Thanks AJ. I think the broader issue is not the tax piece (important but a short term deviation). It is how does the NOI growth translate into Distribution growth. So far the office REITs have been hit by Covid lockdowns and then a sudden increase in interest rate regime which is acting as an hindrance in distribution per unit growth.

Medium term to long term NOI growth should happen however still waiting to see it translated to DPU increase (should atleast match inflation rate consistently)

2 Likes

Medium term to long term NOI growth should happen however still waiting to see it translated to DPU increase (should atleast match inflation rate consistently)

I feel the probability of that happening is low -

- more acquisition = more equity dilution. Valuation issue here.

- Borrowing costs

It would be great to hear another view point or if I’ve made an error in thinking.

2 Likes

SEBI has circulated a new consultation paper on REITs, that seeks to increase the mandatory holding period of promotors/sponsors.

Given the continuous selling and dilution of stake from sponsors of some of the listed reits, and multiple whammies of covid + higher rates + wipe out post budget, this is a welcome move

3 Likes

2 Likes

2 Likes

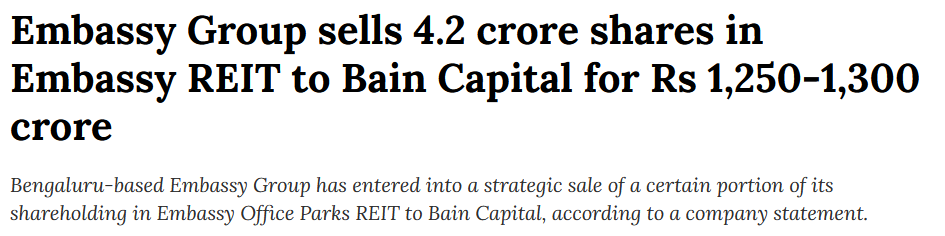

Embassy group had already defaulted… Embassy has Corportae Governance issues…now Black stone has also defaulted, Tax regime is not friendly, Interest rates are rising. Inflation not abating , Main promoter Blackstone is reducing stake, Company is refinancing its debt from NBFC… Company has now lost its negotiation power and debt refinancing onwards will be significantly high…

All hell broke into Embassy REIT…

Discl : Not invested just following for academic purpose…

11 Likes

While the concerns about promoters of Embassy REIT is valid, the structure of trust, too an extent support the investor in REIT. Also, the problem that Embassy group is facing liquidity issues which is resulting in selling REIT units resulting in higher supplier may act against price of REIT, in longer term, it would kind of insulate REIT from the Embassy group issue (with declining stake and hence having limited say in working).

Blackstone default in Nordic company debt has resulted in 1.4% decline in equity share price of the company on stock exchange. While default on debt by Blackstone group entity is really concern, the equity market price movement, at least at primary stage, does not indicate any adverse development on credit profile of the company.

The company refinancing debt from NBFC is not so much concern in my view given that it reduce cost and also provide another class of lender to REIT sector as mentioned in Press release. . Further, loan from reputed NBFC Bajaj Finance which has among the best underwriting standards in India in my view, is strong support to credit profile in my view.

Having said that, the point raised by @VALUE2017 are really worrisome and need close monitoring. The constant selling from both promoter groups in REIT does not provide comfort to unit price in short to medium term coupled with adverse budget announcement of taxability of Capital return being taxable in hands of REIT/InvIT investors from 1 April 2023. As Embassy REIT is among my top holdings, I am cautiously evaluting my investment. For me, Q4FY2023 con call would be critical event when the REIT would share guideance for FY24 distribution. I eagarly look forward to increase in distribution guideance from Embassy REIT. I shall take call about change in investment holding post con call.

Thanks once again to value2017 for brinning all chellanging issues faced by REIT.

Disclosure: I am investor in Embassy REIT/IndiaGrid InvIT/ IRB InvIT. My view may be positively biased due to my investment. I may change my investment view without informing forum. I am not recommeding any investment in Embassy REIT. Not a SEBI Registered investment advisor.

13 Likes

An intreresting artcile from Economist providing insight about R&D outsourcing by MNC companies.

