Since last 2-3 AGMs, the promoters have been giving your last bullet point reason as a reason for them not to go into natural food colours now. This is straight from the horse’s mouth but we can still check it through commentaries by Roha promoters if we are able to find it specific to food colours.

4 Likes

There have been issues in China w.r.t. food color intermediates. Refer extract from Sensient.

Similar to others in chemical industry, this is likely to give a China+1 tailwind. Looking for more evidence to corroborate this.

The same is corroborated here.

QUOTE

Prices of food colorants are determined mainly based on the criticality of raw materials, H Acid, Vinyl Sulphone, and Dye intermediates. Cost compositions of these chemicals are high, which, in turn, impacts the commodity.

Market Situation of Key Raw Materials and Then Impact on Door Dye Market

Vinyl Sulphone

-

Vinyl Sulphone is very important chemical in the process of food chemicals. Supply of Vinyl Sulphone has impacted the dye market many times

Current Market Situation -

The market is tight with less supply and high demand. China Vinyl Sulphone production is impacted to pollution control. India produces approximately 55,000 MT of Vinyl Sulphone per year. Other major producers are from Korea, Taiwan, Indonesia, and Thailand

-

During 2017, shutdown of one of the largest producers of Vinyl Sulphone in China, Hubei Chuyuan, due to environmental issues had resulted in spike in prices

H Acid -

H Acid is a critical raw material both by value and volume in the dye production

Current Market Situation -

H Acid is one of the most impacted chemical, due to the pollution control measures across the globe. Shortage of H acid was the major reason for the increase of dye prices in the past

-

Supply for H acid was very tight until Q1 2018. Though the supply has eased marginally after Q1 2018, the market still remains tight

Dye Intermediates -

The global dye intermediates production is about 17,50,000–18,00,000 MT/year. 70% of the supply comes from China, 15% from India, and the rest by countries, like Korea, Taiwan, and others

Current Market Situation -

Due to pollution control measures, operating rates of dye intermediate producers in China are impacted, which, in turn, has impacted the global supply. Dye producers in the US, Europe were impacted, due to the supply breakdown in China. However, Indian food dye industry had the least impact compared to other regions, due to the integrated production setups and availability of domestic supply

UNQUOTE

Source: https://www.beroeinc.com/category-intelligence/synthetic-food-colorants-market/

Saloni: Can you you dig the list of intermediates from the EC?

7 Likes

For what its worth, I did a quick check. Vinyl Sulphone is NOT on Dynemic Production/Consumption list in EC doc. H-Acid is - On the Raw Material Consumption List.

27122017XGCW8P4BAnnexure-documentofRiskAssessment.pdf (1.6 MB)

This 2018 data on Vinyl Sulphone, H Acid shortages in Food Color Dye intermediates may or may not be relevant now, depending on new capacities that might have come on stream. For a quicker grip on (any) current shortage list - we can ask the domain experts.

