In public shareholding there seems to be 7 % stake that is owned by privi-promoters related persons and entities like Banbridge and rajesh budhrani. Whether they exit or not and this open offer route is for them to exit will be known only after offer is over. If they tender their shares then I think there will be mandatory OFS again to keep the company listed on exchange.

Can anyone throw some color on how the buying price for Fairchem Organics would be calculated if one held shares of Fairchem Specialty before the demerger? The math for 99.98% in the new entity seems odd to me.

1 Like

Fairfax India holdings has completely exited from Priivi and sold their entire stake of 48.75% to Privi promoters. Total No of shares sold are 1,90,42,828 for a transaction price of Rs. 1222 crores. Price per share work out to Rs. 624 per share.

1 Like

Fairfax India Announces Sale of its Equity Interest in Privi Speciality Chemicals Limited

04/22/2021

Download this Press Release (PDF 178 KB)

NOT FOR DISTRIBUTION TO U.S. NEWS WIRE SERVICES OR DISSEMINATION IN THE UNITED STATES

TORONTO, April 22, 2021 (GLOBE NEWSWIRE) – Fairfax India Holdings Corporation (“Fairfax India”) (TSX: FIH.U) announces that it has entered into an agreement to sell its 48.8% shareholding in Privi Speciality Chemicals Limited (“Privi”) to certain entities affiliated with Mahesh P Babani (“Mahesh”) and D B Rao for INR 12.2 billion (approximately $163 million at current exchange rates). The transaction is subject to customary closing conditions and approvals and is expected to close in the second quarter of 2021.

Fairfax India also intends to invest in Non-Convertible Debentures (the “Debentures”) of up to INR 550 million (approximately $7 million at current exchange rates) to be issued by entities affiliated with Mahesh.

“We have had a great partnership with Mahesh Babani at Privi. We have admired Mahesh’s visionary leadership and believe that consolidating his shareholding is in the best interest of Privi’s future growth. We continue to partner with Mahesh through our investment in the Debentures. We wish him continued success in the future,” said Prem Watsa, Chairman of Fairfax India.

“We have had a long and successful partnership with Fairfax India. This partnership has enabled Privi to grow to its current scale. We believe that consolidating our holding in Privi from 22.7% to 74.1% will facilitate accelerated growth and take Privi to greater heights, through both organic and inorganic opportunities,” said Mahesh P Babani, Chairman and Managing Director of Privi.

Fairfax India is an investment holding company whose objective is to achieve long term capital appreciation, while preserving capital, by investing in public and private equity securities and debt instruments in India and Indian businesses or other businesses with customers, suppliers or business primarily conducted in, or dependent on, India.

| For further information, contact: | John Varnell, Vice President, Corporate Affairs |

|---|---|

| (416) 367-4755 |

Recently, I got to study Fairchem Organics and I composed this article to provide an overview of the company.

Fairchem Organics: Emerging Oleochemicals Leader

A few months back, Fairchem Organics (“Fairchem”) demerged from Fairchem Speciality Chemicals (now Privi Speciality Chemicals) and got listed. There is not much analyst coverage of this company. A few days back Moneylife printed an article titled “Fairchem Organics: Exceptional Growth.”

