See the 1QFY23 conference call transcripts. Management talked up the company. Said last year’s problems were behind them. Pumped up the stock price to Rs2000 plus and then delivered a very bad set of numbers

4 Likes

Exactly!

The margin guidance was 16%-18% in the last concall. Need more clarity on this.

If someone plans to attend the next concall, please ask abt this (I’m sure everyone attending will ask this anyways ![]() )

)

I have not seen any Earning call for Q2 FY23 , I think they skipped it this time , does anyone have any Q2 call minutes ?

1 Like

Is anyone tracking this company? Very poor set of results yet again and no clarity from management on the sudden decline in performance

3 Likes

They have indicated in the investor ppt saying it (reduced revenues) was due to the reduced demand from the paint industry and not due to missing out of any customers.

I was going through the numbers to see if it was right to trim my holdings due to the poor set of numbers, deciding not to trim. good management team, solid moat, 10-15% compounder with great return ratios.

1 Like

What I hate about companies like Fairchem is the fact that they stop concalls as soon as results go bad. On a lighter note, their name has “Fair” but they are not fair to their investors…:- ![]() Investors need more explanations and clarifications (hand holding) when things go bad and not otherwise round…

Investors need more explanations and clarifications (hand holding) when things go bad and not otherwise round…

Disclosure - sold at loss after last quarter fiasco. Happy to remain away from this stock