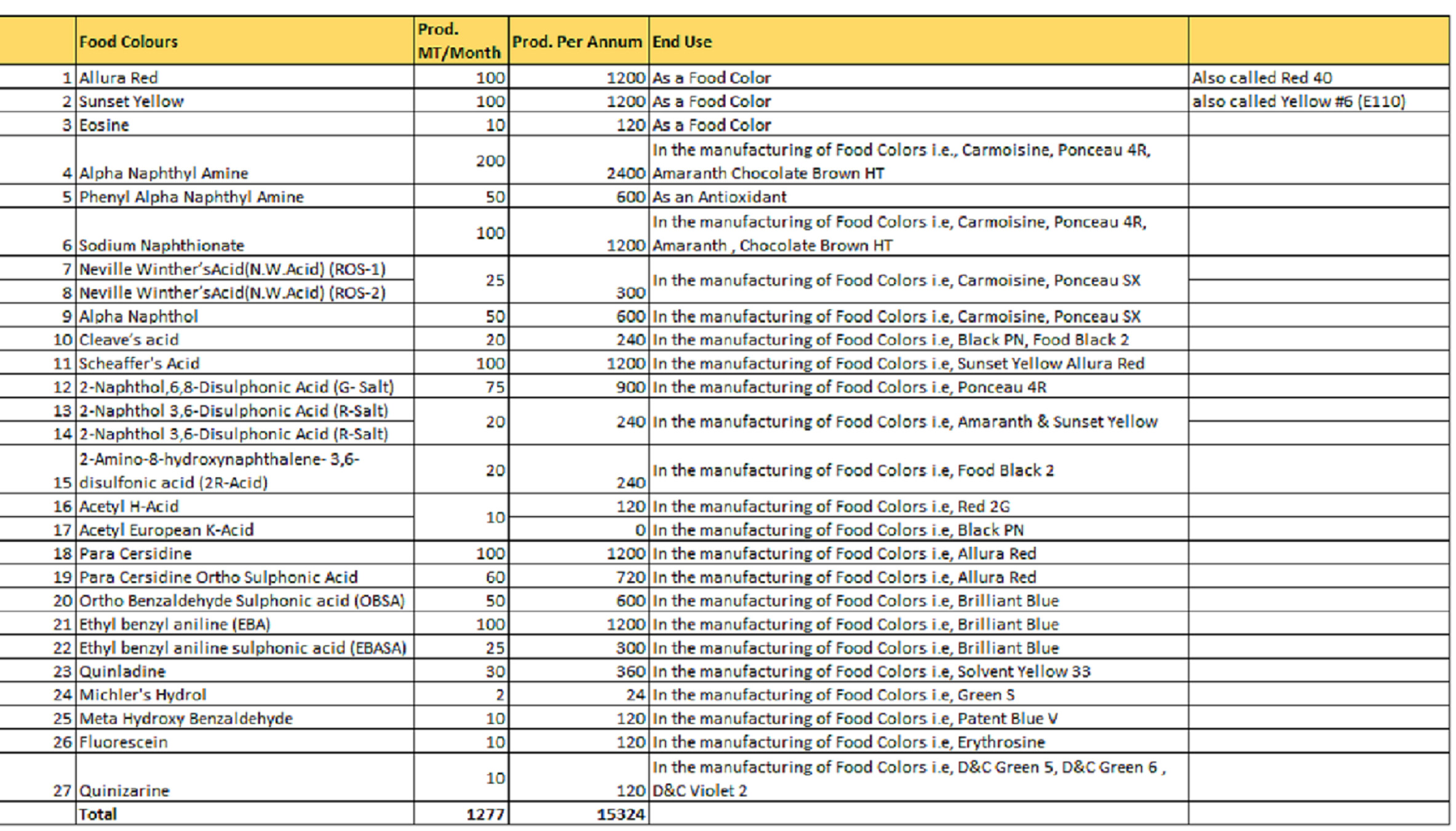

Dynemic Dye Intermediates (from current website). EC doc (above) will have the updated list.

From a quick scan, of 42 (27+15) products listed, 38 relate to food colours and intermediates (end use clearly outlined). 1 antioxidant for food colour use, and rest 3 are

Human & Vet APIs

- Oxyclozanide - cattle, sheep, goats

- Chlorozoxazone - muscle relaxant (human)

- Chlorhexidine - topical antiseptic

Let’s get back to identifying the “Gaps” in the story put up so far - that we want validated through scuttlebutt with domain experts.

- Critical Raw Materials supply chain - is one good addition. Thanks Yachna

Disclosure: Not Invested

7 Likes

As seen in the qty of each intermediate, the company is heavily into Red 40 and Sunset Yellow and Brilliant as these are the most in-demand (higher volume) products in food colours.

The company is planning to export around 50 tons/month of Red 40 in the US. US market size of Red 40 is 500 tons/month.

14 Likes

Small contribution to the deep dive exercise:

To get a sense of the past behaviour of the management - went through past annual reports FY11 to FY15 of Dynemic Products. Detailed findings in the attached files.

Sharing my thoughts while glancing at the past annual reports, my views are basic since I don’t have a detailed understanding of the space, hopefully other collaborators can chip in with a current perspective.

Brief key takeways of past annual reports (FY11 – FY15)

- Credit rating withdrawn recently, since they did not co-operate on info (First rated in FY13 and was assigned BBB/Stable rating)

- Unable to understand their MEE (Multiple Effect Evaporator) plant opex costs which impacted margins in at least 2 years sharply

- Their disclosures have reduced in FY15, vs earlier years… they provided production nos, power costs etc. Maybe it was not mandatory to disclose details in Form A subsequently.

- Some speculative investments in the past, by buying HDIL, Rel Comm etc – Unrealised losses of Rs 20 to Rs 35 lakhs in FY11/FY12 which is sizeable on their then profits of Rs 8 cr

- FY14: Board approved variable compensation pay of 2% of net profits to Shri Bhagwandas K. Patel

- Promoters have distinct responsibilities – Shri Bhagwandas K. Patel (administrative & finance), Shri Rameshbhai B. Patel (production/R&D of Unit I Ankleshwar), Shri Dashrathbhai P. Patel (total production, R&D of Unit II, Ankleshwar).

- 13-14% of Raw materials were imported; power costs are significant and key costs to monitor in the manufacturing process

Positives

- Related party transactions are not significant

- Prudent capital structure (However, MEE plant capex has been unable to improve pricing power for the company in FY12 and FY13.)

PS: Not invested, discount my views accordingly.

Dynemic Products - AR.docx (812.0 KB) Dynemic Products - Excel.xlsx (41.1 KB)

25 Likes

On the MEE Plant aspect, I believe the comments made in AR over the years would help:

2012: “Dynemic had delivered sustained growth in generating total revenue with an increase by Rs. 18 crores, a growth by 27% in comparison to the previous year. But in comparison, net profit has been negatively impacted by Rs. 42 lacs, a decrease of 7% than the previous year. This negative impact on net profits is largely attributable to the MEE plant, which has incurred Rs. 4.5 crores on working capital and Rs. 3.8 crores on fixed assets which is a step ahead for pollution control.”

2013: "Though the revenue are higher by 4% but the net profits in comparison to last year are down by 18%. This impact as last year informed is largely attributed to MEE plant, which has incurred Rs. 4.57 crores on WC this year and Rs. 47 lacs on fixed assets which is a step ahead for pollution control and GPCB norms.

As you know our industry is pollution prone and for that, we had installed MEE for treating the effluent generated by both units as per GPCB norms. This year due to MEE, we had incurred Rs. 4.57 crores on working capital and Rs. 47 lacs on fixed assets. We are facing stiff competition in the market with other competitors who are not required or are not treating their effluent themselves. This year our turnover had raised by 4 % then also our Net Profit after taxes had decreased by 18% due to MEE plant."

2014: “Dynemic had installed Multiple Effect Evaporator Plant (MEE) in both the units which had incurred capital cost of around Rs. 28 Lacs this year. This plant recycles maximum water waste which could be used again in the process. The working cost of this plant for both the units, for a whole year had incurred Rs. 4.60 crores which were 4.57 crores last year.”

These costs accounted for 4-5% of sales of these 3 years.

