Thanks @RajeevJ for sharing your view on this. It helps to know your views and gives us confidence to know that you believe its a minor irritant. I hope too that this is just a temporary blip and not a speed-bump to expansion plans. My concern comes from the past trend of how the management typically moves lethargically at snails pace on execution. The Goa LPG storage plan for instance.

They floated the plan in 2012 and applied for environmental clearance in the same year. They got the approval in May 2014. Three years later, in 2017, they tried to obtain CRZ clearance on basis of the Environmental Clearance received in 2014. The Environmental Clearance approval received was valid only for 5 years, till May 2019. Haven’t been able to find documents showing the current status of the environmental approval. I hope it has not lapsed already, since that may mean another long wait for the approval, all over again.

Delay in LPG project may be justified on financial grounds, as the company’s finances during 2012 to 2016 were in doldrums, and then onwards, it was under BIFR revival plan, so may not have had the liberty to allocate capex for that project. It also failed to attract any financial / strategic investor during this period, probably due to BIFR status or the fact that no investor would want to invest funds till businesses were not demerged / restructured to insulate them from loss making chemical business.

Despite the situations, 8 years is a long time for a project to take off, especially if it carries a superior revenue realisation and profitability potential (as noted in a post detailing notes from AGM 2018, on this thread)

Logically, management priority should be to fortify the business by adding high yielding assets. So I hope this expansion issue at JNPT does not turn into a long drawn wait due to inaction of the management, and that they move fast to fix it in quick time.

The rejection by MPCB committee is pertaining to expansion in plot No.7 for 5300 KL dated 22.10.2019 which is clearly mentioned in point no.12 of MPCB order attached herewith.CTO - 27.10.2020.pdf (5.6 MB) . Also attaching Consent to expansion for 5300 KL order dated 22.10.2019 for reference .CTE - Tank - 22.10.19.pdf (7.5 MB)

As per Last 2-3 Annual reports they were saying that they are increasing the capacity by upgrading its storage facilities by regular refurbishment of tanks and pipelines. It is clearly visible from the new consent to operate received from MPCB. They have increased the capacity (173819 KL) by almost 25% from existing capacity (137700 KL) in Plot No.7.

Expansion through Plot Acquisitions will be the turnaround story.

Thanks Sanket for the clarification on this, and the detailed documents. Good to know that they are trying to squeeze out additional capacity from the existing tanks / plot. As you rightly mention, expansion on additional plots will be the big rocket booster!

I don’t have a great understanding of their business.

Since they have storage of chemicals and oils there must be some cold storage facilities with them.

There will be a huge demand for cold storage incase a vaccine is found as our Govt. is also interested in providing vaccine to all .

However I’m not able to analyze if that will impact Ganesh Benzoplast.

Either it can get some business to store covid vaccines or due to other storage players allocating more space to vaccine and less to chemicals, Ganesh’s storage business can gain more demand or there can be no impact at all.

Experts provide your opinion on this. Thanks.

