Gland Pharma Overview:

Company was incorporated in 1978 as ‘Gland Pharma Private Limited, Hyderabad. The business was started with single molecule, further expanded with other molecule. Due to some problem in business operation, the company shifted its operation to contract manufacturing.

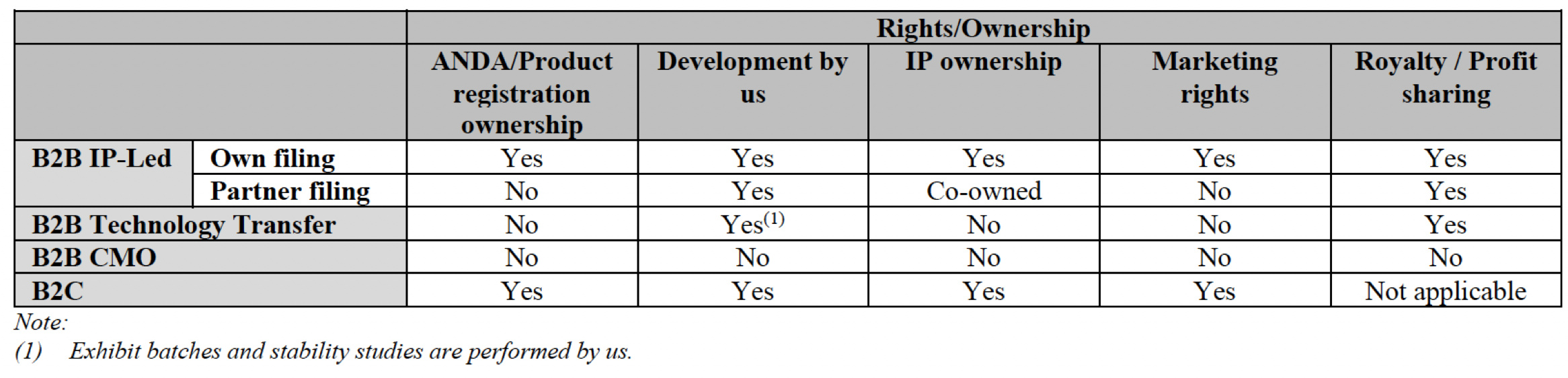

Company is primarily in Business to Business Model in over 60 countries, including the United States, Europe, Canada, Australia, India and the Rest of the world.

The company has expanded from liquid parenteral to cover other elements of the injectables value chain, including contract development, own development, dossier preparation and filing, technology transfer and manufacturing across a range of delivery systems

After continuation of work, Shanghai-based Fosun acquired a 74% stake in Gland Pharma in 2017 for over $1.2 billion.

Key Insights of Gland Pharma:

- The IPO issued by the company is majorly for selling the stake of Fosun Pharma. Out of total issue only Rs 1250 crores are utilized in IPO. Company already has cash balance of more than 1000 crores.

- There are many other players entering in the injectables segment. Companies such as Zydus, Cadila Healthcare, Caplin Point Labs, Maksumn Biotech Pvt. Ltd, Bliss GVS Pharma, Strides Pharma. These are the potentially good competitors for the company.

- Company is almost debt free. No burden of debt and cash rich company.

- Working Capital requirement of the company is pretty high. Companies working capital needs are almost 50% of the sales.

- Inventory of the company is almost 35% of the sales, which is pretty high compared to the competitors.

- Most of the ownership is in the hands of Fosun Pharma. This can materially impact the listing price of the company.

- In year 2018 company has done buyback of which the price was way higher.

(Source: DRHP)

In year 2018 company did buyback of 9.5 lakh shares at price. The buyback total amount is 344 crores. As mentioned in the image. This makes the price of Rs 3,600 wit face value of 10 Rs. The current face value of the company is 1 Rs making the buyback price of more than Rs 360.

Assuming 360 Rs to be the fair value of the company and now after the buyback, the IPO price of 1400-1500 Rs seems to be much over value. Company didn’t gained that much in sales volume and PAT value to quote at the price of more than 4-5x than that of the current IPO price.

- The Injectables segment is eyeing for good growth.

- Recent vaccine news can increase the short term price in the market. Injectables, Logistics and cold storage is the basic necessity in the supply chain of COVID vaccine.

- Company imports more than 30% of the raw material from China, which can have material impact due to any import ban. However, the possibility of this in near future is very low.

- Top 5 customers in Fiscals 2018, 2019 and 2020 accounted for 49.92%, 47.86%, 48.86% respectively. Any material impact in the business of customer can significantly impact the revenue of the Gland Pharma. Each customers have a revenue share of more than 7-8%.