24 Likes

Synthetic Food Colour Discussion: Scuttlebutt #1

Anyone having friend (of friends) connect in the Food Colours Industry, please help us conduct more such scuttlebutts to learn progressively from the domain experts. Do drop a line to @salonihemnani011 @YachnaBhatia, @Donald, @ankitgupta

33 Likes

Scuttlebutt #2:

With Synthetic/Natural Colours Industry Source

-

There is so much hype & hoopla around the Natural vs Synthetic Food Colour debate. If one were to read up/educate oneself from the literature available, one might be excused if he/she thinks the synthetic food colour market is already gone, it’s a dying industry; yet we instinctively know that in developing economies like India, all-natural-coloured foods is still a very distant dream. As for the natural colour additives products, even there we hear its actually a hybrid, small amount of Synthetics are added to stabilise, add vibrancy, and reduce costs (self-defeating, a newcomer to this industry like me, would observe). Great if you could start from there.

Currently Indian Regulator FSSAI allows a few Synthetic Colours with usually 100 ppm in Food items. More than 100 ppm is considered harmful, and not allowed. Some details here. This is backed by research on harmful effects with higher dosages and different countries have come up with their own regulations around the same. US FDA allows some of these colours FD&C Blue No. 1 (Brilliant Blue FCF), FD&C Blue No. 2 (Indigotine), FD&C Green No. 3 (Fast Green FCF), FD&C Red No. 3 (Erythrosine), FD&C Yellow No. 5 (Tartrazine), and FD&C Yellow No. 6 (Sunset Yellow). Complete List and Food Colours Additives History is here. -

Natural Colours from plant sources/vegetable origin are usually not considered harmful as they are from natural sources.

-

Now if we take the case of a Cake, 100 ppm synthetic colours may not be enough. For the right colour stability & vibrancy maybe 500 to 600 ppm is required. So what is done is one can add 1 to 1.5% Natural Colours in addition to 100 ppm Synthetic. By a judicious mix of Natural with Synthetic, the manufacturer saves some amount on costs and also allows him branding options. This will never be mass market products. Maybe marketed for niche segment – maybe say targeted at children.

-

How are the cost structures in Synthetic vs Natural Colours?

There is big cost differential for use of synthetic colours vs natural colours. It might be 50 paise to 1 Rupee of Synthetic Colours per Kg in a food item. To match the same shade as produced by Synthetic colours, the spend will be 5Rs or 10Rs for Natural Colours per kg of same food item. Also there is a big lead time taken (lots of trials) to get the correct match in colour shade/vibrancy – 6 months to 1 year depending on the kind of product. -

What’s the right way to segment this market? While big brands may be able to afford using Natural colours in premium products, is it a fair argument that this is not yet feasible for mass-market products?

The trend worldwide is to move towards natural colours as it is the healthier option. The transition will take its time. Just like in the case of Fruits and Vegetables – the trend in Metro Markets may be more towards Organic, same way for Food Colour Additives. The customer in Metro markets may start expecting Natural Colours – all Clean Labels, and stuff like that. -

Synthetic Colours Market is still there – it’s not going away in a hurry or vanishing. It is still growing. Let’s take the case of Vanilla flavour – the premium Vanilla will available at 1000 Rs/Kg and it is also available at Rs 100 per kg. Now a Britannia or a Cadbury or a General Mills may be using the premium very good quality flavour for its premium products. But the 100 Rs/kg flavour product will go only in distributor/retail market and serve rural/mass market segment. That is just like Essence, not even a Flavour.

-

The use of Synthetic or Natural today is to a large extent dependent on the Market addressed. And what kind of Margins you hope to make. Rural/Mass Market will primarily be synthetic. Metro and Tier II city customers can afford Natural food colour additive products. Natural Colors use is 4-5x costlier than Synthetic, but allows different branding options/perception setting for manufacturers.

-

Of late, last 8-10 years there is growing inclination for Natural colours. So let’s look at Bakery/Confectionery segment there will be 10s of products; However as we know for Cake in the market - sold at Rs 20, there will be at least 10 selling at Rs 20-25; So the restriction for competitors is to play within that range; Patanjali can sell plus or minus Rs 5; but someone cannot come and sell another similar cake at a Rs 20-50 premium. That luxury does not exist. But in Metro Markets Big MNC premium brand customers might be willing to pay Rs 20-30 more for the same kind of cake for (more) natural and slowly they want to go all natural.

-

So what’s the current market share between Naturals & Synthetics in India? Is it 50-50 already, or?

Significant market for synthetic colours is existing on a very large scale; transition is happening yes, but synthetic will dominate for some more time. 60-70% mass market products like Candy, cakes, beverages will still use synthetic; rural or slightly above rural market products – because of the nature of the market; Metro market has higher awareness, so there is scope for newer niche products/brand pushes towards more natural or all natural. It’s a slow transition today in tandem with customer awareness, and regulations. -

What are the challenges for the Synthetic Industry in coming years?

Synthetic Colour manufacturers in India do run the risk though of running into stiffer Regulations. For Example Tatrazine (not allowed in Middle East), Ponceu 4R, Carmoisine, and Allura Red may see restrictions at some time in the future (based on new research evidence and proactive action by Regulators in India and US or EU). Or if say FSSAI revises the new guidelines to 50 ppm instead of 100 ppm – something that forces the hand of manufacturers, the trend could accelerate. -

How does a Core brand decision get taken – let’s say for something like a Good Day for Britannia?

If for some unavoidable reason, they do have to make changes then they will think 10 times before touching that brand, and will treat very carefully with alternate application solution trials – to make sure the exact taste and colour match is provided what the customer is used to. Lots of deliberations, lots of planned execution, make sure that the actual consumer hardly notices any difference; this is from the manufacturer’s perspective. But if we see it from the customer’s perspective - whatever change happens with “Goodday” biscuit – the extent of faith in brand Goodday - in rural markets - stays; won’t impact his thinking or consumer won’t even come to know if minor changes have happened; he might take it as a good change. Core competency of exact matching comes from natural colours solution providers R&D, while Britannia, General Mills or Cadbury or ITC R&D Labs are continuously carrying out such trials too, for different products. -

What drives the decision-making for shift to Naturals?

