Thanks for the detailed note. I invested in and exited the stock during the period 2016-17. They did a QIP in Sep’16. The stock went up from 1,000 to 1,500 before QIP and came down to 1,000 levels within few months from QIP. No major change in the industry and market conditions in that 6-8 months time frame. To my knowledge, this issue has no impact at present or in near future. However, this is a key point to note while assessing the corporate governance of this company. My 2 cents

1 Like

Hi. Thanks for the reply and your view on this story.

In the last concall, the management has stated (two times in different questions) that the margins for LED will be in a similar range after a certain level of ramp-up. Unfortunately, I am not sure of the exact reason but assume that price competitiveness is an important factor limiting margins here. Most auto ancillaries usually operate on weak OPM barring a few.

Lumax (which I intend to study more soon) is a very competitive player in LED segment. It caters mostly to four-wheeler companies but is present at two-wheelers such as Honda and HMSI as well. It claimed margins of around 18% for LED segment but they supply larger volumes to 4 wheeler companies rather than 2W that Fiem does.

But as of now, it seems that there won’t be any margin expansion for 2-3 years.

1 Like

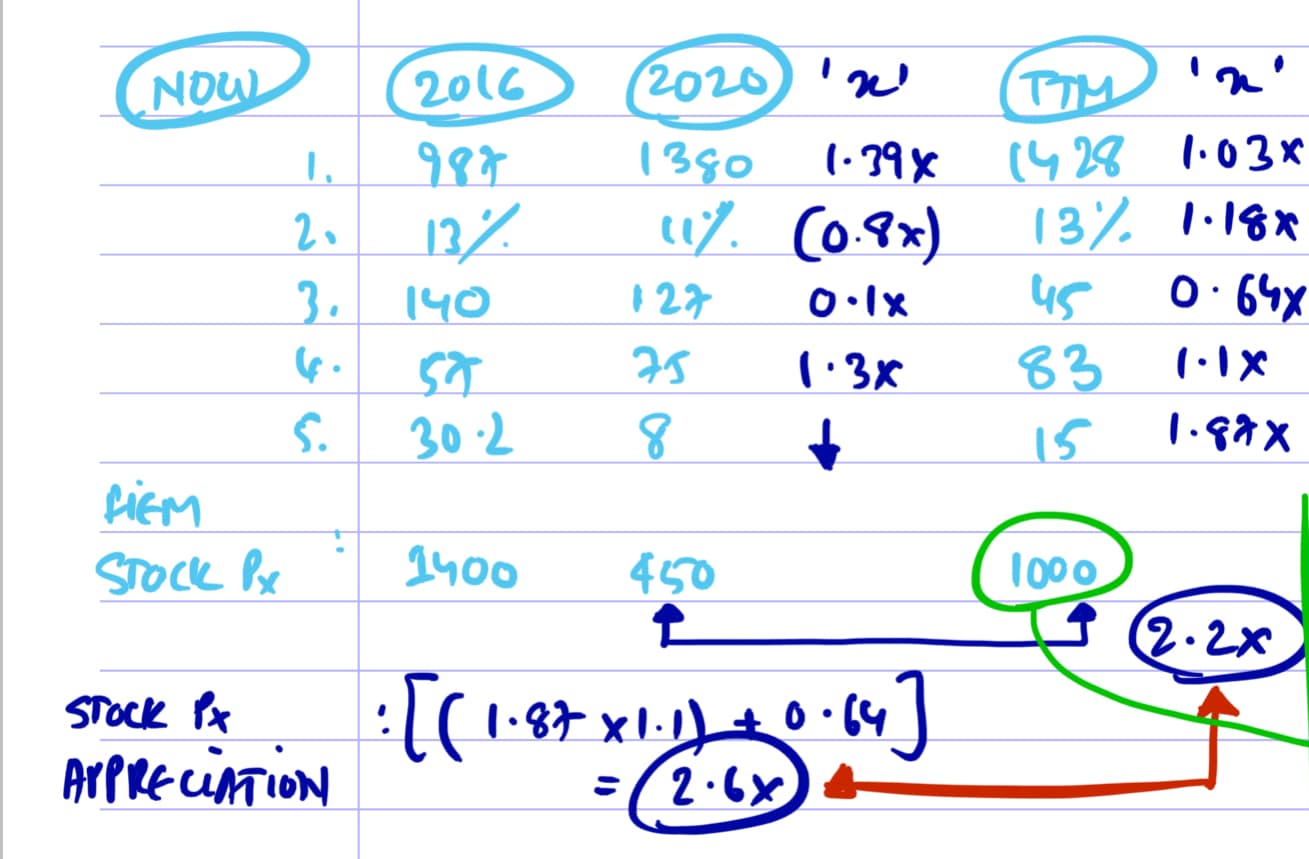

While the thesis is clear that future product mix can generate at-least 2x value even if volumes remain same like past decade, there are some red flags that one needs to be aware -

- Foreign JVs not audited

- Contingent Liability > 70 Cr

- Low Cash yields for 3 years < 5%

3 Likes

This Should largely put to rest why it doesn’t matter if margins remain in the 10-13% range like it has for the company in the last 8-10+ years across the 2W business cycles.

Returns would largely be generated from op leverage and pe expansion. Post which the Pe rerating takes place.

2nd image explains what happened next. One needs to stop fixating so much on margins especially for a company which has done well across business cycles.

3 Likes

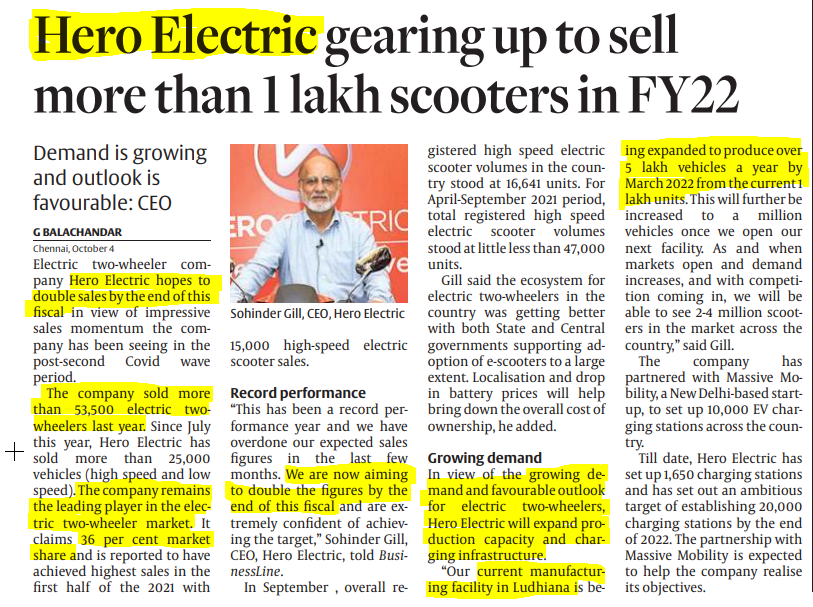

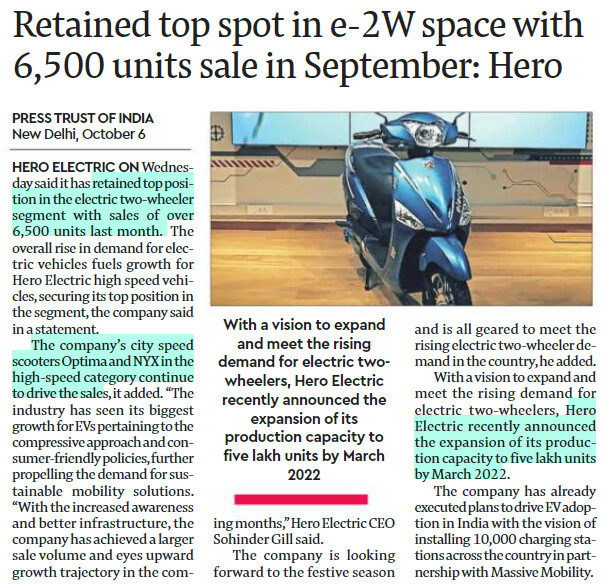

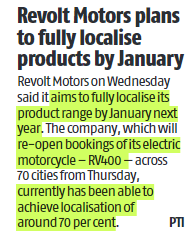

Posting recent newspaper articles which highlight potential business opportunities for the company.

Revolt Motors:

TVS planning big inroads as well…

HMSI plans entry now.

