Embassy REIT Background:

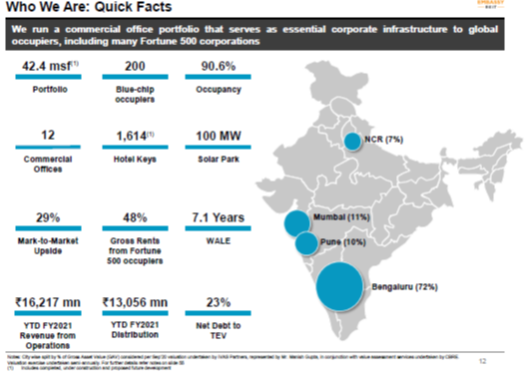

Embassy REIT is India’s first publicly listed Real Estate Investment Trust. Embassy REIT owns and operates a 42.4 million square feet (“msf”) portfolio of eight infrastructure-like office parks and four city‑centre office buildings in India’s best-performing office markets of Bengaluru, Mumbai, Pune, and the National Capital Region (“NCR”). Embassy REIT’s portfolio comprises 32.3 msf completed operating area and is home to over 200 of the world’s leading companies. The portfolio also comprises strategic amenities, including two operational business hotels, four under‑construction hotels, and a 100MW solar park supplying renewable energy to tenants

REIT India’s Past experience

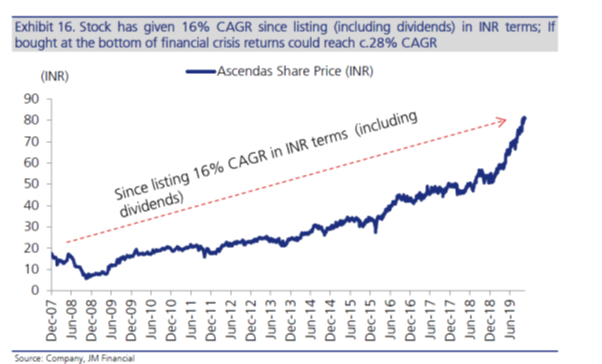

While Embassy REIT being the first one REIT listed, I read an old JM Financial Report, which provided information about Ascendas India Trust, a business wsith Trust characteristic which is broadly comparable to REIT structure in India and has been listed since FY08 on Singapore Stock exchange. Over FY08-19 period, Ascendas reported property income growth of 12% CAGR, with RE portfolio increasing from 3.6 mn sq ft in FY08 to 12.6 mn sq ft as on June 2019. The instrument return since listing are as under.

The above example provide some template about how one can expect REIT performance in India over long term.

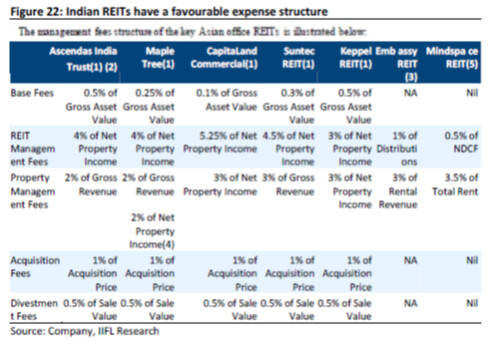

Management fees/Expense charged for Management

As per information sourced from IIFL report, the Indian REIT structure charges appear reasonable when compared with other peers (which are listed in Overseas market) Find enclosed comparable table on same.