For newer products – decision making comes from 3-4 different inputs. 30-40% weightage is based on current research and solutions available; and 50-60% weightage is from what is the prevalent notion in the relevant market. For example just like in Fruits and Vegetables more and more customers are expecting things to move away to more organic products, in the same way Metro customers will start expecting more and more clean label solutions with more naturals. -

Please give us an idea on the consumption by major segments like Bakeries, Confectionery, Beverages, Pharma

Bakery has highest consumption – cakes & creams; Second is spirits with 8-12 % alcohol content, vodka, gin, flavoured beers, or mocktails and cocktails - preference is for natural; metro city consumption people are ready to shell out money for premium products; Confectioneries candy, toffies - use lot of synthetic; for the same 200-300 Rs per kg for mass market MNC Colour manufacturers won’t have competitive product solutions; Beverages dairy, breweries, distilleries, fruit beverages, carbonated, - second highest consumption; Sweets market - huge market - only a few enquiries - they want more margins – transition is happening very very slowly ; rest is pharma, others. -

What is the conversion rate currently for the main segments?

The beverages segment has largely gone all natural. Usage of Natural colours in Indian traditional sweets is very very minimal. Even reputed sweets brands in Metro markets - very sure they are using synthetic colours; Traditional family owned businesses typically don’t want to get into these issues only; 2013 raids happened in many sweet houses; Now if you ask them, they say they don’t even use any colours; which is a complete lie. Bakeries & Confectioneries market is still dominated by Synthetic colours. -

Given that Synthetic is still a big market, why are MNCs vacating?

MNC companies have limited products today in Synthetic. 10-20 products in synthetic to offer – permitted to use only 100 ppm; actually usage is 600 to 800 ppm by many manufacturers; Very difficult market at 200-300/kg of colour; Imagine the food manufacturer may be making tons and tons of products using synthetic colours; So MNC manufacturers are gradually moving away from serving synthetic markets in any major way -

With Multinationals vacating the Synthetic market, is it now a much greater opportunity for existing Indian Synthetic majors?

Roha is among the good ethical players. Local players are cheating – they are providing adulterated products – much in excess of allowed limits; with more awareness customers will switch to organised synthetic players who are reputed to be ethical and offering solutions within FSSAI prescribed limits. Sensient, CHR Hansen, ADM Foods - instead of selling 100 kg Synthetic Colour, prefer selling 10 kg Natural colour – first it’s about serving the market ethically & legally, and then it’s also all about Revenues/Margins. -

10s and 100s of products using exhorbitant limits of synthetic colours or even outright banned colours; something that you are doing that is not being caught – doesn’t mean it is legal; A good example is usage of Mica – provides sparkling finish in colours; go to any smaller market - one will find many many products manufactured with Mica as a colour additive.

-

Any comments on India based major players on this ethical/legal front?

Neelikon - is a brand of Roha; Vidhi and Dynemic - if exporting in large quantities - might be adhering to prescribed standards. -

How easy or difficult is it to convert a customer to all Naturals or More Naturals?

Development of any application using Natural Colours is time consuming; Skill or development not that difficult as we have competencies; Challenging in terms of cost in use - few paise or 1 re for 1 kg; at least 5-6 times to 10x cost in use for natural colours; And convincing their own customers is an ask; Any project takes 6 months to 1 year to 2 years even; Vendor and Customers have good R&D set up for trials. But it’s NEVER easy. As we know Natural colours have stability issues, demanding formulation parameters, packaging and stored conditions issues; Recommended to store in cold or refrigerated conditions; because of all that it takes more development time. -

How easy is it for someone like say Roha to shift to Naturals?

Well Roha has natural colours segment also; they have Experts in Natural colours; they are selling both natural and synthetic colours; someone only in synthetic colours, to move into natural colours it will be very very difficult; It takes years and years of expertise. So someone proficient in Synthetic only, will stay in Synthetic; someone who knows about Colours market will today choose Natural segment; Those in Naturals will not shift to Synthetic – that’s how the pecking order remains. -

Why an existing Synthetic Player can’t just hire 3-4 key people and start supplying Natural Colours?

a) natural Raw material sourcing - is a herculean task

b) consumption forecast/transportation not so easy - because of covid -additional complications - much is imported too

c) gaining the confidence of the customers is not easy - market share or image exists; walking into any Cadbury, Britannia, ITC office a new player offering 50% discounted – will not be taken seriously or entertained; Food Colours can easily get into controversy; big customers won’t want to risk -

How about the Flavours Industry? Similar Issues/Challenges?

In Flavours there are 200-300 players totally. Natural flavours are way more complicated to handle than natural colours; We have lots of restrictions, limited products; minimum order quantity, pricing will be very very high, so uncompetitive -

In a nutshell again Synthetic market is not going away in next 5-10 years, it’s very much there. Someone like Roha is well-hedged because they are doing both Synthetic and Natural. Others only into Synthetic carry some risk with respect to future business continuity.

Disc: Not Invested

46 Likes

Dynemic_Intermediates_Competition.xlsx (57.4 KB)

[Filter used: >=50T/month production, from EC doc]

Time for Scuttlebutt #3

Time to get focused on understanding Dynemic Intermediates manufacturing strategy/Mgmt Claims

(40% Captive, 60% outside Sales in India)

a) Import substitution

b) Largely Intermediate outside Sales will be to non-food industries like Textile, Pharma

c) Lots of small manufacturers making each of the Intermediates

Grateful if anyone of you can put us in touch with a Dye Intermediates domain expert ![]()

Please drop a line to @salonihemnani011 @Donald @ankitgupta

Sustainability beyond immediate up cycle (China pollution curbs led?) is the major risk we can see as 60% is outside sales plan, despite entrenched competition. Good thing is they are taking baby steps in the direction of value migration that much bigger scale businesses like Atul, Aarti Industries have walked (as you can see in the Excel). Perhaps Management is ultra conservative and likes to underplay (unlike say Vidhi).

