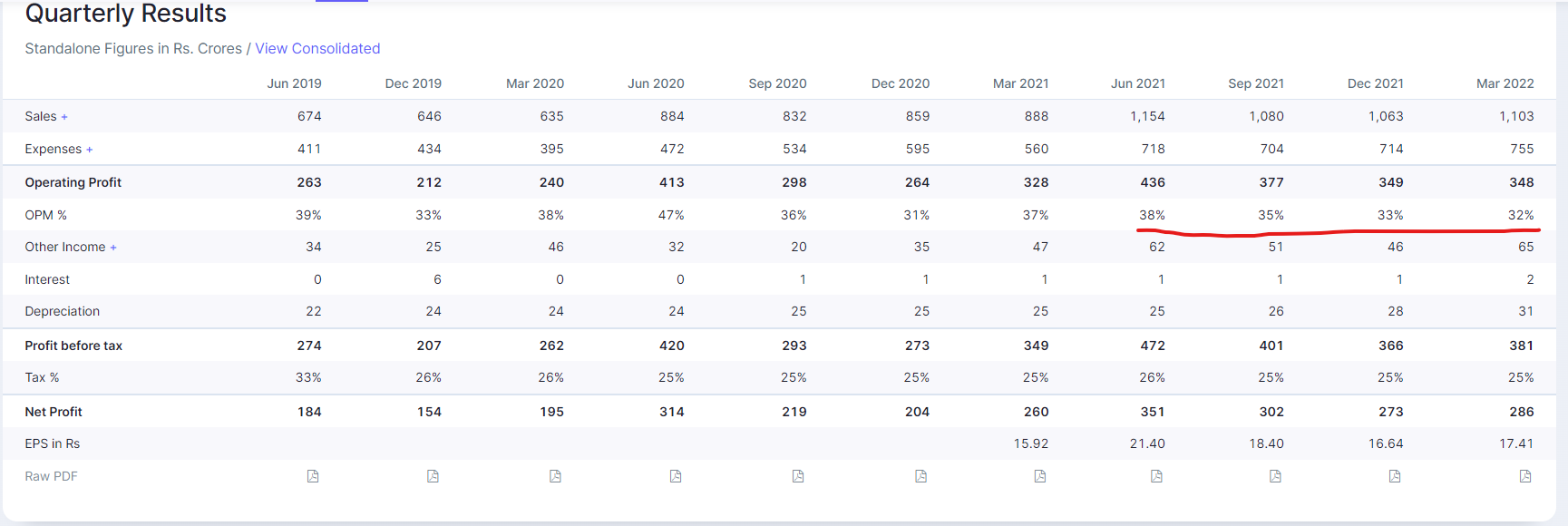

Biosimilar/Biologics CDMO business during FY22 was a key strategic initiative to transform Gland pharma into a full-fledged CDMO company both in Small and Large Molecules. It positions us for long-term growth and value creation for our stakeholders. We reported a strong revenue growth of 24% for Q4FY22 at ₹11,030 mn driven by growth across all geographies. On a full- year basis, we delivered revenue of ₹44,007 mn, a growth of 27% and reported a PAT growth of 22% at ₹12,117 mn with PAT margin at 26%. Our Gross R&D spend for the year of ₹2,273 mn is about 5.2% of revenue. Our investments in R&D are in line with our strategy to expand our product portfolio into complex injectables, we made 29 ANDA filings during the year up from 20 ANDA filings the previous year. We also started our new R&D centre to expand our development capabilities during the year.”