- No compliance issue in US plant since inception while that of competitor has constant compliance issue from US FDA.

About the Industry:

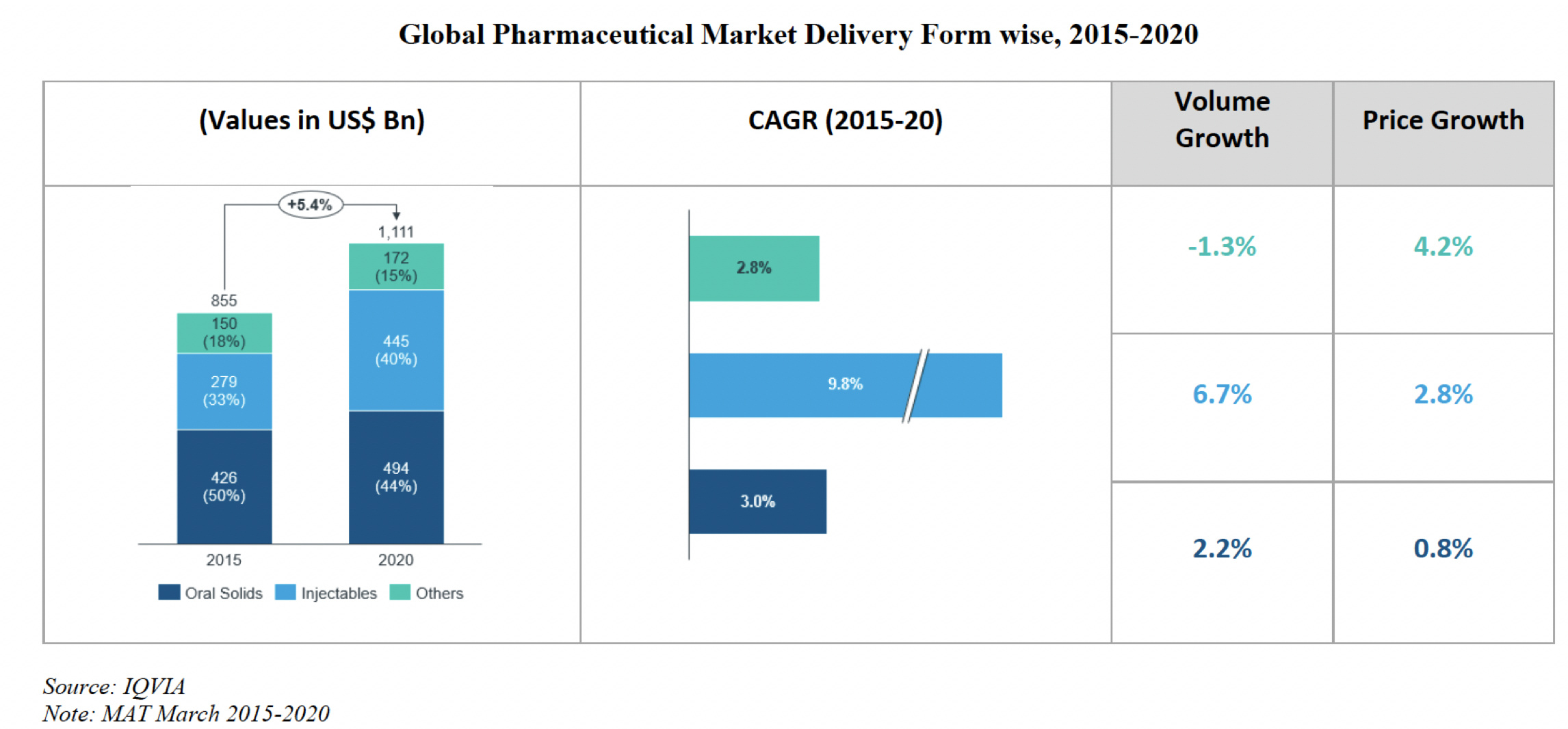

Company is in pharmaceutical sector, specializing itself in formulation delivery system which includes injectables form such as oral solids, injectables and other form.

The share of Oral Solids has been decreasing compared to that of injectables. Increase in share of injectables is mainly because of 6.3% increase in volume growth and 3.6% price growth from 2014. While the oral solids has seen volume degrowth of -2%, and price growth of 5.6%.