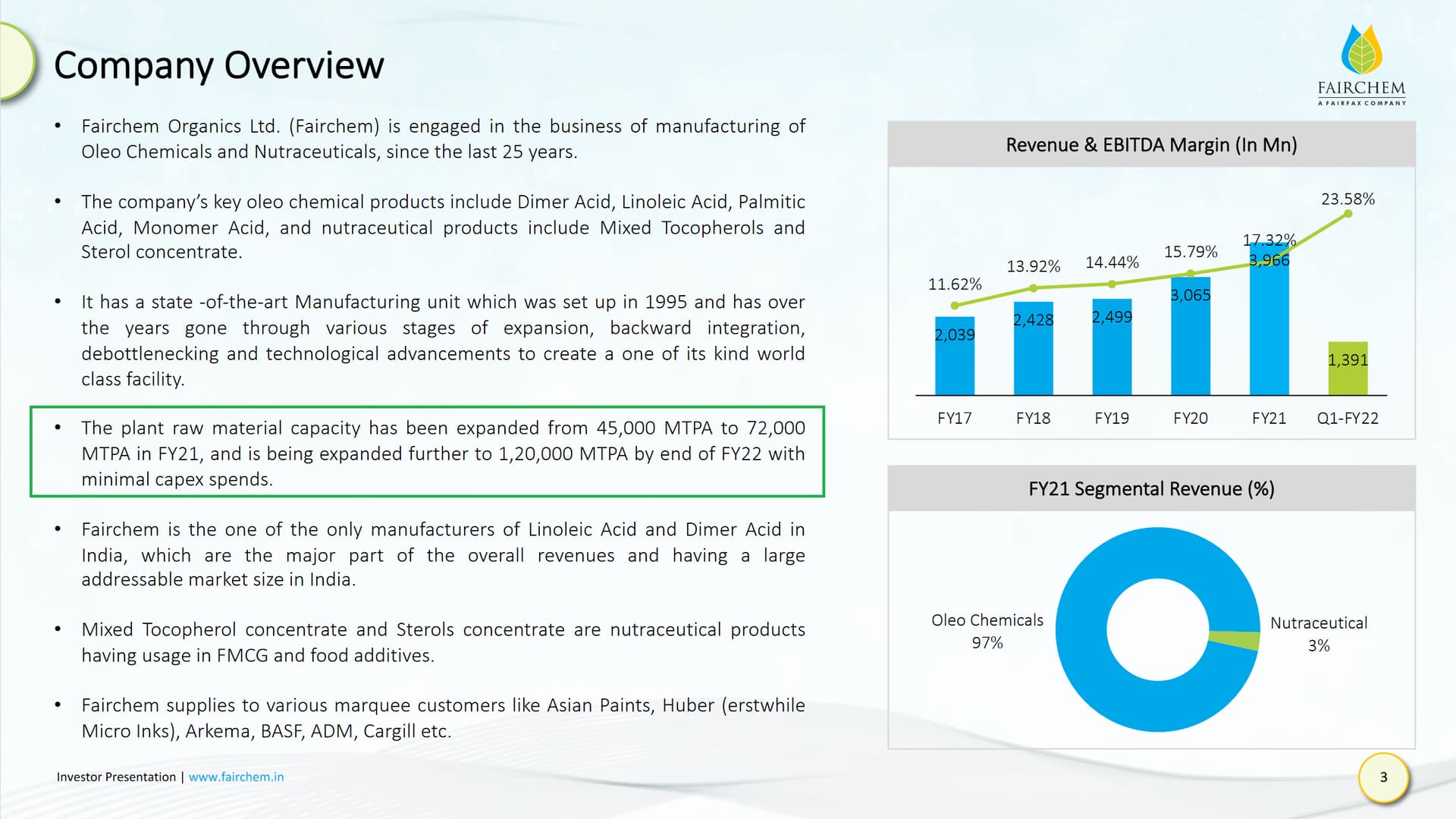

Fairchem’s products are classified under oleochemicals. Oleochemicals are green replacement for petrochemicals. Oleochemicals are derived from vegetable oils and constitute 7.5% of the speciality chemicals market in India. They are used as food additives, plastic additives, pharma additives and surfactants. Oleochemicals worldwide demand is likely to grow at 7.57% CAGR between 2021 and 2028.

Fairchem: Emerging Oleochemicals Leader?

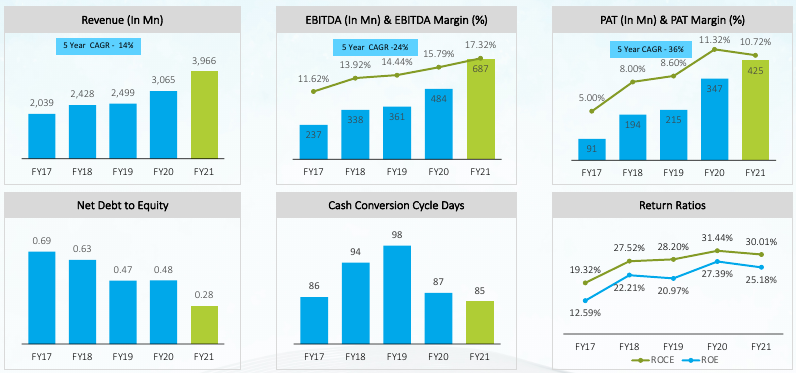

In summary, Fairchem Organics is an established, fast-growing, low-cost manufacturer of certain oleochemicals. Fairfax India Holdings, backed by the billionaire Prem Watsa, is the major promoter of Fairchem. The company completed its capacity expansion from 18K MTPA to 45K MTPA between FY14-FY16, and to 72K MTPA in FY21. Within FY22, expansion to 120K MTPA and forward integration will be complete.

