Being publicly listed means you’ll be scrutinized! The reason everyone is picking apart the Q3 call is because there were some inconsistencies.Now there are more people invested so more ears are hearing and hence the higher volume of posts here too.If the IR or management gets to know about these discussions then they should take it in their stride and plug the gaps:

→ Let the CFO speak more and let him discuss the numbers.The MD can stick to macro commentary and defer to the CFO when needed.

→ Be clear about the specifics.The specifics have been pointed out on the thread(Mundra land,growth rate,margins,etc.)

The investor community has only one interaction with the management in a quarter,if even there things get a bit muddled up then it clearly gives a bad impression.The intention is not to malign the management,but to ensure that company improves it’s communication quality.The biggest beneficiary will be the promoter group itself since they hold almost a 70% stake.

@sharemarketgen_ All the points raised by you are valid. The mgt. has to do a better job of presenting the facts. The last call left investors more confused after the call!

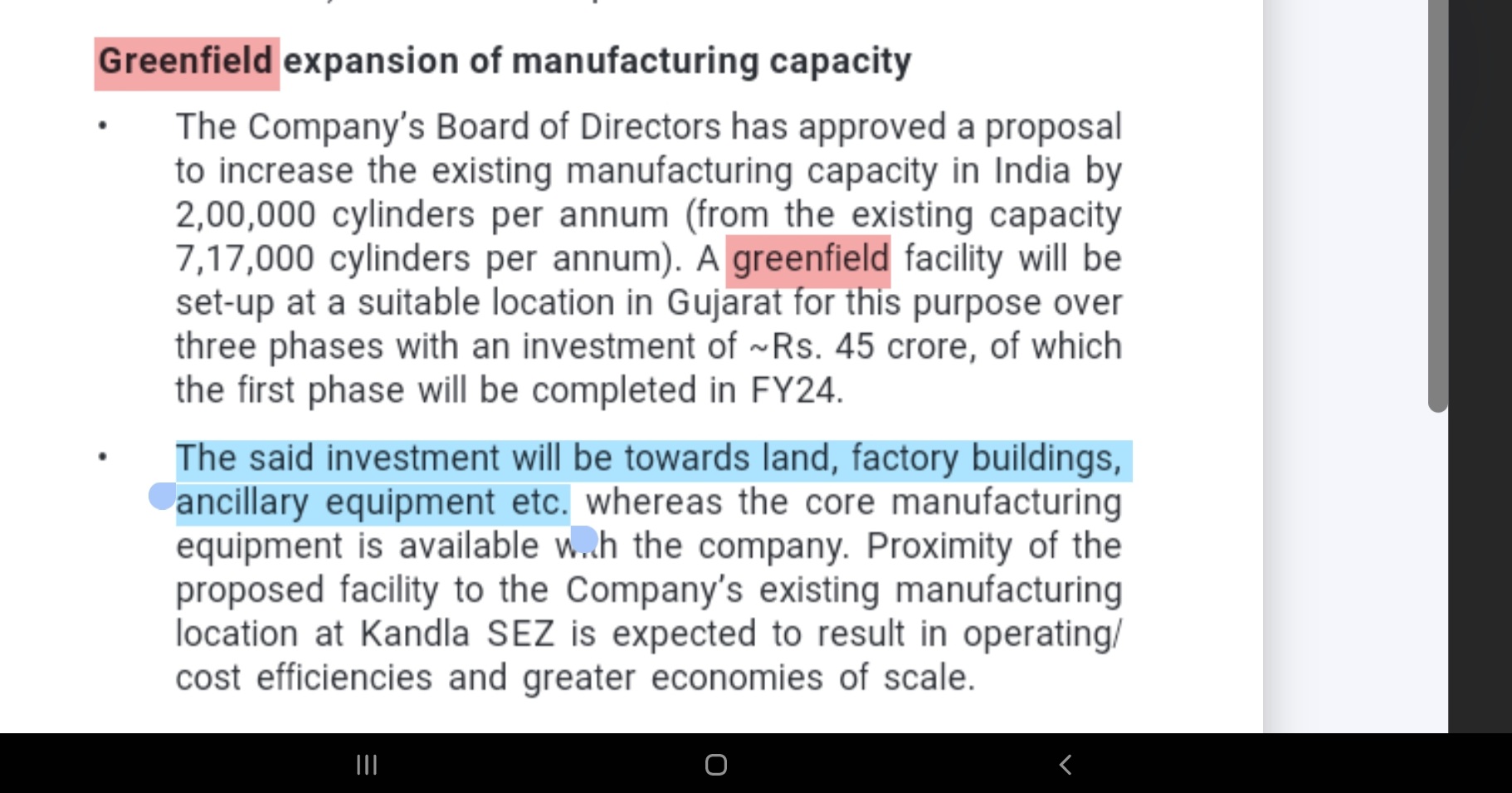

I have been doing my own scuttlebutt post the call. Apparently the land for the greenfield project is 53 acres, but did not cost 53 crs. The cost is much lower. Also logically, the land cost should have been included in the cost of the proposed greenfield expansion. Let’s hope the mgt. issues a clarification.