Research and Development:

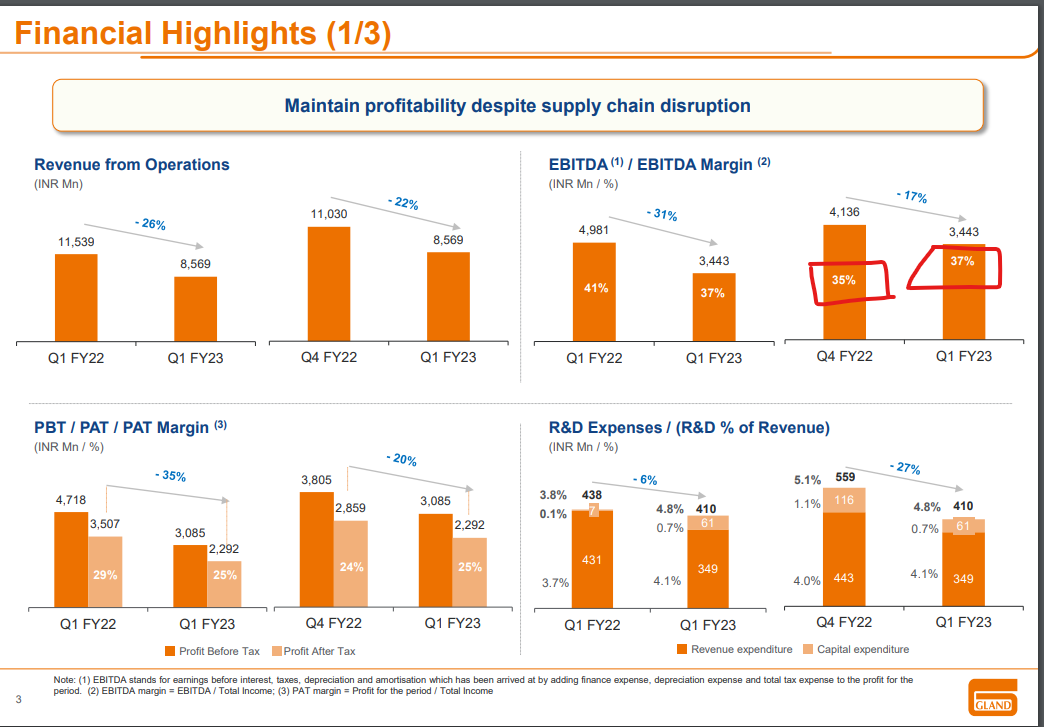

The total R&D expense for Q4FY22 was ₹559 million which is 5.1% of revenue and for FY22 the total R&D expense was ₹2,273 million which is 5.2% of revenue.

During the quarter ended March 31, 2022, the Company has filed 2 ANDAs, and received 3 ANDA

approvals. During financial year 2022, the Company has filed 29 ANDAs, 11 DMFs and received 19

ANDA approvals.

As on March 31, 2022, the Company along with its Partners have filed total 311 ANDAs, out of which

252 were approved and 59 are pending approval.

Capex:

Total Capex incurred during the quarter ended March 31, 2022 was ₹674 million. During the financial

year, the Company incurred Capex of ₹5,221 million.

My take on Management commentary and Results.

- Gland has maintained their consistency in sales growth, which is a good sign.

- The geographical diversification target is progressing well, which is clearly seen in ROW Qtr YoY Growth of : 32% & India business Qtr YoY Growth of: 137%

- Cost pressure due to RM & logistics have hurt EBIDTA/PAT considerably, As per management commentary vendor diversification still work in progress.

- US business growth may not return to normal levels in next quarter or two because of Syringe shortages and base effects.

- For next few quarters, growth depends purely on new launches in US, ROW & India. Also on getting low cost raw material supplier outside china for Enoxaparin.

- Management has not been able to onboard Biosimilar manufacturing opportunities independently, they are trying to start as backward integration to ‘Henlius’ products with fosun’s help. Still work in progress.

- No solid steps on M&A front too. still work in progress.

- Cash in the books going up, with good opportunities in terms of capacity expansion and M&A, Management is slow, hopefully can invest with good ROIIC. action to be closely monitored.

- Vaccine thing is not moving and it may not take off. Write offs/penalty clause to be closely monitored going forward.

- Utilization levels will be nil on investments made on vaccine facilities.

June quarter will be crucial, historically they had done well. Management execution will show whether they can sustain and grow.

Looks to be an Average execution by management; in terms of Bio similar CMOs, M&A and cost handling.

Disc: Invested

@Anand_Investor thanks

The journey continues…

What went wrong ?

