Thanks for all the points. So the only exemption is the Dividend if not availed thru a concessional tax regime by the trust? Will have to redo all the post tax scenarios

I see two broad scenarios:

Valuations of REITs/INVITs take a beating due to this change

OR

REITs/INVITs decide to change their distribution mix to be more dividend heavy which would be tax free (not sure this can happen in the short term as majority of asset growth comes from borrowing)

Am i getting this right?

Still think this would appeal to retirees or people in early retirement stage as the tax rebate upto 7 lacs in new regime has been implemented. Taxation would be from 1st April 2023 i guess (This budget was for the coming year)

I find many investors are getting concerned with taxability on return of capital in InvIT/REIT structure. I also have large exposure in Embassy REIT and critically evaluting my position. Having said that, the main factors which would be determined my decision would be issue about Embassy Group Corporate governance and Blackstone group constant reduction in holding. Find enclosed my key issues in current situaitons:

Positives:

No fundemental change in the business prospects. In fact, during Q3 concall managment did give some indication (or my listening between the ears) that during FY24 , they may registered double digit growth at NOI level. While growth in NOI during FY23 did not translate in distribution to change in funding of debt (zero coupon to interest bearing) and higher share of Hotel busines (which has lower margin then Commerical rental business), I still consider this factor as positive.

Clarity on SEZ building denotification. In Bengaluru city (where most of assets of the company are located), in case building has no tenant operating under SEZ, then building can be ednotified within 2-3 months from SEZ to normal office area

Negatives:

Constant selling from Blackstone and issue of corporate governance from Embassy group

Growth in NOI not translating in growth in distribution for one reason or other. Since listing, quarterly distributions from Embassy has not grown even to past level. Partially, one can attribute same to COVID related issues, but the new office development, which might benefit in long term is taking toll on distribution in medium term. For investor like me, who consider this as substitute to debt, it is not serving the purpose. Hence, for me, next quarter call when management would issue guideance about FY24 distribution, growth in distribtuon would be key consideration for remain invested in Embassy REIT

Budget announcement about Taxability of capital redemption: While this may be pain point in near future, post announcement, I have mentally prepared myself even for taxability of Dividend in future. Further, as per budget documents I read, same was expected to implemented from 1 April 2024 (This is my reading and I am layman. My understanding may be completely wrong). Thirdly, other peer like Mindspace REIT are able to distribution 90% distribution in form of dividend, so within 6-9 months, I would consider even Embassy REIT would attempt to structure cashflow in way they are the most tax efifcient. This is my wishlist and may be completely wrong. In medium term (2-3 years), I would even consider dividend as taxable while taking my final view about holding.

In view of above, my current view is to wait and watch Embassy REIT closely. At current valuation, Rs 308 as I write, I do not find any sense to reduce my postion. I shall wait till Q4FY23 con call during April-May 2023 to decide way forward of investment.

Disclosure: Among my Top 3 investment idea in Debt portfolio (4% of my financial wealth). No trading in last 3 months. Not a SEBI registered advisor. Not suggesting any investment action in Embassy REIT. I may exit/increase my allocation without informing forum. Reader shall consult SEBI registered financial advisor and also do his/her own due diligence before investing.

Thank you for the candid opinion DD. I echo your thoughts and am in the same boat (although My exposure to REITs/INVITs is pretty significant…Brookfield and Embassy followd by IRB and Indigrid)

I am also of the opinion that these are long term assets which require a longer gestation period and the tax announcement is a short term deviation. Ultimately what matters is the underlying growth of the asset holdings in yield and distribution. That is the major differentiation as compared to pure debt (e.g. Bonds)

On corporate governance, REITs are structured investment class where there is a lot of regulatory oversight (hence the REIT laws took time to be drafted). Globally they have proven to be powerful compounding asset classes.

On Embassy will be observing as of now. No change in strategy as of now. I personally dont see Blackstone selling as a major negative. REITs are mainly for income investors (individual) + large institutional pension funds who want annuity returns. Blackstone being a Private Equity player had to cash out at some point to redirect funds to other emerging assets. What would be more important would be to see which large investors take Blackstones position. Bain capital looks interesting

PS: These are just my thoughts at this point. I could be wrong. Please use your discretion. Thank you

I too have huge exposure to REITS/INVITS. Even though there has been taxation changes I think post tax it is still much better than the residential yield one gets on physical property. For eg in Mumbai where I live, the yield on residential flats is pre-tax 2-3%. I see so many people trying to park excess liquidity in these apartments just because of the joy of owning a physical/hard asset.

Even though there may be a minor dent in post tax returns of REITS/INVITS, they still trump over physical hard assets is what I think. Also, we need to consider the upside in the actual appreciation of the underlying assets. These real estate trust’s own some of the best assets in the best of locations pan India.

Does anyone know when the BIRET conf call is ? They are the only REIT that are still to have the concall and my guess is that a lot of questions around taxation would come up.Their results come out on Feb 7th but no communication around the con-call yet.

Embassy Office Parks REIT (NSE: EMBASSY / BSE: 542602) (‘Embassy REIT’)

While the recent announcements in the Budget have created some uncertainties in the market regarding the taxation of one

of the distribution components, the announcement impacts around 40% of our current distributions. Plus, REITs are a total return product combining steady distributions with upside on account of capital appreciation driven by growth levers. We, along with other Industry participants, are currently evaluating next steps, including suitable representations given the to-date attractiveness and success of the product, especially to retail investors.

