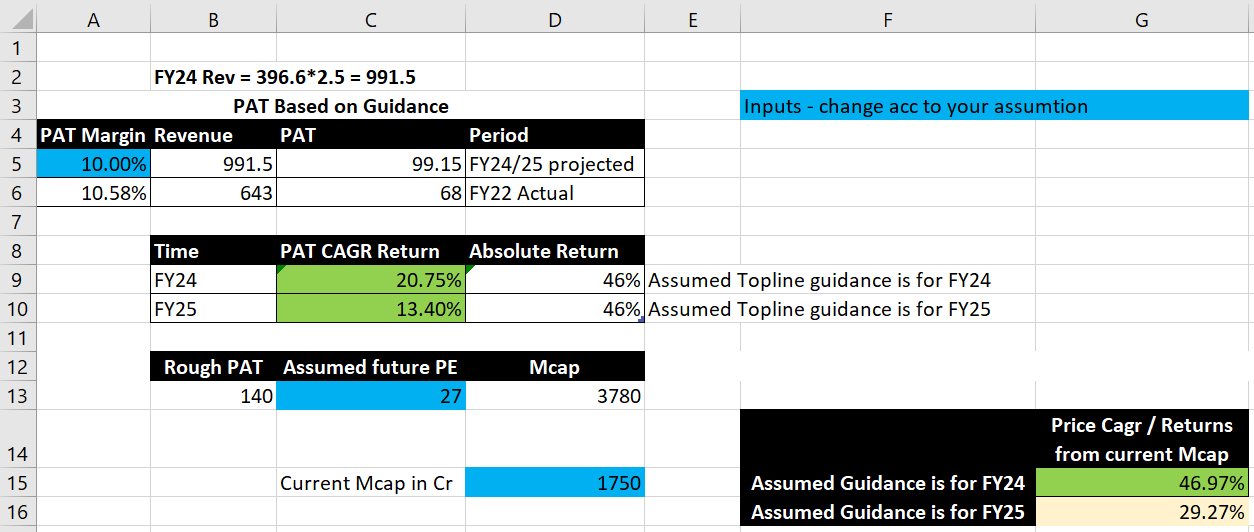

Assumptions

1.Rev increase to 2.5x of FY21 (396Cr) = Approx 1000 Cr

2. Pat Margin of 10% will maintain

3. Considered topline guidance for both Fy24/25

4. PE of 27 . Median PE has always been around 30

Thank you

Current Capex = more than 50 % of capex they did last 7 years…so we can now assume what growth we can expect…with 10 % minimum…and passing RM prices with Lag…so that will give answer.

Capex to be complete by H1 FY23. This is a delay of two quarters compared to

their earlier presentations. No reason has been provided for this delay.

This is disappointing.

The company has set the target of Rs 1000 cr revenue (2.5x of FY21) “in 3

years”, a phrase copied from the previous quarter

presentation. The management does not appear confident about the

timeline. Given the high capacity utilization of the current capacity, the

management was expected to be more confident of selling its products from

the new capacity within a couple of quarters of commissioning, but it does not

appear to be the case.

The company has been unable to pass on the higher costs to the customers over

the last two quarters. Now, they have indicated that the raw material prices

may remain high in the future as well. There is no indication of possible

higher end-product pricing which may result in higher EBITDA. They may keep

end-product prices low in the near term because they need to produce and

sell a higher quantity.

Rs 1000 revenue at 10% PAT margin and PE of 30 gives a target

market cap of Rs 3000 cr by FY25. Economies of scale and higher

contribution from value-added products are likely to facilitate a

higher EBITDA margin. Also, it is possible this target can be achieved by

FY24/H1FY25. However, it is better to be conservative given the current

economic situation.

Disclosure: This stock constitutes a small percent of my portfolio. The

above is for educational purposes only. Not a buy/sell recommendation.

Thanks for pointing out. It should be value be 99.15Cr .

You can update in excel attachment & share

Not sure about EV . We can consider EBITDA multiple of 16 & that gives us same Mcap. Fairchem Organics Valuations_with_EBITDA_multiple.xlsx (13.8 KB)

Other Oleochemical companies such as Fine Organics (53x EBITDA) & Galaxy surfactants (25x EBITDA) won’t be a fair comparison in my opinion

Is company misallocating any capital?(Red Flag) CWIP for capicity expansion is increasing a lot. (43 cr is not yet operational)

Dividends- Is paying dividends. Last year it paid - 0.17% yield. It is negligable.

EBITA/CFO and CFO/PAT ratio for last 3,5 years

| Year/Ratio | 2022 | 2021 | 2020 |

|------------|-------|------|--------|

| CFO/EBIDTA | 24.2% | 35% | 34% |

| CFO/PAT | 60% | 93% | 89.82% |

CFO on March 2021 - 39.58cr where as revenue is 55 cr however,

CFO on March 2022 - 40.48 cr where as revenue is 91 cr. Even though there is a 1.5x of revenue there is no increase in CFO. Which is alarming red flag.