7 Likes

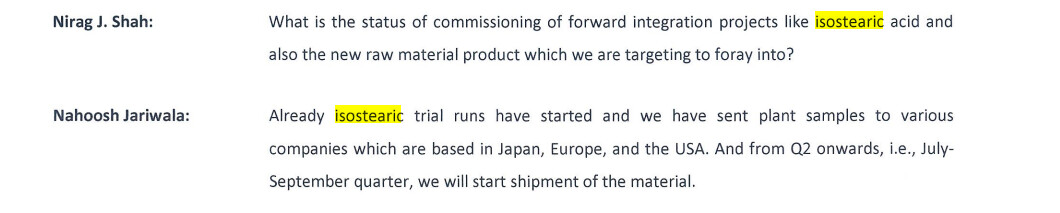

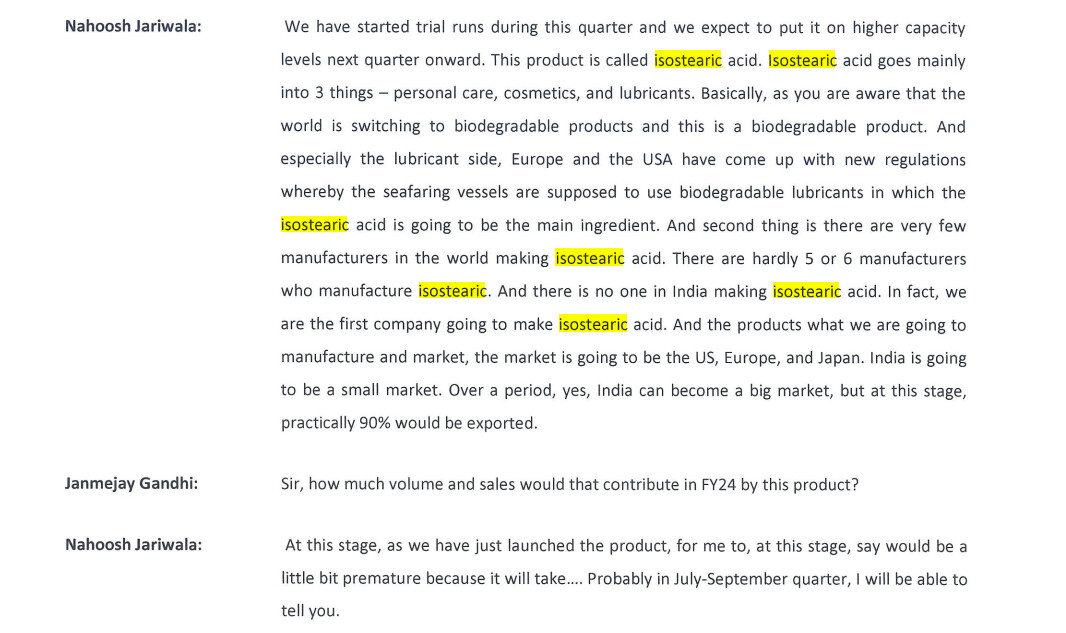

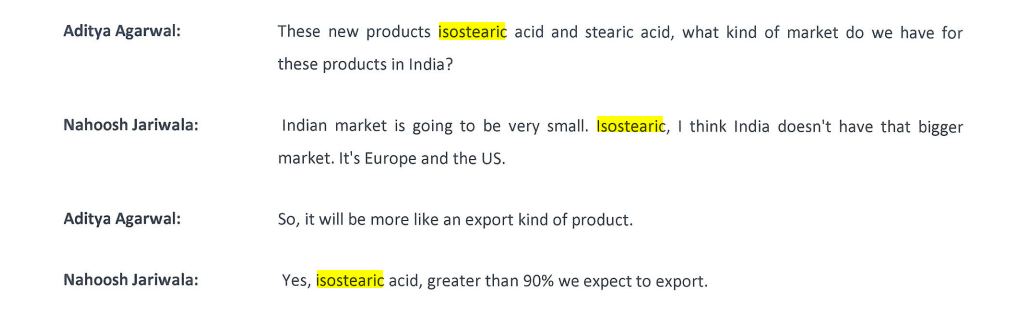

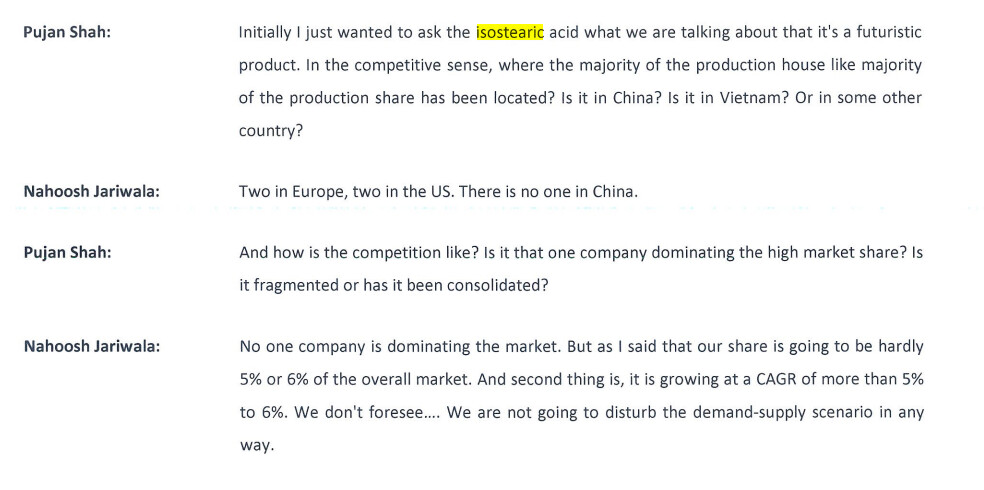

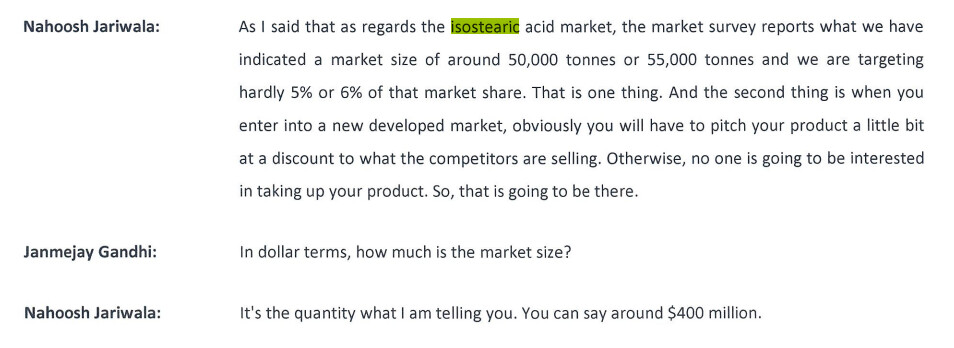

company will be switching it tocopherol capex plan with isoteraic acid.

isoteraic acid is only manufactured by 4-5 players in the whole world. very difficult to make, fairchem will be coming up with a capacity which is just 6% of the total market (lot of headroom to grow in future).

isoteraic acid is high margin, higher than current business.