Heard from friends who have met Management - they have scotched all plans of Natural Colours move. They are happy to scale up on the current Synthetic Food Colours. So now looks like the bet might be equally ON the Synthetic Intermediates Industry - which from the looks of it, is certainly NOT an Oligopoly (Food Colours is safe/protected Turf). They are venturing into a much more competitive market - at the right time perhaps in the up cycle, yes, but after?

8 Likes

Although the mgmt’s focus is backward integration, there is a risk for leftover intermediate capacity. This is one of the questions I want to ask the management is what is their plan to mitigate this -

-

Do they see themselves increasing more FC capacity post-expansion (logically shouldn’t be soon since this is debt-driven and payback needs to happen)

-

If not, how do they see themselves protecting the margin profile if the intermediates cycle turns against them?

3 Likes

The way I see it, yes

a) I see the 60% excess capacity in a much more competitive industry as a red flag (strategic mgmt thinking) till the time we can get more insights as to why this may still work (because the ground realities are x,y,z say)

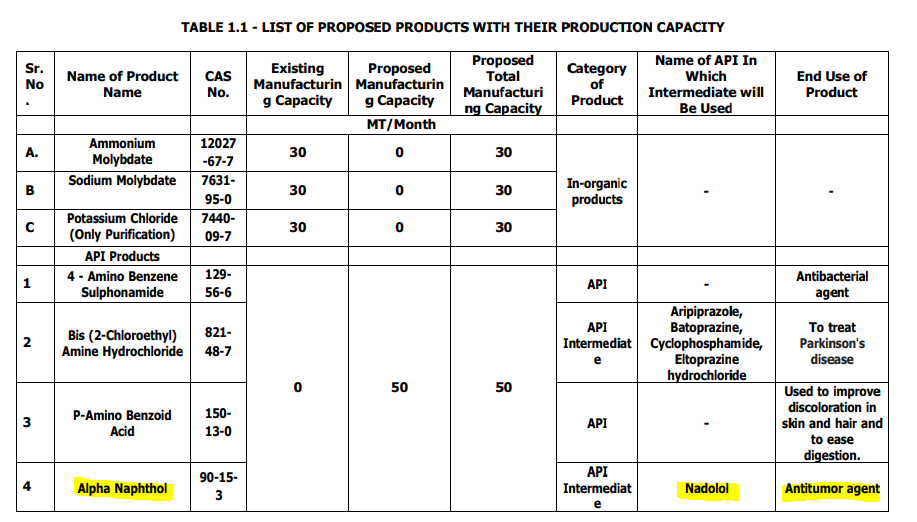

b) The limited pharma intermediates and pharma API plans (only in EC doc, don’t know if they will proceed) these are actually good signs for me to see - implies they are thinking about value migration

There is a player called Chandan Intermediates which is supplying the same Alpha Napthyl Amine and Alpha Napthol in pure refined pharma grade applications. So yes, there are very interesting possibilities from many of these intermediates. Whether they have acquired the skills to deliver on such fronts, only time will tell - but I guess now we are better equipped to quiz Management on value migration possibilities.

We might be aware that Ramesh bhai may be bringing in the required pharma expertise in the company. Managing Director at Ratnamani Bio-Chemicals And Pharmaceuticals Pvt.Ltd, and Production Head, Ankleshwar for Dynemic

https://www.linkedin.com/in/ramesh-patel-12774340/

[thanks to @RamanTiwari for alerting on this expertise within Management]

8 Likes

Totally 60-65 companies.

Only 8 Indian companies requesting/received US FDA Food Colour Certification within last 2 years

| 1 | Ajanta Chemical Industries |

|---|---|

| 2 | Dynemic Products Ltd. |

| 3 | Koel Colours Private Ltd. |

| 4 | Neelikon Food Dyes & Chemicals Ltd. |

| 5 | Roha Dyechem Pvt. Ltd. |

| 6 | Sudarshan Chemical Industries Ltd. |

| 7 | Sun Food Tech |

| 8 | Vidhi Dyestuffs Mfg. Ltd. |

17 Likes

I guess Krishna industries and shree krupa salespvt. ltd. have been removed.

Koel Colours Private Ltd.- product profile doesn’t include food colour…more cosmetic and pharma (Lake colours more) and pigments like ultramarine colours

7 Likes

Building on the thoughts and questions raised by the collaborators.

How much will Dynemic be backwardly integrated after this expansion?

