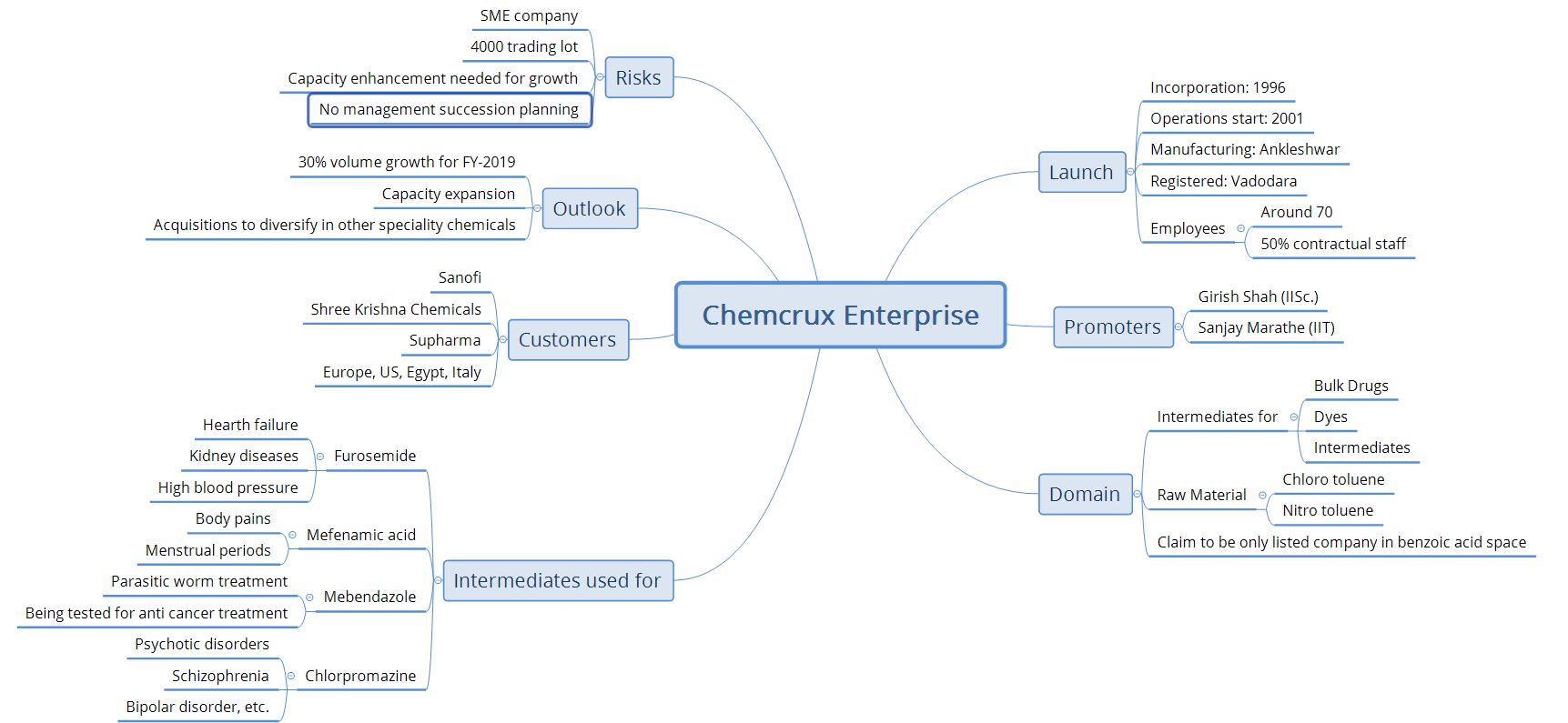

Chemcrux enterprises is a Gujarat based company dealing in manufacturing of chemical intermediates for bulk drugs, dyes and pigments.

The end consumers are the organizations which are into manufacturing of these drugs and dyestuff.

It was incorporated in 1996 by technocrat promoters Girish Shah and Sanjay Marathe from IISc. / IIT.