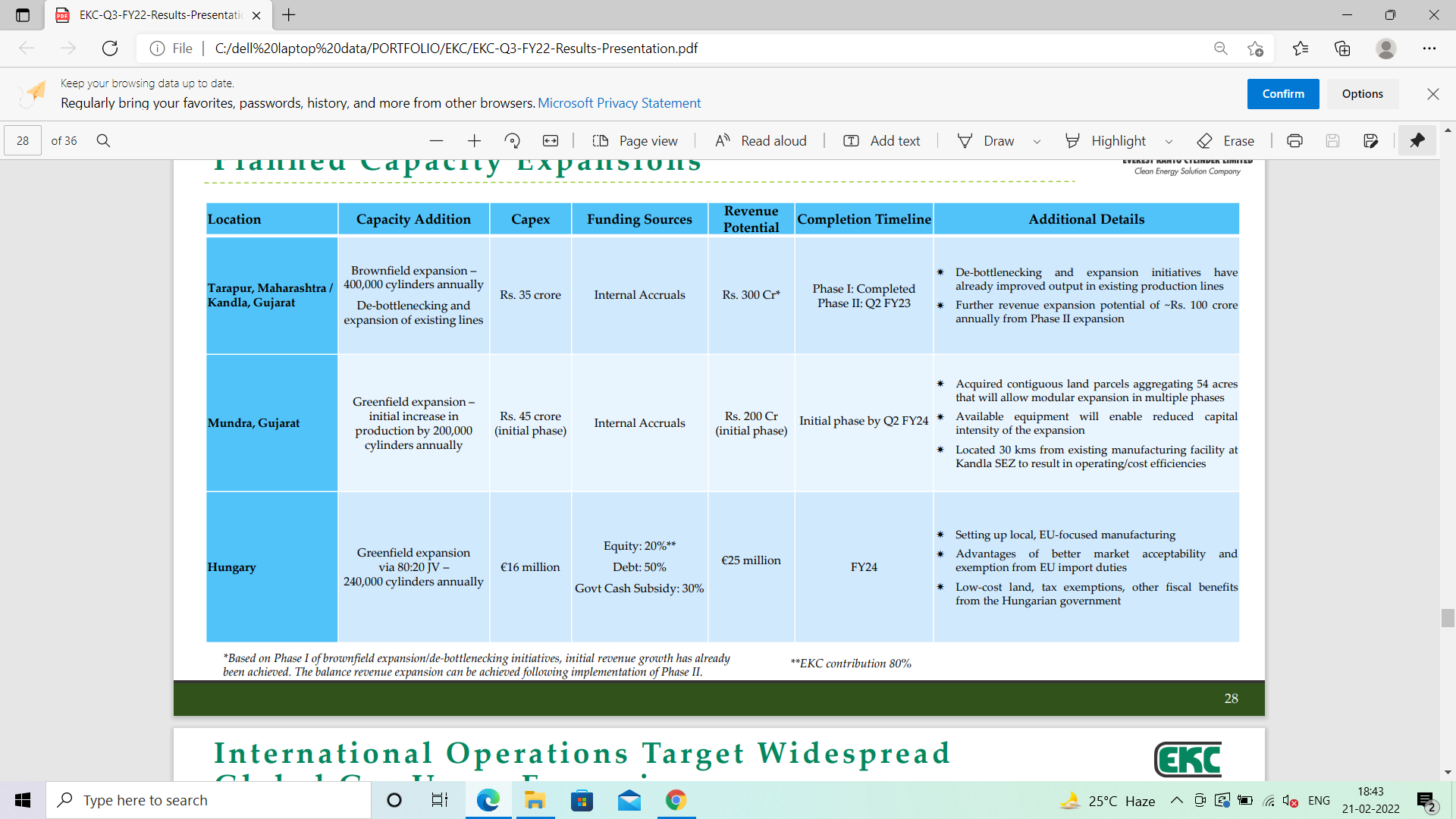

In the PPT no where its has been mentioned that 53 crores is the cost of land. rather total cost of expansion of 2nd phase at Mundra including plant machinery & other expenses is 45 crores which appears reasonable. screenshot enclosed n also the ppt.

Yes Vivek, nowhere does it say 53 /54 crores is the cost of the land, because that is not the land cost. The stand alone land cost has not been mentioned any where. I think the MD meant to say the land was 54 acres, but inadvertently said it cost 54 crores, if he said it at all!

Now this seems to be the logical explanation. It will help if someone can talk to the CFO or the IR firm to confirm the same.

In the entire forum, not much discussion is happening on its CGD business. That’s the biggest growth story in the next 8-10 years. It will be a more stable growth story.

How does top EV manufacturers sees CNG growth, Tata views on CNG share in portfolio

12% to 20% share in near future ( 3 years)

Diesel replacement theme

Expect to Cannibalize petrol too

Tata being a major leader in EV is equally bullish on CNG, says something about strong tailwinds in sector. One of larger customer for Kanto.