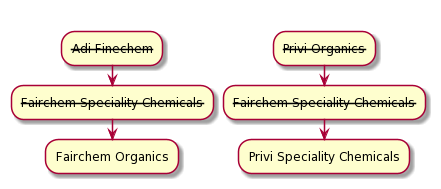

History: Mind the Names

Back in 2016, there were two companies: Adi Finechem (listed company) manufacturing oleochemicals and Privi Organics (unlisted) manufacturing aroma chemicals. The end-markets of both the companies have been fast growing. In 2016, Fairfax India Holdings acquired controlling stake in Adi Finechem, and bought and merged large part of the Privi Organics business into it. The resulting entity was named Fairchem Speciality Chemicals.

Oleochemicals and aroma chemicals businesses are very different. So, the two businesses parted ways. After various activities of mergers, capacity expansions and demerger, the end result in 2021 is two companies:

- Fairchem Organics (listed), focused on oleochemicals, is promoted by Fairfax.

- Privi Speciality Chemicals (listed), focused on aroma chemicals, to be controlled by the promoters of the erstwhile Privi Organics; 48.8% stake to be bought from Fairfax.

Since Fairchem Organics is demerged recently, its pre-2020 results are not accessible via the usual means.

The investor presentation does depict the highlights of the results from FY17. The pre-2016 results of Fairchem Organics business, when it was Adi Finechem, are the pre-2016 results of what is now Privi Speciality Chemicals. Between 2017-2020, the results of Fairchem Organics are (with likely small discrepancies) the standalone results of what is now Privi Speciality Chemicals.

High Entry Barriers

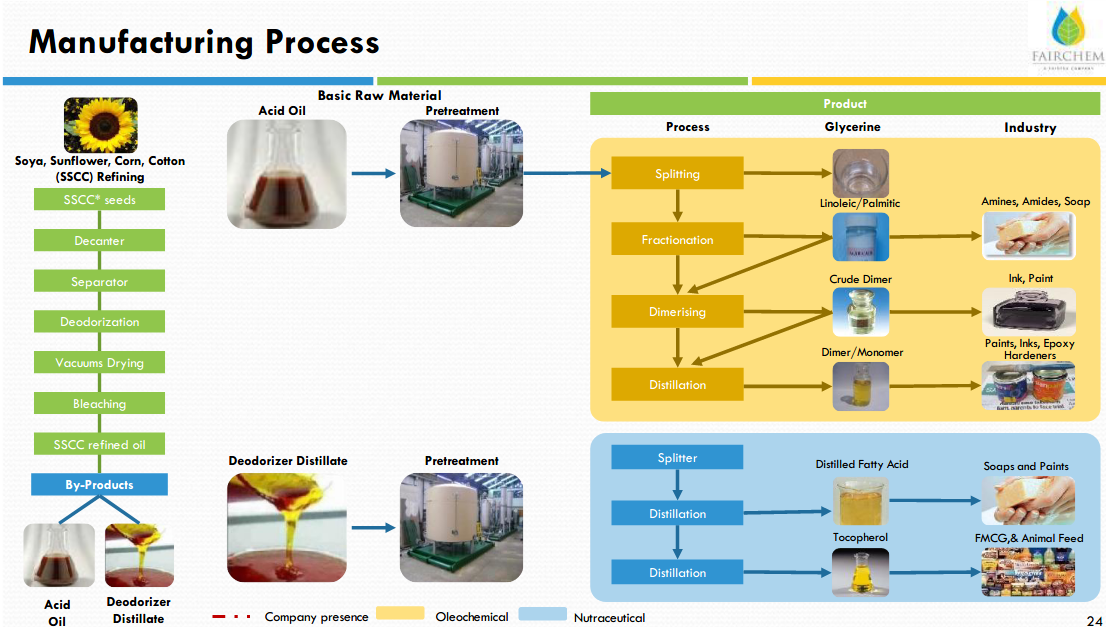

Fairchem has one-of-its-kind manufacturing using by-products of vegetable oils (namely Acid Oils and Fatty Acids), creating Waste to Wealth. Over the past several years, they have perfected the technology to convert inconsistent raw material quality into consistent quality output. Whereas other oleochemicals manufacturers use vegetable oils, Fairchem uses by-products of vegetable oil—this gives them a distinct price advantage.

Fairchem has been manufacturing for 25 years. Customers include Asian Paints, Huber (erstwhile Micro Inks), Arkema, BASF, ADM, and Cargill. They use imported equipment such as Short Part Distillation from UIC Germany, and Fractionation from Sulzer Switzerland.

Fairchem is one of the few manufacturers of Linoleic Acid and Dimer Acid in India, which are the major part of the overall revenues and having a large addressable market size in India.