Europe and the USA have come up with new regulations

whereby the seafaring vessels are supposed to use biodegradable lubricants in which the

isostearic acid is going to be the main ingredient. And there is no one in India making isostearic acid.

concall info

8 Likes

Source: Transcript Document

Summary: Isostearic capex completed, deliveries starting Jul-Sep qtr onwards, 90% export, Co targeting 5-6% marketshare of a product that is 50K-55K tonnes and $400M value (i.e. $20M = ~160Cr). Only 5-6 manufacturers, no dominant manufacturer, 2 in USA, 2 in Europe, none in China/Vietnam/India, market growing 5-6%, so Fairchem entry will not put pressure in market as of now, but pricing might be discounted due to new entry. Questions: 1) Will the Isostearic market demand grow upwards to current 5-6% growth? 2) Do current players have capex plans?

8 Likes

Fairchem came out with a decent set of results, with sales growing by 45% and margins reviving to 13%. Management is very bullish on quick scaleup in isostearic acid which seems to be the near term growth driver, along with continued margin revival. Concall notes below.

FY24Q3

-

Sales volume increased by 2.64% and value decreased by 2.8% quarter-to-quarter

-

Process quantity was 15,277 MT (4.9% lower on Q-o-Q). 15% higher on 9MFY24 vs 9MFY23

-

Q3 Dimer acid: 2,000 tons, linoleic acid: 7,000 tons

-

9M Dimer acid: 6,000 tons, linoleic acid: 22,000 tons

-

Isostearic acid :

-

10 MT export shipment to EU in December, revenues not booked as they book revenue once customer receives shipment (CIF basis)

-

Overall capacity of 2000 MT and hope to reach full utilization in December 2024

-

Croda, Arizona have higher capacities

-

Will allow them to better compete with Chinese on dimer acid as isostearic acid scales

-

Differentiated product, required 5-6 years of development to manufacture because technology is not available off the shelf

-

-

Export : 10% of sales in Q3. Will not face delay due to Red sea crisis for US exports

-

Linoleic acid : China doesn’t compete because of high freight component

-

Overall capacity: 120,000 MTPA. 80,000 MTPA dedicated towards current products including isostearic acid and 40,000 MTPA are earmarked for new projects. Have adjoining land for expansion if required

-

Growth focus will not shift towards introducing higher value items than just processing more input material

Disclosure: Invested (position size here, bought shares in last-30 days)

6 Likes

Fairchem came with flattish results (6% sales growth, flat EPS), however the internals look very strong. They grew volumes by 13% in a tough year and are confident of double digit volume growth in FY25. Additionally, they are confident that isostearic acid will reach 100% utilization by September 2024 as they have more orders than capacity. Management is expecting 15-16% EBITDA margins by Q4FY25. Concall notes below

FY24Q4

-

Volume growth of 15% QoQ and value decline of ~8% (due to decrease in raw material and finished product prices**). Paint industry volume for them grew by 15%** (higher than industry level growth of 10%) due to increased penetration into existing and new customers

-

Process quantity was 19,000 MT in Q4 and 65,000 MT in FY24 (13% growth in FY24). Expect ~72,000 MT in FY25

-

Linoleic acid: 46% (~286 cr.), dimer acid: 27% (~168 cr.). Not seeing any Chinese dumping in dimer acid (66-70% market share in India, rest is imports)

-

Export: 5% of Q4 sales

-

Isostearic acid:

-

Currently depressing EBITDA margins due to initial losses incurred as loss of material and high utility cost while stabilizing production process and reach desired quality level

-

Did full container load exports to Europe in March and have secured more export orders from existing and new customers (in Europe, USA)

-

Expect 100% capacity utilization by September 2024 and will potentially reach 15% EBITDA margins by Q4FY25

-

Have more orders than what they can fulfill

-

-

The new product they are working on with new raw material is still in R&D and they don’t expect commercialization in FY25. It’s a biodegradable product used in lubricants and other high value applications

Disclosure: Invested (position size here, no transactions in last-30 days)

9 Likes

Hi

Thanks for a conscise summary of concall.