Pricing power - When suppliers capacity are running at full and new capacities take time and risky money / investment to come online( Kanto capacities are at full from few Qtrs including brownfield pahse1, Pahse 2 and Greenfield seems easily consumable if end market OEM see it grow fast), supported by good demand of CNG from end customers- OEM won’t mind paying well to secure supplies - Kanto mgmt also alluded to renegotiate older contracts in con call. Some supporting data below

Here is CNG vs other waiting time from Google baba as of Dec 21

Other factors which will likely accelerate the trend

CNG adoption is a function of CNG vs Diesel spread( Petrol as well) - anybody guess on Crude prices in near term- most analysts predictions in range of $100 to $125. All the more reasons for acceleration in demand - courtsey Russia Ukraine issues

What choices Govt have as Crude boiling being the biggest weighing factor on budget deficit- Push CNG( auto and Infra), Push ethanol, Push EV - also evident from WIP policy push to retro fit

While market is being harsh on Stock, approaching longer term trend line support, no doubts its a vary volatile journey with Kanto. Could be gut wrenching if high allocation - traders paradise and investors dilemma.

Here are the details on Greenfield expansion as called out by company ( incl land and equipment 45 cr) - subtle points being some equipment being already available & phased expansion & location = cost optimization/ higher returns - Page 39 AR 2021.