The Company started its business activities in the year 2000-01 by taking over the running business of

M/s. Chemcrux, a partnership firm of the promoters, as a going concern.

The promoters currently hold 73% of the equity.

Office location: Manufacturing unit in Ankleshwar and registered office in Vadodara.

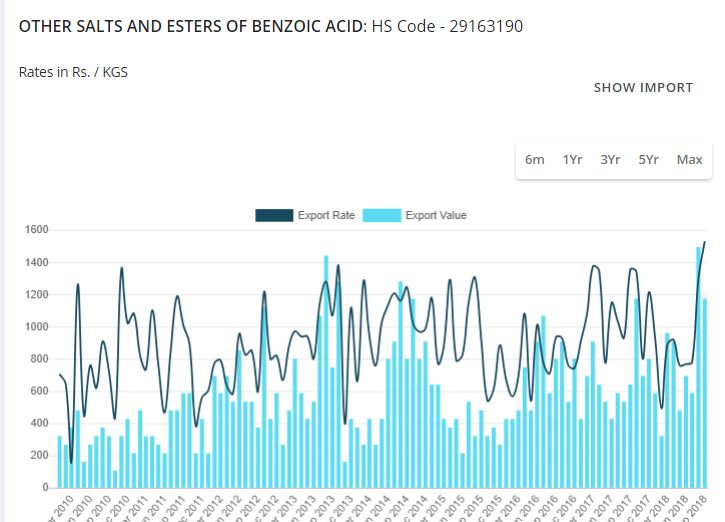

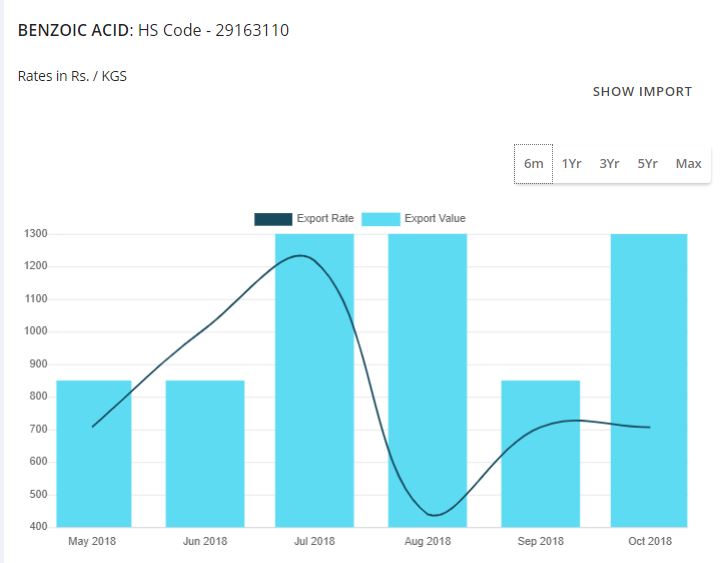

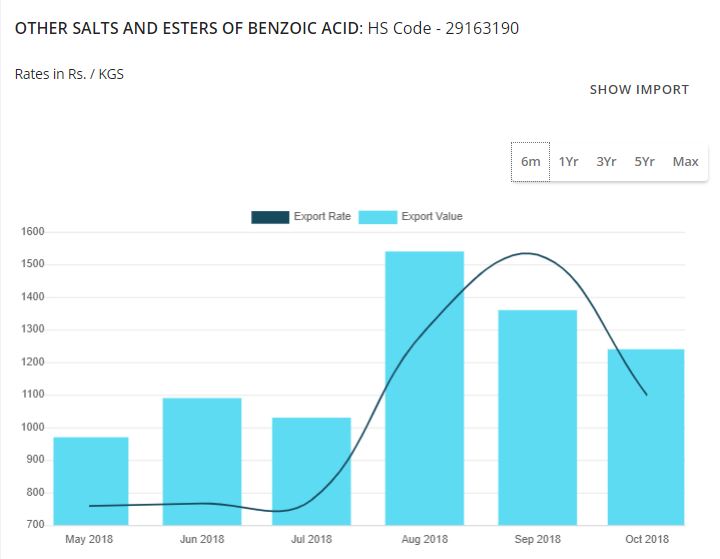

Raw Material: The basic raw material they use are chloro and nitro toluene based chemicals which is procured domestically as well as from International markets (mainly China).