Key takeaways

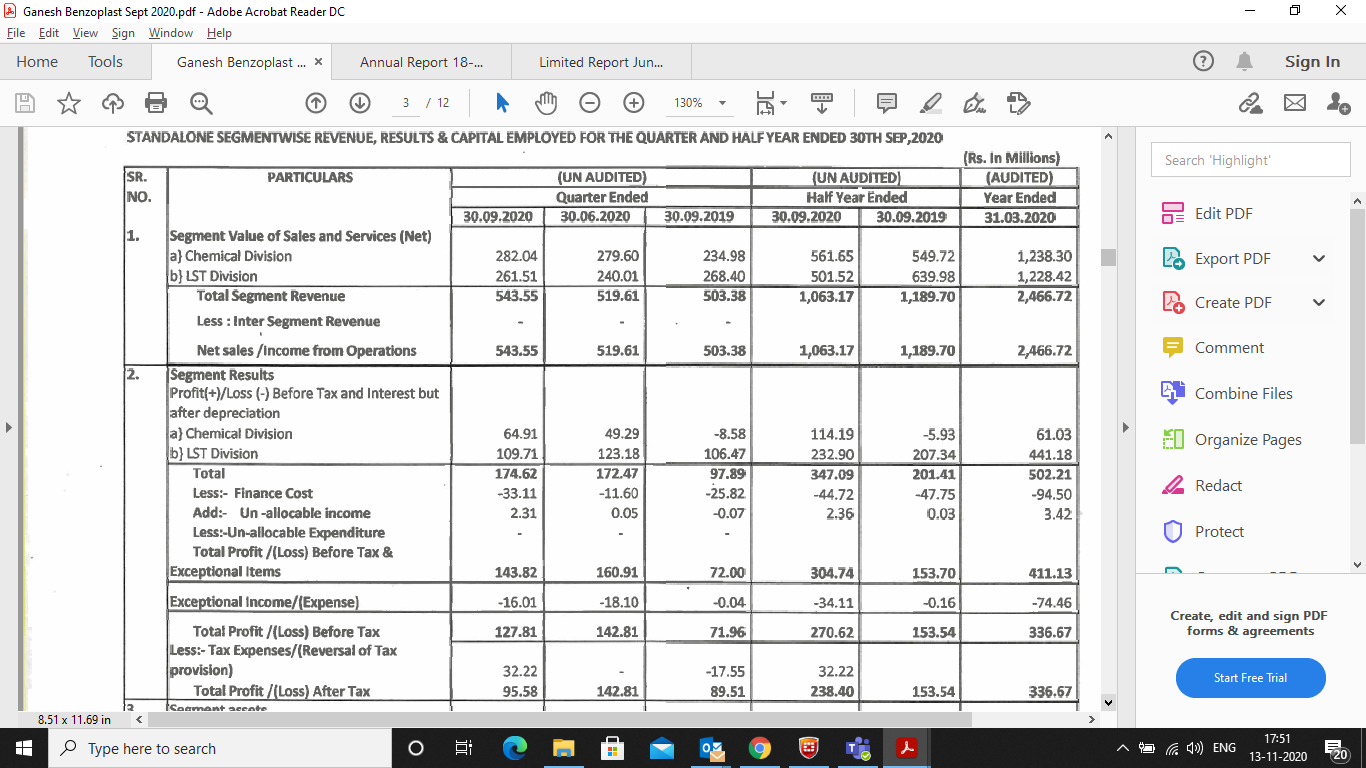

1.Operating Margins of Chemical division has improved further in September qtr which was 23% as compared to June qtr where it was 17%. The big turnaround in Chemial Division.

2.Margins of LST division is decreased , it should be mainly due to Work Contract work which has been mentioned in June quarter. Annual Report will give more clarity in the coming days

3.Ganesh Benzoplast is rebranding himself as “THE ULTIMATE INFRASTRUCTURE & STORAGE SOLUTlONS” . It might be due to new partnerships with Stolt.

4.CWIP should be converted into PPE in the coming quarter as they have recieved MPCB consent in October 2020 as mentioned in earlier thread. It should add to topline by 15-25% and to profit as well.

5.Finance Cost (2.2cr) and Exceptional expenses(1.6 cr ) seems to be of Contingent Liability pertaining to Morgan Securities Pvt Ltd . Will have to wait for clarity from Management in the coming Annual Report. This was the biggest hurdle in Demerger of Chemical and LST division.

6. Company has paid tax of 3.2 cr after a long time as company is hopeful of Profits in the coming quarters for Chemical division as well.

7. Date of AGM yet to be announced. Ganesh Benzoplast Sept 2020.pdf (4.3 MB)

The company received ex-parte order from the Delhi High Court in a case with Morgan Securities & Credits. After this, the process of preferential issue to Stolt Singapore and others has been stopped until the next court hearing in the case on 8 December.

Curious to understand few things around operating style of mgmt.

for a paltry 1.5cr+ dues to Morgan, whole process gets in limbo with STOLT. So why not anticipate it and settle it first? Two LC means 10 times mkt cap wiped off + embarrassed for future.

STOLT would have done some due diligence before this merger? Were they okay getting on boarded prior to resolving known issues? Assume they knew all liability aspects before coming on board. They have much to lose if it goes southward.

All in all , buying opportunity if matter at stake is small and will be settled, as management called out in update.

As Rajeev ji said in his earlier post, these are minor irritants and will be resolved with time. Fundamental value of the business is far more than CMP thereby leaving large scope of price catch up as events unfold and stock participants increase (in particular, institutional investor).

As per Annual Report 2018-19 -

Claim by M/s Morgan Securities and Credits Private Limited (Morgan) not acknowledge as Debt by the Company. M/s Ganesh Benzoplast Limited (GBL) has challenged the Arbitration award given in favor of Morgan in the Hon’ble Delhi High Court. Principal demand of 3.4 Millions along with interest @ 36% p.a with monthly rests on said sum from 29th September, 2001 till 09th December, 2015 (date of award) and post award interest @ 12% p.a on the awarded amount (Total claim of 780 Millions).