As per chart 4, in enclosed article, R&D spent by US Based MNCs have gone near $ 2 billion in 2000 to around $ 12 Billion in 2022. Of these spent, regionwise spent shown in graph, in my reading, indicate, that Share of India in this R&D spending has gone up from near zero in 2000 to USD 5 billion in 2022. which is more than 40% of total R&D spending by US based MNCs. This indicate strong secular trends for Global Captives which are major market for Embassy REIT.

The reader need to sign up with Economist to read the article. Since it is paid service, it would not be correct to publish the information without consent.

Discl: Same as previous note.

5 Likes

If the above is true, the brief lived hope will be reversed by Monday !!

This one came at 1.59 PM

My Q is , why did the market not react in those 90 minutes ??

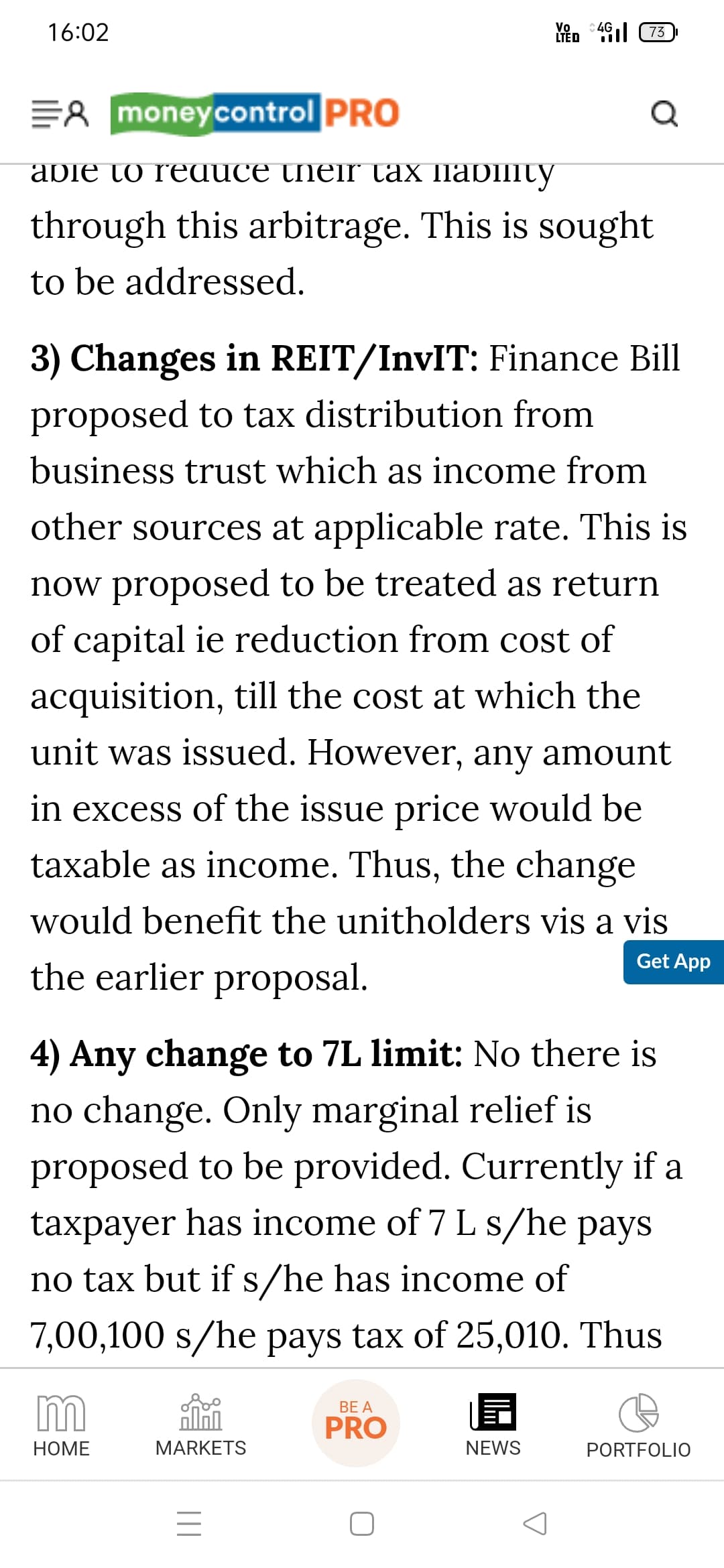

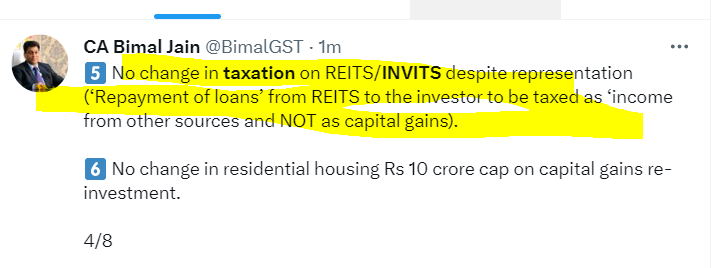

Finance Bill 2023 passed in Lok Sabha with THESE major amendments. Details here

A committee will be set up under Finance Secretary on the pension system to address the needs of employees and also maintain fiscal prudence, said FM Nirmala Sitharaman while proposing The Finance Bill 2023.

So basically no change to what was proposed earlier? Even if there is…as an individual investor tracking return of capital (on a qtrly distribution basis) above cost of acquisition will be mind jamming? How does one go about it?

This actually complicates the need of keeping track of reducing from cost of acquisition…it’s much more tedious…not the worth to have them as a retail investor

2 Likes

Above gives more clarity and seems this tax on Return of Capital may not be applicable for many years as none of the listed Reit/Invits have returned significant capital from their launch price and are unlikely to do same in coming 8-10 years.

7 Likes

Agree. While it might not have been articulated earlier, I am not sure how InvITs or REITs could have returned more than the original capital raised I.e. under “return of capital” category.

Thanks a lot Amit,

Quoting a para from the article: “If a REIT or InvIT had an issue price of ₹100 and in 2024, the amount distributed (as capital repayment) was ₹20, there will be no tax on this since it is lower than the issue price. If in future the trust’s cumulative distribution becomes ₹110, then ₹10 is taxed in the hands of the unitholder. If in the subsequent year the amount increases to ₹130, then tax will be on ₹20, since tax has already been paid on ₹10 in the previous year.”

