zeo dividend and zero tax rate, first. is concern and second just tell me that earning profit will be not in proportional to revenue growth/

The Co. went into BIFR sometime in 2015 & should be coming out of it this year. This would enable it to give a dividend this year, though the mgt. is more inclined to go for a share buy back is my understanding.

Once its carried forward losses are wiped out, then it will start paying taxes. Probably next year.

2 Likes

Pursuant to the Regulation 29 of the SEBI (LODR) Regulations, 2015, we would like to inform

you that a meeting of the Board of Directors of the Company will be held on Wednesday,

October 07, 2020 to, inter alia, consider and approve the issue of Equity shares on

Preferential/Private placement basis amongst other matters. Private Placement Intimation.pdf (480.6 KB)

Price at which Private Placement happens will be key trigger. Procedure of Private Placement by law .Private Placement of Securities under Company Law.pdf (150.1 KB)

There must be some purpose to issue shares. Why would they do this? They are already making good free cash flow and reducing debts. Management has remained bit silent on their actions and nothing much is shared with minority shareholders though they are doing very good in biz. I expect them to be more communicative in future with regards to future developments.

2 Likes

There are several things I am worried about

-

Is the business scalable?

They are expanding their capacity by building a wall heigher than it’s already.

But in this way is it possible to add capacity in multiples, like 3x-5x capacity, even 10x, as there is a limit to the height any storage tank can be built? How much room is left for this kind of cheap capacity expansion? After that point, there has to be new place or land for capacity expansion.

What I basically mean is, quoting Vijay Kedia, “Is is aligator in a pond or it’s a fish in the ocean”. We want fish in the ocean, & not an aligator in the pond -

Are they able to increase rents per unit of volume storage?

It seems they have huge demand as customers payed for capacity expansion.

So I guess if they have not increased rents, it’s a good sign as they have UNTAPPED PRICING POWER.

1 Like

Any idea why they are planning to issue preference shares / private placement of shares. In any case it would dilute the equity of existing share holders. Does it have something to do with demerger ? Or is to shore capital for LST expansion/ LPG capacity ?

Perhaps it’s better we wait till Wednesday instead of speculating now. This story has a number of triggers that will play out over the next 6-8 months.

As the market cap increases, we will have investors feel more comfortable with the story as is always the case.

3 Likes

I completely agree with Rajeevji as the company is at an influx point, I believe. It will be great interact with the management in the upcoming AGM (date and notice not yet disclosed) to know more about future plans as there is hardly any communication from the management. Lack of openness is common in small cap companies as in most cases there is an anchor investor who wants to accumulate sufficient shares at lower price and then give a growth story in the market along with price action to market the stock.

As far as fundamentals are concerned, there is an all round improvement in the business and now the stock is set for re-rating depending upon the future plans of the company.

Disclaimer: I am invested in the stock.

1 Like

Outcome of board meeting

1 Like

Ganesh Benzoplast (GBL) is acquiring 86.52% in Stolt Rail Logistics Ltd., which was till now a JV between the promoters of the Co. & Stolt Nielson Ltd.(SNL). Stolt Rail Logistics is in the business of providing end to end logistic solutions from the Port to the Plant so the business is complimentary to GBL’s Port storage facilities.

SNL is a global giant in bulk liquid logistics business. It is the World’s largest owner of ISO tankers & its division Stolthaven Terminals has liquid storage terminals in 12 countries with a capacity of about 50,00,000 KL. To put things in perspective, Ganesh’s current capacity in liquid storage is about 3,00,000 KL.

In an all share deal, in lieu of the the 86.52% stake in Stolt Rail Logistics, GBL will issue 1,05,75,128 shares in the Co. The net result of all this is that SNL will hold almost 10% equity stake in GBL. This is huge. For a global giant like SNL to agree to come on board is a big vote of confidence in the mgt. of GBL. Needless to say that SNL will henceforth play a big role in the future growth story of GBL which is in the process of expanding its liquid storage division in a big way. SNL also has major investments in LNG & could play a role in GBL’s future LNG plans in Goa.

All in all, a very positive development for the Co.

9 Likes

Rajeev bhai this is credit rating for stolt…flat topline for last couple of years.even in press release similar nos are being talked about.also in 2017 they only made 30 lacs pat… the aquisition price is 60 pdd crores…any idea on current pat of stolt?