The Company has challenged the award vide filing a appeal in the Hon’ble Delhi High Court, which has been admitted and notices have been served to the party.

But as per BIFR sanctioned scheme, during the pendency of the scheme up to December 2020, the maximum payment to unsecured lender cannot exceed 25% of principal due of Rs. 3.4 Millions.

Also as per view of the senior advocates and as a principal of natural justice the allowable interest in such cases cannot be more than simple interest at the rate of 18% per annum (which is itself on the higher side)

the maximum contingent liability would not exceed ₹ 15 Millions.

As per High court order dated 08.11.2019 - This Court is of the view that the parties should make a serious endeavour to resolve this matter through mediation. Order attached herewith Morgan Nov 2019.pdf (252.7 KB)

High Court Order dated 17.11.2020 attached herewith for reference.Morgan 17.11.20.pdf (391.7 KB)

I believe that Morgan Securities is trying to recover the amount as much as they can by getting stay each and every time when there is major event occurrence for the company.

We can hope that this time it will be resolved as management is confident which they have communicated through BSE intimation.

I think the High Court Order came in after the Share allotment process to the shareholders of Stolt Rail Logistics Ltd. had already been completed, so to my mind, that stands. The rest we will know on December 8th when the hearing is scheduled. The order does not come in the way of the operations of the Co., but does create another irritant in the affairs of the Co.

The sooner the Morgan issue is resolved, the faster the Co. can move forward. I guess Morgan Securities is aware of that & is playing difficult. Perhaps the best course for Ganesh Benzo is to get the court judgement. That is likely to be cheaper for the Co.as courts normally do not give more than 12% interest on amounts payable. The arbitration award of 36% p.a., compounded monthly will not hold in the High Court, which is perhaps why the Co. is waiting for the law to take its own course.

LST rentals at JNPT could remain subdued because of the expansion(height) …the tanks will not generate rentals when the expansion is being carried out. Just my view…

Any idea about capacity utilisation at Chemical division? or any expansion plans at Chemical division interms of new chemicals ?

As per Annual Report 2019-20

The Company is continuously upgrading its storage facilities by regular refurbishment of tanks and pipelines. In LST division during the current year Company has incurred major repair and maintenance work at its terminals. Chemical Division

During the year, we have been able to improve the profitability, due to better capacity utilization and increased sales volume. Chemical Division of the Company is showing better performance in terms of increase in revenue as well as profitability as compared to the past years.

Expansion has been completed for tanks by refurbishment of tanks and pipelines and company had got consent to operate from MPCB in October 2020.It is clearly visible by comparing MPCB orders for Plot No.7 .So revenue should increase from October 2020 in LST Division. Capacity Utilization at LST Division is 100%.

There are no plans in Chemical division expansion because they were having very less utilization in chemical division which is getting pace in recent quarters.

So that it means they can easily clock 20% growth in topline and more than that in botttomline. As per AR Goa is being used at 40% but in the previous year it was 70% utilization. We can also interpret from above that the overall realization has gone up. They must disclose if any conflict in their operation at Goa port.

Also the in other expenses Rent part has gone up significantly from (in millions)

FY18 FY19 FY20

53.28 64.70 116.86

Also the in other expense head: Stores, Spares and Packing Material Consumed including Infra project works jump is huge. Which IMHO due raw material in form of steels. May be the rent is also up because of the Infra Division…they may have started it at rented place. In last 2 years bad debt written off is also significant 37.36+56.76 millions. If this is temporary then we may see more jump in bottomline.

Management is also not putting up recent rating action on BSE announcement which is strange.

Disc: Reduced holdings due to less communicative management

So far as there is ‘negative news’ about the company in public domain. …stay invested. Also small caps are in a massive bull market.

Here is my view…

No mention about Goa LPG project in AR . Last year AR had mentioned that ‘Foundation work’ has started.

May be they could not arrange funding . Also they could carry out expansion in GOA only after demerger and induction of an investor in GBL LPG.

As they have a long manufacturing experience in Chemicals and its profitable now…company must increase focus on the Chemicals division ( Less capital intensive and hence less risky than LST) …stable cashflows from LST should be used to finance new Chemicals manufacturing…Ideal situation.