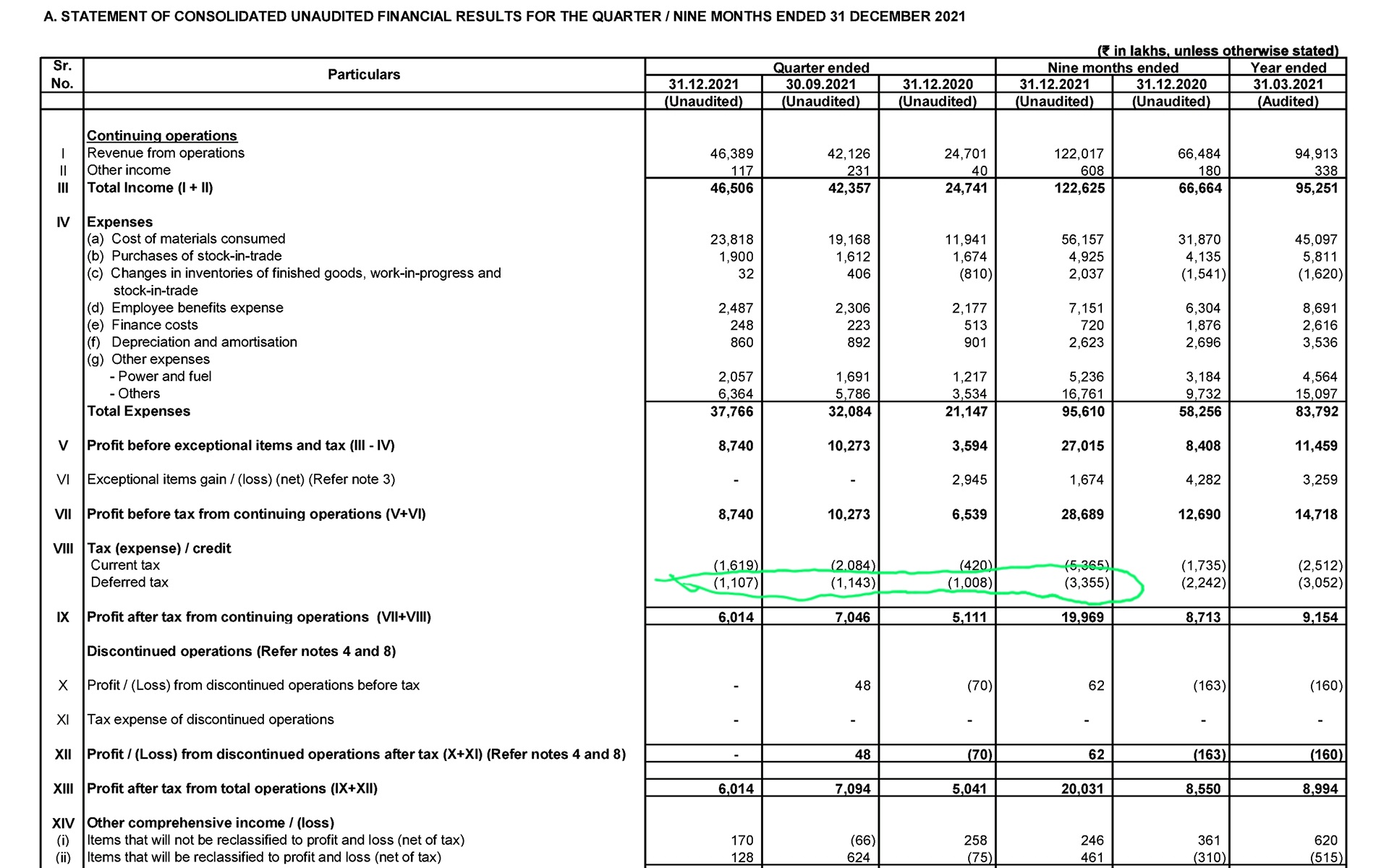

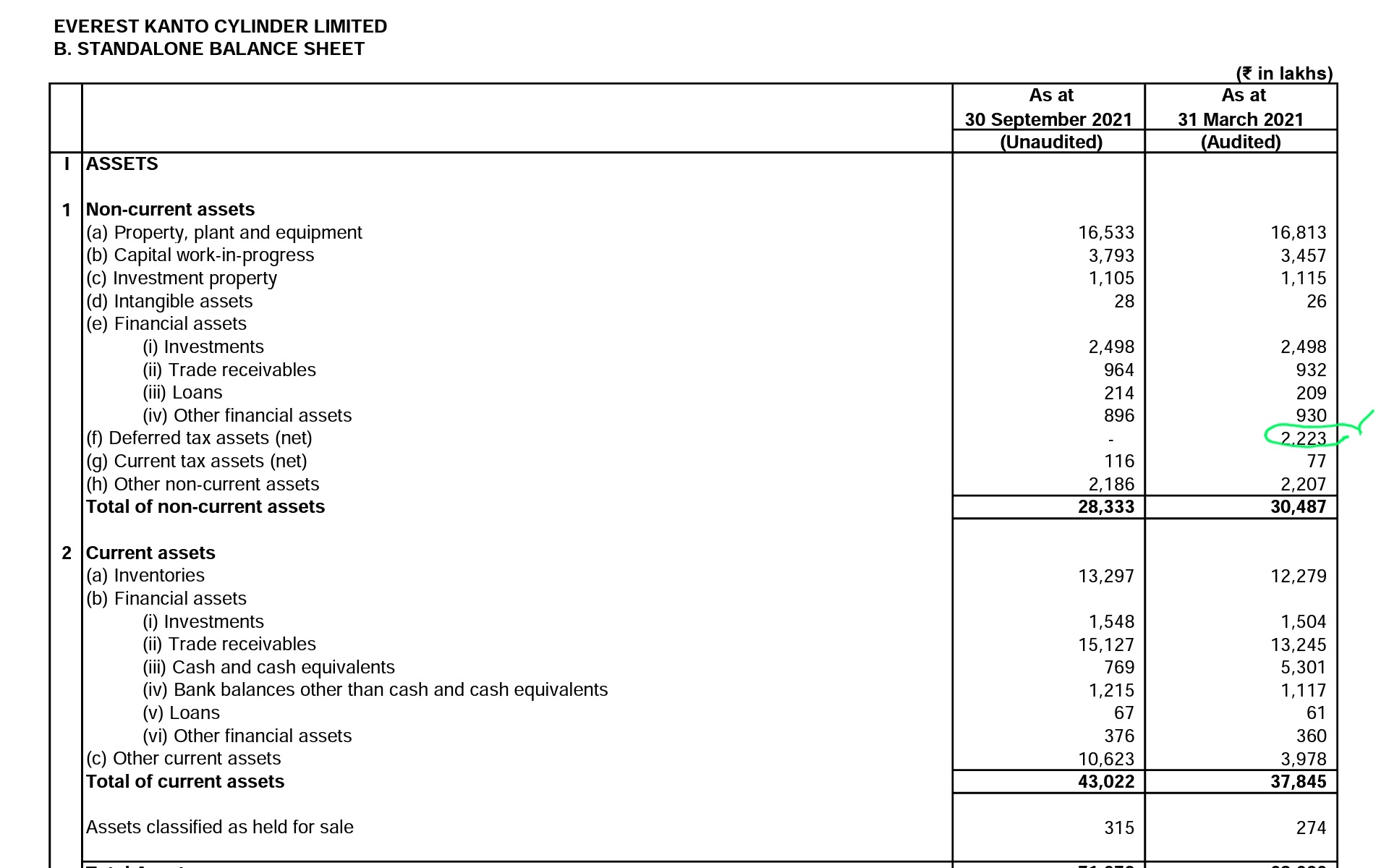

Hi @RajeevJ ji , would you have a view on when Tax rates normalize for EKC?, currently they are 31% for last few quarters - thus suppressing profits, assume this has to do with Deferred tax possibly. Each quarter there seems to be deferred tax around 10Cr + in FY22

Edit – amount outstanding on Deferred tax as on 31st March was 9.3 Cr, 8.9Cr in Sept 21 however in 9Mo FY 22 company has paid close to 32cr+ - not able to reconcile. Anyone any comments?

Once Deferred tax were to go away at some point and Tax rate normalizes, Bottomline would on its own jump by another 15-20% as well. Making valuations more attractive.

Concall transcript is out.Notably they have added ‘clarification’ at 3 places all saying the same thing: “The management’s response regarding EKC’s greenfield expansion plan was not communicated

accurately. To clarify, the company has acquired 54 acres of land, the cost of which

is included in the estimated capex of ~Rs. 45 crore.”

Hopefully company will avoid such confusions in the future.This clarification should soothe the nerves of many.

Summary of Q3 call:

