Thanks for the reply. You posed some really good and valid questions.

You are right about Industry tailwinds that will ensure PE rerating and top-line growth.

My view is on the first question is: Right now, the market is in its early phases. Tracking standalone macro indicators in my opinion can be misleading and can lead to mistaking correlation for causation. An electric scooter revolution has not happened anywhere in the world except ………… China.

I do think one can analogize the pattern that took place in China and apply it to India. We can try to see the indicators that led to its boom over the last 10 years (Before expanding on that, I am aware that this analogy may have many holes as India is not China but still, this can be worth a perspective).

China had many things going for it. It had a really strong decadal GDP growth and per capita income growth combined with strong companies/start-ups pouring money and government subsidies/support which has led to its boom. Not to forget the great infrastructure of roads in most of the major Chinese cities that also help influence demand.

So, I do think to anticipate the demand, one has to take all the factors into context which makes forecasting extremely hard.

But China is a little different than India and some measures they take will be unimaginable from Indian context. A few things I learnt somewhere on a forum while scrolling on internet:

-

There is a ban of gas-powered motorcycles in major Chinese cities. Laws which govern electric scooters are a lot less strict. Such extreme measures are unlikely to happen in India.

-

Moreover, Gas powered Motorcycles are considered ‘vehicles’ there and the drivers have to drive in vehicles lanes, obtain a licence, follow the same traffic rules and pass an annual inspection. Can’t see that happening here.

One thing that will certainly boost this space is larger government subsidies and better infrastructure as it did in China. Currently, FAME-II subsidies are Rs 15,000 for electric two wheelers. On the contrary, any removal of subsidies will deal a big blow to manufacturers. (Indian governments do have a tendency to surprise you from time to time).

India is a price-sensitive market as of now. Moreover, the public probably needs confidence in buying an electric scooter (or kind of social proof that this thing will work well. Most people I know still have second thoughts on buying an electric scooter). I would bet on the odds that their market share will grow with GDP growth and industry shift over the longer term. But don’t know when.

The second question is a really important one. Because it signifies having some sort of moat with respect to competitors.