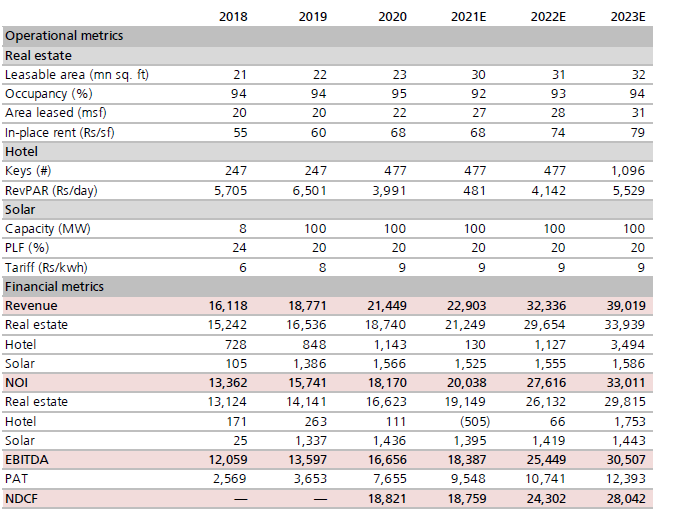

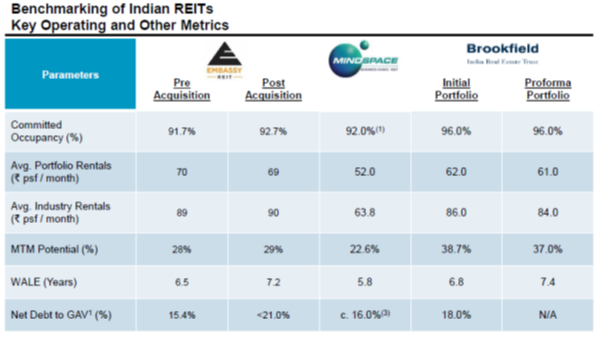

The management insight details about various information parameter over last 8 quarters in Datasheet, Valuation report, Annual report, Financial Presentation and Conference call transcript. The link for same is enclosed herewith for latest quarter results.

Some key highlights are as under:

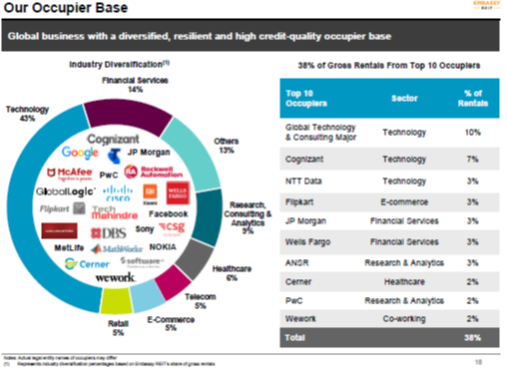

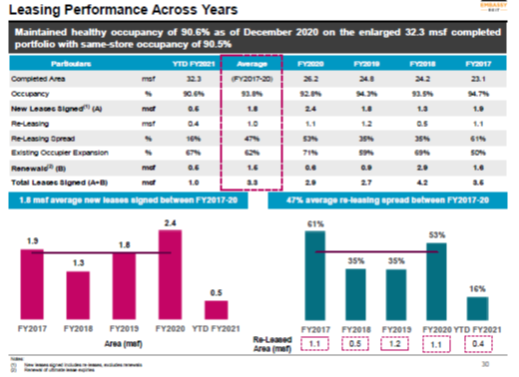

Comparison of Embassy REIT with its peer

Positives:

Performance history in Covid period

Embassy has longest tenure of listing history among all REIT. It was only REIT which continued it’s distribution during Covid period during March 2020-June 2020 period when India underwent countrywide lockdown

Acquisition of new assets

Embassy has successfully completed a major acquisition during Q3FY21 of Embassy Techviallage by raising additional units by way of QIP

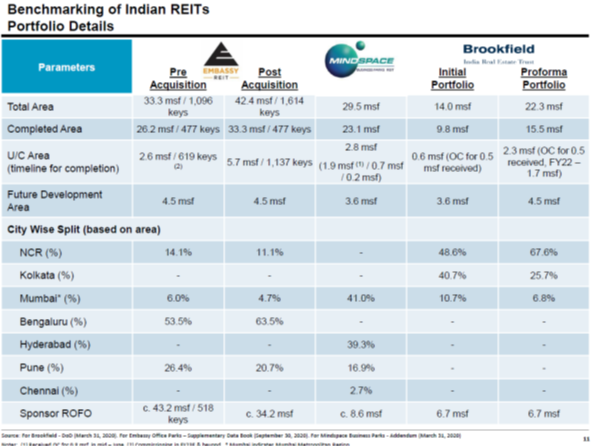

Better asset portfolio

Despite having 72% assets in Bangaluru region, Rent per square feet is highest for Embassy at Rs 70/sq ft vis Mindspace and Brookfield.

