I think point 3 can play out in India as well considering how many start-ups have popped up in India ,I don’t think embassy have full 100% A list tenants like Google and Amazon and even in these companies we are seeing downsizing.

1 Like

Yes, it may happen to some extent in small startups, but Embassy’s tenants are 81% international and 47 % of these are Fortune 500 companies (according to half yearly report). I don’t feel any major impact of small startups leaving having any material impact on the collections personally. As per the concall of all 3 reit’s new demand remains strong.

3 Likes

Fundamentally, I think that InvIt (Indigrid and Powergrid) may be better for getting more predictable returns given the business profile. REIT are more cyclical and there may be more variability in stock prices as compared to InvIt. So if we are looking to quasi debt (with increasing yield), I would prefer Invit. The structuring to make the dividends and other payouts taxfree is however important . This can be done quite simply by owing Invit in Wife/HUF account where the income is less than 5L/annum.

Regards,

Nikhil

5 Likes

The key IMHO with REITs (and even more so with INVITs) is the investment time horizon. When we buy a personal residential property (for investment or rental income purpose), we dont or cant monitor daily price movements (mainly because the market is illiquid and price transparency doesnt exist). Subconsciously we are tuned to a longer gestation period. The same needs to be applied to REITs. As long as there is comfort in the sponsor and REIT manager agency, ideally we should treat it the same way (ideal doesn’t exist though ![]()

6 Likes

InvIt’s downside to me seems to be the fact that there is no scope for capital appreciation.

In a low inflatn environment, ur point regarding capital appreciation is valid. In high inflation period, assets generating immediate cash flow will yield higher and vl thus be preferred over those where cashflows are in distant future

4 Likes

The capital appreciation comes from the growth in underlying assets in the INVIT portfolio. As more profitable and yield additive assets come in the portfolio the higher is the income potential

4 Likes

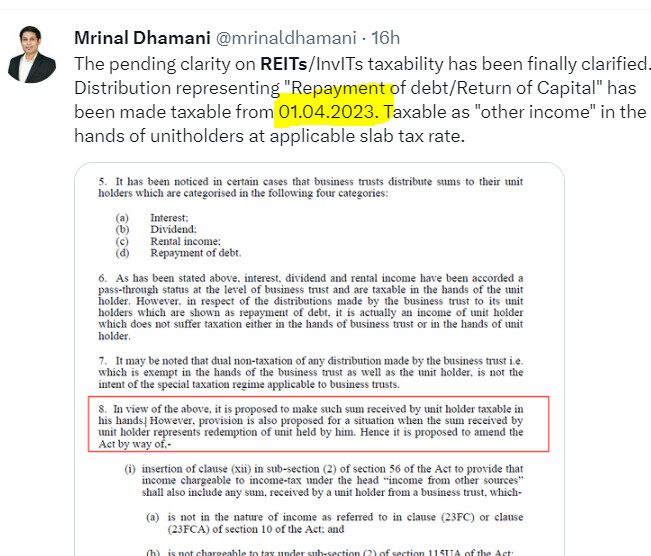

Embassy has been badly falling for the last few days and today, it fell to an intraday low of 315 (from a recent high of 342)… Here is the fine print in today’s budget that some of the biggies perhaps knew already and have been selling…

Budget fine print ![]()

Tax avoidance through distribution by business trusts to its unit holders

Finance (No.2) Act, 2014 introduced a special taxation regime for Real Estate Investment

Trust (REIT) and Infrastructure Investment Trust (InVIT) [commonly referred to as

business trusts]. The special regime was introduced in order to address the challenges of

financing and investment in infrastructure. The business trusts invest in special purpose

vehicles (SPV) through equity or debt instruments.

2. Keeping in mind the business structure, the special taxation regime under section

115UA of the Act, inter-alia, provides a pass-through status to business trusts in respect of

interest income, dividend income received by the business trust from a special purpose

vehicle in case of both REIT and InvIT and rental income in case of REIT. Such income is

taxable in the hands of the unit holders unless specifically exempted.

3. Sub-section (1) of section 115UA of the Act, inter-alia, provides any income

distributed by a business trust to its unit holders shall be deemed to be of the same nature

and in the same proportion in the hands of the unit holder as it had been received by the

business trust.

25

4. Further, Sub-section (3) of section 115UA of the Act, inter-alia, provides that if the

“distributed income” received by a unit holder from the business trust is of the nature as

referred to in clause (23FC) or clause (23FCA) of section 10 of the Act i.e., is either rental

income of the REIT or interest or dividend received by the business trust from the SPV,

then, such distributed income or part thereof shall be deemed to be income of such unit

holder.

5. It has been noticed in certain cases that business trusts distribute sums to their unit

holders which are categorised in the following four categories:

(a) Interest;

(b) Dividend;

(c) Rental income;

(d) Repayment of debt.