Q4 revenues will be higher than Q3

Margin expansion indicated

Brownfield capex being implemented

Greenfield capex Rs 45 crore includes land

All capex funded by accruals

Several years of demand expansion potential

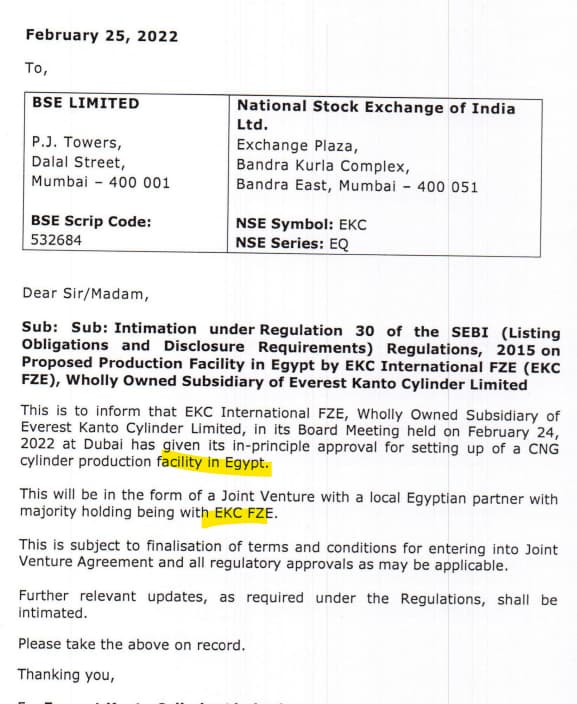

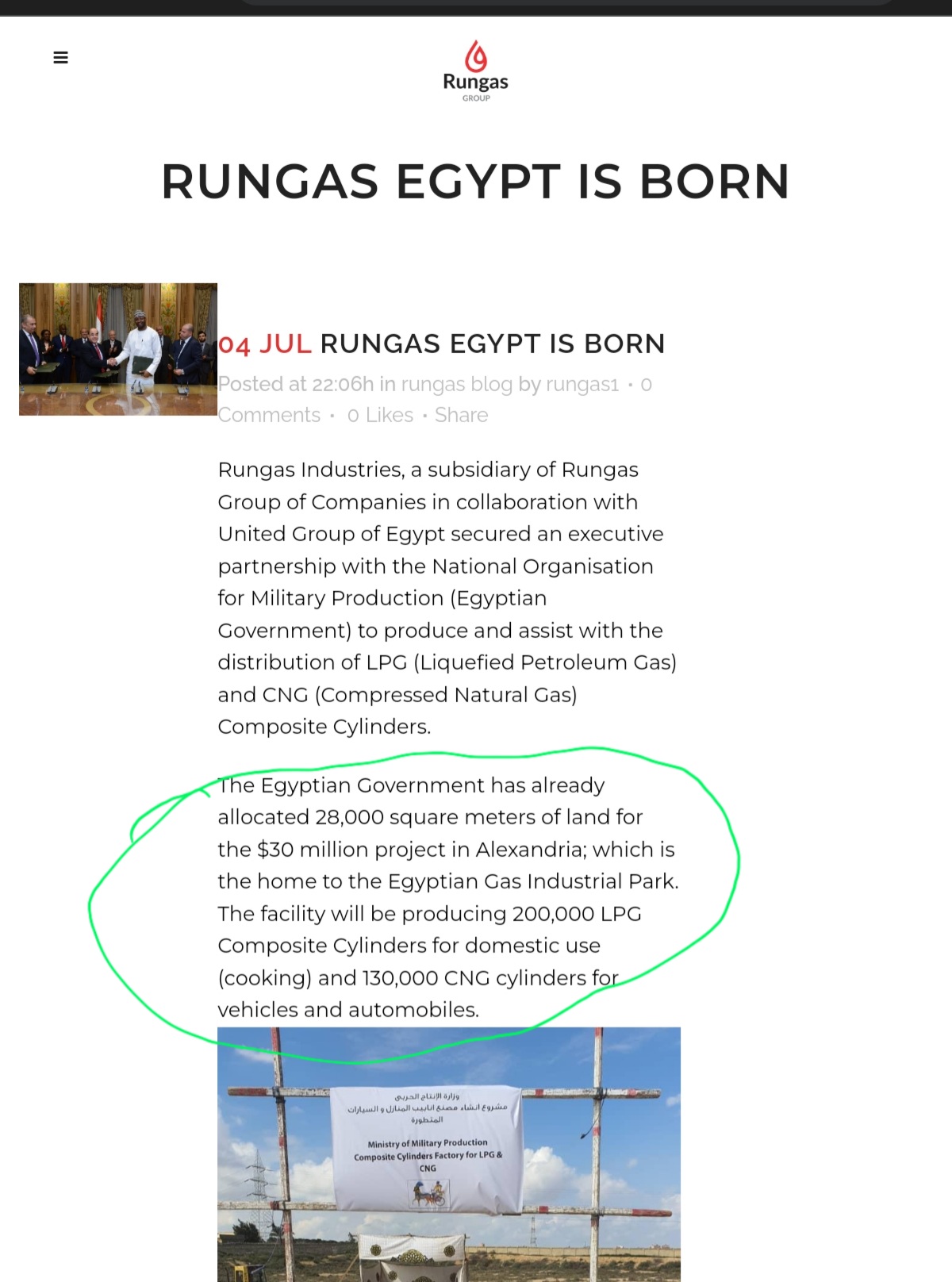

Rungas is setting up facility for 2L LPG AND 1.2L CNG at cost of $ 30M , in partnership with Amtrol-Alfa ( now part of Worthington group) - was planned to commission by end 21 - both local and Africa exports