10 Likes

That will never allow company to sqeeze any considerable margin , with this product (led) one can not imagine fiem to creat any large wealth…

Disc. Not invested

not necessarily. Prices depend on demand & supply. You’re only thinking about the supply. Think about the demand. Entire 2w market will be replaced to ev at some point in the future (10/20 years). While prices might come down a bit, but generally volumes make up for that handsomely.

Attaching couple of snippets from q3fy21 concall. Would suggest going over all them.

And another one

While it is very much possible that over a very long time horizon with economies of scale & with ev going from 1% of fleet to 99% of fleet led prices might reduce by 50%, but primary question for investors is whether in a concentrated industry structure with only 2/3 efficient players and one of them having already penetrated the supply chain of 90% of 2W OEM EV manufacturers is the risk reward in our favor or not. Imo it is. Only thing missing here is volume growth for entire 2w industry. Imo that can come back with GDP economy growth and that would make this a perfect investment.

Disc: have a small position, closely tracking.

4 Likes

FIEM has moved up 9% today on very good volumes. I couldn’t find any news or announcement? Any idea what the market factoring in?

Invested recently for EV exposure. In the process of building conviction to increase PF allocation.

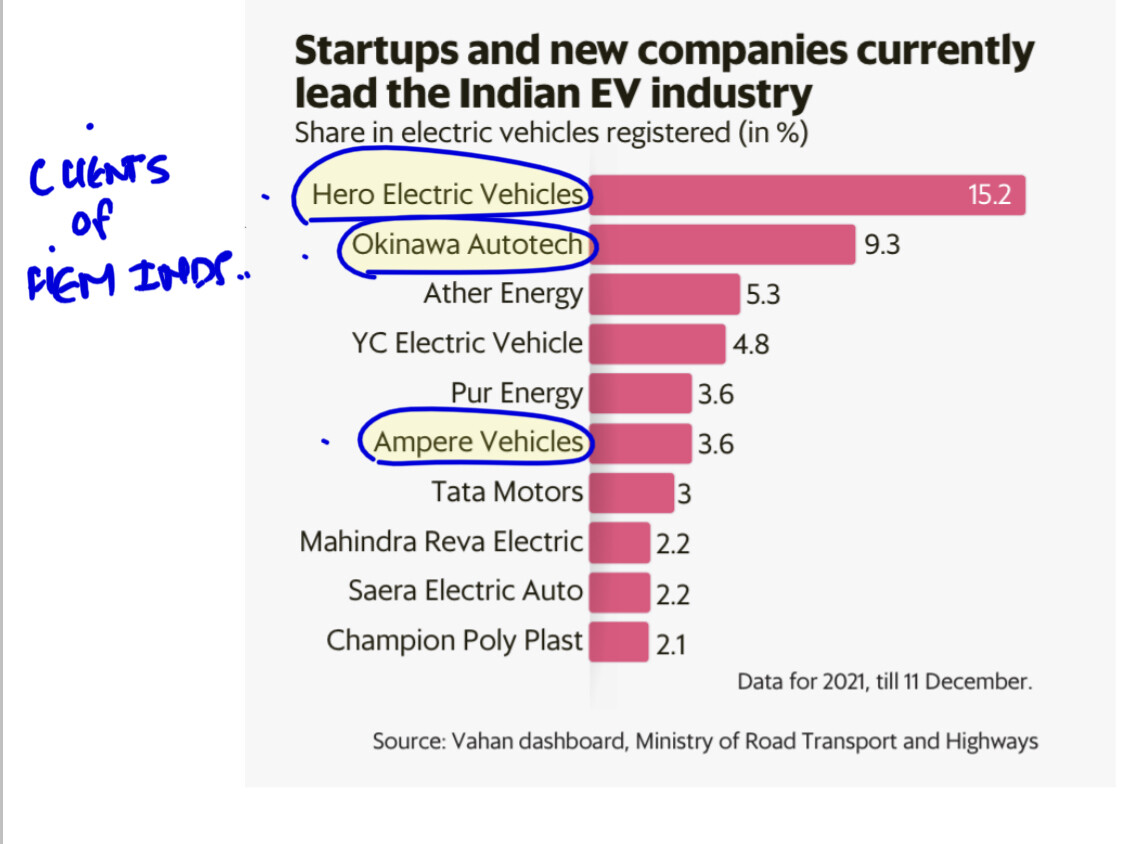

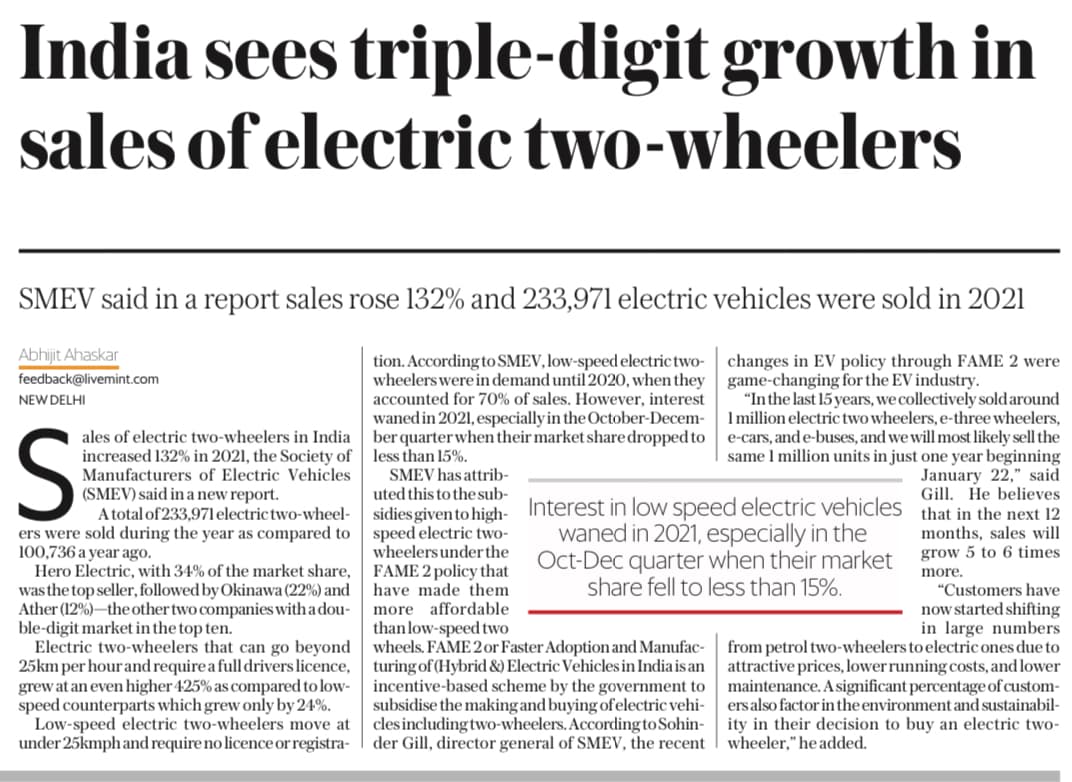

Found the below chart for EV 2W sales in India this CY on Twitter (Haven’t verified it).

4 Likes

Q3 results out.

Q-o-Q topline de-growth of 7.2%, EBITDA margins have largely held (Q-o-Q reduction of 28bps). Most other auto ancillaries have reported flat Q-o-Q revenues, so this 7% drop seems a little steep on the face of it.

Company has decided to exit from its JV with Japanese firm Aisan

2 Likes

Ola S1pro catches fire spontaneously in Pune. This can affect short term safety perception of EV wheelers in India.

a1b50a8d-d1e2-44df-8389-155a990355ca (1).pdf (4.4 MB)

Excellent Q4 results from Fiem. Strong revenue and margin growth QoQ. Strong YoY revenue growth as well and YoY margins are flat.