As demonstrated by our recent 3QFY2023 performance, our results are strong, our business model is growth-oriented, and we paid out our 15th consecutive quarter of 100% distributions, now totalling Rs.7,300 crores. At 27% leverage and a 7.2% cost of capital with AAA rating, we are proud to have the best credit in the real estate industry. Our best-in-class unitholder register comprises sovereign wealth funds, global mutual funds, domestic mutual funds, life insurers, family offices, High net worth individuals and retail investors. We will continue to serve the interests of all our stakeholders by doing what we’ve done before we listed and since we’ve listed: providing the best office solutions to the world’s best companies.

I took a stab at what price, Embassy REIT will become attractive

It all depends on what tax slab is one at and at what surcharge % they are at. Whatever bracket and surcharge, don’t forget to add the 4% Health & Education surcharge.

Let us assume that you are in the top tax bracket of 30%…(33% or 1/3 total for easy calculation)…last quarter was 2.39 rupees distribution was impacted by budget (45% of distribution), …so, the rough impact on the distribution is a 1/3 of the 45% or 15% must be the correction.

Assuming the pre-budget stable level of 330, this 15% correction works to 280.

If the market wants a post budget, post tax return of 6% (again tax brackets as above), the price works to 286.

If you want to breathe easy and buy/forget price, it is more like 273-275.

That is my back of the envelope calculation.

For me, I may not go near this, unless it is comes to 260s

PS - God save the REIT investor, if they decide to tax the dividend too !! who knows…anything is feasible. Nothing ever will surprise me, after this budget.

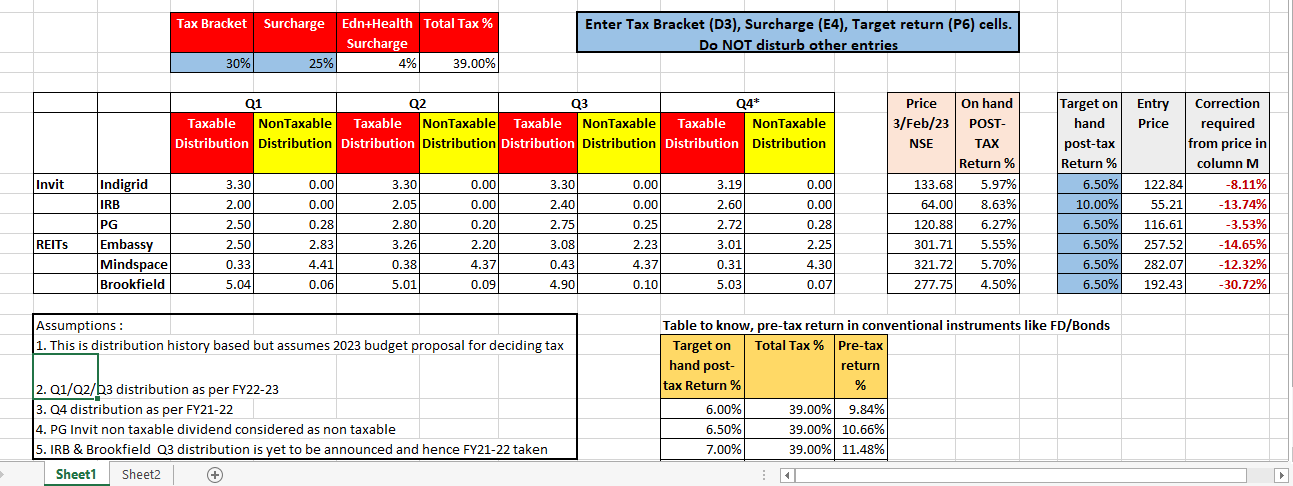

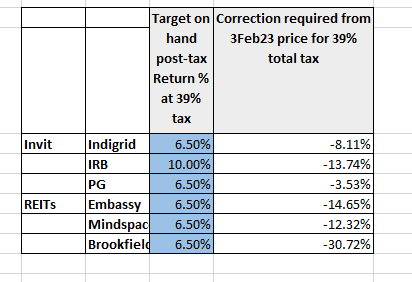

I have attempted to come out with a calculator that depicts the ravages of the 2023 budget taxationTarget entry price for a target return and current return %

All the assumptions are in the spreadsheet and it is self explanatory), A very important point is that this is historical distribution based and assumes that if this distribution is continued as such, what will happen with the new budget proposal. I have also included a table for comparison with conventional instruments like FD

The only input cells are tax bracket, surcharge and target return(all in blue accent)

Pl give feedback and I am open to correct the excel

What shocked me was the amount of correction needed in Brookfield, post the budget change…how did it escape? is it held by entities who don’t have tax?

DDT is not applicable if the reit spv claims tax deduction as per old income tax regime…and if I recall right these REITs (When I say, these, I mean only Embassy and Mindspace),do use the old regime.

Also, this budget is very specific about killing the loop hole of tax avoidance in both ends (as in the case of Return of capital or amoritsation)…and not about double taxation

The term loop hole is based on how they described it. They want any payment to be taxed at least at one place (otherwise, it will itch the Babus in Fin min !! somewhere, they have to milk it). since, it was a pass through, it itched them and they said ‘you unit holder, get slaughtered’… that is that !! I have pasted the exact Fin bill above in post 149 above…and you can infer this !

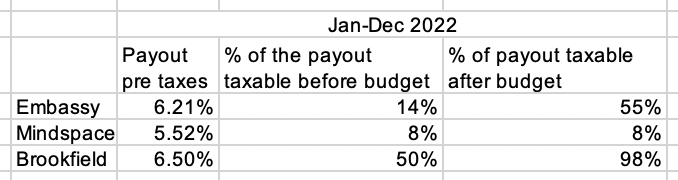

I compiled the last 4 quarters payouts for REITs and studied how the recent budget will impact it. Here it is… Looks like Brookfield will be the most impacted while Mindspace shouldn’t worry much…