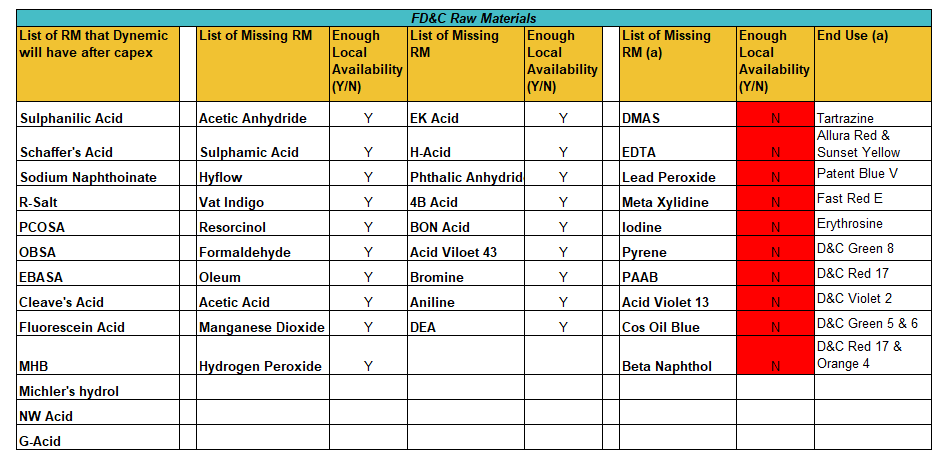

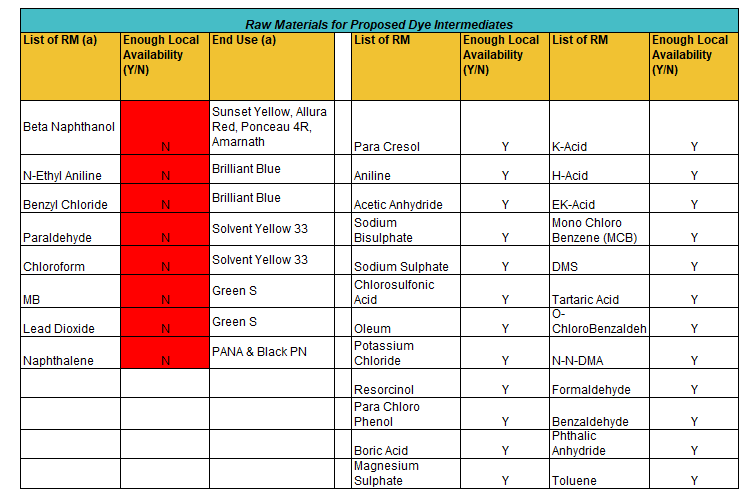

I went to the website and listed down all the food and D&C (FD&C) colours they manufacture. From Dynemic’s, Neelikon’s, and Vidhis’ recent EC filings, I listed the RMs required to manufacture each of these FD&C colours. Here are some of my findings-

- There are some very common RMs like Carbon, Sulphuric Acid, Ice, Sodium Chloride, Sodium Nitrite, Soda Ash, Hydrochloric Acid, etc that are used in all these FD&C colours and can be easily sourced domestically.

- Each FD&C Colour has its own uniqueness and requires some unique RM(s). In total, there are ~45 such unique RMs. There are around 30 RMs that are missing and Dynemic would still have to procure.

From what I could gather till now, Dynemic has very strategically done backward integration in those molecules where a lot of domestic players are not present and has left those chemicals where there is enough domestic presence. There are a few high chemistry molecules which either have no domestic players or very few present, and hence, will have to be imported. The chart below does not have the common RMs.

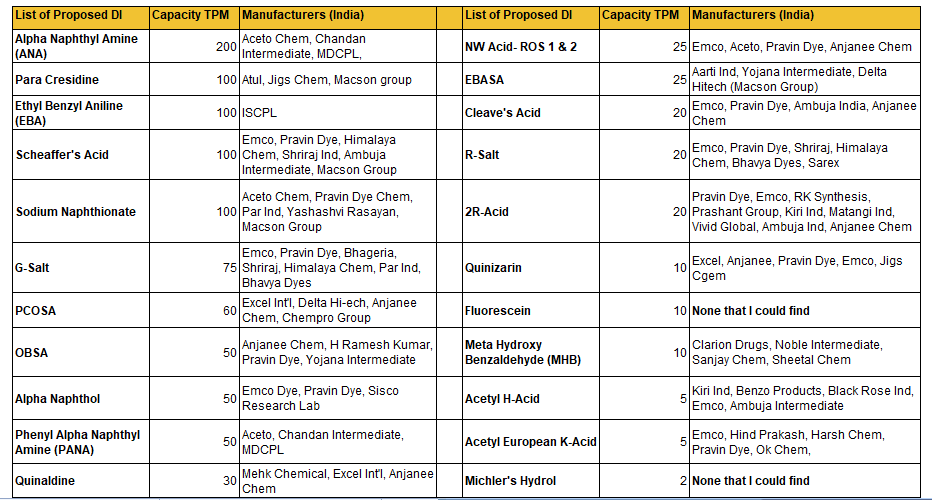

Since 60% of the Dye Intermediates (DI) will be sold commercially, what is the competition like in the Dye Intermediates Dynemic has proposed to manufacture?

There are 22 DIs that Dynemic has proposed to manufacture. What is interesting to notice is that most of these DIs have only 4-5 credible domestic manufacturers and only a few companies manufacture more than 4-5 DIs from this list. I could not find any listed player that is manufacturing even 3-4 DIs that Dynemic has proposed. Some companies that manufacture more than 5 DIs that Dynemic has proposed are- Emco Dyestuff, Pravin Dye, Macson Colour, Anjanee Chem, Excel International, Ambuja Intermediates, Shriraj Ind, and Himalaya Chem.

I urge valuepickr members to tap into their network and see if we have friends and family in these companies so we can understand the Dye Intermediate industry better as this will be a major growth factor going ahead.

Are the proposed Dye Intermediates commodity in nature?

We have already established that there is limited competition in a lot of the DIs proposed by Dynemic. Let’s have a look at what’s the nature of some of these DIs.