2 Likes

@Gaurav152

The profit figures for Stolt Rail Logistics are not available. Its possible that they may not be great, but its a small price to pay to get SNL on board. Besides, its a share swap so no cash outgo either. So far Ganesh was not getting the desired valuations due to the legacy issues of the past. With SNL invested, investor perception towards the Co. will change & that itself could potentially re-rate the stock over the next 4-6 months. Also to be noted that unlike most cases where private companies of the promoters are merged leading to substantial increase in promoter stake, there has been no increase in promoter holdings in this case, so that was clearly not the motivation here.

Another concern earlier was that promoters were is a similar line of business (Logistics) in their individual capacity & that too was held against the Co. when it came to valuations. With GBL taking over Stolt Nielson, that concern too has been addressed.

That the Co.'s numbers going forward are going to be top notch in any case is a given. Hopefully, the Co. should get a more acceptable multiple too!

Based on last years numbers, there is ~20% dilution for ~14% additional revenue. We don’t know of the profit margin of SRNL yet, let’s see. Getting SNL on board is a definite positive and also with the two entities getting merged, hopefully, the sum of parts will be greater. Promoters having an unlisted entity on the side operating in the same business segment wasnt great interms of corporate governance. Interesting to see what synergies this move will bring in.

Disc: Invested recently after all the shares were unpledged.

1 Like

Kindly forgive my ignorance…

So essentially in lieu of diluting the equity for about 20% ( 5 cr previously to 6cr odd after acquisition ) the share holders get to participate in the spoils of SRLS ? One more added benefit is that Stolt Nielsen Singapore becomes a part of Genesh Benzoplast through the preference shares allotted. ( is there a mention somewhere on the 10% allotment ?)

Please see Page 11 of the Postal Ballet Notice.

1 Like

The correction in the share price presents an opportunity to enter for all the investors who missed the bus earlier. Consider the following recent developments in the Co.

-

The numbers which have been pretty good for sometime due to the steady performance of the LST business now gets a huge boost with the changing of environment for for the Chemicals division. This change is structural in nature & is sustainable.

-

One of the issues plaguing the Co. was that of pledged shares of the Promoters. Even though these shares were pledged against the loans taken by the Co. in the regular course of the business, the investors were not convinced. With debt reduction, these pledged shares have been released. The Co. in fact is on the verge of becoming debt free on a net basis.

-

The issue of High Contingent liabilities, another concern has been addressed with the reduction by about 50% with the litigation with the STC being settled & paid for in full.

-

Merging of other logistics business of the Promoters, Stolt Rail Logistics Ltd., a profit making entity with enormous growth potential, with the Co. So going forward, the entire gamut of the Logistics business will come under the Co.

-

Stolt Nielson, a world giant in the field of liquid storage & transportation takes a 10% stake in the Co. This has huge ramifications in the future. Stolt will surely want to have a bigger presence in the big growing market, that is India & it will come as no surprise of the Co. scales up its operations at a fast clip going forward with increased participation from Stolt. Stolt’s presence would also have a material impact to the valuations & the stock is quite likely to get re-rated in the coming months.

18 Likes

Thank you @RajeevJ for bringing this Company (along with a quite a few other fantastic looking opportunities) to our notice. Just wanted to add that for anyone looking at an exact entry point the offer for sale to Stolt Nielson provides the exact number:

“The members of the Company be and is hereby accorded to the Board, to create, offer, issue and allot, 1,05,75,128

equity shares of face value of Re. 1/- (Rupee One only) (hereinafter referred as the “Equity Shares”) at a price of Rs.

62/- (Rupees Sixty-Two only) per equity share”

Source: postal ballot notice above

Not seen this mentioned directly in the thread so thought this would help prospective investors since I believe 62 looks like the fair value now and the lower circuits of late shouldn’t scare investors away since it was just reverting to this OFS price which represents what the company itself thinks is fair value.

Disc: invested @62 yesterday after patiently waiting for that price. Not a sebi advisor

8 Likes

Found this in the minutes of meeting of the consent committee of Maharashtra Pollution Control Board, held on 7th Aug 2020.