-

Like Stelis all others including Gland have to write-off their spending on Sputnik. I will go through the transcript once it is available to understand more on this.

-

For the past 4-6 quarters they are talking about China opportunity, is there any further update ? This is the key trigger to watch for

What I am not comfortable with is; they are sitting on huge cash, I understand they are looking for value buys, but why they are not rewarding share holders with Dividend ? Is it a chinese thing?

What is gong right ?

- They are consistently growing their market share in unregulated markets and Indian market

- BIo-CDMO opportunity size is huge and their parent Fosun group company Henlius can outsource (from the above commentary ) some of their needs to Gland. They already have direct Indian connection with Cipla (Source Henlius IP )

- Though Sputnik is a lost opportunity, the money spent on Bio infra ( Like bio reactors and all ) is fully fungible in nature

What is worrisome ?

- Margins are continuously going down (Industry phenomenon)

what is your anti thesis for gland…?

-

We don’t have good chemistry with China, being a Chinese company and having Chinese people on board - More here

-

It is a B2B player and injectables is not a barrier in itself, there are many other players in injectables, even Gland outsources their work to many small players (contract manufacturing) . Gufic has the highest Lyophilization capacity along with different drug delivery methods. So if someone says injectables business has a barrier to entry then I run away

-

Today’s Niche is tomorrows commodity, it could be niche drug delivery or niche generic molecule or niche complex molecule (nothing is complex , today’s complex chemistry tomorrows off the shelf chemistry , one can buy the technology and start producing on their own )

-

Biologics business from the parents subsidiary - so far nothing concrete in place

-

Loss they booked due to sputnik opportunity (though the infra is fungible but there is definitely hit on their earnings )

-

If Chinese government do not give approvals (there are 5 molecules ) to launch Gland products in China

Signs of slowing down ,

Some offloading in the recent past

Q1FY23 Concall (Just scribble will post the detailed one once the transcript is released )

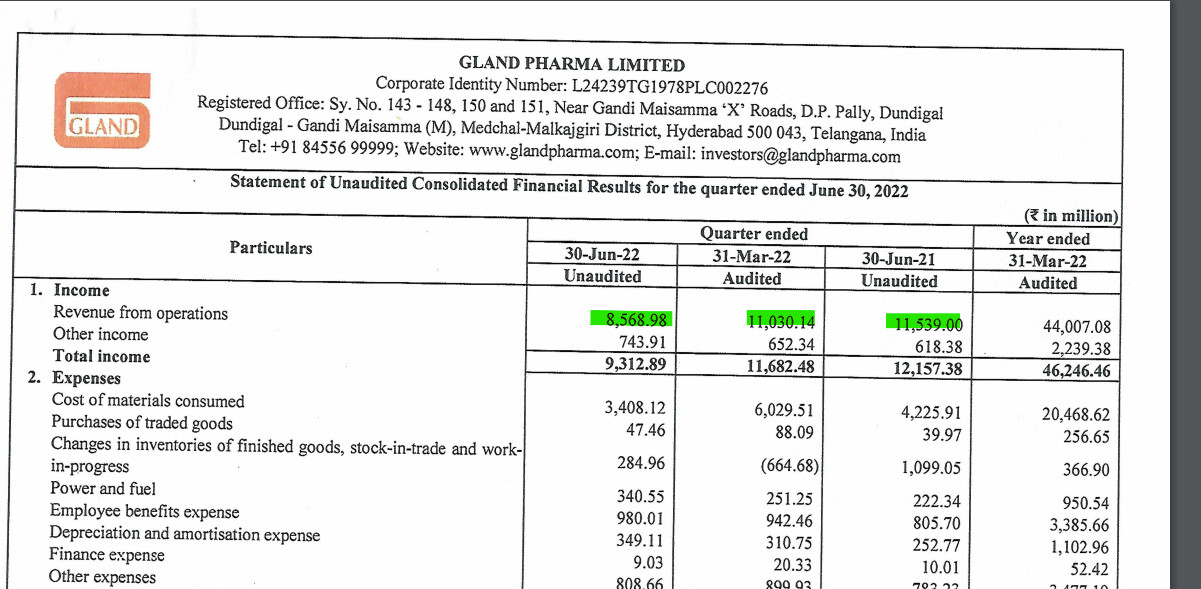

Revenue impact

- US 4% grown QOQ and degrown 4% YOY

- 10% of the Revenue is Profit share ( I think this related to in-license products I guess )