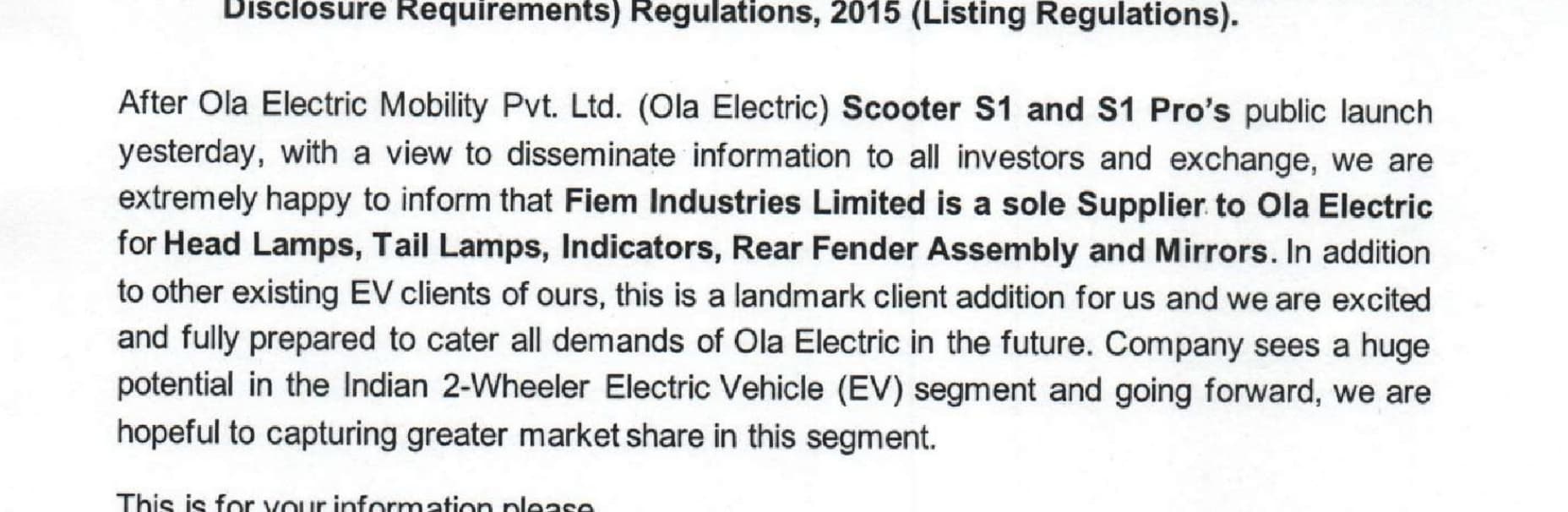

I think many factors combined together have led it to break into EV scooter supply chain. I do think a major factor is how the management runs its business. They mentioned how they got Ola business.

Basically, in any business, any new customer comers or any OEMs give business, based on, QCDDM, how is your quality, how is the quality rating with the existing customers, how is your factory, how much you are better equipped than your other, how is your design capability, how is your basically electronic capacity, as I told earlier that we were the first in India to put up the SMT line. Today we have most of thing in-house which our competitor doesn’t have. So, basically, it depends how better you can do as compared to your competitors. So, based on QCDDM, they select you and based on that we got the order from Ola also.