-

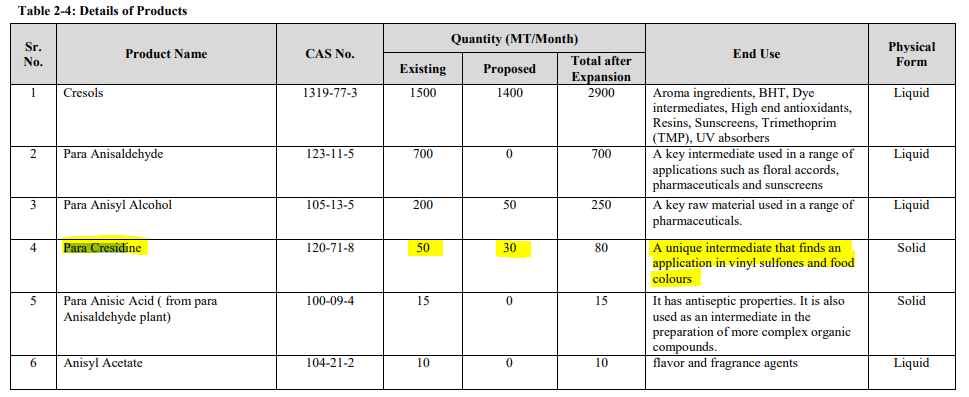

Para Cresidine- From Atul’s EC filing-

-

-

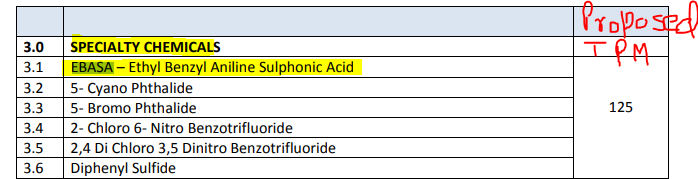

EBASA- V India Chemcical’s EC Filing

-

EBASA- V India Chemcical’s EC Filing

-

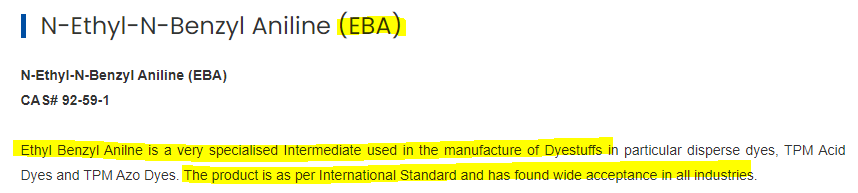

EBA- ISCPL is one of the only credible manufacturers of EBA. A snapshot from its website.

-

Alpha Naphthol- Again, there are very few companies producing this and it has a varied application.

- There are multiple DIs whose proposed quantities are small like PANA, Quinaldine, NW Acid, Cleave’s Acid, Quinizarine but have very limited players present in the domestic market. We need to establish how specialised these are.

What about the RM that will be required for the manufacturing of Dye Intermediate proposed?

Dynemic is doing backward integration but will require RM to manufacture those dye intermediates. Dynemic’s EC document has mentioned the RM required to manufacture each of these DIs. I listed the RMs required to manufacture each of these DIs. Here are some key highlights-

- Here again, there are some common RMs like ODCB, Soda Ash, Catalyst, Sulphuric Acid, Caustic Lye, HCL, Nitric Acid. These can be easily sourced domestically.

- Each DI requires a different set of RMs and in total there around 30 such RMs. Out of these, around 20 can be easily sourced domestically. There are no or very few domestic manufacturers for the remaining. I have skipped the common RMs in the chart below.

Conclusion:

-

Dynemic has very strategically done capex into RMs that can’t be easily sourced domestically (apart from a few) and has left out others where there are plenty of domestic manufacturers.

-

Dynemic will not be 100% backward integrated. They will still need to procure a few Dye Intermediates and RM to manufacture proposed Dye Intermediates but most of these RMs are easily available domestically.

-

Dynemic will still have to import certain RM but that is now very small in number. Some key RMs that will still need to be imported are- Naphthalene, Beta Naphthanol, Paraldehyde, Lead Dioxide, DMAS, PAAB, Meta Xylidine, EDTA etc.

-

60% of the Dye Intermediate capacity will be sold commercially. Most of these DIs (>70% of proposed 12,800 MTPA) are manufactured by only 4-5 other companies. Some of them have been categorised as specialty chemicals by the players already manufacturing it. We need to establish if there is enough demand for these DIs and if they have applications other than FD&C colours then Dynemic won’t find it difficult to sell these since many of these will be import substitutes.

-

Dynemic has proposed to manufacture certain chemicals like- ANA, EBA, Para Cresidine, and Quinaldine, that don’t go directly into making food colours but are RM for manufacturing Dye Intermediates.There are very limited players manufacturing these in India.These form around 40% of the total 12,800 MTPA proposed DI capacity. Then there are products like Michler’s Hydrol and Fluorescein for which I could not find any credible domestic manufacturers.

-

There are some ECs that I could find by companies like Macson Group and Paraswanath Intermediates that are coming up with capacity in the dye intermediate space and have some common products that Dynemic has also proposed. Sign of rising demand?

Further course of action-

- Get in touch with a dye intermediate industry expert and figure out what the demand and market is like for the proposed DIs that have limited domestic competition.

- Collect Import data for the proposed DIs. Could use some help here from the data experts.

- I plan to do a similar exercise for their proposed Bulk Drug and Intermediates.

I am attaching the raw excel sheet which was used to create these tables.Dynemic Intermediate (1).xlsx (63.7 KB)

Disclosure: Invested.

51 Likes

Company Announcement - “Trial run for Food colors Plant at its manufacturing

unit situated in Dahej, Gujarat from 07.06.2021. Also, we will update the commencement of

commercial production in due course.”

According to me, the capex has crossed Rs. 210-213 crs. Need some clarity on the reasons behind the increase and is it a hole in the pocket due to some cost overruns or is it going to contribute to the topline?