- Supply Chain Issues (Syringe Issues ) : 25 crores lost Developed Markets || 40 crores lost in Indian Market || 100 crores lost ROW markets

- Syringe Issues mitigation Plans : Some other suppliers (syringes) we are qualifying from the china and Italy for the rest of the world This is easy to do in India but takes some time in regulated markets

- Shutdown of the insulin lines

- India market down from 200 crores to 50 crores (Intentionally let the business go due to low margins , this was supplying to third parties )

- Capex In-line with last year

- Biologics CDMO

- 4 customer visits happened

- Discussing about commercial terms with the potential customers

- No clarity yet on when revenue contribution from this segment

- Is there any CDMO opportunity from Henlius ?

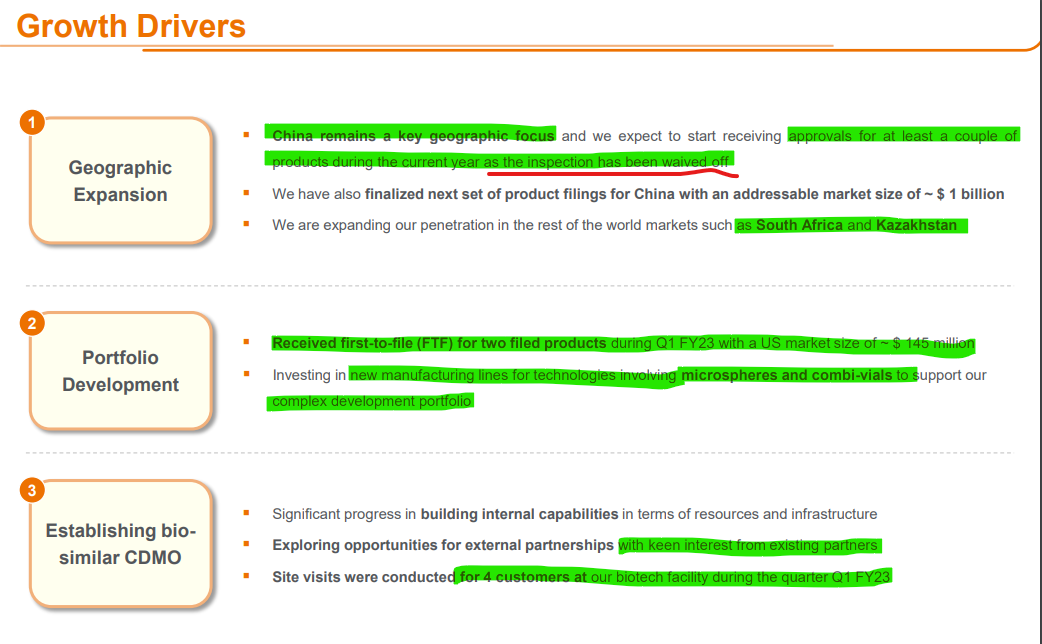

- China : Two molecules got exception from inspections (might commercialize by this or next quarter ) 4 filings in FY23 and 6-7 in FY24