(Source: AR)

Factors leading to growth in Injectables form:

-

New Drug Delivery System (NDDS)- The development New Drug Delivery System has brought up major shift in the delivery mechanism. It includes device such as auto injectors, pen injectors, pre-filled syringes (“PFS”) and needle-free injectors. NDDS refers to formulation system and technology to transport medicine in the body in safely and therapeutic manner. Major of its advantage Decrease the side effects of the medicine

- Reduces the time of recovery as NDDS directly works against the antibodies.

- Complex manufacturing, but reduce the wastage of medicine compared to conventional method

- Increase the efficiency of the medicine.

- Pre-Filled Syringes: Patient receives the dosage according to their requirement. These includes the injection which are pre-filled with the medicine required to work against the antibodies.

- Chronic Disease had lot more side effects and the medication of such disease required longer time to fight against the anti-bodies. (eg. Chemotherapy disease)

- Fill and finish aspetic technology: Fill and finish is an advanced aseptic processing technology, which uses a continuous process to form, fill with drug or biologic and seal the container in a sterile environment. Most of the manufacturing partners specialising in injectables outsourcing are developing fill-finish capabilities to meet the growing needs of the market.

Porter Analysis on Industry:

With industry being divided in generic and formulation segment, it has been witnessed that global generics market was estimated to be US$393 billion in 2019, constituting approximately 36% of the global pharmaceutical market. According to IQVIA report, the market grew at a CAGR of approximately 5.0% from 2014 to 2019 and is estimated to grow at a CAGR of approximately 5.3% to reach US$508 billion by 2024.

(Read other players of Pharma Player here)

Global Generic Market:

Global Generic market of every region is increasing gradually over the period of time. Major demand is still coming from America and Europe Region. Growth is led by both Price and Volume growth.

Geographical Country Trends:

US Market: The injectable drug shortages in US has increased by approximately 23% in 2018 compared to 2014. The USFDA is particularly focusing on approving complex generics and generics where the reference listed product has no, or limited, competition. Injectables share in US has been increased from 33% in 2014 to 46% in 2019.

India: Indian market is expected to show double digit growth in pharmaceutical space over the period of few years. Generic formulations form a significant portion of the domestic market. India will have lead in export of generic medicine with increasing share in Europe and America region.

China: There has been shift from the generic demand of China to India. Generic formulations form a significant portion of the domestic market. Pricing pressure and quality assurance made the giant MNC to look for other player than China to remove the dependency from China.

Europe: Holding share in Europe is the upcoming target of many Indian Pharma players. Drivers in detail are mentioned in DRHP. (Source: DRHP)

(Source: DRHP)

Drug Shortages:

Over the years, the major reason for the drug shortages is the quality issues (holding 62% weight), following with increase in demand (holding 12% weight). Shortages of even generic molecule has been increasing, and below are current shortage molecule.

Patent Expiry Growth:

Value of lost patent in 2013 for period of 2014 to 2019 was US$32.8 billion.

Lost patent between 2020 and 2024 is US$61.3 billion. 2x increase in the size of patent expiry. According to the IQVIA Report, the value of small molecule injectables in 2019 expected to lose patent protection between 2020 and 2024 is US$ 7.9 billion.

About the Business:

Company has established portfolio of injectable products across various therapeutic areas and delivery systems. The company is present in sterile injectables, oncology and ophthalmics, and focus on complex injectables, NCE-1s, First-to-File products and 505(b)(2) filings.

Delivery system: The delivery system includes sterile injectables, oncology and ophthalmics, and focus on complex injectables, NCE-1s, First-to-File products and 505(b)(2) filings.

Gland Pharma Business Model:

Below is the cost model for the company

Business Model Canvas

Gland Pharma Value Chain:

Company has tried to become almost horizontally and vertically integrated, from manufacturing of API to Finished Product.

Vertical Integration allows company to achieve greater control over cost, manufacturing process, and setting up required standard, operational efficiencies.

Manufacturing Capacity:

3 API manufacturing facilities are USFDA approved; one is an R&D pilot plant and the other two have an annual capacity of 3,000 kg and 8,000 kg, respectively.

Expansion Plans:

- Expansion is in progress in oncology segment.

- Company is in line to built another injectables facility in Pashamylaram, Hyderabad and has increased the manufacturing capacity.

- Company is further planning to set up new R&D building in Pashamylaram, Hyderabad

Product Fillings:

265 ANDA filings in the United States, of which 204 were approved and 61 were pending approval. The 265 ANDA filings comprise 189 ANDA filings for sterile injectables, 50 for oncology and 26 for ophthalmics related products. Out of these 265 ANDA filings, 100 represent ANDAs owned by company, of which 63 ANDA filings are approved and 37 are pending approval.