(Source: Company presentation)

Market Recognition for the Listed Peers

Fine Organic is one of the largest manufacturer of oleochemicals in India. Its current market cap is more than 4x Fairchem Organics. Galaxy Surfactants has 60% market share in surfactants derived from fatty acids. Godrej Industries has 13% revenue from oleochemicals.

Fine Organic is into food additives and Galaxy is into household products. Their products cater to a different market compared to Fairchem.

Fine Organic’s PE ratio is as high as 70. It is one of the few small caps that performed well during 2018-20. Galaxy Surfactants has a PE ratio of 35.

Risks

-

New promoters:

Even though the company has done well for the last 3-4 years under the new promoters, yet the governance, strategy, cash deployment and investor-friendliness have to be monitored going forward.

-

Recent demerger:

Detailed information is not available, for example, regarding client concentration, current capacity utilization, current and future revenue mix, and R&D focus areas and expenses. The Moneylife article said 50% of their revenue comes from top 5 clients, which is a client concentration risk (I could not verify this independently).

-

Raw materials:

Fairchem calls itself an Oleochemicals and Nutraceuticals manufacturer. However, Nutraceuticals revenue is declining from around 33% of the total revenue in FY13 to 3% in FY20, likely due to the high price of raw materials. In Nutraceuticals, the company produces Tocopherol, which is used in natural Vitamin E. This product of the company is intermediate and therefore does not command high price. Company has been unsuccessfully trying to shift to better-margin products.

The company faced the issue of unavailability of raw materials in the past, for example due to drought in the countries from which these are imported. Raw material availability of soybean oil by-products in India is low. Company is trying to shift to other raw materials like palm oil by-products to reduce risk of unavailability.

-

Forex:

Forex risk is limited since a large part of the raw materials is imported and finished products are exported. Also, the product prices are correlated with raw material prices.

-

Technological:

If a competitor develops new and substantially cheaper manufacturing technologies using altogether new inputs for making various kinds of resins for making paints, printing ink, hardeners. The likelihood of this happening is low.

Financials

The company has low debt. PAT margins grew from 8% in FY18 to more than 10% in FY21. ROE consistently grew from 22.2% in FY18 to 25.2% in FY21.

(Source: Company presentation)

Capacity expansion from 45K MTPA to 120K MTPA and forward integration will cost around Rs 100 crores, most of which will be paid via internal accruals.

Good Upside Potential

In the last five years, Fairchem’s revenue has been growing at 14% CAGR and profit at 36% CAGR. Fine Organic revenue has been growing at 11% CAGR and profit at 13% CAGR. Galaxy Surfactants’ revenue has been growing at 9% CAGR and profit at 24% CAGR. Both the revenue and profit growths of Fairchem are higher than Fine Organic and Galaxy. EDITDA and PAT margins are similar to Fine Organic and higher than Galaxy.

For Fairchem, PAT of Rs 150 crores seems to be achievable after the completion of capacity expansion to 120K MTPA. At PE of 30, the market cap will be Rs 4500 crores. The current market cap is around Rs 2000 crores. Fine Organic is currently trading at PE of around 70, Galaxy at 35.

References

- June 2021 Investor Presentation.

- FY20 Annual Report of Privi Speciality Chemicals

- Mergers, demergers: July 2016 Merger Investor Presentation and FAQ. May 2019 Demerger Transaction Overview.

Disclosure: Invested 3% of my portfolio, currently with small profit %.

33 Likes

Capacity expansion being done efficiently as has also been highlighted in the above post.

Good performance in Q1 despite revenues being impacted by the pandemic.

10 Likes

FOL has a moderately diversified client base with top 10 customers contributing around 64% & 66% of its total income during FY20 & 9MFY21 respectively. From credit report.

2 Likes

I had one question - If the company is expanding so heavily and the RM is not abundant and there is a very limited amount of it, how will it Procure more raw material for the future because that is it’s major cost advantage over other Players.

2 Likes

As I understand, usually the availability of the raw material is not an issue at all. However, this has been an occasional issue in the past due to dry weather/drought in Argentina/Brazil.

Their main raw material is the wastage of soyabean oil refining. This raw material is imported as it is not abundantly available within India. Argentina and Brazil are the largest producers of soyabean oil.

Vegetable oils are also being used to produce biofuels, which should result in increased production and easier availability of raw materials.

Much better if the company has been successful in diversification to using palm oil refining wastage as this can be imported from South-East Asian countries. Such diversification reduces the risk of occasional non-availability of raw material. I am not sure about the current status of diversification.