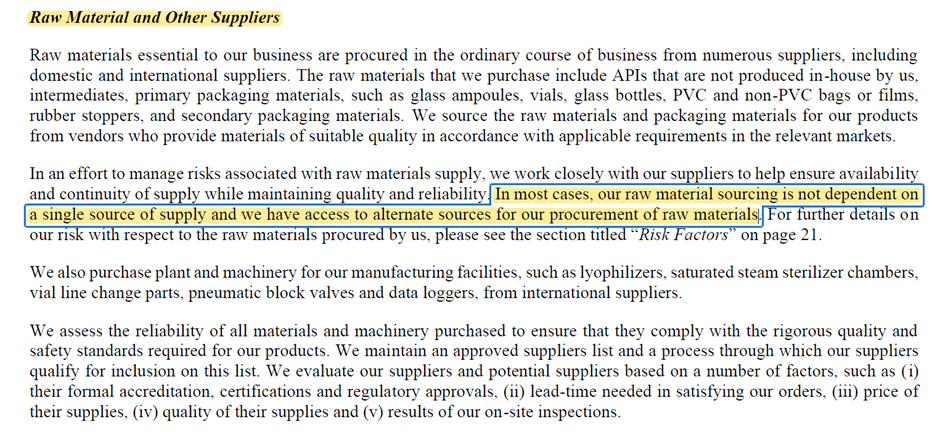

What exactly was the issue with syringe supplies? I will be very much surprised if the company has only one supplier for such a critical input or if they did not stock enough inventory. In the DRHP, the company says “In most cases, our raw material sourcing is not dependent on a single source of supply and we have access to alternate sources for our procurement of raw materials”.

Elsewhere (p.263), they have also said “we do not have any material dependence on a single or a few suppliers or customers”.

I heard the concall but did not get any proper idea (or may be missed it) of what caused the problem.

The management mentioned they did not procured the Syringes from other vendor as the prices were high and also the logistics cost was high to get them shipped to their facility. They have started to get a good supply of Syringes since May end and this should not hamper their production henceforth.

It is surprising that management is focusing just on bottom line and not the topline and not procuring the Syringes to supply to their customers even if they have orders in hand.

The answers given by management shake the confidence. On one side they are keeping high inventory to mitigate the supply challenges and on other side they are saying that they were not able to procure Syringes and this impacted their revenue.

The MOFSL analysts look surprised as management must have guided for 18-20% growth this year during their meeting and this sudden deep was surprise.

Disc: Sold 75% of my holdings today in the stock and will add if revenue and profit visibility grows in next few quarters. At 35 PE with no or negative growth this year stock price may correct further.

- Shortage of syringes

Entire world impacted due to this shortage and here is the latest update from FDA

Even if one has multiple sources ( I am sure Gland must be having them ) still they can’t meet the needs of Gland. The management decision was prudent, instead of buying them at any price they prioritized deliveries for the regulatory markets first ( in this noise no one is talking about margin expansion, during these high inflationary times how come their EBIDTA margins have gone up ? ) to meet their contractual obligations (hence positive impact on margins )

- Shutdown of dedicated insulin line taken for increasing the line productivity impacted quarterly sales

Shortfall in Insulin production to be compensated by improved line productivity for the rest of the year

- Higher input costs due to supply side challenges for our core portfolio also impacted sales conversion.

Mr Sadu clearly said in the call, they let go some of the orders where they feel it doesn’t make any sense to spend so much on Raw Material (power costs have also increased substantially ) and logistics that will not give good return so they let go that business

Management Foresight (I know these are narratives but at the same their Parent Fosun is very big player in China market, then I don’t see why Gland cannot benefit from this in future )

-

They are ready with Biosimilar CDMO infrastructure , 4 customers visits are complete and their peer group of company Henlius might give some work (Mr Sadu mentioned this in earlier calls )

-

China launch, I think now the time has come to launch, they are now saying they may launch in Q2/Q3 of FY23

I concur @Rafi_Syed views.

Just add to one point; co says there is a shortage of syringes and if we source from other than a regular vendor, it may have cost us more. Hence they give priority to their main market (USA) and compromised on the non-priority markets including India and RoW. The same can be seen in numbers as well,

It’s common sensical to think about syringe shortages- as the entire world went on a huge vaccine drive in last 1-2 years. For how long it persists, from management answers. It seems even they don’t know. Likely this year’s growth might get impacted.

Disc:- Not invested. Studying. Pricing erosion doesn’t seem to be the issue as per the narrative as gross margins have actually expanded.