Few things i am trying to understand

- Company doesnt seem to have any pricing power. It seems most of its product are commodity in nature and customers are guiding the terms.(both product price and offtake.

- Company says isostearic acid is high value items. However it also says sales will not be increasing due to this product. How can a product achieve more than 15/18 % ebitda (existing 11%)on same raw material and same sales price?

Please share if you have an understanding for anove points.

Thanks in advance.

Disclosure:-under watchlist . Studying for potential investment. My views are not to be considered neutral.

1 Like

Sharing AR24 notes.

Dimer acid

-

Had developed a process for optimum yield 3-years back which has enabled them maintain their market share in domestic market

-

Started exporting to USA and hope to increase exports in FY25

-

Non-reactive polyamides: used in printing inks, adhesives, paper coatings, etc.

-

Reactive polyamide resins: used in surface coatings & adhesives demand in marine and construction

-

Customers: epoxy hardener, paint, and printing ink

Linoleic / soya fatty acid

-

Had improved quality of product 5-years back

-

Have been able to sell these to another Indian customer for a different application in last-12 months which seem sustainable

-

Both linoleic acid and Soya Fatty Acid are used for making Alkyd Resins which in turn is used in making paints

-

Customers: paint, printing ink, and oil drilling

Isostearic acid

-

Expects to do good business with remunerative prices in Europe and USA

-

Mainly used in Lubricants and Cosmetics industry

-

Only 6 to 7 global manufacturers, Fairchem is the first Indian manufacturer

-

Customers: lubricants

Intermediate nutraceuticals

-

Manufacture (natural) Tocopherols and Sterols – both are intermediate nutraceuticals and are exclusively exported and used in pet foods and food (prevents rancidity)

-

Did limited business in FY24 and will continue with this in future

-

Customers: vitamin E manufacturers

Revenue breakup

-

Domestic: 579.06 cr. vs 614.58 cr. in FY23

-

North America: 34.93 cr. vs 26.31 cr. in FY23

-

Middle east: 1.55 cr. vs 4.63 cr. in FY23

-

East Asia: 0.81 cr. vs 0.81 cr. in FY23

-

Others: 1.96 cr. vs 0 in FY23

Miscellaneous

-

15% increase in sales volume

-

Capitalized 44.64 cr. of CWIP

-

Top 2 customers: 195.11 cr. (vs 236.07 cr. in FY23), 62.04 cr. (vs 9.62 cr. in FY23)

-

Foreign earnings: 41.25 cr. (exports to 5 countries)

-

Foreign outgo: 58.9 cr.

-

R&D: 16.26 lakhs

-

Median salary increase: 12.05% (21.5% for Nahoosh Jariwala; 2.98 cr. vs 2.58 cr. in FY23)

-

employees: 227

-

Audit fee: 31.15 lakhs

-

Share price: 911.95 (low), 1528.8 (high)

-

shareholders: 32’136

-

Contingent liabilities: 1.05 cr. (vs 0.78 cr. in FY23)