From this, it seems that the MPCB consent for expansion has been held up due to non-compliance - submission of CRZ clearance. This will delay the plans for capacity expansion at JNPT… which is much needed for revenue growth of the company…

2 Likes

Was trying to assess the details of expansion plans for LST business at JNPT, but found nothing significant in AR 19. I have some questions about this. Tried to find the answers, but got nothing concrete so far, hence checking with fellow boarders who may have some info on this from previous ARs / AGMs or other sources.

-

Does the company have the land to expand capacity at JNPT, or is it looking to lease more land from the port?

-

Has the company disclosed any plans about the expansion? Volume, CAPEX, Timelines?

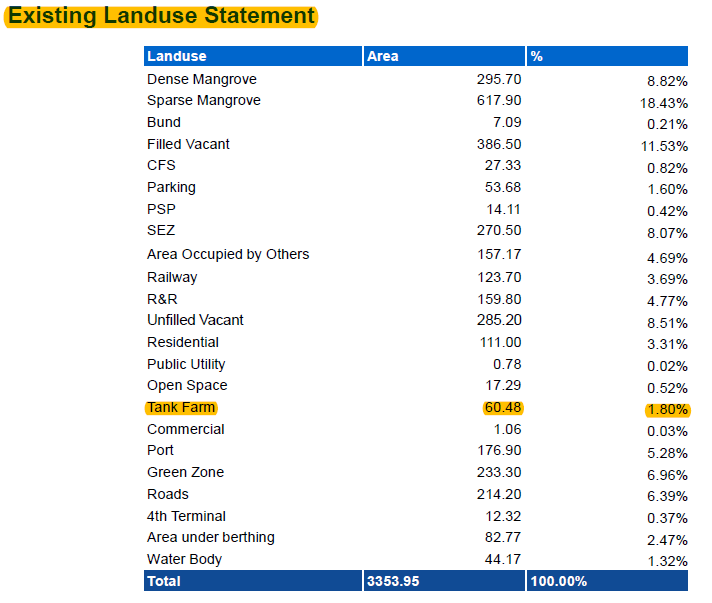

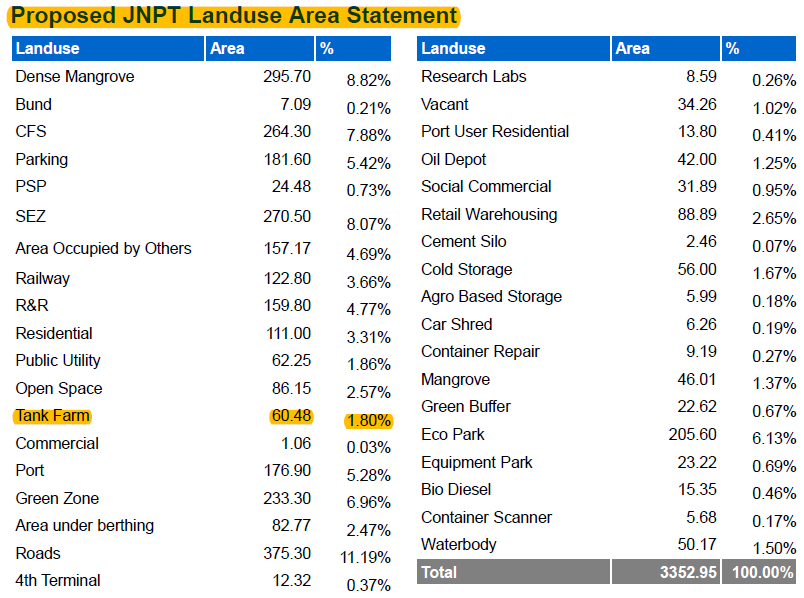

If it plans to lease more land, then it will mean longer lead time. In worst case scenario, it may not get any land. As per land use plan of JNPT, it has no plans to allocate land for new tank farms.

Existing Land Use

Proposed Land Use

2 Likes

@bhambani

These are minor irritants & will get resolved when the time comes. The fact is that the Co. is the largest operator on JNPT with about 2,00,000 KL capacity & have the necessary wherewithal to make it happen. Your post however confirms that the process for land allotment is on. The land in question I believe is adjacent to their existing operations, & there is every likelihood that it will be allotted in due course

3 Likes