2 Likes

I think you might be wrong here. Majority of it’s raw material is Procured from domestic Players. It’s in the care credit report, have a look.

Large part of its Raw Material comes from Kutch - 2017 Investor Presentation

7 Likes

I beleive they have a tie up with adani for raw material

1 Like

Updates:

-

The company has posted QoQ flat results for Q2 FY22. In the investor presentation, the management said the lower EBITDA margin is primarily due to higher power cost. Furthermore, June-Sept period has lean availability of the raw material. The import of vegetable oil was restricted due to higher freight costs. Considering these factors, the results appear to be excellent.

-

Capacity expansion to 120K MTPA as previously announced is ongoing and likely to be complete before the start of the next financial year.

-

On Nov 9-10, the promoter FIH Mauritius sold more than 13% of the total number of shares in the open market. Its holding now stands at around 53%. This is disappointing particularly given the bright prospects of the company. I will trim down my holding by around the same proportion.

6 Likes

Check out the below on FIH selling…

6 Likes

Any specific reason behind the stake sale?

The company, capacity has been successfully expanded from 72,000 MTPA to

90,000 MTPA and the company is also on track to further expand the

same to 1,20,000 MTPA by end of FY22. Ongoing Capacity expansion is to increase capacity by more than2.5x by end of FY22 with minimal CAPEX. The company doesn’t need any more capital, the promoter can cash his shares. One positive note, this increases the liquidity too of the company’s shares too.

6 Likes

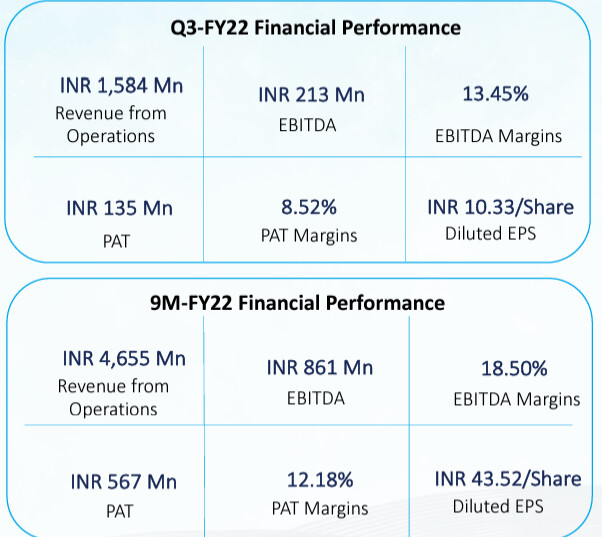

Q3 - FY2022 – Investor Presentation:

Some Operational Highlights:

-

The fall in revenue on a QoQ basis was mainly due to lower lifting of one of the prime products by the customers in anticipation of some correction in relevant commodity prices from the then existing level. The customers reduced fresh buying. The Omicron variant of Covid-19 also played some role in impacting sales.

-

Prices of raw materials remained quite volatile and the price of coal also ruled high during the quarter. The increase in cost of raw materials and fuel accounted for nearly 80 % of the decline in net profit on a QoQ basis.

-

The Company was generally able to pass on the rise in RM cost to its customers. The Company, however, is in the B2B segment and enjoys long term relationships with most of its customers. So when there was a sudden hike in raw material prices, the Company had to absorb some part of it for future sustainability.

2 Likes

If customer has lifted lower Product this quarter, it will have to lift more of it the next quarter because you can delay your Purchase upto a certain limit only.

Seems more of a qtrly disturbance but on an annual basis, it should be fine.

Can someone help me with the Revenue guidance in Q3 Fy22 presentation ?

"Company to increase its top line by 2.5 times of FY21 in 3years and intends to maintain EBITDA growth."

Please see if I am interpreting & calculating the numbers correctly

FY21 Rev: 396.6Cr

FY24/FY25 Rev : 396*(1+2.5) = 1388Cr

I can see Fy22 rev closer to 650 Cr, I want to understand the growth I will be paying for based on above statement. Questions are as follows:

- Rev guidance is for Fy24 or Fy25?

- Increase by 2.5 times (as above) or to 2.5 times ?

Fairchem Q3 FY22 Presentation

2 Likes

My interpretation is 1000cr topline by FY24. Such projections are conservative and the actual performance depends on the market conditions. The market conditions are volatile as of now due to the ongoing war and enduring Covid disruptions, resulting in increased raw material and fuel prices. The company has raw material price advantage compared to competitiors but is dependent on coal. Fine-grained analysis of projections is futile.

6 Likes