Gland - In the concall Mr. Sadu said impact is due to syringe supply constraints, but in Reddys latest concall, they said there is no such issue experienced by them. (It is evident there is huge demand for syringes all over the world for vaccines ) How to understand these kind of statements (in terms of management honesty / integrity ) ?

Question asked in Hitesh bhai’s portfolio thread by @Rafi_Syed @hitesh2710

My thinking

Syringes required for different products are different

Gland uses (as I know famous BD syringes and device)

Some of them are glass syringes for specific measured doses

Some high viscosity medicine are difficult to inject (usually done by support staff) (some time at home)required some locking system and flanges proper holding

All this syringes and devices are preapproved by regulators so you cannot change overnight

Now coming to the Dr Reddy’s concall comment

They have only 15% revenue from injectable(how much prefilled syringes i don’t know) (how much in US market)and maybe having different products, even in previous calls of gland Pharma… Gland is making products for Dr Reddy’s

Just taking small statement out of context and making big on social media (twitter) is trending

personally I take it as personal bias of some analysts

Ultimately time will tell the truth

(Syringes supplied with ampules & muti dose vials are just commodities)

I think the answer lies in between non-availibility and high cost. As Mr Sadu said if we have procured it, may have cost us high and impacted our margin. The same view is offered by Siddharth Mittal of Biocon in BQ Prime interview; says, row materials are available plenty, no dearth of it, but the cost is very high.

Gland is a classic case of degrowth and margins compression, thus significant derating in last 2 -3 Qtrs.

Given core thesis of Gland is Injectable manufacturing, what good is a strong manufacturer vs average without better hold on supply chain.one would expect a solid procurement capability and risk Mitigation in place. Given they are still scouting and qualifying suppliers for emerging countries after having to air lift syringes in last many qtrs says somewhere there are inefficiencies.

While they did get away with logical arguments of not many syringes supplier out there which are approved for developed countries, thus a clear crtical path item.

Of some misses in q1 - some will come back shortly, for e.g. insulin shutdown for maintenance and freight cost. However do not foresee supply glut of syringes or price correction given limited suppliers for regulated markets, their best bet is to find a solution for emerging matkets syringe suppliers rather then letting biz go - but doesn’t look like without sizable scale of orders they are getting prices good enough to cater demand profitably, shows competetitive intensity for other Injectable players with better supply chain management.

Given a huge cash pile - it may be interesting to see if they do look at inorganic options to solve above issues for once and all - may sound offbeat to have captive syringes arrangement( even partly) but thats a choice that need to be made.

Another point to note is biosimilar/biologics foray, as well as china supplies via fosun - the answers from management are not affirmative and time bound. Doesn’t generate a confidence.

Its still an exciting and high growth area, they have inorganic growth options and capital in hand, however there is a clear lack of aggression ( likely to do with ownership and board construct/permissions etc).

Exited post Q1 nos and better opportunities.

Gross margin expansion was simply a function of geographical mix. Company prioritized US business and had to let go of RoW business. US business for Gland has higher GM.

From Gland DRHP

Revenues / Financials

- 27% YoY growth in Revenue (4400 crores)

- 22% YoY growth in PAT ( 1212 crores)

- 37% EBIT Margins

- 26% PAT Margin

- Zero Long term borrowing

- Gross Block 7,833 crores

- Capex 522 crore (228 crore in FY21, 194 cr in FY20)

Intellectual Capital

0.95 cr average revenue per employee

29 ANDAs filed - 19 approved

56 Customer Audits

11 DMFs filed

19% Attrition rate

India 60% YoY Growth

Europe 59% YoY Growth

Canada 26% YoY Growth

USA 13% YoY Growth

Australia 7% YoY Growth

India saw an impressive performance (revenue growth of 60% in FY 2021-22 compared to FY 2020-21), primarily on account of volume growth of existing products (India is the only B2C play rest all is B2B )

ROW - The biggest contributors were the LatAm, GCC and other Asian countries. Very positive response from the markets we have recently entered, including Singapore, Israel, Saudi Arabia, and CIS countries

Revenue contribution from new launches

236 crore in FY 22 (Dip in revenue from new launches )

366 crore in FY 21

229 crore in FY 20

Existing Products / New Launches

- Launched a total of 44 product SKUs (29 molecules) during FY 2021-22. Other core markets of Europe, Canada, Australia and New Zealand have also demonstrated strong demand for our products

- Micafungin Sodium, Ketorolac Tromethamine, Heparin Sodium, Ziprasidone, and Dexmedetomidine are some of the key products driving our growth in our core markets.