| Citywise Area | Embassy | Mindspace | Brookfield |

|---|---|---|---|

| Bengaluru | 72% | ||

| Mumbai | 11% | 41% | 22% |

| Pune | 10% | 17% | |

| Noida/Delhi NCR | 7% | 56% | |

| Hyderabad | 39% | ||

| Chennai | 3% | ||

| Kolkata | 22% |

| Rent per sq ft | 70.00 | 55.20 | 62.00 |

|---|---|---|---|

| Bengaluru | 72.00 | 0.00 | 0.00 |

| Mumbai | 176.00 | 56.20 | 90.00 |

| Pune | 46.00 | 63.90 | 0.00 |

| Noida/Delhi NCR | 43.00 | 0.00 | 67.19 |

| Hyderabad | 0.00 | 51.30 | 0.00 |

| Chennai | 0.00 | 64.00 | 0.00 |

| Kolkata | 0.00 | 0.00 | 42.00 |

My expectation and working for information (Please Read disclaimer and note specifically for projection of return)

While an investor in REIT would take business and market risk, given that dividend distribution being exempted from taxation, REIT offer good risk adjusted post tax return for my risk profile.

Further, I have compiled an indicative distribution expectation for three REIT, from various sources. Please note that this are expectation of analyst/management and IT MAY UNDERGO MAJOR CHANGE given the volatile environment. The objective to provide this information is only to compile data from various sources and NOT to ADVISE ANY INVESTMENT.

| Projected Distribution per unit | Embassy | Mindspace | Brookfield |

|---|---|---|---|

| FY22 | 25.64 | 20.62 | 21.84 |

| FY23 | 29.58 | 22.02 | 23.16 |

| Source for DPU | Kotak Report | Axis Bank report | Brookfield presentation |

| Unit price of 9Apr2021 | 313.9 | 299.93 | 239.5 |

| DPU yield/Current price FY22 | 8.2% | 6.9% | 9.1% |

| DPU yield/Current price FY23 | 9.4% | 7.3% | 9.7% |

PLEASE NOTE that every investor shall do his/her own assessment for risk profile and take personal investment decision. Secondly, my understanding of Tax exemption may not be correct and hence reader shall consult his/her tax advisor before making any investment decision.

Negative:

Return are indicative and NOT ASSURED like debentures/fixed deposits

The investor is REIT is subject to business and market volatility risk. The distribution from REIT is not an right of REIT investor. In case, business performance is adversely affect, like dividend, management may not distribute any amount to investor. Hence, REIT is NOT SUBSTITUTE TO DEBT PRODUCT.

COVID related uncertainty

Embassy REIT distribution has declined during 9MFY21 vis same period in FY20 due decline of income from Hotel Assets. The expected recovery from Hotel may take longer period due to COVID related uncertainty.

Secondly, COVID has changed the work space requirement for society and business. The flexi workspace and work from home are emerging as strong trends which may change long term demand for A Grade office space in which Embassy REIT operate. This may not only adversely affect Growth prospect, may also adversely affect demand and rent realization for Embassy REIT in future. Reader shall do his/her own assessment on this factor.

Disclaimers:

I have invested in Embassy REIT during last 3 months. My view may be biased due to my investment. I am not SEBI registered investment advisor. I am not suggesting any investment action to reader by this note. Reader shall do his/her own due diligence and/or consult his/her investment advisor before making investment decision. The projected distribution over next two years are my compilation from various sources and by no means shall be considered as assured distribution.