21 Likes

Would be great if anyone have info on below

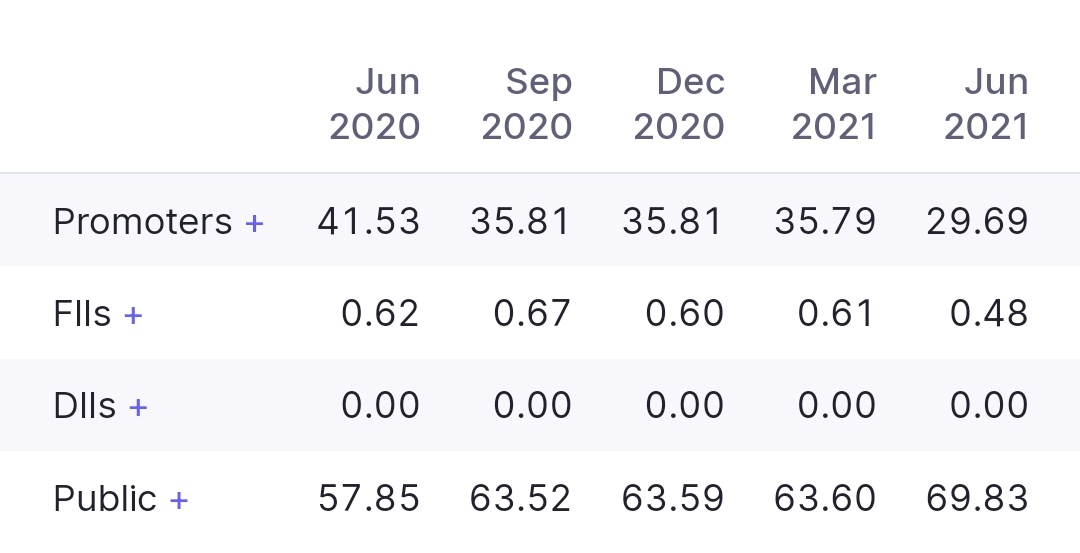

- Does anyone have information in the promoter % decreasing again…needs to be concerned?

2)what is the status of Capex?

If you just read the notes and content shared in the thread above, it has all the answers - one promoter has moved to non-promoter category.

Capex - New Food colours plant started 5th July

Dye intermediaries - To start very soon

(Source - Annual Report)

9 Likes

Dynemic FY21 AGM Notes:

- We have already started Food colour production.

- Dye intermediates expected to start by next qtr.

- Total Capex incurred – 210 crores. Addition in capacity post revised capex is only done in FC. (Earlier estimated addition was 2,520 MT. Actual has been 2,760 MT). Rest everything has been due to cost overrun and delays.

- Earlier there were 3 plants planned. Addition has been plant 4.

- FY22 Estimates - Sales - 265 cr, EBITDA - 51-55 cr, PBT - 33 cr

- FY23 Estimates - EBITDA – 110 crores, 20% + /- margins

- Total Revenue from Dahej - 58 cr for FY22, 330 cr FY22-23 (not additional)

- Total Revenue for FY23 – 550 cr

- Peak Revenue – 650 cr definitely but beyond that depends on market

- We do not foresee any major risk and expect smooth operations

- Dahej plant – peak revenue to be achieved by FY24-25.

- FY22 – CU – 40-45%

- FY23 – CU – 75-80%

- FY24 – CU – 80-85%

- FY25 – CU – 85-90%

- PEAK REVENUE - Revenue – 207-210 cr from Ankleshwar, 38 cr Profit from Ankleshwar. Dahej: 400-450 cr excluding captive consumption

- Products manufactured in Dahej for backward integration will improve the margins

- Interest impact - 1.8 cr on term loans 1.5 cr on WC loans Qtrly for FY21-22

- Depreciation impact - 3.6 cr Qtrly impact

- Debt repayment – FY25-26 to repay the entire debt. 60-65 cr repayment within 3 years.

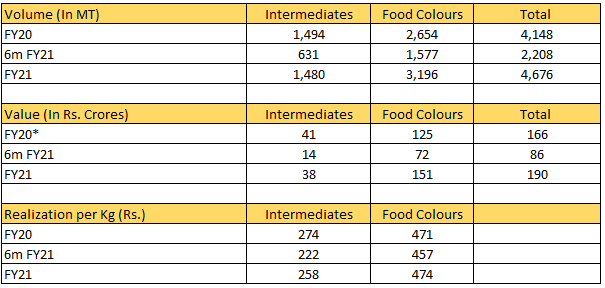

- FY21 Production - 3095 MT FC, 3303 MT Dye intermediate.

- FY21 Sales Volume - 3196 MT FC, 1480 MT for Dye intermediate

- FC existing capacity – 3067 MT. Additional – 2760 MT. Total FC capacity 5,827 MT

- Overall cost overrun is 45 cr – land, building and machinery.

- 60% space in Dahej currently utilized. Balance 40% space in Dahej unutilized for future capex.

- Interest cost 9 cr and Depreciation 18 crores for FY22.

- Interest cost 13 cr and Depreciation 13 crores for FY23.

- Capacity utilization for Q1 FY22 – 82%, FY21 - 87%.

- Do not foresee any pricing pressures.

- Dye intermediates made are value-added in nature. They are not commoditized. Our intermediates are import substitutes of China. Dye intermediates that we are planning to make does not have much competition. Atul is a competitor in this segment.

- Our existing capacity of Allura and Sunset was too small in front of demand. That’s why these FC products were planned.

- Main market is synthetic food colours. Due to pollution, US and other players don’t want to make it themselves. They would rather source it from India.

- When asked about the reason behind cost difference between capex of Dynemic and Vidhi. Management’s comment – “Abhi joh vidhi ne estimated cost bataye hai, sir unhone plant start nhi kiya hai abhi, jab plant start karege aur jab aayege, toh aap dekhna ki estimated cost kya aati hai. These are estimated costs.”

- Additional plant has been set up as well.

- We have already planned for IR.

66 Likes