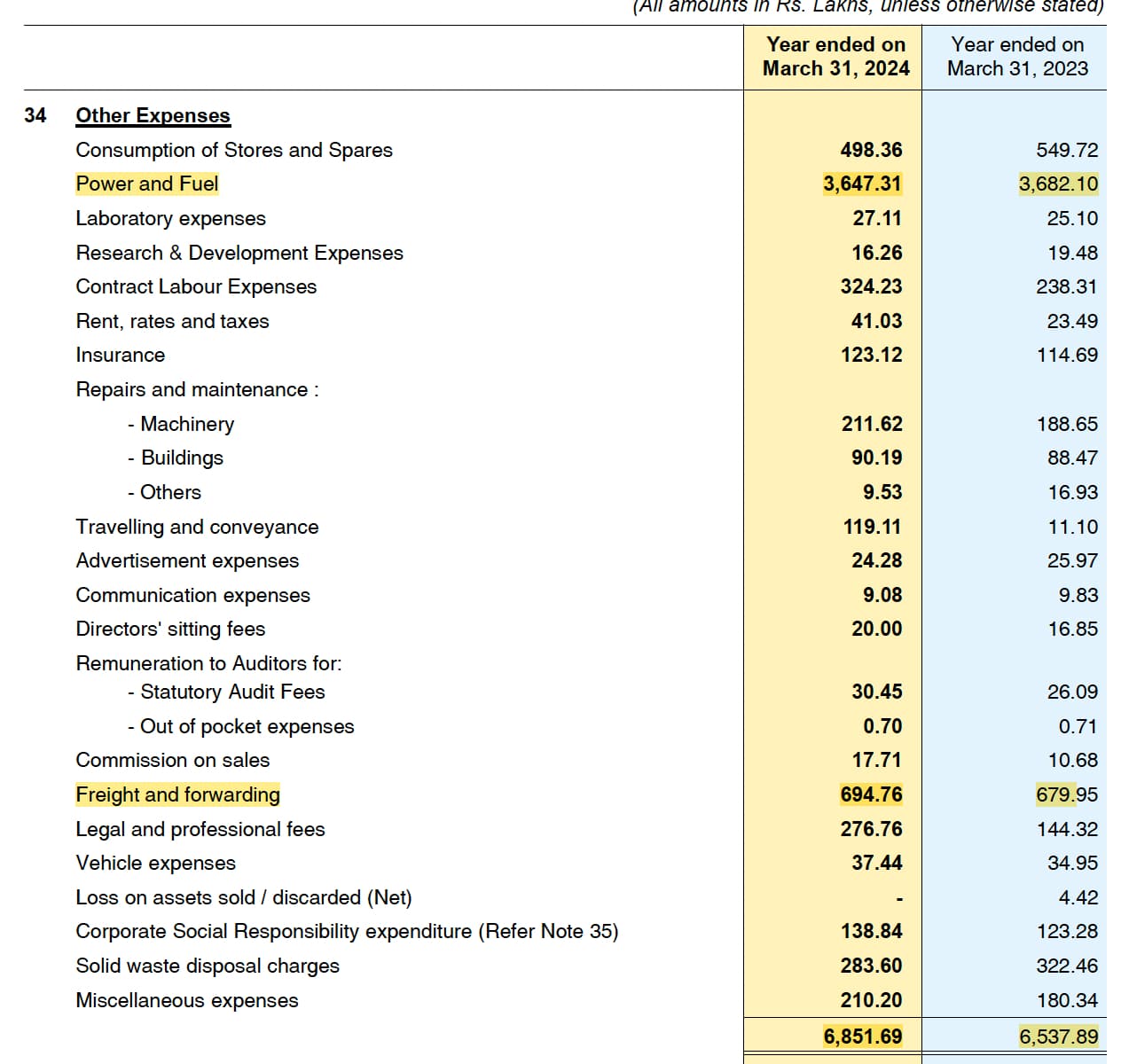

Other expenses

Disclosure: Invested (position size here, bought shares in last-30 days)

3 Likes

Fairchem Q1FY25 concall lasted just 9 minutes! They have made full load sample shipments of isostearic acid for customer approvals, 3-6 months approval time. So, Q3 (Dec '24) onwards we should be seeing full shipments and I suspect decent margin expansion. No interest from investors at all. Only 1 question (good one, not for the sake of asking something) asked, ha ha! Surprised to see this.

Disc: Invested

3 Likes

From Q1-FY25 concall

Management mentions they are working on something akin to Isostearic acid, another novel product. Only a few companies worldwide produce it, and none in India. They’ve indicated that while it’s difficult to provide a precise timeline, updates will be shared during con-calls once pilot plant runs are successful.

3 Likes

this company has very less gross margin to be called as speciality chemical company. anyone know what is the reason for such high material cost?

Fairchem came out with a disaster set, their key raw material prices have increased and finished prices are facing competition from China + their main paint customer (Asian paints) is struggling to grow. Also, isostearic rampup has been much slower than previously guided. Q3 will be another disaster because the full effect of RM increase will come in. Sharing concall notes from last few calls.