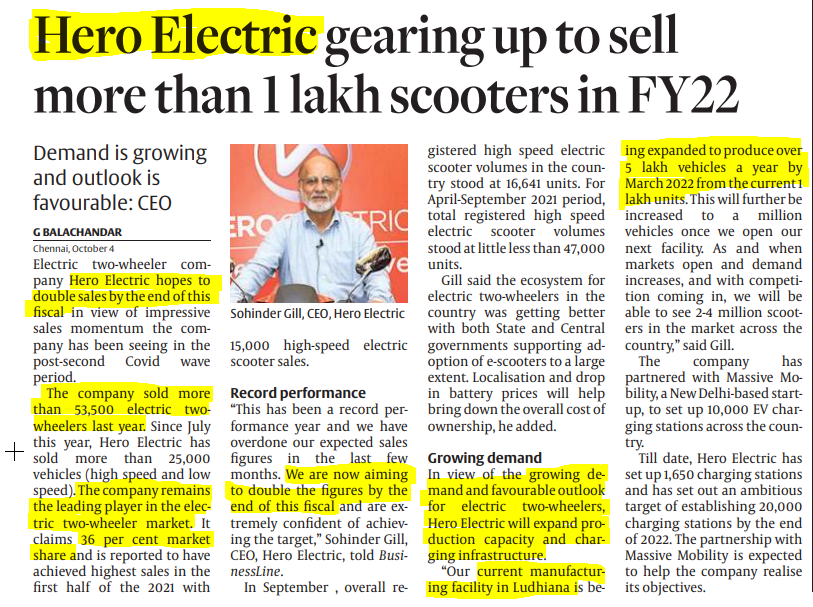

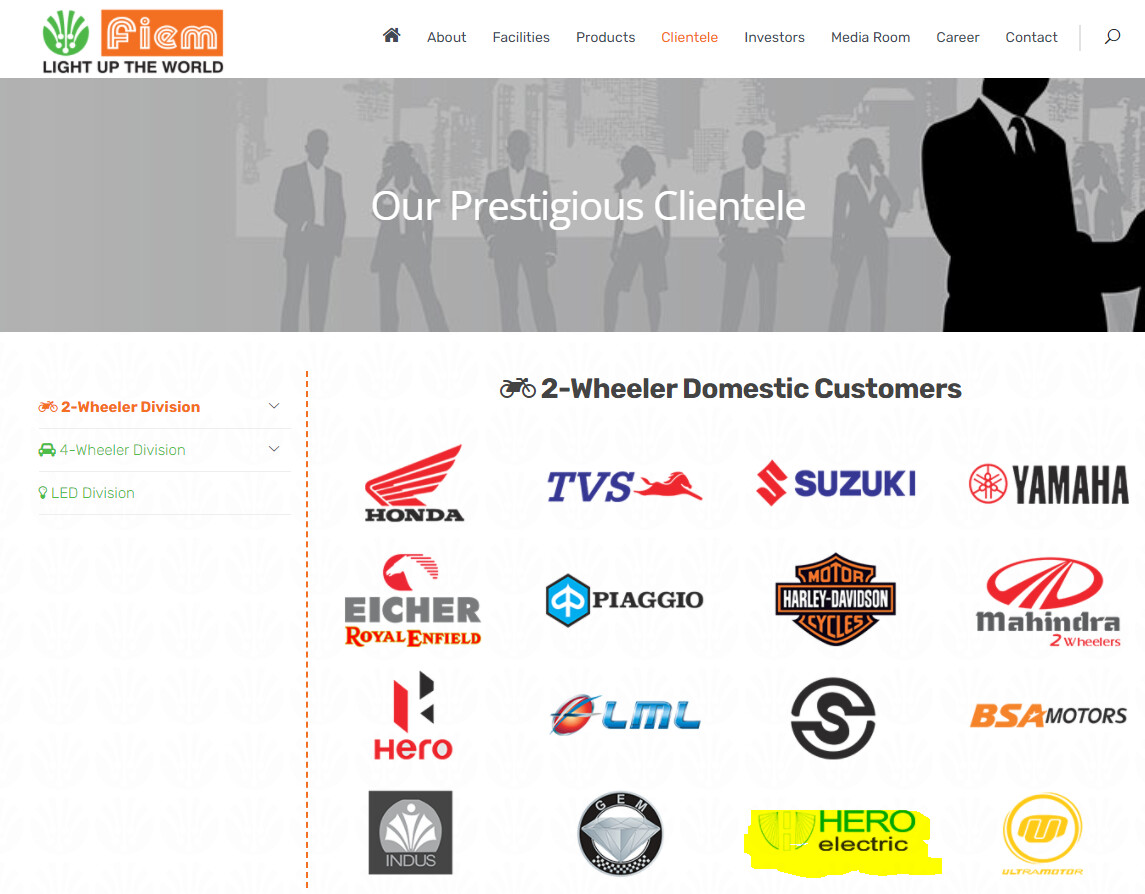

I presume a culmination of all these factors helps and not a single factor alone. The good news is that they have broken into the supply chain of most EV’s (most recently Hero) and retained customers at large which does show some advantage, even though I can’t exactly pinpoint which was their X-factor.

(Incidentally, most concalls often have ‘Lucky Investment managers’ posing many questions, which means famed investor Ashish Kacholia is also closely tracking this space)( Also, most concalls have questions on the financials and numbers, not on the technical side/advantages of business which is disappointing)

The geographic location of factories also helps (but to an extent I think, not much). It helps that they have a few plants in the South (3 TN, 1 KAR) and North(2 HR,2 RAJ, 1 PB). Only one in Gujarat. They said of this advantage for Ola order.

Yes, as you know, that our Hosur plant is strategically located near Ola factory in South India. We are thus very well positioned to handle the Ola business. And moreover, whenever the capacity is required, as I told earlier, we have enough land. So, it can be built in four to five months it can start production, as to their requirements.

They also do mention that price dynamics play some part in their contracts and that explains why most auto ancillaries are squeezed in OPM numbers.

They claim that they give a lot of focus to R & D and some advantage on that front. They did mention it once. (May 2019 concall)

Basically, our products come into esthetics. If you remove lamps and mirror out of any vehicle, it becomes a structure of steel or plastic. So, basically, the development of the lamp is very, very imperative and if you don’t have the R&D in-house, then you can’t compete in the market. Because of the R&D in-house and because of the R&D state and because of the capability of R&D, we are getting the newer models and you can compete the world. Today, as a non-Japanese company, we are competing in this segment is a big thing. It is not a small thing. Basically, this is because of the R&D capability. If there is no R&D in the company, I think that company will die not slowly and it will die very soon. Through the basic strength of R&D, we are surviving since long. In our company, basically the R&D is playing a big role.

On top of that, they bought a company in Italy which handles all design-related tasks and is a technical center for them. They work with the customer and with help of the subsidiary design every product (they can’t copy).

I wouldn’t take the management’s word as gospel (as one never should) and see over the next quarters how the advantages they claim have helped them get new customers while retaining old ones.

Other than that, I do think studying Lumax and Rinder more deeply can give some important insights about this space and can help one see this scrip from a competitor’s point of view and see what other technical and non-technical advantages they do have.