End user application: The benzoic acid intermediates it supplies are used in manufacturing of following important drugs:

FUROSEMIDE: Sold under the brand name “Lasix” is used for the treatment of fluid build up due to heart failure, kidney diseases, high blood pressure, hypertension, etc.

Mefenamic acid: Used for the treatment of mild to moderate pains from various conditions including blood loss from menstrual periods.

Mebendazole: Used to treat parasitic worm infestations including pinworm, hook worm, etc. Its application is also currently being tested as an anti cancer treatment.

Chlorpromazine: Its primary usage is to treat psychotic disorders such as schizophrenia, bipolar disorder, etc.

Customers: Some of its customers are Sanofi, Shree Krishna pharma, Su pharma, etc. They also export to Europe, Italy, Egypt and U.S.

Employees: Current strength is around 70 with around 40% contract staff.

Outlook and growth: The company is planning to setup another manufacturing unit to increase the production and looking for various options.

Established in 1983 and still at 20 crore market cap. That’s almost like zero growth company for past many decades!

A decent business can reach 1-2 cr profits in 5 years and hence, 20 crs mkt Cap! Infact reaching 2 cr profits can be done by almost anyone on this forum itself in many kind of businesses!

Respect your point of view but don’t agree with a generic statement that a decent business can make profit of 1-2 Cr in 5 years. Each business has its own priority.

Flipkart never made profit ever doesn’t mean it was not a decent business.

Market capitalization is not a function of how many years you are in a business.

Look at the market cap of Liberty shoes, Dai-ichi Karkaria, etc from screener and you would know what I mean.

Stock investing is solely based on future projections, that’s why this thread. Regarding micro / nano caps which have made big on this forum, following threads can be used:

They are planning for new high margin products and capacity expansion or some strategic acquisition. This is not finalized as of now and might be revealed in near future.

They are running on almost full capacity since 2017. However, variation in product mix, moving towards higher margin product variant having higher demand and higher market price on the particular period helped topline, bottomline and middleline growth since the last one and half year or so. Going forward, the same strategy will yield growth without any capacity expansion as long as external market supports or as long as they can align themselves to the supply-demand equation.

Further, they are looking for small scale factory acquisition or/and installing advanced process development equipments to fuel the next leg of growth. I am not sure about any time period/deadline for the same but it might be finalised within the current financial year itself (rough guess).

They already shifted bigger new office in recent time.

Disclosure - Holding the stock since IPO in March 2017, gradually increased stake in various times. As per September 2018 shareholding, I am holding 2.19% stake. Further increased stake in November 2018. Can’t comment anything on stock price as it is highly illiquid SME stock. Market cap during first entry 15cr. Current market cap 32cr still a nanocap!

The most important point to note here is that Chemcrux is not product driven company, rather a process (Chlorosulfonation & Oxidation) driven company. It means they can swiftly change the products depending on the supply-demand scenario. This is why the company didn’t get highly impacted during crude price and forex volatility.

“Company expects to continue with the momentum of growth in revenue and

profitability with emphasis on operational efficiency, capacity expansion, value added product offerings,

penetration in new overseas markets. Company targets growth to three digit Topline in next 3 years.

Management is consistent in internal target. During October/November 2018 too they had guided 100 cr+ topline in the next 3 years and currently maintaining the same stance.

As I am invested since IPO in March 2017, so as per my experience, in all the earlier occasions, the numbers outpaced management guidance.

Sorry, I can’t disclose my position in other stocks in which I didn’t provide any public recommendation or research notes.

As this thread is all about Chemcrux Enterprises and I expressed a positive view so offered disclosure that holding Chemcrux since IPO time (March 2017)