What does cumulative mean? Is it cumulative sum of capital repayment since the year of listing >100 OR capital repayment in that standalone year only >100. I am assuming its the former (as it mentions the word cumulative). If that is the case wouldnt it reach threshold faster?

2 Likes

For embassy it pays ~10 RS per year as return of capital. It will take even considering increase in distribution later years multiple years atleast 10-15 yrs away coming in tax net. Embassy units were issued at 300 rs ,so calculate based on that.

With debt mfs coming in tax net suddenly this has again become best debt investment now with this change

1 Like

Conceptually complete Return of Capital will take a lot of time for many Invit/REIT. I am invested mostly in IRB Invit and that being first Invit launched in 2017.As on date it has Returned around Rs 20 from Rs 102 initial Book Value. Their current Toll concessions for one of their portfolio assets go upto Dec 2042 and so it will take at least 2042 for complete Return of Capital. The portion of this ROC will keep changing through years but still current investors can be assured that there will be a tax free distribution in each quarterly payout.

3 Likes

Thank you everyone for the amazing insights here. I still have another query here. If I have not acquired units at IPO price but have rather acquired them randomly post the IPO and let’s say that my avg buying price is ‘X’ which could be less or more than the IPO unit issue price, how then would this tax rule imply to me ?

1 Like

This has has become so complicated now to even think logically. How does IPO price matter? Should it not be your cost of acquisition of the unit? This looks not right coceptually.

Remember that the original finance bill had typos with mismatching FY and AY numbers. How can they have typos in such an important doc? After that, there was confusion on what was passed in the amended finance bill…I myself posted links of various twitter statements that said that the tax on RoC has not gone away…thank God…some sense seems to hv prevailed but the fine print is so awful that it will take a sum total of CA + lawyers + co secys to figure this out !! but for now, forget the tax on RoC and move on… we will wake up after a decade !!

4 Likes