EKC currently using its Dubai facility for primarily exports and makes a margins of 18-19% on 70 Cr type revenue - best they have ever seen, used to be lower in past- function of utilization

If production is done locally at Egypt- will save on shipping and logistics cost - however pie will be shared with partners as well , doubt that end margins will beat India standalone

Going by competetion investment nos they will need approx $10M type for 1.2L CNG - wants to keep majority share - so not a major outflow ( might get some subsidy etc as well)

Will take 1.5 to 2 yrs to commission - FY 24+

Puts a question mark on Dubai investments as clear overlap with end markets from Egypt.

Summary

We know that communication has been an issue with mgmg credentials/perception, Egypt announcement adds another layer of doubts on Capital allocation style and predictability - While actual event is med term but most of investors would have been happier if this growth Capex was in India- Given history of global forays/exits in past as well as current lower margins in US and Dubai. Explains no participation in today’s huge rally - mkt is disappointed/confused - so am I as it is already a low conviction case as of now!!

The Egypt info was reported around 3 pm but the stock was lower since morning and at LC for a short while,so I don’t think the info had any bearing on today’s weakness.If price was at 270-80,people would say this shows that company is hungry for more growth and chasing it in new geographies. I am not very concerned since the company’s balance sheet is in good shape.They also declared plans of entering Hungary last year so that’s another ‘outside India’ foray.Still bulk of the spend continues to be for India biz.Will need to see whether Hungary and Egypt are cash drains or no.

In any case,EKC stock has been badgered out of shape but I don’t know how to assess market reaction these days:

Deepak Fert- Q3 PAT 180 cr,Marketcap 6500 cr,no one-offs in Q3.Stock down from 660 to 510(today UC)

Tips Inds- Superb growth and margins in Audio biz in Q3,good outlook and large discount vs. industry leader.Music industry won’t be hit by Ukraine-Russia war in any manner! Stock down from 2600 to 1800(today UC)

Tinna Rubber- Q3 PAT 4 cr,190 cr Mcap,loan repriced at lower rate,strong outlook.Stock down from 363 to 220.

I could go on.In weak markets,a lot of selling is unreasonable.EKC anyway has a history of wild price moves.We can theorize with whatever data point that the fall happened coz of x & y reason.Markets overreact on both sides which is why we have bull markets & bear markets.One school of thought suggests that relative strength matters a lot.But it’s also true that the strongest performers of March 2020 underperformed big time over next 2 years(HUL,Nestle,Britannia,Ipca) I continue to be a shareholder here and for now the last 1 month has been quiet unpleasant.Let’s see what the future holds.Rajeev ji can add further insights.

One factor which is now playing in favour of Time Technoplast is high inventory cost for Type-1 cylinder. While going through their PPT , still LPG cylinder cost of Type- IV is higher as compare to Type-I where cost has been doubled in recent times. Time Technoplast may have advantage in Hydrogen (Where Size of cylinder matters) but in CNG I think Type-1 will lead. This is my assumption.

I share similar concerns regarding capital allocation abroad when capital allocation in India has far better ROCEs. But I guess we have to believe that the Management has done their math and worked out that the excess capacity being built in India is going to be enough for the next 2-3 years (3L + 2L cylinders). If that is the case and Egypt capex gives the company an opportunity to increase its sales without cannibalizing demand from Dubai and at better margins than Dubai, then this is the right decision.

CNG is a limited time opportunity. You have to grab as much demand as you can (Of course demand that can be served profitably and at reasonable ROCEs), else somebody else will eat your share of the pie.