FY25Q1

-

Linoleic acid ~45%, Dimer acid ~22%

-

Sale volume: 16,728 MT (vs 16,314 MT in Q1FY24, 17,584 MT in Q4FY24)

-

Isostearic acid

-

Made several full container load export shipments to Europe and US, received additional orders for exporting Isostearic acids to other locations for existing and new customers

-

Stability test requires 3-6 months followed by trial order and then full container load orders

-

Material is under analysis with 15-20 new customers

-

FY25Q2

-

Quarterly sales volume: 14,000 MT+ (vs 16,728 MT in Q1FY25)

-

Linoleic + dimer acid contribution: 68%

-

Linoleic acid demand was low from paint sector (66% of Fairchem’s supplies are to Asian Paints, they also supply to other paint cos but don’t make similar margins and working capital is worse; so Asian Paints losing market share adversely impacts Fairchem). Q3 also looks bad

-

In September 2024, Government increased custom duty by 22% on certain crude vegetable oils resulting in higher raw material cost for dimer acid production. RM increased and there was no increase in dimer acid prices resulting in margin compression. Must retain market share in dimer acid because isostearic acid is made from the byproduct

-

Q3 margins will be even worse because the full effect of margin pressure in dimer acid will be visible in Q3 and paint demand (absorbing linoleic acid) is low

-

Isostearic acid: initial supplies were going into lubricants, now they are also going into cosmetics (requiring longer approval cycles, but higher margins). Can reach peak annual revenues of 150 cr. (from 3000 MT capacity)

-

Isostearic acid receivables are higher as its export focused and with scaleup, their receivable cycle will increase further

-

Will invest in solar power, payback period of 4.5 years. Looking to finalize land for the solar power plant

-

Not focusing on tocopherol

Disclosure: Invested (even bought shares in last-30 days ![]() )

)

14 Likes

Q2 F5,results are bad, infact, the pain is gonna be there for next year too, until the 3000Ton Isostearic acid comes and contributing the top line, there wont be much of surprise on the upside.

Due to Governmet increasing the import duty for unforseeable future until then the raw material prices are to be elevated, in fact we can expect the margin worse than this too in the coming quarters of this financial year.

Postives:

So the business is totally bad??, Certainly NO, Infact its quite opposite of that, Isometric (High value product - though not certain about this to be high margin business) used in cosmetics too, Like Fine organics.

I liked the management a lot, the promoter is quite transparent , I think they are doing correct things

- Backward integration for key raw material

- Looking for low cost to stay competitive (Setting up solar panels for electricity requirement)

- Getting into adjacencies where they have expertise - which are more value added

For Example: It seems Isometric components can be extracted from dimer acid, if we discount the e current slowdown which is transient in nature, though it may even take 3-6 quarters to even come back to current level of margin and profitability they are expanding their TAM and getting into value accretive adjacencies

They seems to be not interested in products which are not long term beneficial for them, ex: tocopherol, since this product market has already 2-3 players, but the demand is very low , they are not getting into this one, only if they receive specific order than only they are supplying (Cutting off the weeds)

on a side note

One thing is apparent, that paint industry demand is quite low , this is seen across the vendor of that industry, the competition may or may not be playing a bigger , however the data suggest the economic slowdown is real, will be recovered in the second half, mostly fourth quarter onwards

So when asian paint sneezes lot of the players gets cold too anyway I got side tracked

All in all I don’t see any drawbacks specific to the company, the management is competent, the stock may get beaten down much further too in the coming months.

But the future remains bright, since we don’t have clear idea or even predict when does the gov will lift the import duty and demand revival in paints sector, we can’t time the entry, however I believe this stock should at least yield 2-3x in next 3 years from current level, though next 1.5 years it may even beaten down further since the PE is not so cheap. But I m quite optimistic about this company future, if things falls in places , can hold this company up to another 5 years too since the isometric ramp will start to happen after second year and its sticky product (export market), only draw back may be opportunity cost, but its fine

Disclaimer: Invested (Currently in loss, Feeling the drawdown - will accumulate further on the dips over this Financial year)

4 Likes