Company’s concall was held yesterday. KTAs:

→ Continue to see strong demand across industrial and auto sector.

→ Barring Maruti all major OEMs are clients. Maruti already has 2 vendors,couldn’t break through.

→ Growth depends on pace of infra addition. If the government sticks to it’s plans,growth will keep accelerating. Company is open for even more capex if demand is there.

→ Promoter loan is being charged at 9%. Company will pay this debt down soon,no need to refinance. Will be LT debt free within 8-12 months,some WC loans will stay on B/S.

→ No risk from composite cylinders.The products have a niche application and are 25-30%+ more expensive than steel cylinders.However,if market matures for this EKC doesn’t mind entering.

→ Q2 was “special” for margins. Company is doing everything it can to recover margins and has repriced old contracts,Q4 will be better than Q3.

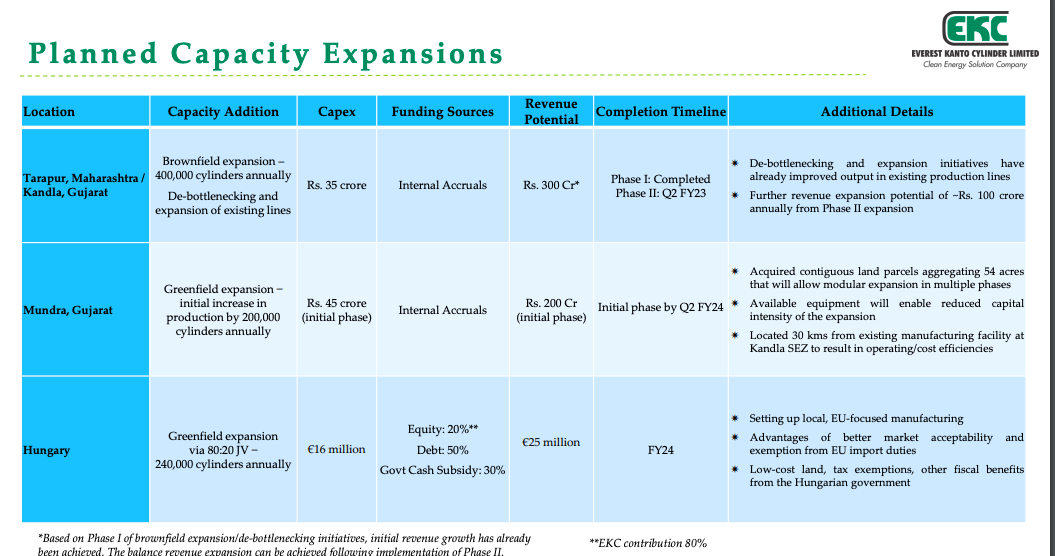

→ Mundra land has enough area for addition beyond the stated greenfield capex.The capex number given earlier didn’t include this land cost(why?)

→ Capacity addition of ~10% over next 1-2 qtrs so expect a 500 cr type run rate. 15% revenue growth in Fy23. Company is focusing on enhancing RoCE and EBITDA at all times. Already at 30% RoCE which will rise further. See no downside to realisations.

I see a lot of confusion post the call,mainly on margins and revenue growth.For anyone who’s been tracking EKC since a while would know that Mr. Khurana isn’t very good with numbers.When asked about medical cylinders contribution,he didn’t know the answer.Similarly,almost an year ago there were lot of questions raised on capacity constraints since the brownfield addn was 2 years away Mr. Khurana gave a similar 15% guidance saying valued added products will help eke out more.However,company suddenly went to 285 cr qtrly run rate from 240-ish without any capacity additions! So I won’t be surprised if a similar situation happens in Fy23 as well.On margins when asked if he sticks to his 22-24% consol guidance,Mr. Khurana said they expect to do better than that which brings us back to 25-26%.At the same time he says “Q2 was special” so 26% won’t repeat? (even Q1 was 26% EBITDA!)

Recent entrants might be alien to this concept but EKC is always a rocky ride.Stock went from 77 to 162 in a few weeks last year and then crashed 50% to 80-82,only to end the year near 250.Let’s see what Q4 has in store.In the short term stock might meander within the current range.

Since there is lot of controversy around future margins attaching the audio transcript.

listen from 21:20-50,mgt clearly says >22-24% EBITDA.

Disc.: Invested.Views are biased.

Edit: @RajeevJ pointed out that the 53 cr land cost wasn’t mentioned in the call and I have made the correction.Apologies for the confusion from my end.However,point remains that excluding land cost from the stated greenfield expense reflects badly on the company.