1 Like

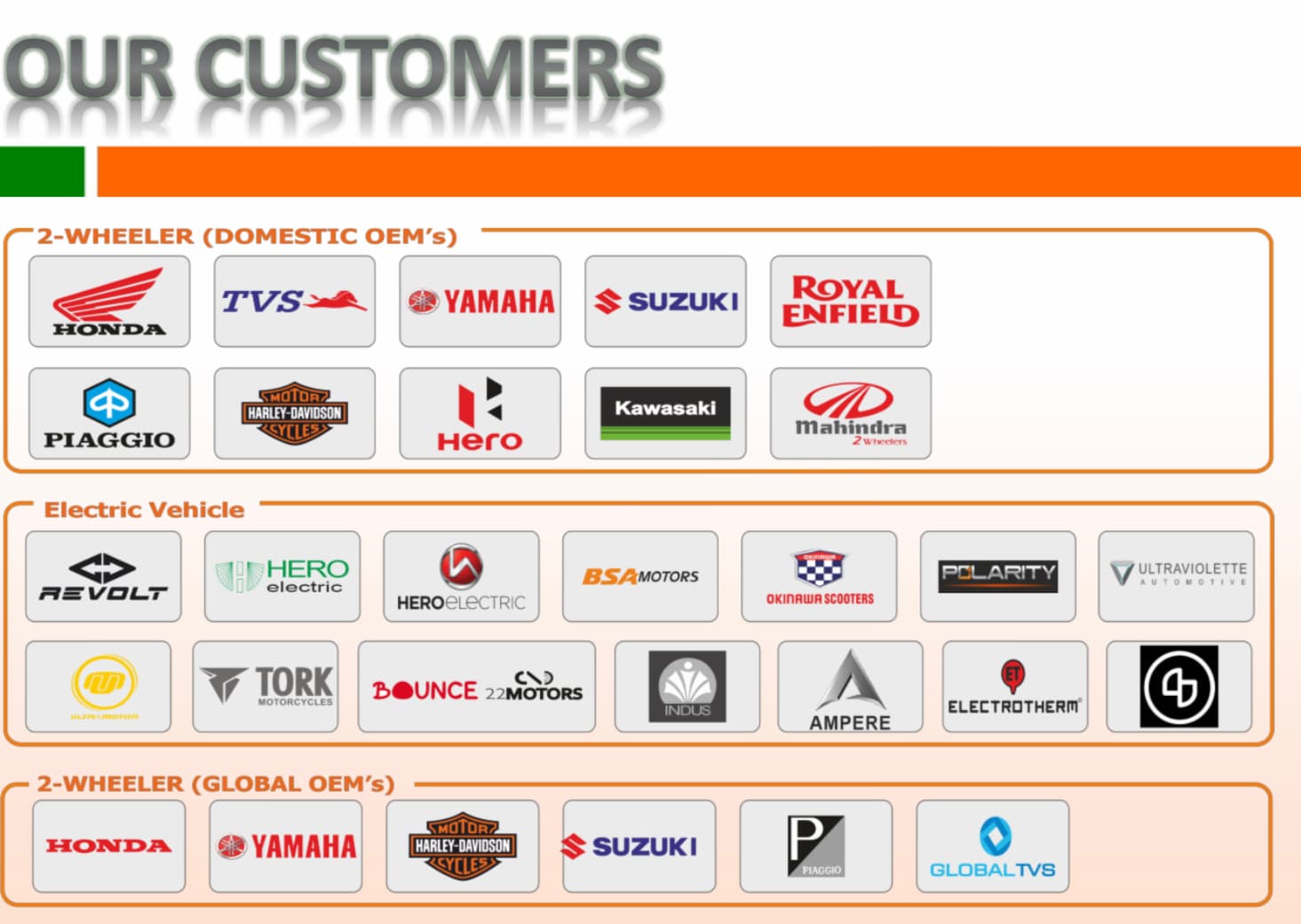

Fiem Industries: Highest ever revenue recorded in the history while the auto industry, two-wheelers in particular de-grew by 3.5%. The company doubled it’s profit and guides for more than 80 projects in development for OEMs, and customers. Hero MotoCorp and Yamaha providing a strong support to the company with new models launching very soon. EV segment volumes grew a whopping 464%, although it was on a small base, the future looks promising. EV two-wheeler brands like Ola, Okinawa, Hero Electric and many more prefer Fiem as their supplier and more such brands are to be added going ahead.

QnA Highlights:

-

Newly added customers such as Ola, and various other smaller segments grew more than 70-80% YoY contributing to the overall growth of the business. Yamaha still is and will remain the highest contributor in revenue, the relationship has always been very strong. They believe the worst for auto (two-wheelers) is behind us. 30 crs capex at Hosur plant and 10 crs to 20 crs regular maintenance/small capex. LEDs, now contributing about 44%, will go up to 55% to 60% over the next three years. Mirrors & plastic part also witnessed growth this year, with OEMs buying complete sets of components (LEDs, mirrors etc.)