Product Registration: Along with partners company has total of 1,415 product registrations, comprising 368 product registrations in the United States, Europe, Canada and Australia, 54 in India and 993 in the Rest of the world.

Product Portfolio:

Research and Development:

Company has in – house team of approximately 250 personnel including PhDs, pharmacy post graduates and chemists with expertise in synthesis of low molecular weight injectables drugs, steroids and oncology drugs and in developing complex injectables such as lyophilized products, high-potent drugs and long-acting suspensions.

Quality Control:

Quality Control plays the major role in Pharmaceutical industry. Company manages to maintain quality standard across product development, formulation, packaging, storage and transportation.

Gland Pharma till now had no warning letters from USFDA since inception of the facility. Company has received WHO GMP certifications from the Drug Control Administration. Company is supported by a quality assurance and quality control which numbered 1,166 number of new employees.

Sales and Marketing:

Company has total work force of over 200 employees and a countrywide distribution network in approximately 2,000 corporate hospitals. Company has already registered 66 trademark

Competition

Global Players who follow this segment:

B2C customer : Hikma, Fresenius Kabi, Amphastar, Sagent, American Reagent, Mylan, Teva and Sandoz.

B2B: Recipharm, Lonza and Piramal Pharma Solutions.

Large B2C pharmaceuticals companies also active in B2B market: Pfizer Centreone, Merck Bioreliance, Abbvie, Baxter, Ratio Pharma, Sanofi and GSK.

According to the IQVIA Report, principal competitors of company include Recipharm AB, Catalent, Inc., Lonza Group AG and Piramal Pharma Solutions.

The Indian listed players eyeing or already are in injectable segment are:

- Zydus

- Cadila Healthcare

- Caplin Point Labs

- Maksun Biotech Pvt Ltd

- Bliss GVS Pharma Ltd

- Strides Pharma

Key Personnel Management

Shrinivas Sadu: MD and CE. Holds Master’s degree in science from Long Island University, New York and a master’s degree in business administration from University of Baltimore. He also holds a post graduate certificate in finance and management from the London School of Business and Finance. Previously worked at Natco Pharma Limited at Hyderabad, India, and is presently a director on the board of Sadu Advisory Services Private Limited.

Yiu Kwan Stanley Lau: Chairman and Independent Director. Director on the board of directors Solasia Pharma K. K. and TaiLai Bioscience Ltd. Previously the chief executive officer of Amsino Medical Group, the chief operating officer of Eddingpharm Investment Co. Ltd, and the president of China Biologic Products, Inc

COVID Impact :

- Delays in treatment of non-COVID-19 patients

- Face-to-Face interactions minimised.

- Upsurge in demand for medicines to alleviate COVID – 19 symptoms.

- Impact on Innovation: Manufacturers may consider postponing their approach to new product launches. Lack of personnel could also result in delays to regulatory approvals and formulary listings.

Post COVID: In US, there has been longer prescriptions in retail pharmacies in terms of number of days of prescription so that renewals need to be more infrequent and this trend is also seen in other countries. The result will be a drop in the share of major chronic medication markets that is dynamic (i.e. new or switched prescriptions).

Financial and Valuation:

Revenue

Revenue from Operation is divided in Sale of Goods and Revenue from Service. Out of this Revenue from sale of goods constitute around 90% of the revenue while sale of service constitute around 10-12% of the revenue. Revenue from sale of service has increasing share in revenue from 8% to 12%.

Revenue from Service includes the CDMO, CMO revenue and Licencing fee

Expense Breakup:

Major of the expense includes the Cost of material which cost more than 60% of the total expense. While the other expense is around 10% of the expense, which includes the research and development cost and the quality assurance cost, depreciation cost.

PAT Margins of the business is continuously increasing since the past 3 years with increase in PAT margins. This is mainly because of price realisation and cost control due to backward integration.

Working Capital Requirement

Working Capital Days of the company is pretty high, but has been decreasing in the last 3 years. However the working capital requirement of the company is around 1000 crores, which is pretty high. Most of the inventory levels affects the working capital needs of the company.

Inventory days of the company in the current market is around 250 days. Receivable and Payables are both near to 80 days. This leads to continuous increase in the need of the working capital.

Company is almost debt free, and have debt of around 40 crores which is also interest free.

Geographical Revenue Share is increasing in every region with major increasing focus in rest of the world countries.

Revenue from Canada and Europe is increasing constantly with increase in focus. While company is also holding its share in US region with constant increase in sales by partnering with major players.

Order book of the company roughly stands at around 1-3% of the annual revenue, which is increasing gradually YoY.