Why this is happening?

CFO - 65.48 cr

Inventory incresed from 18.16cr in 2021 to 30.37 cr in 2022 - 12cr gap

It looks fine to me. Ratio of inventory/revenue remain around 33% Hence it is not happening at CFO level

Trade receivables is 46.76 to 62.22 cr in 2022 - 14cr gap

Trade receivables to revenue decreased. This looks good to me.

14+12

CFO is getting suppressed due to rapid increase in revenue. Here money is getting struck due to the rapid increase in revenue.

Does promoter have private entities in same line of business?

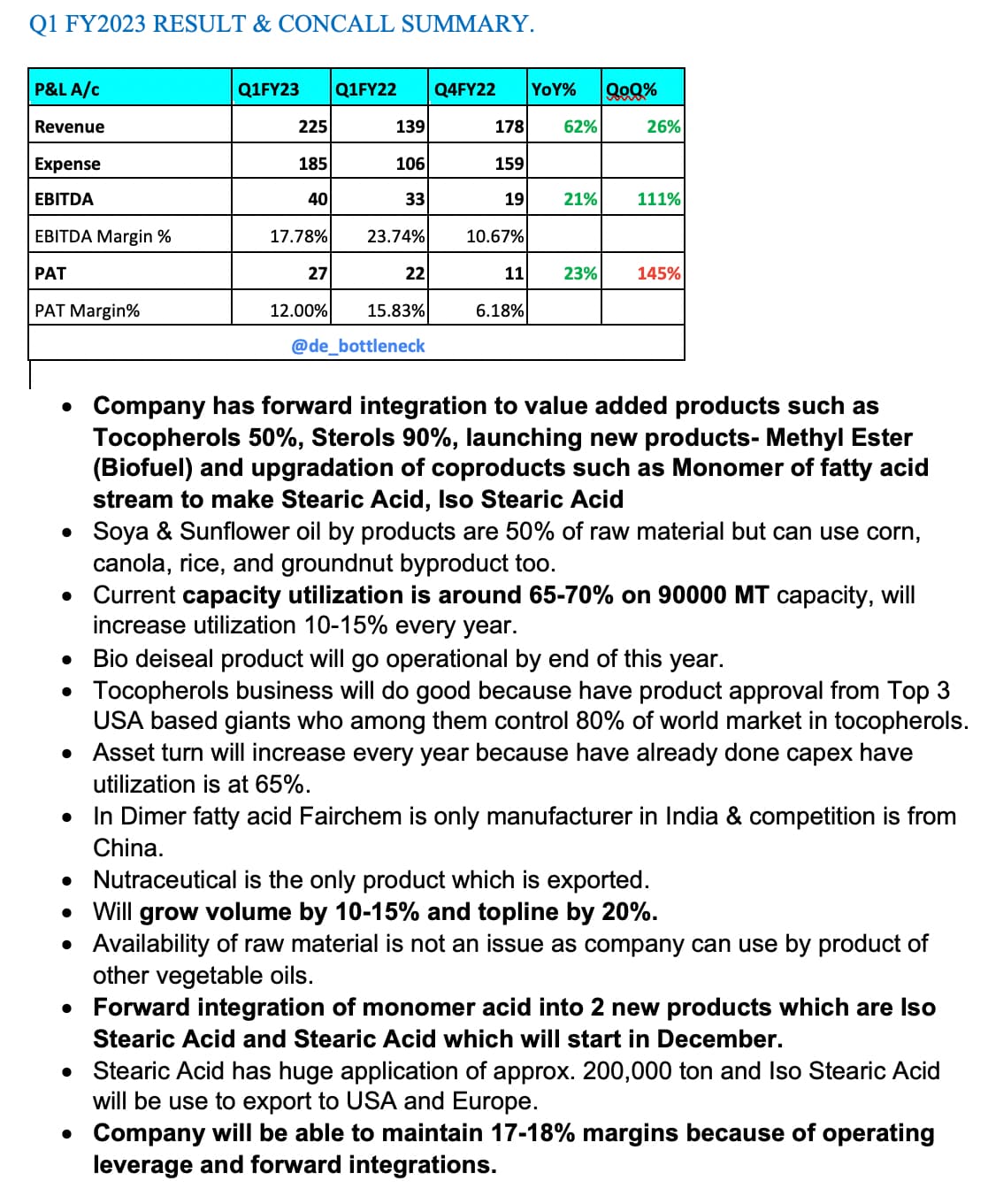

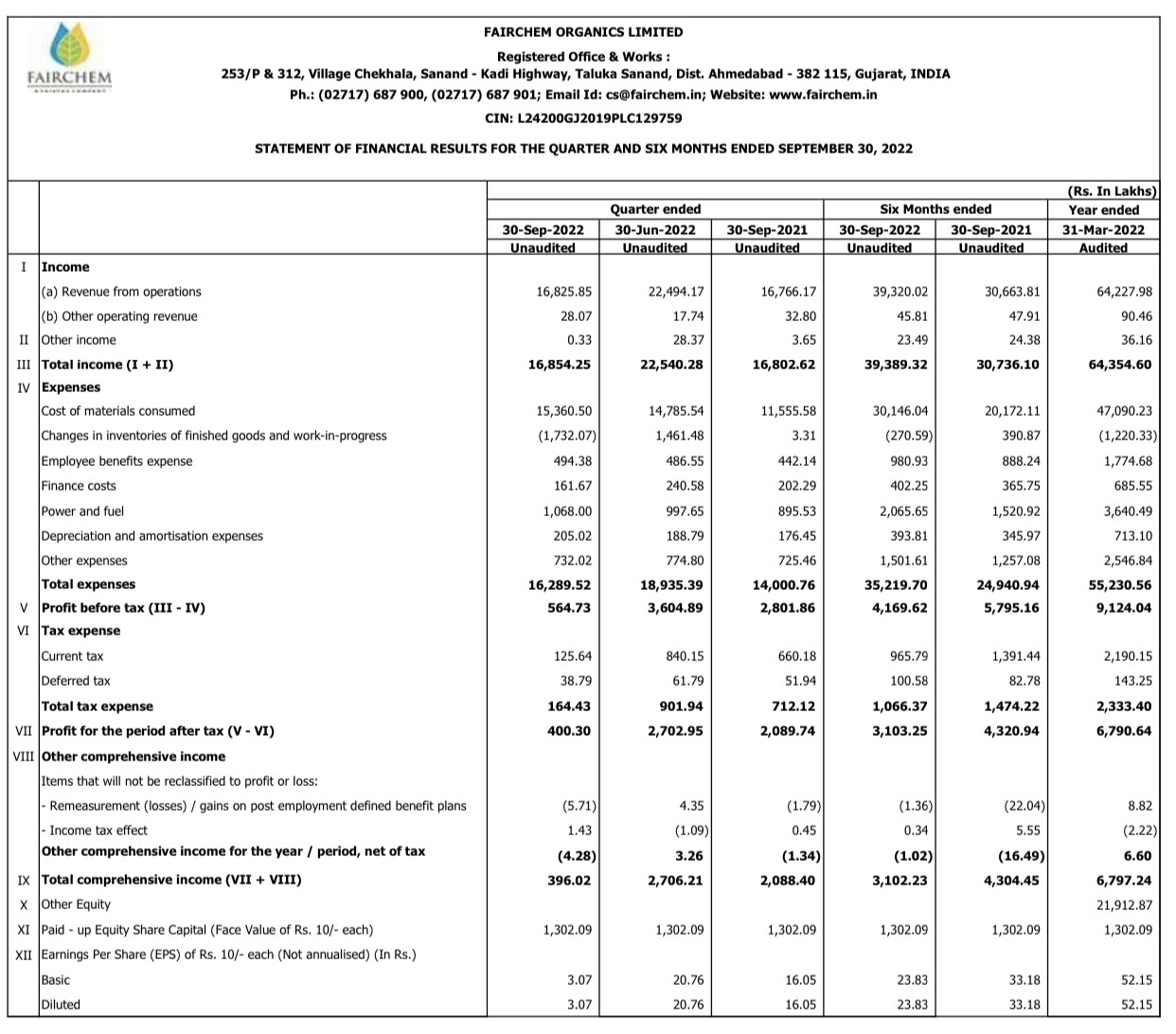

Superb results by Fairchem Organics. If you extrapolate 1Q EPS for FY23 you get 20.76 X4 = Rs83.04. At Rs1998 stock price stock trades at 24x FY23E which is one of the cheaper chemicals stocks.

Company guidance of Rs1000crs revenues for FY24. Extrapolating Q1 PAT margins of 12% that implies Rs120crs PAT in FY24E which implies at current market cap of Rs2600crs stock trades at 21x FY24

For the first time, the company has shared a very detailed investor presentation, which is able to depict the management’s confidence in the future of the company in a way the previous presentations could not.

Has anyone done a comparison between FAIRCHEM and FINE ORGANICS …since both deal in ole-chemicals …just the RM for FAIRCHEM is used oils whereas FINE uses PALM oil so import dependency but it has price elasticity.

Where FINE scores is the customer which are FMCG companies so it again doesn’t have to do a price bargain, whereas FAIRCHEM majorly supplies to PAINT companies so it is like a commodity chemical.

If anyone can do a comparison on SCREENER(paid version has option) and share here it would be helpful.

Baba Ramdev is also into olechemicals manufacturing business…but non related …but can scale it if he intends to …can be league of FAIRCHEM,FINE …And biggest advantages is that he has raw material sorted as he is cultivating palm on 6 lakh hectares of land allocated to it in INDIA