-

All new projects are now under LEDs, now it is almost 2x of conventional lightings. There is clearly possibility of other components such as mirrors & plastics also picking up pace. Guiding, conservatively, for 15-20% growth in the next year provided the industry supports. Margins to remain stable at 12-12.5%.

-

The products of Fiem doesn’t fall under any of the PLI scheme issued by the Govt. March 22 debt - 50 crs, Jun 22 debt - 20 crs, By Dec 22 the company will completely debt free.

-

The total contribution from EVs in the last year was 40 crs. The guidance is for 3x the current revenue rate from EVs in the next couple of years.

-

The current capacity utilization is around 78-80% and even with the current mix the company can do business on the upwards of 2000 to 2200 crs. But as the mix changes with LEDs share increasing, the capex planned will be fruitful. The limits for debtors and creditors is being given in the industry, and whatever surplus or deficit is remaining in the working capital is due to the inventory stocking esp. electrical components due to shortage in the global market. The joint venture to enter into four-wheelers is temporarily on hold as less interest is being shown in the industry.

-

The planned capex is for land buildings & machineries adjacent to the current plant itself. The asset turn should come around 6x i.e. 300-400 crs., but this should be considered as overall asset turn at Hosur plant. Greenfield in LEDs have asset turn of around 2x.

-

LED Luminaire, D2C light bulb brand, is no more a focus area.

Key points quoted as it is from the management:

“I am sharing the wallet share of our top four customers. HMSI, headlamp 40%, tail lamps 76%, winker 85% and RVM, we are sole supplier at 100%. TVS, 73% headlamp and tail lamps 69%, winker is 82% and RVM is 55%. For Yamaha, headlamps is 91%, tail lamps is 64%, winker is 5% and RVM is 32%. For Suzuki, headlamps is 80%, tail lamps is 80%, winker is 23% and RVM is 100%”

“We have told earlier we were the first in India to put the SMT plant way back in 2002 where at that time nobody was knowing what is LED. So, we started with automotive lamps in Europe. So, that was our beginning. Naturally, we are way ahead and we put up. Now today, we have the seven SMT line machines with us. So, we have an edge over our competitors.”

With the auto downcycle rotating upwards, I believe this company and the management has the potential of growing their business consistently and creating wealth for their customers, OEMs, as well the investors.

Disc: invested

9 Likes

Fiem Inds - Better late than never – reiterate LONG - 75% Upside - Equirus Targer 1794.pdf (451.2 KB)

FiemIndustries-CompanyUpdate-June2022_112557_665fe.pdf (1.0 MB)

4 Likes

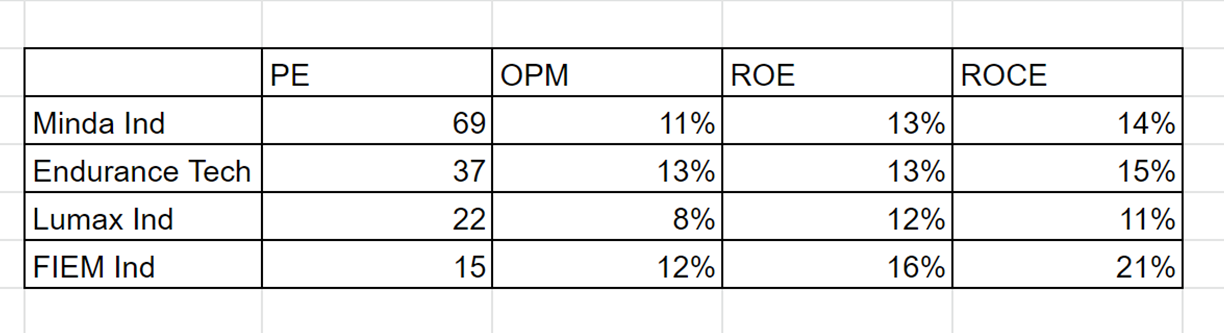

The report shared by @rcinvestor999 and some other data from screener shows:

Except for Fiem, others also have reasonable amounts of debt on their balance sheet. What could be the reason for such a low PE (no rerating), is something unseen or being missed on our end of the research?