6. As has been stated above, interest, dividend and rental income have been accorded a

pass-through status at the level of business trust and are taxable in the hands of the unit

holder. However, in respect of the distributions made by the business trust to its unit

holders which are shown as repayment of debt, it is actually an income of unit holder

which does not suffer taxation either in the hands of business trust or in the hands of unit

holder.

7. It may be noted that dual non-taxation of any distribution made by the business trust i.e.

which is exempt in the hands of the business trust as well as the unit holder, is not the

intent of the special taxation regime applicable to business trusts.

8. In view of the above, it is proposed to make such sum received by unit holder taxable in

his hands. However, provision is also proposed for a situation when the sum received by

unit holder represents redemption of unit held by him. Hence it is proposed to amend the

Act by way of,-

(i) insertion of clause (xii) in sub-section (2) of section 56 of the Act to provide that

income chargeable to income-tax under the head “income from other sources”

shall also include any sum, received by a unit holder from a business trust, which-

(a) is not in the nature of income as referred to in clause (23FC) or clause

(23FCA) of section 10 of the Act; and

(b) is not chargeable to tax under sub-section (2) of section 115UA of the Act;

(ii) insertion of a proviso to the said clause to provide that where the sum received by

a unit holder from a business trust is for redemption of unit or units held by him,

the sum received shall be reduced by the cost of acquisition of the unit or units to

the extent such cost does not exceed the sum received;

(iii)insertion of sub-section (3A) in section 115UA of the Act to provide that the

provisions of sub - sections (1), (2) and (3) of this section, shall not apply in

respect of any sum, as referred to in clause (xii) of sub-section (2) of section 56 of

the Act, received by a unit holder from a business trust;

(iv) insertion of sub-clause (xviic) in clause (24) of section 2 of the Act to provide

that income shall include any sum referred to in clause (xii) of sub-section (2)

of section 56 of the Act.

9. These amendments will take effect from 1st April, 2024 and will accordingly apply to

assessment year 2024-25 and subsequent assessment years.

Discussion points

- In case of Embassy, the Dividend exempted and amortization amount will be under the tax scanner now…

- What does the fine print of effective from 1/April/2024 means but putting it as AY24-25 (which means FY23-24, which means, it kicks in from 1/april/2023)…which is a typo here? Knowing how these things usually work, they mean 1/April/2023, afterall ?..

No wonder, the biggies exited in time

8 Likes

If all distribution by reits and invits are taxable then no one will invest in these funds unless they have over 10% yield, it doesn’t make any sense…

3 Likes

Brookfield becomes 98% taxable

Embassy becomes 50% taxable

Mindspace remains 90%+ TaxFree

These are my Approx calculations based on historical distribution.

Please correct me if I am wrong.

5 Likes

I don’t think Dividends are still taxable… They are proposing to make only the “Amortization” component taxable… so Brookfield will also be approx 50% taxable just like embassy…

How can repayment of debt be taxable as income?

Lets say A borrows Rs 100 from B, and then pays back Rs 20 every year for 5 years. Is Rs 20 an income in the hands of B, who lent it out in the first place?

1 Like

Sadistic are the ways. It’s the way the bureaucracy thinks and acts in this country. Genuine money making is considered crime. Will they have guts to tax rich farmer ?

4 Likes

Was heavily invested in Embassy since IPO (added most qty in the pandemic) but sold off recently because of rising rates and Embassy Parent Corporate goverance issues.

But this is a ridiculous googly. Don’t think one can consider REITS and INVITS unless they are available at a deep discount. Tax arbitrage can disappear in the snap of a finger, MUST give a discount to that.

Now another bigger risk is - They may raise capital at current valuations to buy the chennai asset because of the Stress Level at the Embassy group.

4 Likes

REITs were big part of my portfolio since they simplify cash flows on real estate vs the hassle of managing and renting your own property out. But these tax googlies mean there is hardly any value in them over even debt instruments. For instance, pre-tax dividend yield of Embassy is around 5.5%. Post tax, its a terrible return.

There isnt enough trust in these instruments compared to developed markets, now with ever changing taxations its a hard sell. Even the CEO of Embassy Mr. Vikash has been selling his entire ESOP allotted units, every single year.

If the CEO doesnt have confidence to hold yield generating assets allotted to him every year, atleast for a short period, then I guess others should consider what that means

2 Likes

Divdend yield at current valuation is more then 6.5 % and out of this only 20% was taxable till now ,how did you come with the 5.5 % figure and that to pre tax?

-

These changes do affect retail holders negatively but it I think it does not affect mutual funds as it is a pass through for them and if a equity fund holds it it becomes LTCG

-

I am not too sure about this but the terms of the debt that the Trust gives to the SPVs can be changed such that there is lower repayment of SPV debt. Of course it will then show up in interest or some other category which is also taxable but if it is dividend it might be better off

1 Like