International investments you have to look at ROE. EKC is investing only INR 20 crs in Hungary plant while total capex is 120crs (remaining is debt and subsidy). With savings in import duty and logistics costs, margins will improve substantially on exiting sales and will help increase volumes due to price reduction (due to import duty savings). I think it is a very good investment and with local partner getting subsidy and local approvals will be very easy. they have learnt from mistakes made in China. Even if sales from Dubai will be replaced by sales from Hungary overall sales and profits will increase.

For Egypt plant the details are yet to be known but should be on similar lines or else there is no reason to make investments in a new plant there as even now they are exporting to Egypt.

Lets look at the ROE and ROCE numbers for investments in India and abroad for EKC

Hungary plant

JV capex cost - 16 mn Euro (135 Cr)

Financing - 16% equity EKC, 4% equity Rev, 50% debt, 30% Govt subsidies (I am assuming all the debt is on EKC’s books)

EKC equity investment = 22 Cr (16%) i. . Annual Revenue potential - 25mn Euros i.e. 215 Cr ii. EBIT - FY22 9M EBIT margin for Hungary/USA is 11.7% i.e. 25Cr : I am assuming EBIT margin for Hungary would be higher than USA as USA has plant depreciation. So, lets assume existing EBIT for Hungary business would be 13.5% (29 Cr). This would also be existing EBITDA since no depreciation is there at present. Assuming new plant is depreciated via SLM for 25 years, per year depreciation charge will be INR 5.5 Cr (135Cr/25). Therefore new EBIT margin for Hungary plant will be ~11% i.e. 23.5 Cr iii. Interest costs - Annual interest costs on 8mn Euro loan (68 Cr) @ 5% is 3.5 Cr iv. PAT - 15 Cr. EKC share of PAT @80% equity = 12 Cr (net margin 5.5%) v. EKC ROE - 55% (12/22) EKC ROCE - 26% (23.5/89)

2. India brownfield capex:

Capex cost - 35 Cr

Funding - 100% equity i. Revenues - 300 Cr ii. Existing 9M EBIT - 27.5%. This EBIT has significant depreciation loaded. Since brownfield depreciation is much lower, EBIT% is likely to be higher, but lets for the moment proceed with same EBIT margins for an EBIT of 82 Cr iii. Interest costs - 0 iv. PAT - 61.5 Cr (20.5%) v. ROE - 197% (61.5/35)

3. India Greenfield Capex

Capex cost - 45 Cr

Funding - 100% equity i. Revenues - 200 Cr ii. Existing 9M EBIT - 27.5% i.e. 55Cr iii. Interest costs - 0 iv. PAT - 41 Cr (20.5%) v. ROE - 91% (41/45)

The projected ROE, ROCE numbers for the Hungary project are very good when seen separately (>25% ROCE, > 50% ROE). However, India greenfield capex has far better ROEs compared to foreign greenfield capex (91% vs 55%). So if the company was debt laden or capital strapped and has to choose between 2 competing projects - one in India and one in Hungary - choosing India project would be a no-brainer. But the reason Management is still going ahead with foreign capex has to be because

India capex right now seems sufficient to them and further capex may create over-capacity and margin pressures causing India ROEs to come down

CNG is going to be a limited sized pie for a limited period of time world over. Its heyday is likely to be from now till 2035, give or take a few years. If you don’t setup capacity now, that demand is gone forever. If Project meets your ROE/ROCE hurdle rates and you are confident of your execution and Govt regulatory environment, go ahead! These are additional, accretive profits. You are not sacrificing anything by going for these profits.

Considering the company has very low leverage (0.2x D/E), it can comfortably afford to take up projects in parallel.

Forex risk of Euro debt must be fully hedged due to Euro revenues from Dubai and Hungary businesses.

Now, whether or not, Management will learn from its past poor track record with foreign subsidiaries execution remains to be seen. One hopes, they will! Plan seems ok, execution is awaited.

I am not very concerned since the company’s balance sheet is in good shape.They also declared plans of entering Hungary last year so that’s another ‘outside India’ foray.Still bulk of the spend continues to be for India biz.Will need to see whether Hungary and Egypt are cash drains or no.

I am not very concerned since the company’s balance sheet is in good shape.They also declared plans of entering Hungary last year so that’s another ‘outside India’ foray.Still bulk of the spend continues to be for India biz.Will need to see whether Hungary and Egypt are cash drains or no.