During the year under review, also successfully launched Caspofungin Acetate and Enoxaparin Sodium (Multi- Dose Cartridge with Pen Device) in the domestic market.

Along with other products such as Heparin Sodium, Rocuronium Bromide, and Dexmedetomidine, Enoxaparin Sodium was a key contributor to growth during the year.

We also registered our products Dexmedetomidine, Ertapenem and Tigecycline in new geographies.

Manufacturing Capital

- 28 production lines**

- 1,000 million units Finished formulation capacity (800 Million units last year)

- Added additional approved lines for our existing products to help reduce manufacturing risks

- Investing towards creating robust infrastructure for Biologic CDMO. (Dedicated team in place to take this forward, exploring opportunities to collaborate with our partners (Fosun ) and other companies to expedite our entry in this space)

- Vertically integrated injectable’s manufacturing capabilities

- We are also developing our Biotech Drug Substance Facility for biosimilars and exploring collaboration opportunities with established biosimilars producers (Genome Valley Hyderabad plant )

- Supply chain efficiencies are backed by our API production capacity, which ensures a secure supply of critical production inputs for our key products.

Human Capital

- 4,639 Employees as on March 31, 2022 ( 315 in r&d and 1449 in QA&QC - 31.24% of the work force is in QA&QC)

Management

25 Years of average experience of top management in the pharmaceutical industry

R&D Spend

- 86% YoY growth in R&D expenditure to strengthen product pipeline and enhance capabilities (Mainly into Biosimilar capacities setup ? )

Gland Strengths

- Complex injectable’s , oncology, and ophthalmology segments

- Drug Delivery methods - liquid vials, lyophilised vials, pre-filled syringes, ampoules,bags, and drops

New Capabilities (Work in progress )

- Complicated injectables such as peptides,long-acting injectables, suspensions, hormonal, pens and cartridges medicines.

KMP Remuneration

Note :FY20-21 89.43 cr

Mr. Srinivas Sadu was reappointed as MD & CEO for a further period of five years w.e.f. 25th April,

2022 vide resolution passed by the Shareholders through postal ballot on 20th April, 2022.

Industry Overview

Key Takeaways

- Entered markets in China by leveraging the credentials of our parent company, Fosun Pharma

- Spending on modern therapies by setting up biologics infra.

- Working on new drug delivery methods

- Since China is mostly tender driven business how Gland can piggy back on parents strong presence is something we have to watch out for.

- Since Bio CDMO is new space they are ready with capabilities, what is their right to win is something interest to watch

- They can gain more from Fosun in terms by strengthening KSM supply chain, this is the most important variable to avoid the issues like shortage syringes or other materials that are the life blood of business.

FY23 AGM Notes

Opening remarks by Mr. Sadu - Link

Answers for the questions posed by share holders Link

Growth Triggers

- China is 1 Billion dollar opportunity for Gland in injectables space

- Biologics - Biosimilar CDMO Infrastructure in place (learned hard way by failing in vaccine venture)

- Not going to work on Biosimilar development, focus is in partnership with innovators / partners

- Focusing more on process efficiencies, that is already translated into the best volume growth in the industry (Achieved 21% volume growth in FY22 )

- Every year the new product launches are contributing 8-10%

- 4 Complex injectables are in the pipe line to be launched this FY that has $1B opportunity

Capex

- 300 crores in FY23, 250 crores in FY24 (Spent on expanding capacities like microsphere combiline )

Risk Mitigation

- Actively working on alternate API suppliers

- Alternate packaging suppliers for fill and finish products

News